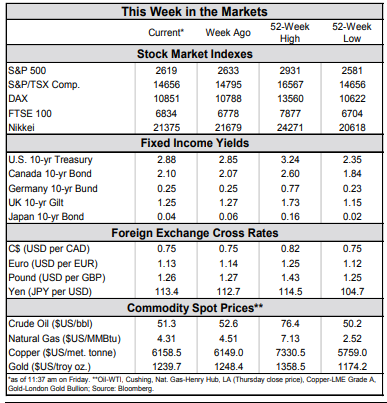

Financial News for the Week of December 14, 2018

HIGHLIGHTS OF THE WEEK

- After some optimism early in the week, financial market sentiment soured as focus shifted back to fears of an escalation in trade tensions, Brexit uncertainty, and a potential economic downturn in 2019.

- The U.S. consumer remained unbowed in November, with consumer spending now tracking above 3% annualized in Q4. Inflation has cooled in line with oil prices, which should help to support real spending going forward.

- The FOMC makes its final decision of 2019 next week, and a hike is universally expected. We will be watching closely to see how members’ views have changed about how many hikes will ultimately be required in this cycle.

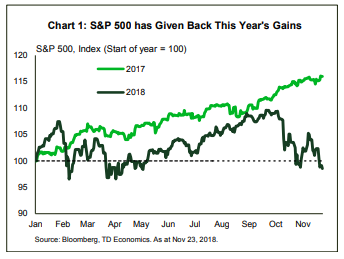

U.S. - “Bah! Humbug!”

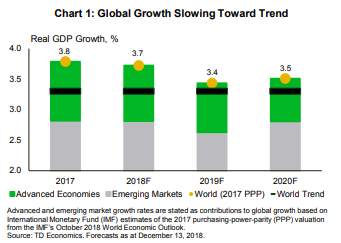

Our latest outlook did feature a small downgrade to global growth (Chart 1). However, the selloff in global risk assets in the fourth quarter has been outsized relative to the magnitude of the economic slowdown. The selloff likely reflects the build-up of unresolved global risks, coupled with a delayed adjustment in growth expectations from lofty levels. Taking a step back from the downturn in equity markets, there are few signs that the economic expansion is nearing an end, other than the fact that the expansion is approaching the longest on record. One worry is that negative sentiment can become self-fulfilling (see our Perspective). We remain vigilant in monitoring signals of an impending downturn, such as yield curves, business confidence, risk-assets, and labor market conditions.

The consumer is in pretty good shape. The job market is strong and inflation is contained. Economy-wide growth in wages and salaries has averaged roughly 4% over the past six months. And, headline inflation has cooled in line with lower oil prices. CPI inflation was at 2.2% year-on-year in November’s data. Our forecast is for inflation to remain around that level through 2019. That sets the consumer up for some decent real income gains. Therefore, we expect consumer spending to slow only modestly in 2019, as the windfall from tax cuts fades, but still running at a very healthy 2-2 ½% clip in real terms.

Overall, the U.S. economy is strong, and the Federal Reserve is well justified in raising rates another quarter point at its meeting next Wednesday. The real question is how the FOMC’s views have changed about how much further rates need to rise. Given the fairly benign inflation backdrop recently, we expect the Fed to hike rates more gradually in 2019.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

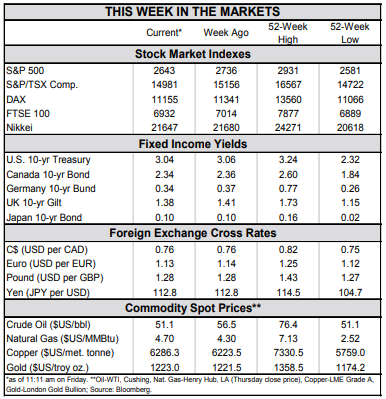

Financial News for the Week of December, 2018

HIGHLIGHTS OF THE WEEK

- Data released this week remains consistent with the view that U.S. economy continues to expand at an above-trend pace.

- Although disappointing in terms of the headline, job gains were also consistent with an economy running near capacity. Furthermore, wage growth held at a healthy pace in November.

- An agreement between the U.S. and China to delay an escalation of tariffs until April failed to convince financial markets that trade tensions are easing.

Markets Gyrate on U.S.-China Trade Headlines

Manufacturing and non-manufacturing activity picked up a bit in November, but is still off the highs recorded earlier this year. Firms continue to report capacity constraints, including labor and component shortages. Import tariffs remain a key concern. Similar worries were echoed in the Fed’s latest beige book report. Respondents to the Fed’s survey for the month of November indicated that labor shortages were being felt across a broad range of industries, and that tight labor markets were preventing them from getting the workers that they needed. In addition, rising costs, although offset in part by the falling price of oil, were impacting margins and leading firms to raise prices to offset them.

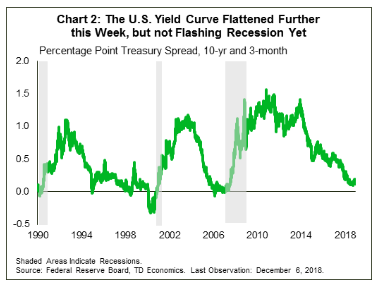

Strong fundamentals, however, are providing little comfort to financial markets. News headlines about slowing foreign demand growth, ongoing trade tensions, and Brexit have driven equity market volatility up, and prices down in the past couple of months. Fear lit a bid for bonds this week, with the U.S. 10-yr yield falling below 2.9% - its lowest level since early September. Although a flattening yield curve typically forebodes an increased chance of recession in the quarters ahead, there is little in the way of corroborating evidence (Chart 2). Instead, the recent move is likely a reflection of near-term concerns about temporary weakness in inflation and trade risks, rather than a deterioration in economic fundamentals.

Undoubtedly, an easing of trade tensions would be a welcome development. The G20 summit proved somewhat constructive as it produced a 90-day break from an escalation in import tariffs between the U.S. and China. But, news of the arrest of Huawei’s CFO later in the week revealed how fraught the relationship is currently between the U.S. and China. Tariffs appear to be just the first step in planned engagement with China on a set of deeper issues that need to be addressed.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

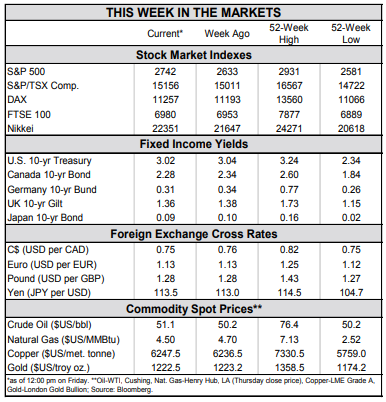

Financial News for the Week of November 30, 2018

HIGHLIGHTS OF THE WEEK

- FOMC minutes released this week suggested that flexible could be the new gradual for the Fed. While a rate hike for December may be in the cards, future moves are now more dependent on the incoming economic data.

- President Trump and Xi are set to meet-up at the G20 summit over the weekend. Stakes are high for an agreement to be reached. If not, higher tariffs are set to kick-in come January.

- While cracks are starting to show in the armor of the U.S. economic expansion, there’s still plenty that’s going well. Q3 GDP growth remained solid, consumer spending is strong, income gains are healthy and inflation is contained.

Yellow is the New Green?

FOMC minutes suggest that a rate hike in December is all but a done deal, but the path thereafter is more uncertain. Indeed, Fed members emphasized the need to maintain flexibility in order to respond to changing economic data. A shift in tenor from possible overheating to slower-than-expected growth was also discernible in the details of the discussion. Trade tensions in particular were “cited as a factor that could slow economic growth more than expected.”

In that vein, the trade tug-of-war with China continues. The hope is that negotiations go well at the G20 meetings in Buenos Aires that kicked-off Friday. The stakes are high. President Trump signaled prior to the meeting that if the two countries failed to reach an agreement favorable to the U.S., additional tariff on virtually all U.S. imports from China would be forthcoming. Such a development would exacerbate the slowdown in global growth - another risk flagged by the Fed.

The good news is that consumers are showing little sign of fatigue. Consumer spending grew robustly in October, rising 0.4% and setting the stage for a strong showing in the final quarter of this year. Holiday spending may get a further lift as households spend the extra coin left in their wallets after filling up at the gas pumps. Revisions to third quarter GDP were similarly encouraging (Chart 2) with business and residential investment revised up.

Overall, the economic data flow out of the U.S. this week was relatively balanced. Unfortunately, the downside risks to the outlook are mounting. It became clearer this week that the Fed is paying more attention to these risks and the economy may not need as many rate hikes as they believed back in September. All said, yellow may become the new green for the still-global-growth-leading U.S. economy.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

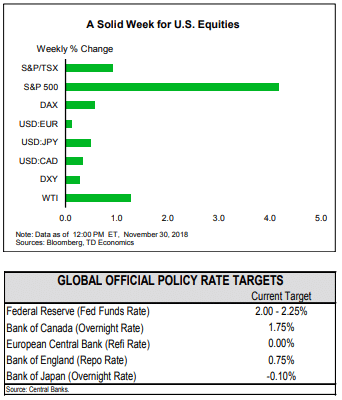

Financial News for the Week of November 23, 2018

HIGHLIGHTS OF THE WEEK

- Equity market volatility persisted this week as the main indexes were dragged down by tech and energy stocks. The latter resumed their slide as oil prices fell to their lowest levels in more than a year.

- Housing data was mildly positive, but continued to drive in the point that the sector remains a sore spot. Both existing home sales and housing starts rose around 1.5% month on month in October. But, sales are still down some 5% year on year, weighing on builder confidence.

- Presidents Trump and Xi will meet at the G20 summit next week in Buenos Aires. Any conciliation would be a plus for financial markets. Here’s hoping that the atmosphere and outcome are as pleasant as the host city’s name.

Despite Sour Week, There Is Still Plenty to Be Thankful for

Despite the carnage in equity markets, there is still plenty to be thankful for. The U.S. economy remains the growth-leader among the G7 and appears likely to retain its lead over the next year. Its labor market echoes this strength, with more job openings than there are unemployed Americans. This backdrop has allowed the Fed to raise interest rates at a faster pace than its peers and also gives it the flexibility to respond to any future hiccups in growth.

With interest rates rising, resale activity is likely to remain soft. Still, a strong labor market and a more gradual increase in mortgage rates going forward should limit the downside. Median home price growth has moderated to 3.8% year on year, which alongside rising wage growth, will limit the hit to affordability as mortgage rates rise. An improvement in the number of homes for sale in recent months also marks a positive step. Still, inventory levels are historically low and this imbalance should ultimately help housing starts retain their mild upward trajectory over the medium term.

Aside from the housing market, developments on the trade front bear close watching. Next week’s G20 summit appears an ideal setting for President Trump to announce a deal with his Chinese counterpart. Without progress, tariff rates are likely to increase in January, which could further undermine market confidence. As Trump and Xi tango in Buenos Aires next week, here’s hoping that the atmosphere and outcome are as pleasant as the host city’s name. Should trade tensions continue to fester, and confidence take a further hit, the Fed’s preferred path of rate hikes will come into question.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

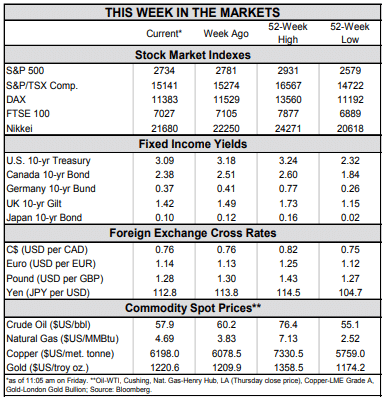

Financial News for the Week of November 16, 2018

HIGHLIGHTS OF THE WEEK

- Equity markets were volatile again this week as concerns over global growth remained top of mind for investors.

- Economic data continues to point to solid economic growth stateside, with little signs that global weakness has caught on domestically.

- Inflation data for October showed a relatively benign picture. While the headline rate rose to 2.5% (from 2.2%), core inflation edged lower on the month.

Growth is Solid, Inflation is Benign, Why Worry?

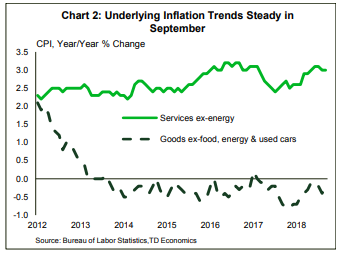

Financial market jitters are not a reflection of any newfound weakness in U.S. economic data, which continues to point to solid growth and limited inflation. This week, consumer price index (CPI) data for October showed headline inflation rise to 2.5%, mainly due to rising energy prices. Core inflation, on the other hand, edged down to 2.1% (from 2.2%). Over the past three months, core prices have risen an average of just 1.6% (annualized), suggesting little cause for alarm on the price front. What’s more, the recent pullback in the price of oil is likely to push headline inflation lower in the months ahead, with the Fed’s preferred metric – the personal consumption expenditure price index – likely to drift back below the 2% mark.

Other economic data confirmed the solid economic growth narrative. Retail sales rose a robust 0.8% in October, reversing a downwardly revised pullback in sales in September. The drop in September and rebound in October reflected hurricane-related disruptions. Overall, the retail sales data are consistent with real consumer spending advancing by around 2.5% in the fourth quarter. For all intents and purposes, this is a great number. Nonetheless, it does represent a deceleration from the heady 3.9% pace average over the second and third quarters of the year.

With real consumer spending likely to run in the mid-2% range, the overall economy is likely to follow suit. In this environment, the impact of tariffs is likely to be more noticeable. Already there are signs that businesses are attempting to get ahead of the scheduled increase in Chinese tariffs to 25% (from 10%) by stockpiling imports. This volatility makes reading the economic tea leaves and the job of the Fed in gauging the reaction of the economy to higher interest rates that much more difficult.

James Marple, Senior Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 9, 2018

HIGHLIGHTS OF THE WEEK

- Between the midterm elections and a Fed rate decision there was plenty of news this week. But after the dust settled there was very little new information.

- In the midterm elections, Democrats gained a majority in the House of Representatives, and Republicans tightened their grip on the Senate. A divided Congress through 2020 will temper parts of Trump’s agenda, and could make some upcoming fiscal tests more challenging.

- As expected, the Federal Reserve left rates unchanged, with a largely unchanged statement. Recent economic data suggest the next hike is coming in December.

Plenty of News, But Not Much New

Congress is now gridlocked through 2020, which raises risks on a variety of fronts. A few tests loom on the near-term horizon. Currently 25% of discretionary spending for the 2019 fiscal year is under a temporary funding agreement until December 7th. The current Congress will likely kick the can into early 2019, which sets up a potential funding battle and the risk of a partial government shutdown in the New Year. Government shutdowns are a risk with a divided government, but typically these do not have a meaningful impact on economic activity (as they have not proved long lasting).

As President, Trump has the authority to push ahead with his trade agenda. He may even get some support from the Democratic House for a harder stance on China. As such, the increase in Chinese import tariffs to 25% from 10% on $200bn of goods on January 1st is more likely than not, presenting a downside risk to our forecast.

Finally, there was little new from the Fed. The statement’s characterization of the economy was broadly unchanged. The slight updates that were made merely reflect the latest data, and are not major new developments. Most importantly, the Fed said it “expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity...” and that “risks to the economic outlook appear roughly balanced”. The recent economic data certainly point to a rate hike at the December meeting.

Most recently, October’s Producer Price Index showed that inflationary pressures are alive well further up the supply chain. And while consumer price inflation hasn’t heated up in recent months, price hikes are likely coming in many sectors as margins are increasingly squeezed.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 2, 2018

HIGHLIGHTS OF THE WEEK

- The U.S. labor market continues to impress – churning out jobs like nobody’s business (+250k), keeping the unemployment rate near record lows (3.7%), drawing people into the labor force (participation rate up +0.2 percentage points), and pushing up wages to boot (3.1% year-on-year – the highest since 2009)

- The fly in the ointment? A fierce sell off in equity markets in October, putting in question the more than nine-year-old stock bull market. Major stock indices closed the month down, eking out only marginal gains year-to-date.

- Trade tension with China is one catalyst for market jitters. A phone call between Presidents Xi and Trump this week signals progress, but the jury is still out on whether a broader trade war can be avoided.

Economy is Hot, but Markets Worried About the Future

The tight labor market is indeed forcing many to compete for workers by boosting paychecks. Both the employment cost index, which captures wages and benefits, as well as average hourly earnings show upticks in workers’ compensation. Wages broke through the 3% growth ceiling that has stood for nearly a decade, coming in at 3.1% y/y. Wages haven’t exceeded 3% growth since April 2009 (Chart 1).

Going in the opposite direction, home-price gains decelerated for the fifth consecutive month in August. The S&P Case-Shiller Home Price Index grew 5.8% y/y, falling below 6% for the first time in a year. After more than five years of solid home price growth, this is the latest indication of a slowdown in the housing market, which is likely to persist as interest rates edge higher. Despite slowing, house price inflation remains well above wage growth, contributing to the affordability crunch prospective buyers have grappled with of late (Chart 2).

Rounding out the week were data on ISM manufacturing and personal income and spending. Manufacturing activity eased in October, though it remained in growth territory as manufacturers continued to struggle with capacity constraints and tariff pressures. Though consumer spending momentum remained strong through the end of Q3 and should result in a solid Q4 handoff, the stimulus from tax cuts likely plateaued in Q3 and could be a harbinger of slower consumer spending. Year-on-year, core PCE inflation remained at 2.0% for a fifth straight month.

One potential development that could raise inflation (and further reduce the stimulative impact of tax cuts) are higher tariffs. On that front, tensions with China continue to simmer. This week, the Commerce Department barred U.S. companies from engaging in business with a state-owned Chinese chip maker after it was accused of stealing trade secrets from an American firm. The news left China’s chip industry on edge, feeling vulnerable to the escalating China-U.S. trade standoff. Subsequently, a spark of hope emerged Thursday when President Trump signaled progress on trade talks. This followed a phone call, initiated by the White House, to President Xi. The two countries are now more likely to resume talks at the G-20 summit in Buenos Aires later this month. As things stand, however, the jury is still out on whether there will be a cease fire in the trade fight following the summit.

All told, the U.S. economy is currently enjoying the sweet-spot of low inflation and unemployment. Only time will tell for how long.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

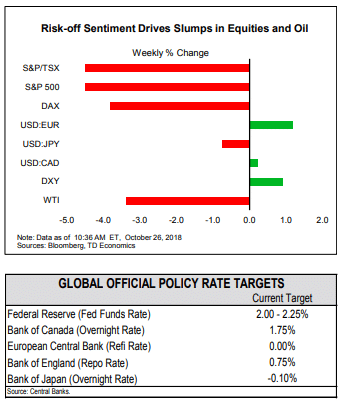

Financial News for the Week of October 26, 2018

HIGHLIGHTS OF THE WEEK

- It was a sea of red in equity markets this week as risk off sentiment set in. As it stands, downturn in October has erased all the stock market gains from the start of the year.

- International developments didn’t help to lift investors’ spirits. The U.S. – China trade negotiations appear to have hit a stalemate, and the European Commission has rejected Italy’s government budget.

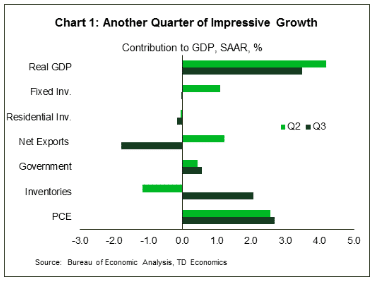

- Domestically, the advance estimate of Q3 GDP was the only major data release this week. After an impressive Q2, the U.S. economy has downshifted slightly in Q3, but at 3.5% (annualized), growth has nonetheless remained very hot and well above potential, giving the Fed ammunition for another rate hike in December.

Economy is Hot, but Markets Worried About the Future

International developments didn’t help to lift investors’ spirits. It seems that the U.S. – China trade negotiations have hit a stalemate. This threatens to undermine a scheduled meeting between the two presidents in November, and raises the probability of further tariffs. Also, in an unprecedented (even if widely expected) step, the European Commission has rejected Italy’s budget.

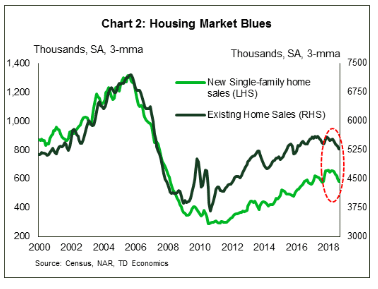

Even as consumers are hitting malls in masses, the housing market remains unloved due to deteriorating affordability and lack of supply. Sales of new and existing homes are down by 11% and 6%, respectively, since December (Chart 2). With both homebuilders and prospective buyers facing a number of hurdles, residential investment has been contracting for three consecutive quarters.

Business investment was another fly in an ointment in today’s GDP report. After setting a blistering pace in the first half of the year, spending took a breather in the third quarter, up only 0.8%. While one quarter does not make a trend, given the tensions on trade front this is where the risks lie going forward. Tariffs have already dented business confidence and could lead to further delays in investment in the coming quarters. If investment spending continues to be soft, dampening economic growth, the Fed would likely temper the pace of rate hikes.

All in all, with trade risks percolating and the boost from fiscal stimulus expected to fade, performance over the last two quarters likely represents the high water mark for the U.S. economy. So far though, despite President Trump taking yet another jab at the Fed this week, it certainly looks like current economic fundamentals warrant another interest rate hike in December, bringing the upper end of the target range to 2.5%.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of October 19, 2018

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Equity markets stopped hemorrhaging and partially recovered from last week’s downturn. Domestic data was predominantly underwhelming, but did little to change the status quo of a solidly-growing U.S. economy.

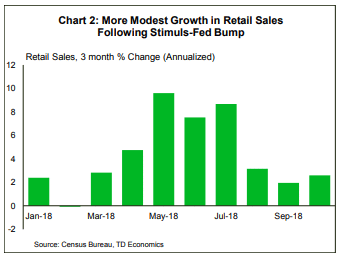

- Retail sales, existing home sales and housing starts all fell in September, with figures likely swayed by Hurricane Florence. Core retail sales however, rose by 0.5%, which suggests that consumption grew at a healthy 3% (ann.) in Q3.

- The FOMC minutes reinforced the view for continued interest rates hikes. Still, downside risks are percolating (mostly external) and the path ahead will require careful navigation.

Plenty of Potholes Will Require Careful Navigation Ahead

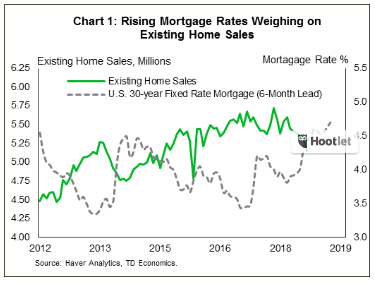

Despite a strong consumer backdrop, the housing market continues to struggle. Existing home sales fell 3.4% in September, marking the sixth straight monthly decline. Housing starts didn’t do any better, falling 5.3% to 1.20 million. Again, part of the weakness can be chalked up to weather-related disruptions, with both existing home sales and starts in the South recording the sharpest drops since late 2015. Going forward, tight inventories of homes for sale should help support moderate gains in new homebuilding. Still, limited supply will keep upward pressure on prices and weigh on demand, especially in the near-term. Rising interest rates, which appear to be behind some of the recent malaise, will be an added headwind (Chart 1).

While the data remain supportive of ongoing rate hikes, there is no shortage of potholes in the path ahead, particularly on the international front. Across the pond, Brexit remains a source of uncertainty, while recent developments in Italy have also become a major cause of concern. The EU Commission has determined that Italy’s draft budget is in serious breach of EU budget rules, and may reject it. The Rome-Brussels rift, which has sent Italian bond yields skyward (Chart 2), will bear close watching next week with Italy expected to reply to the commission by Monday. Chinese economic growth is slowing and policymakers there have a tough balancing act between deleveraging and maintaining adequate growth. A sour exchange between trade representatives of the EU and U.S. this week also reminds us that the Trans-Atlantic trade truce rests on feeble foundations. All told, plenty of risks remain and it won’t be an easy path to navigate.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

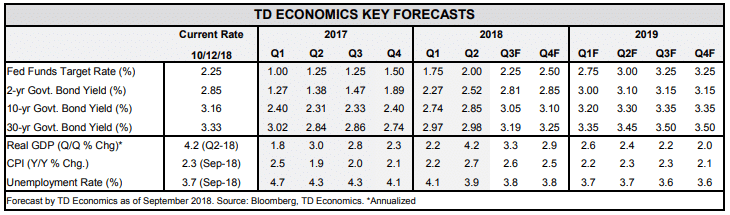

Financial News for the Week of October 12, 2018

HIGHLIGHTS OF THE WEEK

- The S&P500 has seen its biggest five-day loss since February this week. Much like then, higher bond yields have led to a repricing of stocks.

- There are few signs the U.S. economy is cooling. September consumer price inflation data showed that inflation pressures remain quite contained.

- On net, this argues for a continued gradual pace of rate hikes by the Fed. A severe tightening in financial conditionswould put this at risk, but there is little evidence of that yet.

Stocks Adjust to Higher Yields

For its part, the U.S. economy continues to do well. Indeed, stocks have weakened in part because the economy is doing well. The Fed has clearly signaled they expect strong economic growth to continue, and expect to continue raising rates over the coming year. Bond markets are increasingly taking them at their word, and investors now require a higher yield to hold bonds. When analysts value equities, they discount the expected future cash flow or dividends, and with higher rates those discounted cash flows are looking less valuable, resulting in a repricing of stocks.

There are plenty of downside risks lurking around corners for the U.S. economy: negative impacts from increased tariffs; higher government deficits could lead to a further move up in Treasury yields; and the risk of a Fed policy error. But, at the moment it must be acknowledged that the U.S. economy is growing strongly, a healthy labor market is increasing the share of people with jobs, and wage gains are occurring. At the same time, inflation pressures remain very well behaved. That helps ensure the Fed can remain patient as it raises policy rates.

Meanwhile, services inflation has picked up from its 2017 soft patch, but it hasn’t really broken new ground. We continue to expect a tight labor market, and increased wage pressures to lead core inflation higher over the next year. But, September’s inflation numbers provide reassurance that an undesirable sharper upturn is not occurring. We expect the Fed to continue raising rates a quarter point at every other meeting over the next year. It would take a much more severe tightening in financial conditions than recently observed to put this pace at risk.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.