Financial News for the Week of May 10, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Effective today, the U.S. increased tariffs to 25% on $200bn worth of Chinese imports.The threat to extend a 25% tariff to virtually all Chinese imports “shortly” remains. This comes even as the two sides continue negotiations to reach a trade deal.

- The U.S. overall trade deficit edged higher in March to $50bn, even as the bilateral goods trade deficit with China declined to a five year low.

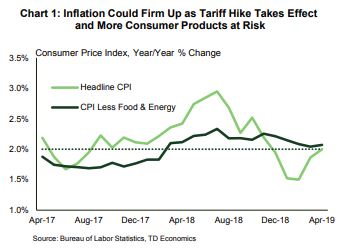

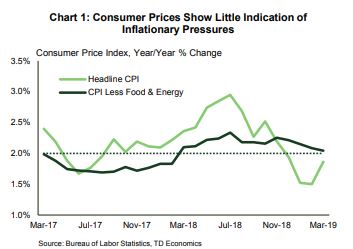

- Consumer price inflation continues to show little signs of accelerating,with both headline and core inflation around 2%. Things could change however, as tariff hikes filter through the economy.

U.S. - Tariff Talks Teeter

The U.S. administration officially implemented the tariff increase from 10% to 25% on approximately $200bn worth of Chinese imports on Friday. Additionally, President Trump has tweeted that he plans to levy the new 25% tariff on a further $325bn worth of Chinese goods “shortly”, a move that would cover virtually all U.S. imports from China. Even as China urged the U.S. to meet them halfway, they announced that countermeasures will be implemented, although specific details have not been revealed.

Despite the new developments, talks continued on Friday as the two sides try to salvage a deal. A sticking point for the U.S., however, is whether China will agree to implement legal changes so as to facilitate the trade deal and to make the details public. China has resisted this push, insisting that it impinges on their national sovereignty.

To date, inflationary pressures have been benign. Consumer prices in April rose 0.3% over the previous month and were up 2% year-on-year (Chart 1). However, the threatened escalation in tariffs could see inflationary pressures firm up. We estimate that consumer prices rose by 0.3ppts from tariffs already imposed and could rise by an additional 0.4ppts if the remaining $325bn of Chinese imports are made subject to 25% tariff (see note).

Despite the U.S.’s heavy use of tariffs to rebalance trade flows, their trade deficit edged up in March, reflecting the difficulties inherent in attempting to redirect international trade. Of note, the merchandise trade deficit with China, a special area of interest, has been declining for the past few months, and hit a five year low in March (Chart 2). This development may positively impact ongoing negotiations between the two economic powerhouses. All told, the U.S. and Chinese economies are at an important juncture. Decisions made now are likely to have significant implications for the global economic landscape in the future.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 3, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Apart from vehicle sales, recent data paint a positive narrative for consumer-related industries at the start of spring. Real consumer spending and pending home sales surged in March, while consumer confidence improved in April.

- Payrolls were up 263k in April, much better than expected; wage growth held steady at 3.2% y/y and the unemployment rate fell to a near-50 year low of 3.6%. A drop in the labor force participation rate assisted the latter.

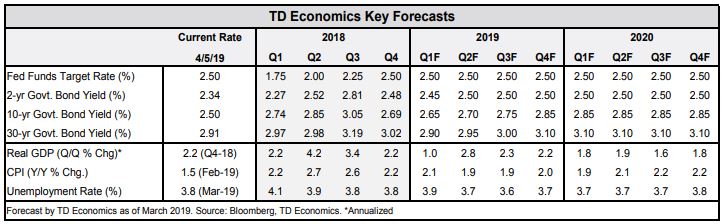

- The Fed held rates steady this week, with an emphasis put on inflation running below target. But in the press conference, Fed Chair Powell noted that inflation was driven down by “transient” factors, adding that there is no strong case “for moving in either direction”. Indeed, for now, all of the tea leaves suggest that the Fed will remain on hold for some time.

U.S. - Q1 Growth Surge Shakier Underneath The Hood

While the consumer had a soft showing overall in the first quarter, a two-month data dump this week provided added detail on recent momentum. Real consumer spending was flat in February, before surging 0.7% in March. This spending upswing points to consumers shaking off the adverse effects of the prolonged government shutdown, and provides a solid handoff to consumption in the second-quarter.

The (mostly) positive narrative on consumer-related industries at the start of spring was further bolstered by a 3.8% m/m surge in pending home sales in March and a pickup in consumer confidence in April. The former leads existing home sales by 1-2 months, and points to further stabilization in the housing market. However, vehicle sales were disappointing, falling 6% m/m in April to 16.4M units. Despite this, overall consumer spending is still tracking a 3% annualized pace in the second quarter, a sharp acceleration from the 1.2% clip in the first quarter. This will provide support to overall economic activity as other temporary factors that boosted growth in the first quarter fall off.

Rounding out the April data reports were the ISM indices. Both moderated on the month but continue to hover around the 55-point mark, which is in tune with the broader narrative of slower, but still decent, growth this year.

With the labor market and economic growth not looking too shabby, inflation remains the Fed’s key concern and main reason for holding rates steady, as it did this week. The FOMC statement emphasized that inflation has run below target. But in the press conference, Fed Chair Powell noted that inflation was driven down by “transient” factors, adding that there is currently no strong case “for moving in either direction”. We agree with the Fed’s assessment. Given that inflation has persistently undershot the Fed’s target, it would take a notable acceleration in price pressures to push the Fed to hike. We do not expect inflation to accelerate that quickly, and all of the latest data support our view that the Fed is likely to remain on hold for quite some time.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 26, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

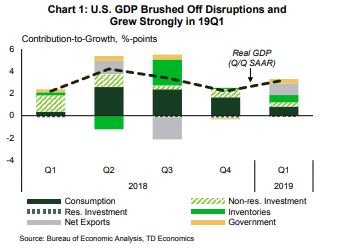

- The American economy grew by 3.2% in the first quarter of 2019, comfortably beating market expectations. However, the strength was driven by inventories and net exports, while domestic demand growth weakened.

- The housing market continues to be an economic weak link. Existing home sales in March fell below expectations. A lack of inventory appears to be weighing on sales activity.

- As confirmed in the GDP report, price pressures were softer than expected early in the year, underpinning the Federal Reserve’s move to the sidelines.

U.S. - Q1 Growth Surge Shakier Underneath The Hood

Amid the hurrah of strong real GDP growth, the one segment of the economy that continued to underperform was housing. Residential investment contracted in all four quarters of 2018, and pulled back again in the first quarter. Early indications suggest a mixed start to the second quarter. Existing home sales fell 4.9% in March, below consensus expectations. The pullback followed a strong gain in February, but the level of sales has shown little overall progress over the past several months (and is well off peak levels seen in the fall of 2017). Fortunately, the news was better on the new home sales front. New single-family residential sales rose 4.5%, building on even stronger gains in January and February. In contrast to the existing market, new home sales are just a touch below the recent cycle peak.

Speaking of prices, PCE inflation data for 19Q1 was released alongside GDP data and came in surprisingly soft. We cannot yet tell which month the weakness was concentrated as only January data are available (February and March data will only be released on Monday). Nevertheless, the weaker reading in Q1 indicates cooling price pressures, reinforcing the Federal Reserve’s position to hold off any interest rate hikes through 2019. Bond yields appear to have dipped lower following the digestion of these details, discounting the surprise in real GDP growth.

Headline inflation is likely to see something of a lift in upcoming months, reflecting the broad-based rebound in oil prices since the end of 2018. Still, the ride may be bumpy. The West Texas Intermediate oil price benchmark hit $65 earlier in the week, before falling on Friday on word that Trump has been upping the pressure on OPEC. This, despite news that the administration will no longer exempt countries from Iran sanctions beginning May 2nd.

Sri Thanabalasingam, Economist | 416-413-3117

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 18, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Spring is coming to the U.S. economy after a tough winter. An impressive bounce back in retail sales in March indicates that consumer spending will bounce back in the second quarter after a disappointing start.

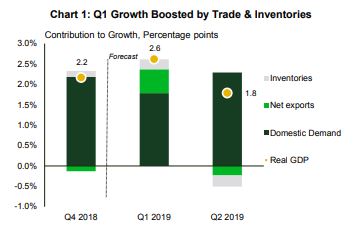

- First quarter GDP growth is released next week, and it is likely going to be messy. A strong headline is likely to belie weakness domestically, while the reverse is likely to be the case in Q2.

- Overall growth in the first half of the year is tracking close to our March forecast, the quarterly pattern is somewhat reversed. The overall story that the economy has slowed from its 2018 pace, but remains above trend, remains intact.

U.S. - Spring is Coming

The first estimate of Q1 economic growth will be released next week. The story is likely to be muddy. Headline GDP is forecast to post a reassuring 2.6% print, but that hides a much softer picture for domestic demand (1.7%, annualized). The combination of an inventory build and a decline in imports is forecast to add nearly a percentage point to growth (Chart 1). Domestic demand, meanwhile, was held back by weakness in both consumer spending (+1.2%) and business investment (+1.6%).

Soft consumer spending is likely to prove temporary. The combination of plummeting stock markets, government shutdown, and bad weather helped send consumers into hibernation at the end of 2018 and early 2019. But, March retail sales showed consumers awakening from their slumber, enough to lift consumer spending to roughly 2 ½% in the second quarter.

Retail weakness had stood out against stronger fundamentals in terms of income growth, low unemployment and confidence surveys. That said, the 3%-plus readings on real consumer spending we saw last year are behind us. We expect continued solid quarterly growth in outlays in the 2-2.5% range for the remainder of the year. This downshift in growth is apparent in the smoothed year-on-year growth in retail sales (Chart 2).

The Fed’s latest Beige Book – its qualitative snapshot of the U.S. economy – reinforces this view of the economy slowing from last year’s pace, but still growing solidly. Labor markets were characterized as tight, restraining hiring growth in some regions. Some weakness is evident in manufacturing, consistent with weaker demand from abroad. Trade uncertainty restrained expansions in some districts. The clouds hovering over the global outlook have not cleared, despite a better-than-expected first quarter growth report out of China.

Trade peace with China and Europe would certainly help global sentiment. China and U.S. negotiators plan two more rounds of face-to-face talks, and are working towards a signing ceremony in late May/early June. It remains to be seen whether a deal lifts the tariffs already in place, or if these are kept on as an incentive for compliance. If they are lifted, it would provide a tailwind to Chinese, and likely global, growth.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 12, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Inflation pressures remain benign, as headline consumer prices rose just 1.9% year-on-year in March, and core prices came in at 2.0%.These numbers reinforce the Fed’s ‘patience’stance that was reiterated in its March FOMC minutes.

- US-China trade negotiations are progressing with China appearing to make further concessions on tech-related issues, and the two sides agreeing on an enforcement mechanism.

- Trade talks with the EU, however, are set to become more contentious as the U.S. threatens tariffs on EU imports following a ruling from the WTO on a longstanding disagreement.

U.S. - Not too Hot, Not Too Cold, (Almost) Just Right

Several months of muted inflation readings have strengthened the Fed’s decision to keep rates where they are. Minutes of the March meeting showed that board members saw little in the data to prompt a shift in policy. This rhetoric is expected to continue through the end of 2019, with signs of an improving labor market balanced against risks to growth from a struggling global economy. The Fed’s European counterpart (the ECB) on the other hand, while leaving rates unchanged this week, signaled that there could be substantive changes to monetary policy at their next meeting in June. With anemic growth among member countries and lingering policy uncertainty, it signalled a willingness to act to ensure a return of inflation to target and bolster the region’s faltering growth.

Boeing for its part continues to deal with fallout from the grounding of its 737 MAX airliners. There were no commercial orders for the product in March, the first time this has occurred since May 2012. Boeing will reduce production of the jet starting mid-April, while it works to fix flaws with the model which resulted in two fatal crashes. If the production cut lasts to the end of the quarter, they could shave 0.1 to 0.2 percentage points off Q2 GDP growth.

Internationally, Britain’s attempt to leave the EU continues to push past deadlines. This week the EU granted another flexible extension to October 31st for the UK parliament to agree to a deal. The gesture, however, came with strings attached, as the UK will have to hold EU parliamentary elections if they have not ratified the deal by the end of May or risk exiting without a deal on June 1st.

Given these and other uncertainties, the IMF downgraded projections for global growth in 2019 to 3.3%, citing ongoing trade tensions and declining confidence (Chart 2). This brings their forecast in line with our own view published in March. Growth in 2020 is expected to rebound to 3.6%, slightly above our expectation for 3.5% growth.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

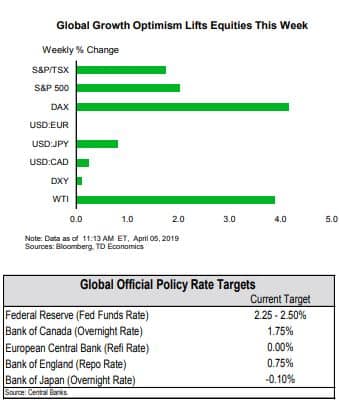

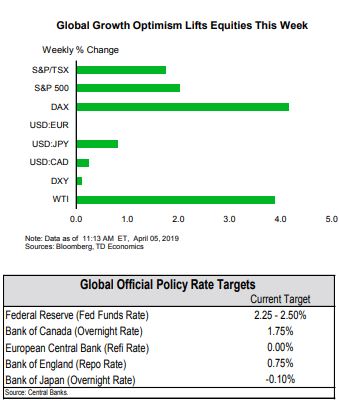

Financial News for the Week of April 5, 2019

HIGHLIGHTS OF THE WEEK

- Progress on U.S.-China trade negotiations helped support risk appetite this week, with equity prices and yields up.

- February retail sales fell 0.2% month-on-month, but an upgrade to January made it more palatable. On the other hand, the job market bounced back in March (+196k), confirming that the weakness in February was but a speed bump.

- The pace of job gains is expected to slow to around 150k per month on average over the remainder of the 2019 – slower than last year, but still decent and more than sufficient to keep downward pressure on the unemployment rate.

Labor Market Strength Back on Display in March

Economic data, though not entirely positive, was broadly supportive. February retail sales undershot market expectations, falling by 0.2% m/m, instead of rising by a commensurate amount. The miss on the sign in the headline print seemed like a cruel April Fools’ joke. But, the hefty upward revision to January mitigates the downside to 19Q1 spending (Chart 1). Proving more constructive was a strong bounce-back in auto sales in March to 17.5 million, after two consecutive monthly declines. But, even with a decent showing in March, first-quarter consumption growth is unlikely to surpass 1% annualized. This soft performance is really no surprise given the drag from ‘residual seasonality’ and the government shutdown.

Lower interest rates and a steady Fed, together with a robust labor market, should continue to shore up spending in the months ahead. On the employment front, the payrolls report did not disappoint, with job gains making a comeback in March (Chart 2). The economy added 196k new jobs last month, while the unemployment rate managed to hold on to a low 3.8%. In addition, the prior two months of data were revised up by 14k combined. Other details were less rosy, such as the participation rate ticking down 0.2 ppts to 63% and wage growth easing a touch.

The recent performance of manufacturing and service industries supports this view. The ISM indices have decelerated on a trend basis from last year’s highs, but both remain well in expansionary territory. In March, the two indices diverged, with the non-manufacturing index undershooting expectations (-3.6 points to 56.1) and the manufacturing index surprising on the upside (+1.1 points to 55.3). Still, both signal an economy expanding at a healthy pace.

The resilience of the U.S. manufacturing sector has been remarkable, given the slump in activity elsewhere. Although manufacturing improved in China and a few regional partners in March, it remained in contraction in the Euro Area. The Old Continent is going through a rough patch, and, with economic growth expected to clock in at a low 1.3% this year, it remains a source of downside risk to the global economic outlook (see here).

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of March 29, 2019

HIGHLIGHTS OF THE WEEK

- The U.S. economy expanded at a slower pace than previously reported in the fourth quarter (2.2% vs. 2.6%). This left annual average growth at just below the 3% mark, though Q4/Q4 they were just able to hit that psychological marker.

- Housing starts declined in February, though the sale of new homes picked up. A recent deceleration in home price growth should support an expected rebound in housing activity in the months ahead.

- The trade deficit narrowed in January, aided by a decrease in the goods deficit with China – down $5.5B. On this front, trade talks between the two countries made progress as China showed willingness to negotiate on tech-related concerns.

U.S. - When the Downside Risks Loom Large

Hang on to your hats folks. With Fed speeches, Brexit votes, and a slew of economic data, this week was exhilarating.

Housing data also came in on the disappointing side. Housing starts declined 8.7% in February, giving back most of the gains in January. The turn lower was concentrated in the single family segment. Meanwhile, the pace of new home sales perked up to the best rate in almost a year (4.9%). Additionally, in January, home price growth decelerated to the slowest rate in almost 4 years – 4.3% (y/y) down from 4.6% a month earlier. It also marked 10 consecutive months of slowing growth (Chart 2). Higher mortgage rates earlier in 2018 and the past run-up in home prices dented affordability. However, recent declines in rates, smaller price gains, and rising wages should result in improved activity going forward as housing demand rebounds (see report).

Across the pond, the Brexit saga continued to unfold, leaving a lingering air of uncertainty. The UK’s Parliament failed to come to a consensus on alternatives to the withdrawal agreement on Wednesday. Out of eight options proposed, not one was able to garner the needed majority. Parliament voted for a third time against the deal today, the day Britain was originally set to leave. Prime Minister May, who offered her resignation in exchange for support, continues to face an uphill battle to consolidate opinion on a deal. Debate on a deal is expected to continue next week.

Lastly, a parade of Fed speakers made the rounds this week. Among them, Chicago Fed President Evans echoed sentiments expressed in last week’s Fed statement – a rate hike for 2019 is likely not in the cards, while his Philadelphia counterpart, Patrick Harker, suggested one hike could be appropriate. All told, policy normalization at the Fed is quite likely nearly complete, as rising global risks leave the U.S. exposed to foreign shocks.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

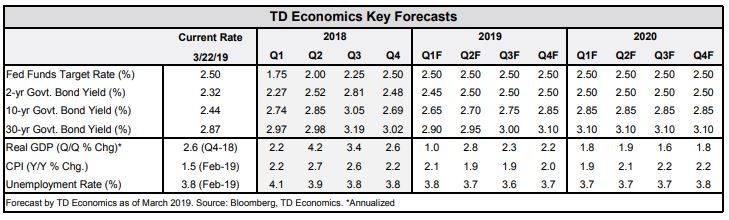

Financial News for the Week of March 22, 2019

HIGHLIGHTS OF THE WEEK

- The Fed’s dots showed that it only expects to hike rates once more by the end of 2020, sending Treasury yields lowermid-week.

- On Friday, weakness in March manufacturing surveys in Europe, Japan, and the U.S. sent longer-term U.S. yields low enough to invert the yield curve. A yield curve inversion has historically preceded a recession by up to eight quarters.

- In a separate drama, the UK has earned a two-week extension on its Brexit deadline to April 12th.It remains to be seen if the UK’s parliament will pass the current deal reached with the EU, and so further cliffhangers are likely.

When The Dots Are Down

The big-ticket event was the Federal Government’s release of its FY2019-20 budget on Tuesday (see commentary). The government’s projected deficits for last year were lower than initial estimates, with the windfall used to finance new initiatives. Some of the measures include a focus on incentivizing education and job training, with new refundable tax credits and EI support, and reduced interest costs on Canada Student Loans. Other areas of focus included environmental initiatives, where the government is introducing a credit for electric vehicles and transferring $1 billion to municipalities for greening initiatives.

Arguably, the most attention-grabbing parts were its housing demand measures (see commentary). Specifically, its First Time Home Buyer’s Initiative includes a shared equity mortgage program and an increase in RRSP withdrawal limits. This may help increase home ownership rates, but the impact on sales and prices is likely to be minor. Indeed, we anticipate both to be only around 3% higher by the end of 2020 if implemented. Still, not all markets are expected to benefit, with some like Toronto and Vancouver likely not benefitting as much due to the price cap, and with tight markets potentially experiencing higher price impacts.

Meanwhile, three provincial governments showcased a commitment to balanced budgets this week. New Brunswick’s decent starting point and planned spending restraint should help keep its books in the black within the projection horizon. Saskatchewan’s government also signaled a commitment to surpluses going forward, an encouraging feat given its outsized deficits following the 2014 oil price shock. Last but not least, Quebec’s new government tabled its first budget, introducing an array of new measures, with an intention to maintain surpluses of $2.5-$4 billion.

Budgets aside, two top-tier data releases capped the week. The CPI inflation print was unsurprising; with the headline coming in at 1.5% and the Bank of Canada’s core measures hovering slightly below its target, at an average of 1.8% (Chart 2). Retail sales disappointed for the third straight month, declining 0.3% and with volumes almost flat, consistent with expectations of a slowdown in consumer spending in Q1. Wholesale trade was decent, with a 0.6% uptick. Altogether, the data reinforce the expectation that the Bank of Canada will likely remain on the sidelines for a long period to come.

Omar Abdelrahman, Economist | 416-734-2873

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

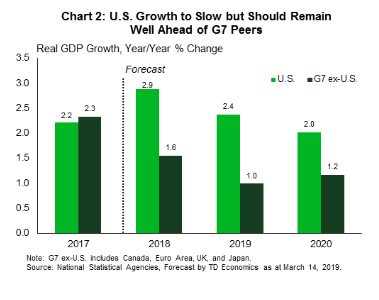

Financial News for the Week of March 15, 2019

HIGHLIGHTS OF THE WEEK

- Our updated economic forecast anticipates a slowdown in global growth to 3.2% in 2019, roughly at trend.

- A weak handoff from 2018 and start to 2019 motivates much of the downgrades in advanced economies, while growth in emerging markets is anticipated to perk up slightly later in the year.

- Growth in the U.S. is expected to slow, but still remain at an above-trend pace this year. That said, lingering economic uncertainty could weigh further on the domestic and global outlook.

Ahead of the (Slowing) Pack

This outlook is consistent with global demand growing roughly at the same pace as capacity, and, correspondingly, subdued inflation pressures. However, the headline print itself masks the disparate regional challenges. For example, a soft end to 2018 and a disappointing start to 2019 results in a much weaker growth outlook for G7 economies this year. Add a global manufacturing slump, and you have the impetus for a relatively weak economic expansion relative to past years. Downgrades like this justify the pivot to patience by G7 central banks. Interest rate hikes are effectively cancelled through the end of 2019.

In contrast, economic activity in the developing world is expected to heat up later this year. An anticipated improvement in global manufacturing activity, weaker inflation and lower global interest rates all support a firmer outlook in emerging market economies. That said, a slowing Chinese economy and elevated trade policy uncertainty vis à vis the U.S. could weigh further on major trading partners, stifling any sort of rebound in global economic activity.

Spending on consumer durables, such as automobiles, is expected to decelerate. Moreover, although a rebound in housing activity is expected later this year, very weak momentum acts to ensure that residential investment contracts for a second consecutive year. Net trade is also expected to weigh on growth again this year, with import demand outpacing exports.

The data this week acted to support this outlook. January retails sales staged a solid rebound from December lows. Combined with solid wage gains in February’s employment report, this sets the table for an uptick in economic activity later this quarter. That said, geopolitical events this week proved less constructive. Trade talks between Presidents Trump and Xi have been punted to at least April, and Brexit will likely be delayed at least through June. This suggests that elevated political and trade policy uncertainty will continue to weigh on global economic activity for at least a couple more months.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

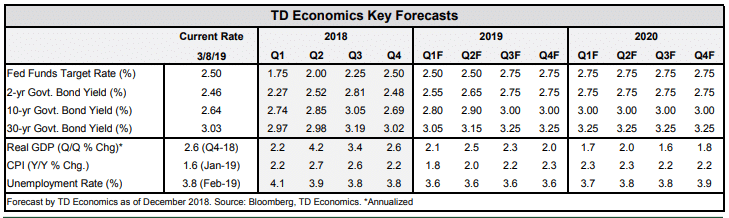

Financial News for the Week of March 8, 2019

HIGHLIGHTS OF THE WEEK

- This week started off on an upbeat note. An uptick in the ISM non-manufacturing index got the ball rolling, with the headline rising by 3.0 points to 59.7 in February.

- In a nice twist to the recent doom and gloom, housing data was also encouraging. Sales of new homes rose 3.6% in December, and housing starts surged by 18.6% in January.

- The positive economic news faced a setback on Friday as the payroll report showed job growth slowing to just 20k in February. The soft payroll print is unlikely to stay, but works to reinforce the Federal Reserve’s current “patient” approach.

U.S. - Positive Economic Data Muted By Weak Payroll Print

Housing data was also encouraging this week. Sales of new homes rose 3.6% in December, edging higher for the second month in a row. Ditto for housing starts. After ending 2018 on a sour note, homebuilding started the year on better footing with starts surging by 18.6% in January. The gain in single-family construction was even more impressive, with starts up by 25% – the highest monthly gain since 1979. As we discuss in our recent report, the housing market has room to grow and demand should rebound alongside rising affordability. With low vacancy rates, housing construction should continue to make gains over the next year.

There is good reason to look past the dour headline, which was probably influenced by temporary factors and poor weather. We expect job growth to slow in the months ahead, but it will be on the back of a labor market that for all intents and purposes has achieved full employment rather than any pronounced deterioration in domestic demand.

Still, the soft payroll print will reinforce the Federal Reserve’s current “patient” approach. On that front, the Federal Reserve has been joined by other global central banks. This week, the ECB unveiled a package of cheap funding for the Eurozone’s banks and said it would keep rates on hold until 2020 on the back of softening economic momentum and rising uncertainty related to Brexit and trade. The Bank of Canada’s statement this week was similarly dovish – noting the increased difficulty in reading the economic tea leaves given the increase in global crosscurrents. The dovish turn in other global central banks means the U.S. dollar is likely to remain relatively strong, giving the Fed even more reason to remain on the sidelines until at least the second half of this year.

Ksenia Bushmeneva, Economist | 647-876-1707

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.