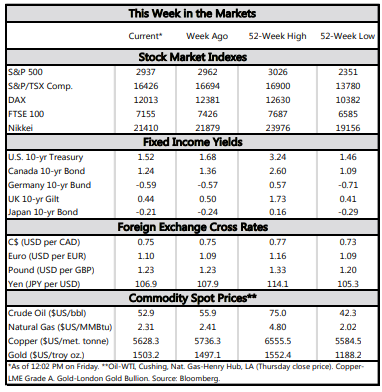

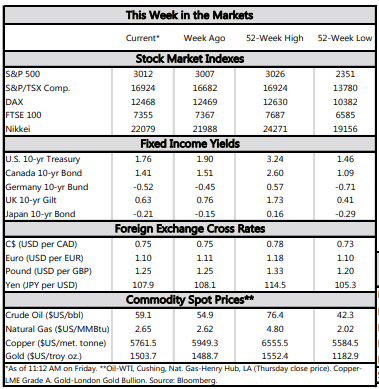

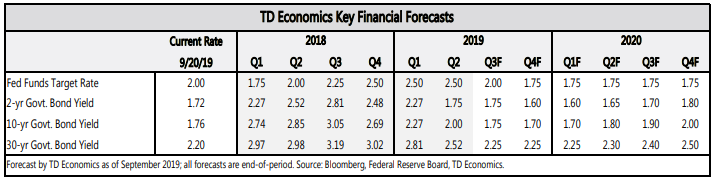

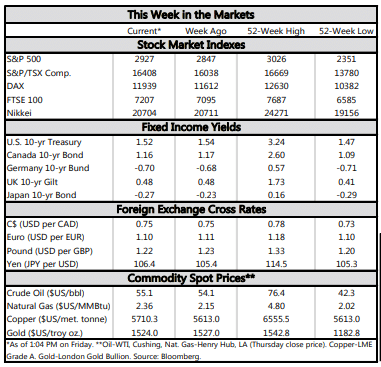

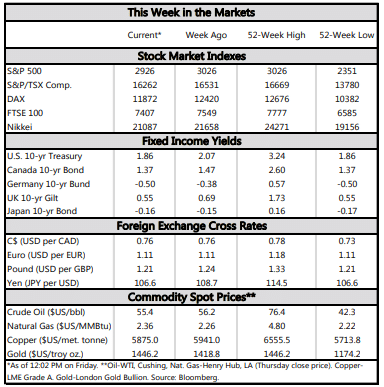

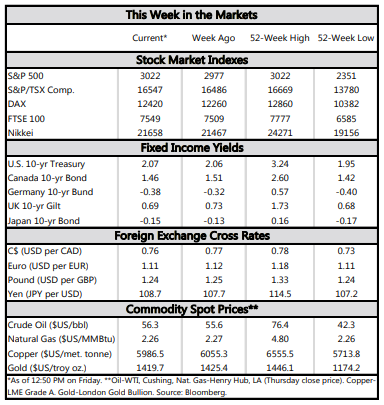

Financial News for the Week of October 4, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- October began on a sour note. A deepening contraction in the manufacturing ISM confirmed that the global manufacturing slump has washed up on American shores, and the sectoral weakness may be spreading into other industries.

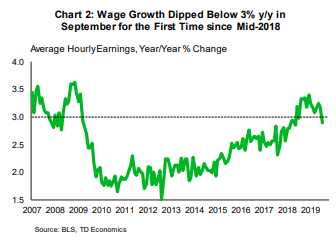

- The jobs report offered some encouragement, even as the details were not entirely positive. Payrolls rose a decent 136k and the unemployment rate fell to a 50-year low at 3.5%. Still, wage growth cooled, dipping below 3% y/y.

- Trade developments remained top of mind. After getting the okay from the WTO, the U.S. plans to apply tariffs on $7.5 bn of EU goods in mid-October. This is around the same time it plans to increase the tariff rate on $250 bn of Chinese goods. This increases the chances of tit-for-tat measures, which would expedite the slowdown in global growth.

Mixed Signals on Strength of Expansion

The consumer remains the main bright spot for the American economy. Keeping with that theme, U.S. vehicle sales continued their momentum with yet another strong reading in September (+1.1% to 17.2 million). On the surface, this bodes well for consumer spending in the third quarter. That said, given that the monthly gain was driven by fleet volume, we caution against reading too much into it.

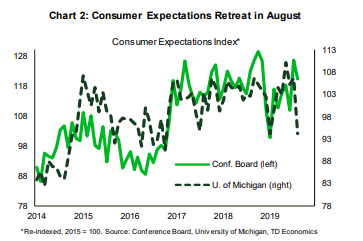

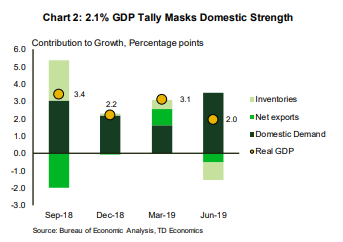

The jobs report however, offered additional encouragement on the consumption narrative. Payrolls rose by 136k in September – a decent print, but one that highlights an expected slowing trajectory in hiring at this point in the cycle. In addition, the tally for payrolls in the two months prior was bumped up by 45k. Meanwhile, the unemployment rate fell to a 50-year low of 3.5%. Given that the participation rate held steady, the drop in the jobless rate appears to be organically-driven, as workers moved out of unemployment and into jobs. One thorn in the side of this report, however, was a cooling of wage growth to 2.9% y/y – a factor that does not bode well for income growth (Chart 2).

A flare up in tensions may get the ball rolling for more tit-for-tat measures. The EU’s retaliation could push the U.S. to levy auto tariffs. A decision on the latter is already pending for mid-November. What’s more, in mid-October, the U.S. is set to raise tariffs on $250 bn of Chinese goods. Increased protectionist measures with any or both of its two most important goods trading partners, will expedite the slowdown in global growth. In this vein, we expect the Fed to continue with its cautionary stance by cutting rates once more this year.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

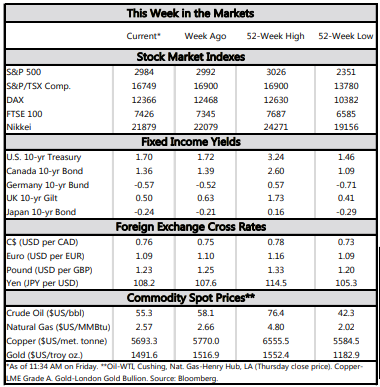

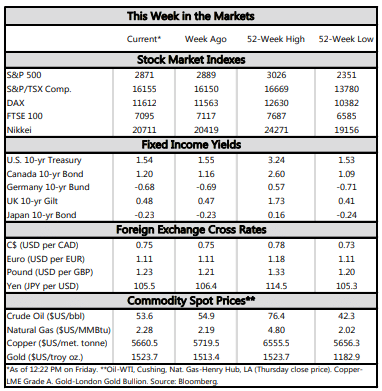

Financial News for the Week of September 27, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A downturn in U.S. consumer confidence and rising political risks as the House began impeachment inquiries against President Trump, triggered volatility in global markets.

- U.S. personal incomes jumped in August (to 0.4% month-on-month from 0.1% previously), even as spending was subdued (0.1% in August vs. 0.5% in July).

- Activity in the housing market continued to perk up with larger-than-expected rises in both new and pending home sales on the heels of similar increases in housing starts and permits last week.

Political Risks Heighten Economic Uncertainty

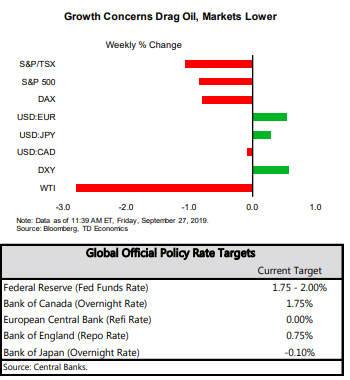

The financial news this week was highlighted by old-fashioned political words like “prorogation” and “impeachment.” In the U.K., the Supreme Court ruled that Prime Minister Johnson acted unlawfully when he prorogued Parliament earlier this month. The ruling is expected to intensify Brexit tensions in the weeks ahead.

In the U.S., House Speaker Nancy Pelosi announced an official impeachment inquiry into President Trump after a whistleblower report suggested that he withheld aid to Ukraine while pressing the country to investigate Democratic presidential candidate Joe Biden and his son. The threat of ousting the president from office contributed to market volatility, but with few believing it will hit the two-thirds of the Senate required for conviction, market reaction was relatively muted, with stock markets edging modestly lower and bond yields down a few basis points.

Meanwhile the U.S.-China trade dispute continues to simmer. Washington and Beijing, sent out mixed signals throughout the week. Mr. Trump noted that he wouldn’t accept a “bad” trade deal with China, but by Wednesday stated that a trade deal with China “could happen sooner than you think.” China, on the other hand, called trade talks “productive” and “constructive” and there are reports that Chinese companies are preparing to increase their purchases of U.S. pork and soybeans, notwithstanding the cancellation of scheduled U.S. farm visits by Chinese delegates.

On a more positive note, Mr. Trump and Japan’s Prime Minister signed a trade-enhancement agreement that will lower agricultural tariffs in Japan, industrial tariffs in the U.S. and set new rules for digital trade between the two countries. The limited accord is potentially the first step in a broader trade agreement between the two countries.

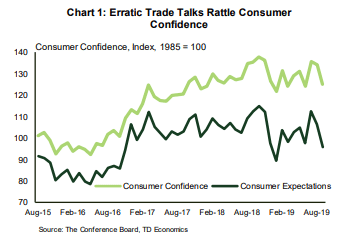

The erratic nature of trade talks has undoubtedly contributed to a falloff in consumer confidence. The Conference Board’s index fell by the most in nine months in September to 125.1, from a downwardly revised 134.2 the month before (Chart 1). The reading was well below market expectations. The expectations index also declined to 95.8 from 106.4 previously. The downturn in expectations could see consumers hold back on spending. Indeed, consumer spending slowed more than expected in August, nudging up just 0.1% month-on-month. On the upside, incomes rose by a solid 0.4%. Price pressures were steady, with PCE inflation holding at 1.4% year-on-year, but the core measure ticked up to 1.8% (from 1.7%).

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of September 20, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- In the main financial event of the week, the Federal Reserve cut its key lending rate by 25 basis points, but was mum on the prospect for additional cuts. Our latest forecast sees slower economic growth leading to at least one more rate cut.

- Fed rate cuts will help to offset some of the dampening effects of trade-uncertainty and weak global growth. In fact, this week saw early signs that the American housing market is responding to lower rates.

- Oil prices spiked early in the week on the attack in Saudi Arabia but gave up much of the gains as the week ended. Elsewhere, the strike at GM is likely to add volatility to the economic growth profile.

Fed Cuts Rates, More to Come

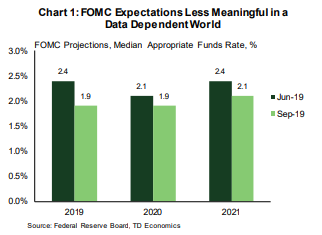

As expected, the Fed cut its key lending rate, but there was little change in its economic forecasts. Investors may have been disappointed by the Fed’s “dot” plot, which showed the median FOMC member does not expect to lower rates in the next few years. It is important to note that Chair Powell de-emphasized the “dots” in the press conference after the decision. He argued that when the Fed is dealing with a high degree of uncertainty and heightened data dependency the dots farther out have less meaning.

Recent history has borne this out. As recently as June of this year, the median FOMC member did not expect to cut rates in 2019 (Chart 1). In the three months since, the Fed has cut rates twice. The FOMC will clearly shift in response to risks to the economic outlook. It is late in the business cycle, with limited pent-up demand and mounting geopolitical risks. This requires the dot plot to be taken with several grains of salt.

Our new forecast discusses how a lower growth trajectory over the next year and continued uncertainty on the trade front is likely to lead the Fed to cut rates once more this year. Indeed, the Fed is not the only central bank easing policy. Easier financial conditions globally should help soften the negative cycle taking hold in sentiment, and ultimately sow the seeds for a modest firming in global economic growth in 2020.

Adding to an eventful week, the GM strike halted production at more than 30 U.S. plants. There are few signs of a deal, and the strike is likely to subtract around 0.1 percentage points off real GDP growth in Q3. The impact on fourth quarter growth will depend on how long it lasts and on how quickly GM ramps up activity after the strike. A four-week strike would see a very limited bounce back in activity in the fourth quarter, but would push the rebound in growth more into the first quarter of 2020.

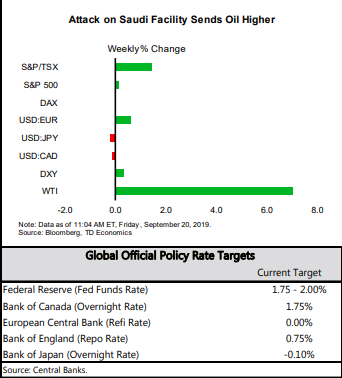

Finally, oil prices have fallen back after their spike on Monday. While the increase was startling, oil prices remain about 18% below their year-ago level, and prices at the pump continue to put downward pressure on inflation, adding to consumer purchasing power – at least for now.

Leslie Preston, Senior Economist | 416-982-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of September 13, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- There was good news in the trade negotiations between the U.S. and China this week as the President announced a postponement of tariffs and China exempted key agricultural goods (pork and soybeans) from existing tariffs.

- The European Central Bank lowered its key policy rate further into negative territory this week and announced a plan to restart asset purchases that will continue “for as long as necessary” to bring inflation back to target.

- U.S. core inflation picked up in August and retail sales beat expectations. Even so, the Fed is likely to cut rates by 25 basis points when it meets next week, likely citing global growth and trade headwinds.

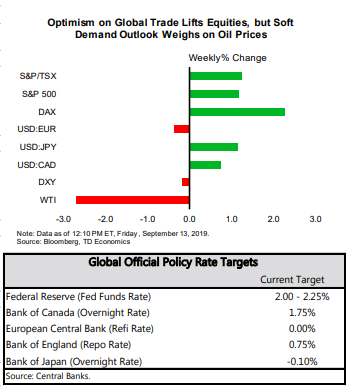

Optimism on Trade Deal Lifts Markets

In other Presidential tweets, Trump once again advised the Fed to cut rates, this time adding “to zero or less”. The president cited “no inflation” as justification. Only a day later, the consumer price index (CPI) data for August showed a pick-up in the core rate of inflation (excluding food and energy) to 2.4% year-on-year (y/y), its highest level since the recovery began (Chart 1). On a three-month moving average basis, core prices are up 3.4% (annualized), a noticeable breakout from the past several years. As much as it is a sign that a hot economy, rising prices also reflect the impact of tariffs. Core goods prices were up 0.8% (y/y) in August, the fastest gain in over seven years.

Trump’s admonishment of the Fed came prior to the ECB’s decision on Wednesday to lower its deposit rate by 10 basis points to a new low of negative 0.5%. The ECB’s decision, however, is a reflection not of economic strength, but of weakness. Right on cue, data showed Euro area industrial production pulled back by 0.4% in July. Inflation in Europe is also lower than in the U.S., hovering close to the 1% mark. The serial disappointment on inflation led the ECB to announce a plan to leave rates unchanged “until it has seen the inflation outlook robustly converge” to its target. President Draghi, in his press conference, said that the ball is now in fiscal policy’s court and expressed hope that governments would respond with additional spending to support the economy and return inflation to target.

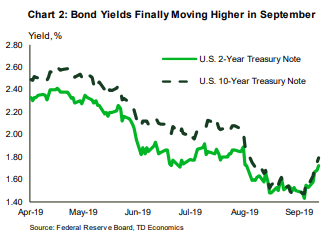

With inflation showing a bit more momentum and signs that an ever-worsening trade war may not be the most likely outcome, bond investors may be starting to reassess just how low the Fed will go. Yields have rebounded through the month of September (Chart 2) and providing the economy can avoid a recession, some further increases may still be ahead.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 30, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- US-China trade tensions spiked last Friday as both countries announced more protectionist measures against each other, but later eased this week. Equity markets swept the escalation under the rug, making a full recovery on the week.

- Second-quarter U.S. GDP growth was little changed in a second reading, but consumption was revised up to an even better 4.7% annualized. Real spending was up 0.4% m/m in July, making for a solid start to third-quarter consumption.

- A cloud of uncertainty continues to weigh on the global economic outlook. The odds of a no-deal Brexit have increased following a planned shutdown of the UK’s Parliament from September 9th to mid-October. Meanwhile, parties are scrambling in Italy to form a new government, but the potential new coalition government stands on shaky footing.

Uncertainty Still Name of The Game

Equity markets shrugged off last Friday’s escalation, making a slow but full recovery on the week. Yet, there are strong indications that the trade conflict is a long way from being resolved. China clarified this week that products listed more than once in its three retaliatory rounds would in fact face a cumulative tariff rate. This would bring the tariff rate to 30% or higher for some imported U.S. products, including some autos and parts. On the other hand, the U.S. is still pushing ahead with an increase in the tariff rate from 10% to 15% that will affect $125bn in goods starting this Sunday. Altogether, these steps may jeopardize progress in talks scheduled for September.

A veil of uncertainty continues to weigh on the broader global economic outlook. In Latin America, the Argentine peso severely weakened as the country remains in economic crisis and on the brink of default. Meanwhile, across the pond, the UK’s parliament is set to be suspended for a few weeks at the request of PM Johnson in an effort to make an unimpeded final push for Brexit before the October 31st deadline. Next week will likely prove to be a tumultuous Parliamentary session that could see a vote of no-confidence put forward by the opposition Labour leader, and an election call possible before the week ends. A snap election could delay Brexit further. Meanwhile in Italy, two parties are attempting to form a new coalition after the Northern League pulled out of the ruling coalition government. A prospective new alliance between an anti-establishment and a center-left party appears to stand on shaky ground. Moreover, opinion polls indicate that the the Northern League remains the most popular party, so the tide could again turn quickly. It’s clear to see that uncertainty is still the name of the game.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

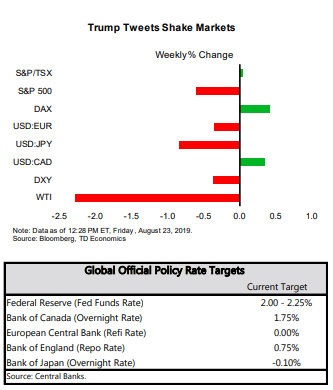

Financial News for the Week of August 23, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- This week may have been short on economic data, but the fireworks were lit on Friday as the President lashed out against China’s decision to impose tariffs on $75 billion of U.S. imports, sending stock markets into a tailspin.

- Risks increased, and global outlook has darkened since the Fed’s last meeting in July. Chair Powell acknowledged this at Jackson Hole, saying the Fed “will act as appropriate to sustain the expansion.” We anticipate two additional cuts will be needed this year to cushion the economy.

- The lone data release, existing home sales, was positive, with sales rising 2.5% in July and up 9.9% since January’s trough.

Markets on Edge as Recession Risks Rise

Earlier this week, the Fed’s minutes revealed that while the majority of the FOMC members supported the July rate cut as a “prudent step from a risk-management perspective,” there was a diversity of views among members. We already knew that two voting members dissented, but the minutes showed that those in favor of cuts citing different reasons for monetary easing ranging from low inflation to headwinds from trade tensions and insurance against slowing global growth.

Rather than abating, those risks have increased since July. Today, China responded to the U.S.’s latest tariff escalation by announcing 5%-10% on the remaining $75 billion of the U.S. imports. While the 10% tariff doesn’t seem like it would kick the chair out from under the global economy, as we argue in our recent report, this recent tit-for-tat escalation between China and the U.S. may be the last straw that damages business and market confidence beyond the point of no-return.

In concert, the global outlook has darkened since the Fed’s last meeting. Global growth is now tracking 2.9% - the slowest pace in a decade (Chart 1). Global manufacturing PMIs have remained weak, and geopolitical risks, such as the no-deal Brexit, have intensified. Consumer sentiment levels in Europe are also low, consistent with levels that have historically preceded a recession. All in all, there is little surprise bond markets continue to flash warning signs, with the spread between the 10-year and 2-year Treasuries briefly turning negative again this week.

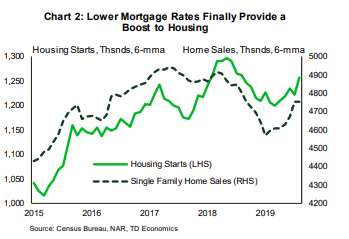

In the one economic footnote to a week that is ending dramatically, the existing home sales data was positive. Sales rose 2.5% to 5.42 million in July and are now up 9.9% from their trough in January, evidence that the more than 100 basis point decline in mortgage rates is helping to revive demand (Chart 2).

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

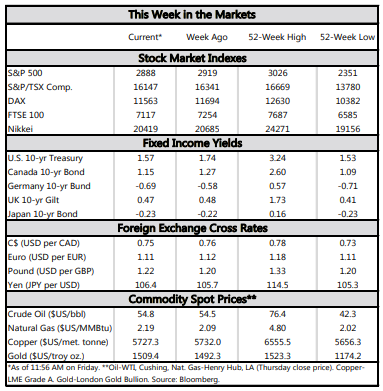

Financial News for the Week of August 16, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- There was no summer vacation from financial market volatility this week as investors were increasingly worried that the global economy is about to slip into recession.

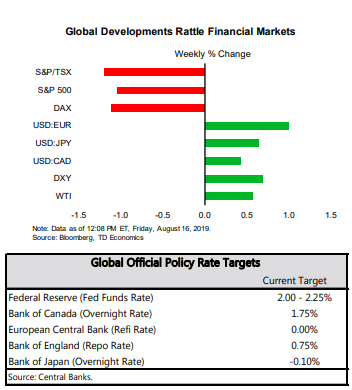

- The difference between the 10 and 2-Year Treasury yields turned briefly negative this week, sending a signal that bond investors expect the economy to get worse before it gets better. While the risks of a recession have risen, we are not there yet.

- The U.S. data was mixed this week, with evidence that tariffs are impacting prices and the factory sector. Consumers continue to be the bright spot, and there were signs that housing may be firming too.

Markets on Edge as Recession Risks Rise

Notably, there is a long and variable lead time on the signal coming from the yield curve. Anywhere from one to two years in the case of the 1990, 2001 and 2008 experiences. The yield curve signals that bond investors expect the economy to get worse before it gets better, but it is not a definitive signal that a recession is imminent. As we discussed late last year (see Perspective) we look at a suite of indicators to see whether we are close to a recession. Our TD Leading Economic Index has deteriorated, but is not yet flashing recession (Chart 2). It is similar to the 2015-16 slowdown, when the Fed paused on its new tightening cycle due to global weakness.

All told, the risks of a recession have increased since the White House ratcheted up trade tensions with China. That said, we still expect the Fed to continue its risk management approach and cut rates another 25 basis points in September. The negative yield curve raises the probability that they take further action in the months ahead.

The manufacturing sector also continued to struggle in July. Factory production fell 0.4% in July and has been trending lower in 2019. Weaker foreign demand and elevated trade uncertainty is taking a toll on the sector (see report). Housing starts weren’t looking too hot either in July, although an increase in single-family starts, and in building permits were silver linings. This is in line with homebuilder confidence, which continued to improve in August after weakening at the end of 2018.

The bright light in an otherwise crummy week was the consumer. Retail sales were up more than expected in July, setting up consumer spending to be an impressive 3% in the third quarter, stronger than we had expected. If the global backdrop weakens more sharply than we expect, the consumer at least seems to be in a decent position to weather it.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 9, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- China responded to the threat of additional U.S. tariffs by halting agricultural purchases and allowing its currency to weaken beyond the psychologically important 7 yuan to the dollar level.

- Central banks around the world responded to the heightened risk posed by the spiraling trade war by proactively cutting policy interest rates.

- The U.S. services sector showed signs of cooling in July as the ISM non-manufacturing index declined to 53.7 from 55.1 the previous month.

As U.S. and China Dig in, Central Banks Ease

Heightened U.S.-China trade tensions continue to occupy the limelight. The fallout from last week’s Chinese tariff announcement by President Trump reverberated through the global economy. Last week, the President announced that the U.S. would be imposing a 10% tariff on the remaining Chinese imports previously untouched by tariffs starting September 1st. In response to the tariff threat, China’s currency weakened this week to below the psychologically important level of 7 yuan to the dollar. China also suspended purchases of U.S. agricultural products and has not ruled out placing tariffs on some U.S. imports.

Following the yuan’s depreciation, the U.S. Treasury Department officially designated China a currency manipulator. The action, though mostly symbolic, requires the U.S. to consult with the IMF to try to eliminate any unfair advantage for China from currency manipulation, and could result in further tariff increases in the future.

Amid the growing trade worries, three central banks in the Asia-Pacific region (India, Thailand, New Zealand and the Philippines) proactively lowered interest rates this week. These actions are consistent with the expectation that the global rate-cutting cycle will intensify in the months ahead as the U.S. and China dig in for an extended battle. Meanwhile, despite the Fed delivering on an insurance rate cut last week, the market continues to expect further cuts in September as odds of a recession lurch higher.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 2, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Financial markets plunged after mixed messaging by the Federal Reserve, and later a 10% tariff on all remaining imported Chinese goods was announced to take effect in September.

- The Federal Reserve cut its policy rate by 25 basis points this week, but markets were unhappy with the lack of commitment to cut more if necessary.

- Slowing global economic growth and past tariff actions suggest that another cut is likely in September. However, escalating trade tensions may require even lower interest rates to help cushion the fallout.

The Fed is Not Done Cutting Rates

Tackling these two events separately, financial markets wanted more clarity on the Fed’s commitment to further rate cuts. First off, many were puzzled as to why rates were cut at all given the solid performance of the U.S. economy. The data this week confirmed that global developments had yet to take a significant toll on domestic economic activity. July payrolls came in as expected, with 164k jobs created, and wage growth firmed up slightly to 3.2% y/y. What’s more, consumer spending for June expanded at a healthy pace, and core inflation registered a slight improvement. Lastly, although motor vehicle sales slowed to a 16.9 million annual pace in July, this remains in line with expectations for 2019 as a whole.

The reason why the Fed is cutting is simple. The data reflects past performance, and forward-looking surveys offer a slightly less favorable outlook. For example, July’s ISM manufacturing survey again edged down and is close to tipping into contraction. Moreover, growth in world GDP is strongly correlated with domestic business investment with a short lag (Chart 1). As a result, the half-point decline in global growth since last year has weighed on business investment enough to shave about a tenth of a point off U.S. growth.

With no end in sight for trade tensions, any larger-than-anticipated negative impact on consumer spending, confidence and business investment would likely call for even lower interest rates to help support U.S. economic growth.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of July 26, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets had no summer vacation this week, with a new British PM, dovish message from the European Central Bank, and new U.S. GDP data to digest.

- Advanced economy central banks are all sounding dovish, with the Bank of England likely to be more cautious next week now that the risks of a disorderly Brexit have risen.

- Second quarter GDP data showed that U.S. domestic growth remained solid in Q2. But the Fed is likely more concerned with weakness in investment and exports as it prepares to cut rates next week.

Summertime and the Policy’s Easy

Former London mayor Boris Johnson is now Britain’s Prime Minister. Johnson faces an Oct 31st deadline to either leave the EU under the terms of the agreement negotiated by Theresa May, or face a disorderly exit without a deal. The EU had agreed that a UK election would trigger an automatic extension to this deadline, but so far the new PM says an election is off the table. How PM Johnson threads the needle on this one remains to be seen, but it is likely to be a wild ride similar to this past spring. Overall, the odds of a hard Brexit have ticked up in the last two months, and we expect the Bank of England to step back from a hiking bias at its decision next week.

The European Central Bank also hinted at easier monetary policy ahead. Further data this week pointed to a sagging European economy in the second half of the year. Consumer and business confidence have not rebounded from lows consistent with past recessions. Morever, the slump in manufacturing activity is broadening into other regions and industries. This is bad news, as it could trigger a broader pullback on spending, locking in a downward cycle.

Today’s GDP report (Chart 2) showed that second quarter growth was supported by strong consumer spending. But, the Fed is likely most concerned about the slowdown in investment and the weakness in exports. For now, the consumer is strong enough to keep economic growth sturdy. And now the U.S. economy looks to get a helping hand from Washington. Congress recently agreed to suspend the debt ceiling until after the next election, and raised the spending caps, removing a key fiscal risk this fall. In fact, spending has been raised slightly higher than we assumed in our forecast, presenting a slight upside risk to growth in 2020.

Monetary policy is set to get a little easier both in the U.S. and abroad, and now U.S. fiscal policy is looking a little easier too. These factors should support growth heading into 2020 just as it was starting to look like the edges of the expansion were fraying. This seems to have put markets in a relaxed mood, just in time for summer vacations.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.