Financial News for the Week of December 20, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

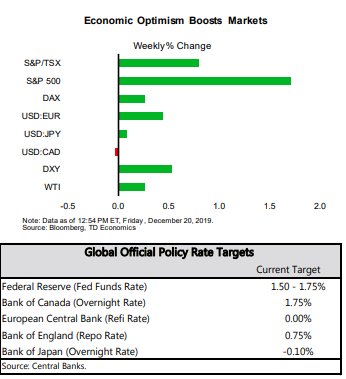

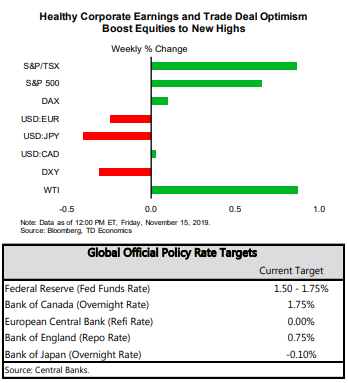

- The House’s impeachment of President Trump did little to detract from broader economic optimism. U.S. equity markets reached new highs this week.

- Housing and consumer spending data released this week confirmed the narrative of resilient U.S. household demand.

- Hopefully the recent progress on Brexit and U.S.-China trade relations are signs that headwinds to global growth will diminish in the New Year, giving the global economy a necessary jolt of goods news after a somber 2019.

Hope for Good Tidings in 2020

Data received this week remained consistent with the narrative of household resilience. November housing starts beat forecasts for a more subdued increase. Both single family and multi-family units rose in the month. Moreover, permits – a leading indicator of residential construction activity – improved for the seventh consecutive month. Housing starts have risen and persisted above the rate of household formation for several months, and all signs point to this trend holding into early next year as well.

The signal of health from existing home sales was a little less positive. November sales fell 1.7%, bringing the level back to a still healthy 5.35 million units annualized. Improved affordability, largely due to a decline in borrowing costs, has been a major driver for the recovery in existing home sales in the second half of this year (Chart 1). However, a dearth of inventory in many regions has put upward pressure on prices lately, tempering strong demand.

Consumer spending on goods and services plus housing form the key pillars of our U.S. outlook that foresees the economy expanding 2.0% next year, a slight cooldown from 2.3% this year. Underlying this view is that the labor market should continue to improve, absorbing more and more workers while wage growth is also expected to hold at fairly robust levels. Add lower interest rates and you get all the ingredients for household spending to rise at a sustainable clip in the year ahead.

Weak foreign demand combined with elevated economic uncertainty does not bode well for a quick recovery in global industrial production. Instead, it raises concerns about whether consumers worldwide will remain stalwart in the face of persistent uncertainty (Chart 2). The global economy this year is expected to grow 2.8%, the slowest pace in a decade. In the year ahead, we anticipate a slight uptick to 3% largely due to more supportive government policies. The hope is that the recent progress on Brexit and U.S.-China trade relations are signs that headwinds to growth will diminish in the New Year. The global economy could definitely use some good tidings after a somber 2019.

Fotios Raptis, Senior Economist | 416-982-2556

Financial News- December 20, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 13, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The U.S. and China reached a partial trade deal. The U.S. will reduce tariffs from 15% to 7.5% on $120 billion of Chinese imports and cancel the tariffs that were to be imposed on December 15th. In exchange, China will increase its imports of U.S. goods and services.

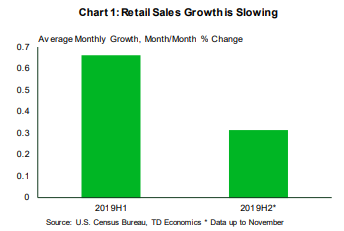

- American consumption remains healthy. While retail sales were soft in November, spending on services continues to be robust, leaving consumption tracking at 2-2.5% for the fourth quarter of 2019.

- The Conservative party won a majority in the UK election, paving the way for Brexit in January 2020. The next step of securing a trade deal with the EU will likely be more challenging.

Partial Trade Deal Cuts Tariffs

Details of the deal are still to come, but the Office of the United Stated Trade Representative stated that the U.S. will reduce tariffs from 15% to 7.5% on $120 billion of Chinese imports and cancel the tariffs that were to be imposed on December 15th. In exchange, China will substantially increase its imports of U.S. goods and services. We do not have any official figures on this, however. It is quite possible, that this “deal” is a head fake.

For the time being, with tariffs on Chinese consumer goods now off the table, U.S. retailers will be breathing sighs of relief, especially as retail sales growth has been slowing recently (Chart 1). Indeed, November data, released today, showed retail sales advanced by a soft 0.2% on a month-on-month basis. While spending on goods took a step down, consumption in services was buoyant in the third quarter. The Quarterly Services Survey had revenues in the services sector growing by 5.8% annualized. Overall, these data imply that consumption continues to drive the U.S. economy forward.

Even with all the vibrancy in spending, price pressures are muted. Consumer price inflation in November increased to 2.1% year-on-year from 1.8% in October, but this was mainly due to energy prices. Stripping out energy and food prices, core price inflation remained steady at 2.3%. Past tariffs, too, appear to be not have been fully passed through to consumers. This can be attributed to U.S. retailers absorbing higher prices, as well as a rising U.S. dollar (Chart 2).

The Conservative Party won a resounding majority in the United Kingdom election. With this result in hand, Prime Minister Boris Johnson should be able to lead the country out of the EU. Anticipating this outcome, the pound appreciated, and UK bond yields moved higher. But leaving the EU is only the first hurdle. Next on the agenda is for the parties to agree on a trade deal. This will likely lead to a messier second chapter of the Brexit saga (see commentary).

The end game on Brexit and the China-U.S. trade war remains uncertain. Even what seems like progress towards unwinding uncertainty, reveals more uncertainty. This will continue to be one of the key forces influencing the global outlook in 2020.

Sri Thanabalasingam, Economist | 416-413-3117

Financial News- December 13, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

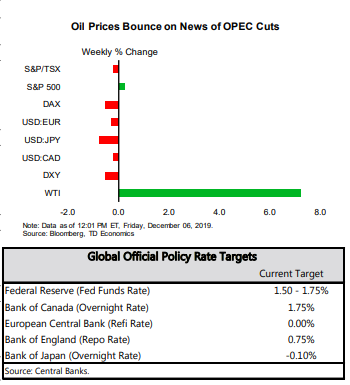

Financial News for the Week of December 6, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A Trade tensions reemerged this week. President Trump suggested that the U.S.-China deal could wait until after the election, announced steel and aluminum tariffs on Brazil and Argentina, and threatened to impose tariffs on France. International trade numbers were also unambiguously weak in October, even as trade deficit had narrowed.

- Despite uncertainty on the trade front, it was another banner month for America’s job market. Payrolls rose by a healthy 266k in November, with service sector hiring accelerating for the fourth consecutive month.

- Contraction in the manufacturing sector deepened slightly in November, with the ISM manufacturing index edging lower to 48.1 from 48.3. Service industries continued to expand, alas at a slightly slower pace than in a month prior.

Hiring Remains Solid Despite Trade Tensions

Equity markets rebounded toward the end of the week, amid news of Beijing reaffirming that the talks remain on track and the excellent job numbers. Oil prices rallied on the news that OPEC+ countries agreed to deepen existing production cuts, and Saudi Arabia promising to maintain its voluntary 400K bpd cut, bringing total cuts to 2.1 million bpd.

Trade data was not encouraging this week as trade volumes continued to slow in October. Export and import volumes declined for the second straight month. Since imports fell more than exports the U.S. trade deficit narrowed for the second month in a row, hardly a sign of health.

The services sector hasn’t been immune to trade-related headwinds, with the ISM non-manufacturing index edging 0.8 points lower to 53.9 in October. However, it remains well in expansionary territory, supported by resilient domestic demand. Two-thirds of non-manufacturing industries surveyed in October reported growth, compared to less than a third in the manufacturing survey (Chart 1).

This divergence of fortunes between the manufacturing and services sector continues to manifest in employment data. Payrolls expanded by an impressive 266k in November, with service industries contributing 206k to the headline. Businesses in the services sector have been ramping up hiring since July (Chart 2), while gains remain muted in the goods-producing sector, with the pop in November reflecting the end of the GM strike.

All in all, despite uncertainty on the trade front and softer global growth, the labor market has remained remarkably resilient. With reports like this, the FOMC can sit comfortably on the sidelines after cutting rates three times this year. As long as international risks do not intensify and hurt confidence domestically, the American economy will remain in expansion, supported by a healthy consumer.

Ksenia Bushmeneva, Economist | 416-308-7392

Financial News- December 6, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 29, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A quiet, holiday-shortened week featured data that painted a picture of an economy that has slowed, but not stalled. Revisions to Q2 GDP did little to change the picture of the economy.

- Durable goods orders were a bright spot, but the Fed’s manufacturing surveys continue to point to a lack of confidence on investment spending. The Beige Book echoed this two-speed view of struggles in the factory sector, and health elsewhere.

- The consumer remains an area of strength, with spending on track to put in a solid performance in Q4, helped by healthy advances in wages and salaries and benign inflation.

Something To Be Thankful For

Final domestic demand was 2% in Q3, after averaging 2.7% in the first half of the year, and 3% in 2018. That is the narrative right there. The economy has slowed from a robust pace to a moderate pace, very close to what we consider its underlying “trend”(Chart 1). The Fed’s latest Beige Book indicated that this tempo has likely continued this quarter. It characterized economic activity as progressing at a modest pace through most districts, unchanged relative to the prior report. Consumer related sectors, including residential construction, are doing well, while ongoing struggles in the manufacturing sector continued.

Durable goods orders for October painted a slightly better picture. Nondefense capital goods orders ex-aircraft, a key signpost to business investment, had a solid gain for the first time in a few months. It wasn’t enough to change our view of manufacturing weakness, but it did support an upgrade to expectations for equipment spending in Q4. Overall, we expect business investment to advance roughly 2.4%, ending two quarters of contraction. However, this does not entirely lift the damper uncertainty is having on investment (see report). Looking at the regional Fed manufacturing surveys, the capital expenditures components on the whole weakened further in November, so we don’t believe business spending or the manufacturing sector is out of the woods yet.

The Fed’s preferred inflation measure – the core PCE deflator – rose only 0.1% in October (Chart 2). The Dallas Fed’s trimmed mean (which strips out price volatility more broadly than food and energy) has been steady at the Fed’s 2% target for a few months. There’s little on the inflation front to spook the Fed to either cut or raise interest rates any time soon. Early in the week, Chair Powell highlighted the benefits of extending the current economic cycle – mainly that lower income households have not yet regained the wealth lost in the great recession. Strong labor markets are finally starting to spark healthy wage gains for lower-income workers, which spreads the gains from a strong economy more broadly. Amid all the trade gloom and uncertainty, that is something to be thankful for.

Leslie Preston, Senior Economist | 416-983-7053

Financial News- November 29, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

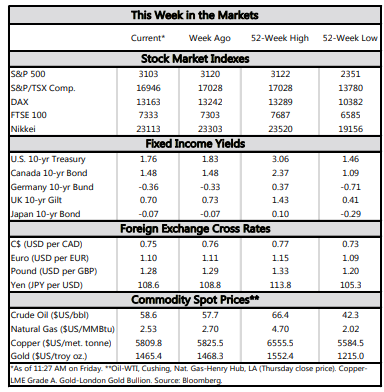

Financial News for the Week of November 22, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Stocks were volatile this week amid signs that U.S.-China trade talks may be stalling. Cautious optimism briefly returned on Friday on news that the Chinese president was calling for the two sides to “strengthen communication”.

- The housing data released this week was uniformly upbeat. Both construction (+3.8% m/m) and resale activity (+1.9% m/m) picked up in October, suggesting that the housing market was responding nicely to lower mortgage rates.

- The FOMC minutes revealed that most participants judged that three rate cuts left monetary policy sufficiently accommodative to meet the Fed’s objectives, suggesting the Fed is putting back on its “data-dependence” hat.

Housing Market Remained A Bright Spot in October

On the demand side, home sales continued to push higher, rising in three of the past four months as lower mortgages rates boosted affordability. In October, the National Association of Realtor’s affordability metric posted its strongest reading since the end of 2017 - a welcome development for prospective home buyers. That being said, without an equivalent response on the supply side, the latest improvement in affordability might prove fleeting. The already-low inventory of houses on the market has been declining year-over-year for four straight months. This has stymied additional activity and pushed home prices higher, with median home prices up 6.2% from a year ago – a significant acceleration from the roughly 3.5% pace seen at the start of the year.

While the housing market has recently emerged as a bright spot, business investment has been a drag on growth. Since last year businesses have found themselves in a deep fog of economic uncertainty brought about by volatile policy making and the U.S.-China trade war, making them reluctant to commit to new investment projects. As we discuss in our recent report, equipment spending – the largest component of business investment – has borne the brunt of the uncertainty impact (Chart 2), with the rise in uncertainty reducing equipment investment by an estimated 4% from 2018Q1 to 2019Q3. The resolution of the trade war could help boost investment. However, a sustained improvement will only be possible once firms are convinced that policy-making will not be as volatile as it has been over the last few years.

The minutes of the FOMC meeting last month revealed that members were also not expecting a quick turnaround in business investment, stating that “trade uncertainty and sluggish global growth would continue to dampen investment spending and exports.” Furthermore, officials have noted that while risks remained “tilted to the downside”, monetary policy was sufficiently accommodative to support outlook of “moderate growth, a strong labor market” and inflation near 2% target following three rate cuts this year. Thus, with regard to future monetary policy, the Fed is putting back on its “data-dependence” hat, and only a material change in the economic outlook will move it off the sidelines.

Ksenia Bushmeneva, Economist | 416-308-7392

Financial News- November 15, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 15, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S. data this week showcased the contrasting feature of the U.S. economy: a resilient U.S. consumer but a struggling manufacturing sector.

- Negotiations on a phase one trade deal between the U.S. and China took a step back this week as negotiators struggled to come to a compromise. A deal is unlikely to be signed before the end of this month.

- Inflation remained subdued as the high dollar, inventory stockpiling and margin compression offset the price increases implied by tariffs.

- With the economy evolving in line with their view, we believe the Fed has completed its mid-cycle adjustment.

Consumers Resilient Amid Manufacturing Struggles

Retail sales data released today showed that spending bounced back from a dip in September. Sales at non-store retailers, which includes online sellers, drove the increase. With the job market strong and consumers continuing to see solid gains in wages, consumption should remain healthy through the remainder of the year.

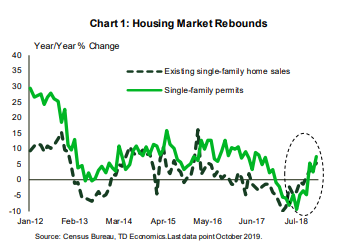

The manufacturing outlook isn’t as bright. Newly released production data indicated that manufacturing took another step down in October (Chart 1). The U.S.-China trade war and softer global economic conditions are clearly weighing on the sector. However, as noted in a recent report, it is unlikely that, the malaise in manufacturing can single-handedly trigger a recession, given its small and shrinking share of the U.S. economy.

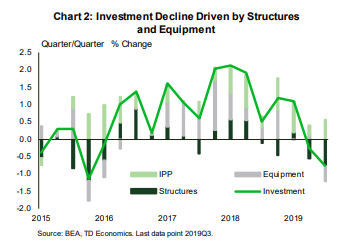

Although manufacturing weakened, we saw some improvement in small business confidence. The NFIB small business optimism index increased in October, with businesses signaling they will move forward with capital outlays in the months to come. This is a good sign for sputtering investment, which has contracted in the last two quarters as economic policy uncertainty spiked (Chart 2).

Much of this increase in uncertainty is coming from the U.S.-China trade war. There was some optimism last week that we might see the first deal in the conflict as the two sides edged towards a phase one mini-deal. It was even reported that the deal might be made official before the end of this month. However, it’s probably too early to pop the champagne. News emerged this week that officials were struggling to complete the deal. According to reports, China wants a greater reduction in tariffs, while U.S. officials do not believe China has made enough concessions to justify their removal. It’s probably a good idea to not hold our breath as we await the first breakthrough in this drawn-out saga.

Although trade uncertainty has made its way through the U.S. economy, it has yet to show up in overall price pressures. Indeed, despite the imposition of tariffs on many imported consumer goods from China in September, goods prices, which bear the brunt of the tariffs, on aggregate only rose by 0.3% on a year-over-year basis.

In addition to the rising U.S. dollar, other forces may be counteracting the price increases implied by tariffs. Elevated inventories for some consumer products are likely putting downward pressure on prices. There are also indications that importers are absorbing tariff impacts by compressing margins. The latter demonstrating how some U.S. firms are shouldering the burden of the trade war.

From the Federal Reserve’s perspective, the data are evolving largely in line with their economic forecasts. Inflation is at target and the consumption remains healthy. In addition, past rate cuts are moving through the economy, with the impacts most noticeable in housing. As we stated in an earlier report, without any further negative shocks, we believe the Fed has completed its mid-cycle adjustment.

Sri Thanabalasingam, Economist | 416-413-3117

Financial News- November 15, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 8, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- It was a relatively quiet week for economic data. The trade deficit narrowed a bit in September, but new tariffs appear to have weighed on both exports and imports. The ISM non-manufacturing index followed its manufacturing counterpart higher in October, with the recent trend indicating a stabilization in activity.

- Trade negotiations continued to dominate headlines. Comments from the U.S. Commerce Secretary suggest that the U.S. is likely to avoid a major escalation in trade tensions with Europe next week over autos.

- The interim U.S.-China trade deal is unlikely to be signed this month, but the mid-December tariffs still appear likely to be scrapped. Pres. Trump poured cold water on the notion that there was an agreement on removing existing tariffs.

The Deal With The Deal

The ISM non-manufacturing report, on the other hand, ushered in a bit of optimism. The headline index followed its manufacturing counterpart higher in October, with the improvement broad-based across the subcomponents. While a bit better than expected, the October uptick was not large enough to offset the decline in the month prior. As such, instead of a major strengthening in the pace of expansion, the recent trend is more indicative of a stabilization in activity (Chart 1).

Other second-tier data reports did little to rock the boat. Of note, job openings continued to edge lower in September, reinforcing the notion that appetite among U.S. employers for labor, while elevated, has waned a bit recently. The September data also affirmed that the pullback in job openings so far has limited geographic breadth, with recent pressures concentrated in the Midwest (Chart 2; for more see here).

When it came to China, developments were more capricious. For starters, contrary to initial hopes, the Trump-Xi meeting to sign the ‘Phase One’ trade deal is unlikely to happen this month. On the other hand, it appears likely that the tariffs that were slated to go into effect in mid-December will still be scrapped (provided that the interim deal remains on track to be signed in the near-term). China’s Commerce Ministry spokesperson suggested that the two economic heavyweights had agreed to roll back existing tariffs in phases as trade talks advanced. But this morning, President Trump poured cold water on the notion of such an agreement, while also stating that he will not fully eliminate tariffs on China. This softened some of the optimism that had built from China’s earlier announcement, highlighting the delicate and volatile nature of trade negotiations.

All in all, there are indeed signs of a de-escalation in trade tensions, which help dilute some of the near-term risk as economic activity shows signs of stabilizing. But, as today’s events have shown, we caution against reading too much into the recent optimism, for as long as core issues remain unaddressed, a re-escalation in the trade war remains a distinct possibility.

Admir Kolaj, Economist | 416-944-6318

Financial News for the week of Nov. 8, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

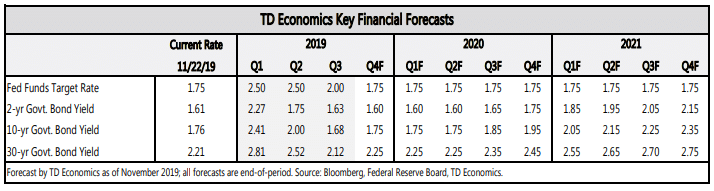

Financial News for the Week of November 1, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S. economic activity decelerated in the third quarter to a 1.9% annual pace from 2% in the second quarter, with consumer spending doing much of the heavy lifting.

- The Federal Reserve implemented its third, and likely final, interest rate cut of this year, citing muted inflation pressures and staid global developments. The bar for future rate cuts, however, has shifted higher

- PCE inflation continues to undershoot the Fed’s 2% target, with the headline measure at 1.3% year-on-year and core at 1.7%..

Consumers Step-Up, Businesses Pull-Back

Other big entries did not fare as well. Most notably, business investment declined for the second straight quarter (-3%), while net exports and inventories were minor drags. The falloff in business spending is the worst performance since late 2015, reflecting a confluence of factors ranging from slowing global growth, rising trade protectionism, and elevated policy uncertainty to appreciation of the U.S. currency. On the flipside, residential investment, having declined for six consecutive quarters, finally returned to positive territory, spurred by falling interest rates and high demand for homes.

The headline PCE price index rose 1.3% y/y in September, while the core measure, the Fed’s preferred inflation gauge, was up 1.7% - well below its 2% target (Chart 2). This allowed the Fed ample room to implement its third consecutive quarter point cut, lowering the fed funds target range to 1.50%-1.75%. Although some easing bias remains, the accompanying policy statement signaled a higher bar for future interest rate reductions. The two previous cuts appear to be paying off by giving a lift to household spending in the most interest rate sensitive areas, such as housing and autos. This outcome has helped to offset a slump in manufacturing. Encouragingly, that slump eased a bit in October, with the ISM manufacturing sentiment index ticking up to 48.3 from 47.8 in September (see report).

Across the pond, Britain not only got a Brexit extension but also an early election. The Brexit deadline was extended to Jan. 31, while British lawmakers voted to hold a December 12th election. This paves the way for one of the most unpredictable and divisive national ballots in Britain, but inches the Brexit issue closer to resolution.

Overall, it appears a healthy jobs market, supported by monetary easing is keeping Americans spending (though with less gusto than before), and helping to make up for a shortfall in business investment.

Shernette McLeod, Economist | 416-415-0413

Financial News- November 1, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

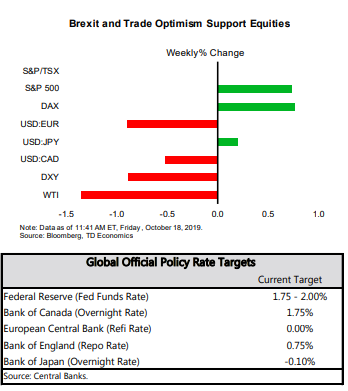

Financial News for the Week of October 18, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The economic data was subdued this week. Retail sales fell 0.3% in September, ending their six month growth streak. Industrial production also fell. Multifamily starts took a step back, but single-family starts fared better.

- The Fed’s Beige Book confirmed that economic activity has moderated in the period covering mid-August through September. Tariffs, prolonged uncertainty and slower global growth were deepening the manufacturing slump and pushing businesses to trim their growth outlooks.

- Internationally, the U.K. and the E.U. have agreed on the new Brexit deal, but the bigger hurdle of getting the deal through parliament still looms. Meanwhile, China’s economy grew 6.0% (y/y) in Q3, the slowest pace since 1992.

Economy Sends Mixed Signals

Across the pond, the U.K. and the E.U. have agreed on the new Brexit deal. The news boosted the British Pound to its highest level since May, even though the bigger hurdle of getting the deal through parliament this Saturday still looms. Meanwhile, Chinese GDP data reaffirmed that the U.S.-China trade war was weighing on economic growth. Real gross domestic product (GDP) rose 6.0% year-on-year (y/y) in the third quarter of 2019, a tenth of a point below market expectations, and the slowest pace since data collection began in 1992. “Synchronized slowdown” across major economies and slumping international trade has led the IMF to downgrade it’s global growth forecast for 2019 to 3% - down 0.2pp from its the previous release in July.

State-side, the economic data flow was mixed this week. September’s retail sales report showed that American shoppers appeared to have switched into a hibernation mode as cooler weather set in. Retail sales fell 0.3% in September, ending their six month growth streak (Chart 1). Even online sales took a breather, edging lower for the first time since last December. However, consumer activity remained healthy on a quarterly basis, with sales up 6% (annualized) in Q3. This leaves our third quarter tracking for consumer spending just shy of 3% - a downshift from the second quarter, but still a solid print. Still, with consumer spending currently being a key driver of economic growth as activity slows in other sectors, the decline in September will not escape the Fed’s attention ahead of the FOMC meeting at the end of the month.

These developments were corroborated by the Fed’s Beige Book this week. The report confirmed that economic activity has moderated in the period covering mid-August through September. Tariffs, prolonged uncertainty and slower global growth were deepening the manufacturing slump (echoed in the industrial production data this week) and are pushing businesses to trim their growth outlooks. The limited agreement between China and the U.S. reached last week is unlikely to do much for the business climate while tariffs remain in place. With no signs of stabilization in domestic economic backdrop, the Fed will likely continue to err on a side of caution, opting to support the economy with another interest rate cut this year.

Ksenia Bushmeneva, Economist | 416-308-7392

Financial News- October 18, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

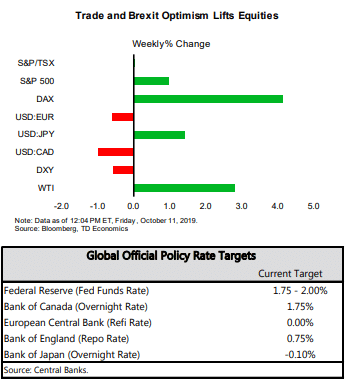

Financial News for the Week of October 11, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- CPI report - the only key data release this week - confirmed that inflation remained tame in September. Both headline and core inflation registered a muted 0.1% increase on the month, leaving the readings flat on a year-over-year basis.

- Meanwhile, the JOLTs survey showed that worker demand had softened over summer. The number of job openings fell in August on a year-on-year basis - a third drop in as many months.

- Unless a breakthrough in the U.S.- China trade impasse is reached later today, benign inflation and further signs of the domestic economy cooling off should lead to an even broader agreement for further monetary easing among the FOMC members when they meet later this month.

Fed Leaves the Door Open for Another Cut

The new leaders of the IMF and World Bank warned about the deteriorating global economic backdrop ahead of their annual meetings next week. The new head of the IMF, Kristalina Georgieva, said that the global economy is now in a “synchronized slowdown”, and that the IMF expects slower growth than last year in 90% of the world. The new head of the World Bank, David Malpass, in turn highlighted the long list of looming risks, such as “Brexit, Europe’s recession, and trade uncertainty,” which may lead to a further downgrade to their global growth estimate.

Chair Powell expressed similar concerns in his speech this week, acknowledging that the U.S. economy has slowed. He also reaffirmed that while the 50 basis point reduction in the fed funds rate so far is providing support, the FOMC committee will continue to assess incoming data signals on a meeting-by-meeting basis. The next meeting will take place at the end of October, and markets are expecting another quarter-point rate cut. Powell’s speech this week did not dispel those expectations, with the chairman reiterating that “policy is not on a preset course”.

Separately, the NFIB small business confidence index showed that businesses may be stuck between a rock-and-a-hard place, as they face rising costs (especially for labor), but are unable (or unwilling) to increase selling prices (Chart 2). Indeed, despite new tariffs coming into effect in September on many consumer goods, inflation remained tame. Both headline and core inflation registered a muted 0.1% increase on the month, leaving the readings flat on a year-over-year basis at 1.7% and 2.4%, respectively. Unless a breakthrough in the trade impasse is reached later today, benign inflation and further signs of the domestic economy cooling off should lead to even more agreement at the FOMC table for the need of at least another rate cut this year.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.