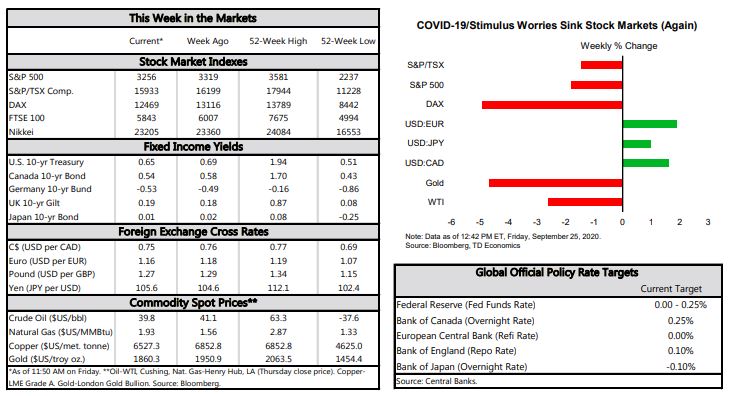

Financial News for the Week of September 25, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Major U.S. equity markets edged lower this week, extending their losing streak to four weeks. This came alongside an uptick in new COVID-19 cases and growing evidence that the economic recovery has shifted into lower gear.

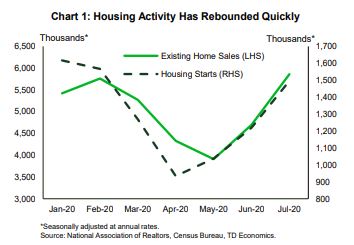

- Existing home sales rose by 2.4% to 6.0 million units (annualized) in August – another post-Great Recession record. New single-family home sales did even better, rising 4.8%.

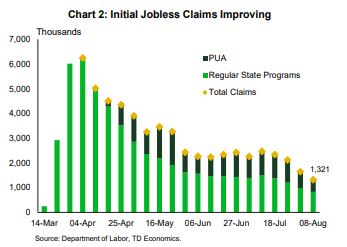

- The labor market is generally still moving in the right direction, but it is doing so at a slower pace. Initial jobless claims rose modestly to 870k last week, extending a flat trend just below 900k. On a more positive note, continuing claims continued to edge lower earlier in the month.

U.S. - More Evidence of Recovery Shifting into Slower Gear

On the data front, the housing market – one of the brightest areas of the U.S. the economy – continued to be a source of good news. Existing home sales rose by 2.4% in August to 6.0 million units (annualized), which marked another post-Great Recession record. The improvement spanned both single and multi-family segments and all four Census regions, though gains in the latter were concentrated in Northeast (13.8%). Meanwhile, in part due to a low inventory backdrop, home price growth accelerated sharply into double digit territory, with the median existing home price up over 11% in August relative to a year ago. New single-family home sales were even more impressive, rising 4.8% even after hitting the highest level in nearly 14 years in July. The level of new home sales has only been higher in the frenzied housing market of the mid-2000s that preceded the Great Recession (Chart 1).

As we argued in a recent publication, housing can’t remain divorced from the broader economy forever (see here). While we expect record-low interest rates to continue to support demand as the economy recovers, the acceleration in prices goes in the other direction. Diminished affordability will become a barrier to further increases. At the same time, the end of mortgage forbearance programs could result in more distressed sales in the quarters ahead. Finally, historically low population growth will weigh on demand growth once the initial recovery phase has played out.

All in all, the labor market is generally still moving in the right direction, but it is doing so at a much slower pace. The capricious nature of the health crisis remains a downside risk, with a still-elevated infection spread to continue weighing on the recovery (Chart 2). In the meantime, without additional income supports, spending could take a tumble as the high numbers of unemployed are forced to reduce consumption. With the Fed clearing up its stance (and limitations) on monetary policy last week, the ball is clearly in Congress’ hands. On this front, yesterday it was announced that Treasury Secretary Steven Mnuchin and House Speaker Nancy Pelosi have agreed to restart stimulus talks, in what marks a small positive step in the right direction.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Estate Planning Actions for the Small Business Owner

ESTATE PLANNING ACTIONS FOR THE SMALL BUSINESS OWNER

Two things people avoid talking about are death and money. Combining the two is estate planning—the process of arranging for the management and disposal of a person’s estate while minimizing gift, estate, generation skipping transfer, and income tax. Estate planning includes planning for incapacity, reducing or eliminating uncertainties over the administration of a probate, and maximizing the value of the estate by reducing taxes and other expenses.

Conversations about estate planning, though difficult, provide clarity and prevent conflicts. If you are a business owner, there are three estate planning conversations you should have.

CONSIDER

What You Want

Would you respond with a blank look if a friend asked, “What do you want your estate to do?” Do you think someone else should figure it out for you?

Remember this: Your estate is yours, no one else’s. Think about what your legacy will be from your point of view—not your childrens’, not your employees’, and not your friends’.

Estate planning is not just about splitting up the goodies. Your legacy is about what makes you unique, what wisdom you picked up over the years, and what you want to leave to those who are here after you die.

Of course, your exit strategy will be a significant portion of your estate planning. If you decide to sell or transfer ownership of your company, you’re making an important decision about your legacy as your company will live beyond your lifetime.

TALK

With Your Significant Other

If you’re clear on why you want certain things to happen, share them with your significant other. You and your life partner should have a real conversation about your reasons.

Don’t be surprised if there are some areas where you have different ideas. If both of you are clear on your reasons, it’s easier to find a resolution. If your reason is “just because,” then think harder. Consider those you’re leaving behind and the difference that your estate will make and the effect your exit strategy will have on their lives.

SHARE

Your Thoughts with Your Heirs

The next step is one that too few actually do. That is to sit down with your heirs and let them know what you think and why. Listen to what they have to say. Your decision will affect their lives and the way you’re remembered. If you care about either of these issues, having this conversation is really important. This gives you the opportunity to explain your reasoning behind your estate planning choices and helps those in your family learn about what your motives are and what you hope to accomplish.

Discussing your estate plan with your heirs also prevents unintended consequences. You might assume that the family business should be split equally between your children. However, this arrangement could end up in a major fight between children in the business and those who aren’t.

Clarity is what makes a good estate plan. You really want to ask lots of questions and have an open conversation about what you want. A well developed estate plan can alleviate the burden of probate on your heirs, and leave them without question about your intent.

ESTATE

Planning 101

After talking with your loved ones, you need to start framing your plan. To simplify this process, it can be helpful to consider three estate planning essentials: organizing your financial information, communicating your plans and, of course, taking action.

Organizing your financial and estate information

Create an organized record that details your accounts and legal documents, so your family can easily locate them. Include items such as:

- Professional and family contacts

- Location of estate documents

- Disability and life insurance

- Home and auto insurance

- List of financial institutions, accounts and account numbers

- Credit cards

- Beneficiaries of retirement accounts

- User names and passwords (including those to social media websites or online photo storage)

We tell ourselves we can get organized later, when things finally calm down. But sometimes later can be too late. Most people believe they will live a long and healthy life, but one never knows. A major illness or death may occur before plans are in order, leaving loved ones scrambling to make sense of incomplete information and financial unknowns during a very stressful time.

Discussing your estate plan with family members

Any time you update your estate documents, communication is key. When you name your friends or family members to any role in your plan, you should notify them right away. Confirm that they are willing to take on the responsibilities of the roles, and explain your intentions.

Discussing these matters with children can be sensitive. Here are tips on how to make the conversations age appropriate:

For children in high school and college, let them know that you have plans in place. Tell them who you name to important roles (grandparents, aunts and uncles) and why.

For young adult children, you may choose to name them to primary roles in your documents. Let them know if you plan to do so, and show openness to engaging them in this discussion in the years to come.

As children reach middle age, giving them full knowledge of your financial situation is important. Mature adult children can help parents navigate the challenges that come with aging.

Taking action

Proactive planning requires careful consideration of possible future scenarios and a good understanding of yourself and your family. It also involves communicating your wishes to those close to you.

Finding the time to discuss death and finances in your busy life is difficult and unpleasant. But since one never knows what the future holds, it is best to be prepared.

Have question? We can help! Call 704-237-4207.

“Estate Planning Actions For the Small Business Owner"ABM.https://abm.emaplan.com/ABM/api/v1/StoredFile/b5f0728a-a93d-4a93-bbc2-5e90da780740/downloadwnload

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of September 18, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- The Federal Reserve is not likely to increase interest rates until at least end-2023, however, this has not been enough to quench investors’ thirst for more liquidity.

- Retail sales strengthened for the fourth straight month this August, with several categories above or close to pre-pandemic levels of sales. However, the recovery momentum is fading.

- The labor market recovery has slowed with initial claims flattening at elevated levels. Almost 30 million people are still claiming unemployment benefits.

Canada

- Financial markets were mixed this week, with the S&P/TSX flat on the week. Meanwhile, oil markets received a boost from a bullish EIA inventory report and Thursday’s OPEC+ meeting.

- Economic data released this week continued to point to an ongoing recovery. However, improvements are uneven across the sectors. The highlight was the ongoing strength in resale housing markets that left sales 20% above their pre-pandemic levels.

- Meanwhile, soft CPI inflation readings for August (0.1% y/y) once again served as a reminder that slack remains in the

economy

U.S. – The Recovery Shifts In to Low Gear

On the economic front, the Federal Reserve indicated that there will be no interest rate increase until at least end-2023. The Fed said that it would not tighten policy until inflation is higher than 2% for “some time”, a move away from its previous policy goal of “maximum employment” and “symmetric 2% inflation”. This announcement makes the Fed’s desire to make up for past inflation underperformance more explicit. However, the Fed continued to remain vague on the period over which it seeks to achieve higher inflation. Despite the dovish stance, markets thought it wasn’t dovish enough. Equities slid, as investors were hoping for the Fed to magnify its QE by announcing the purchase of more government bonds.

In terms of economic data, retail sales strengthened for the fourth straight month in August with many of the major categories being very close to or even above their pre-pandemic level of sales (Chart 1). However, the momentum is fading as sales grew by a meagre 0.6% month-on-month in August, down from 0.9% in July. Cooling pent-up demand and a decline in income for a significant share of the population (due to CARES Act payments being stopped in end-July) may be responsible for this slowdown. However, the strength in retail has been uneven as it masks the continued weakness seen in clothing, restaurants and bars and department stores. It is important to keep in mind that some of the hardest-hit areas, especially high-touch services (recreation, childcare and haircuts etc.) are not included in these data.

Meanwhile, the labor market recovery has slowed down (Chart 2). Initial jobless claims (860k) were broadly around consensus, down 33k from last week. Continuing claims came in at 12.6 million, beating the consensus (13 million) and down 1 million. Moreover, the number of people collecting unemployment benefits edged higher in late August. At almost 30 million people, the total remains incredibly high. Job growth is expected to be slower through the remainder of the year, with a full labor market recovery not taking months, or quarters, but years.

Sohaib Shahid, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of September 11, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A wide dispersion of forecasts for U.S. growth over the next year reflects high levels of uncertainty around the duration of the health crisis as well as future government supports.

- Assuming a modest fiscal package passes Congress this fall and a vaccine becomes available by the middle of next year, the American economy should recover most of what was lost through the pandemic by the end of 2021.

- Inflation data showed an acceleration in price growth in August. Total CPI was up 1.3% year-on-year in August, continuing its recovery from only 0.1% in May.

A Wide Dispersion of Expectations for Recovery

This wide dispersion reflects the unprecedented level of uncertainty around the course of the pandemic, as well as its secondary economic impacts. This can be seen in the wide array of underlying assumptions among forecasters around items key to the outlook. For example: when and if a vaccine becomes available, how effective and permanent it will be, how much future government support will be provided.

We do not claim to have any better insight on these questions than other forecasters, but we have tried to make plausible assumptions to ground our forecast. In the case of the health questions, we assume that a vaccine or effective treatment becomes widely available by the second half of 2020.

Beyond the basic uncertainty around when and if we recover fully from the pandemic, we have little in the way of traditional macro models to gauge how consumers and businesses respond to health crises. This was true on the way down, but also on the way up. We can observe, based on recent data, that after an initial plunge, households have been more than willing to increase spending on durable goods – suggesting little permanent damage to household confidence. Rather, what’s holding back a broader recovery is service-sector areas of the economy where activity is directly impacted by the potential risk of infection. This offers reason to expect a fairly solid bounce back once these fears are allayed.

With these assumptions in place, and assuming no major second wave of the virus leads to another round of shutdowns, it is reasonable to expect the American economy to recover much of what was lost to the pandemic over the past year. While growth appears likely to slow after its initial burst on reopening, it should pick up again once a vaccine is available. Importantly, much of the deficit in spending is due to high-income individuals, who should be able to dip into these accumulated saving to support growth once the virus threat has passed. As a result, we expect the level of GDP to regain its pre-recession level by the first quarter of 2022. We will be publishing our full views on the economic outlook next week and hope you will give them a read.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of September 4, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- After reaching new highs early in the week, financial markets tumbled, driven by a broad sell-off in technology stocks. The S&P 500 is on track to end the week about 3% below last week’s close.

- The labor market recovery continued as the economy generated 1.4 million jobs in August, and the unemployment rate fell to 8.4%. However, the pace of the recovery has slowed from previous months, a theme that is echoed in other economic data.

- In speeches throughout the week, Fed officials warned about the fragility of the current recovery. They emphasized the importance of additional government help in supporting the recovery going forward.

Labor Market Mending Continues, but Risks Are Mounting

On the economic front, the main highlight was the release of the August employment data. As largely expected, the American economy continued to churn out jobs last month, albeit at a slower rate than in June and July (Chart 1). Indeed, August saw a total of 1.4 million net new jobs added, down from 1.7 million in July. Overall, nonfarm employment is about 7.6% below where it was in February. The unemployment rate also continued to trend lower, falling to 8.4% in August. While it has come down significantly since the apex of the crisis, it remains high by historical standards.

As unemployment fell, purchases of new vehicles jumped up 3.9% month/month in August (from 12.4% in July), to 15.2 million units. Meanwhile, the recovery in international trade progressed further in July, as exports rose by 8.1% (from 9.6% in June), and imports grew by 10.9% (from 4.6% in June).

Service industries also lost some momentum in August. The ISM Services Index declined by 1.2 points to 56.9, signaling that the pace at which the services sector is expanding is slowing (Chart 2). By contrast, the ISM Manufacturing Index recorded a surprise 1.8-point gain to 56.0. Despite the top-line increase, the details reveal an uneven recovery thus far, with many businesses still holding back on investment and hiring due to elevated uncertainty.

Given the still very high level of unemployment, the moratorium on residential evictions until the end of 2020 issued by the Center for Disease Control and Prevention (CDC) was a welcome development (it applies to individuals earning less than $99,000 per year). With pandemic-related uncertainty remaining elevated, near-term risks to the economy still appear tilted to the downside. As such, continued government support will be essential in limiting financial stress to households and businesses. This was emphasized by Fed officials in speeches throughout the week, noting that additional support will be key in determining the pace of the recovery. Considering stalled negotiations around the next stimulus package in Washington, consumption growth is at risk of tapering off in the coming months. It is going to be a long and bumpy road back to economic normalcy.

Johary Razafindratsita, Economist | 416-430-7126

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Business Succession Planning

Retiring Business Owners - Plan for Succession

If you’re a small business owner, you’ve invested a great deal of time and effort into building your company. With day-to-day demands, it may be difficult to imagine your eventual transition into retirement. Yet, if you want to build personal financial security and ensure business continuation, it is important to plan ahead. Business succession planning can help create retirement income for a retiring business owner and facilitate the transfer of operations and/or ownership to family or another entity. A succession plan can also provide a strategy to handle unforeseen events, such as death or disability.

Laying the Foundation

It is never too early to begin planning for succession. An early start can allow you ample time to develop an appropriate exit strategy, choose the right person to be your successor, and train your successor to manage the daily operations of your company. Consider the following points to create a foundation for a successful plan:

Business Valuation

A key aspect of planning for continuation is calculating the worth of your business. There are a variety of techniques for business valuation, and the most appropriate will depend on your business circumstances. A qualified professional can help you choose strategies for valuation.

Plan Your Exit Strategy

It is important for a retiring business owner to plan his or her departure from the day-to-day operations of the business. A solid plan can help ensure this transition will go smoothly, as well as facilitate the transfer of ownership.

Choose a Successor

If you plan to keep ownership and control of your business within your family, start by assessing your family members’ interests and qualifications, and how well they match the needs of the business. Discuss with family members who will participate in the company and in what capacity. Then, determine how working members will be compensated and what will be given to nonparticipating members.

If you expect unrelated parties to carry on the business, meet with the key people involved for an in-depth discussion about the company and its future. If succession involves the sale of the business, be prepared to address such issues as what the purchase price will be, how it will be paid, and when the succession plan will be activated.

Develop a Business Plan for the Future

Through your business plan, you can outline clear-cut, short-, medium-, and long-term business goals for your successor, along with an action plan for achieving them. Include budgets and financial forecasts that can be modified according to changing conditions in both the industry and the economy.

Choose a Transfer Strategy

Depending on the type of business, its value, and your personal financial situation and goals, determine the best ownership transfer strategy for your business. There are a variety of ways to structure and fund buy-sell agreements. For transfers to family members or charity, gifting may be an appropriate option. Consult your tax and legal professionals for specific guidance.

Plan for Contingencies

Regardless of your intentions for succession, it can be helpful to compile current information in case an unforeseen event, such as a death or disability, occurs before you have finalized your succession plan. This information should include the following:

- A copy of your current business plan.

- Job descriptions for all positions within the company, including details regarding areas of responsibility and delegation of duties.

- A list of potential successors.

- A plan to ensure extensive “hands-on” training for your designated successor.

- An estate plan that addresses any Federal and state estate tax obligations.

Other Considerations

A comprehensive succession plan involves strategies to handle a number of financial, legal, and tax issues. For instance, how will a successor secure funds to buy out a retiring, deceased, or disabled owner’s share of the business? What are the estate planning issues? How can an owner minimize gift taxes resulting from the transfer of company stock to family members? Such situations can be addressed in a succession plan, with the guidance of qualified legal, tax, financial, and insurance professionals. You owe it to yourself to ensure that your business will continue to flourish after your retirement, as well as in the event of death or disability. Proper planning through a business succession plan can help provide long-term security for your retirement, your company’s future, and your family.

Not sure where to begin? Contact Aventus Advisors for help at (704) 237- 4207.

“Retiring Business Owners - Plan for Succession"Fmex 2017. https://abm.emaplan.com/ABM/api/v1/StoredFile/cda87305-6b3e-4794-9498-0552159efdd9/download

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of August 28, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Federal Reserve Chair Powell unveiled a change in the Fed’s monetary policy strategy, announcing that it will target an inflation rate “that averages 2% over time” (instead of a strict 2% goal), and that it will be concerned with shortfalls of employment from its maximum level (rather than deviations). Taken together, these mean a bias to keeping rates on hold well after economic recovery sets in.

- Personal income and spending data this week showed continued, albeit slowing progress in recovering from the pandemic-induced shock earlier this year. Real personal spending rose 1.6% in July down from 5.7% in June. Total spending is still 4.9% below its pre-recession peak, with the deficit entirely due to spending on services.

Federal Reserve Flips the Script, Targets Average Inflation

It’s not just the health crisis that has complicated the Federal Reserve’s task of achieving maximum employment and price stability (which it interprets as an inflation rate close to 2%). Its traditional policy lever – the fed funds rate – is consistently impaired by the effective lower bound. Once it cuts to near-zero, it must turn to less traditional tools such as large scale asset purchases. At the same time, the relationships between economic variables that it relied on to achieve its mandate appears to have weakened. A hot labor market does not seem to put upward pressure on inflation the way it seemed to in the past.

Faced with challenges to achieving its goals, the Federal Reserve has decided a chance of tack is necessary. Nothing too revolutionary of course, but a recognition that it should be more concerned with employment undershooting its goal than outperforming it. At the same time, having consistently over-predicted the future path of inflation over the past decade, it has come to the view that it should be less concerned about overshooting its 2% objective. So, rather than targeting a forecast of 2% inflation, it will target a rate that includes the recent past – an average inflation target. In other words, if inflation has underperformed, due, for example, to a period of economic weakness, it will not immediately tighten policy even if inflation pushes higher than 2%.

Still, the reaction in markets to the statement has been positive so far. Stock markets rallied on the news. This makes some sense. Taken at face value, the fed funds rate are likely to remain lower for even longer.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 21, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The housing market continues to exceed expectations. Existing home sales and starts rose by 24.7% m/m and 22.6%, respectfully in July. Existing home sales are now 8% above January levels while starts are 7% below the pre-pandemic peak.

- The labor market recovery, meanwhile, appears to be losing steam. Initial and continuing jobless claims are settling at high levels suggesting more modest job gains in August compared to previous months.

- The Federal Reserve is wrapping up its comprehensive monetary policy framework review. Chairman Powell will provide an update next week at the Jackson Hole Symposium.

Markets Optimistic Despite No Deal Yet from Washington

On the economic data front, housing activity continued to exceed expectations. Both housing starts and existing home sales trounced market forecasts in July, rising by 22.6% and 24.7% month-on-month, respectfully. Starts are now just 7% below their pre-pandemic peak (January), while existing home sales are 8% above January levels (Chart 1).

The housing market has been a bright spot for the U.S. economy during this pandemic. Record-low mortgage rates have had a magnetic pull on prospective buyers, especially millennial who have held-off purchasing a home due to affordability constraints (see report). This has given homebuilders the confidence to resume construction at extraordinary speed.

Looking ahead, the housing outlook depends on the labor market recovery. Prospective buyers will need the income to take the plunge into homeownership, but a wobbling labor market could delay their plans.

With the labor market hitting speed bumps, the onus is on policymakers to provide additional support to households and businesses that are struggling due to the pandemic. Congress has been deadlocked on the next set of fiscal measures, with the Democrats pushing for more income support and Republicans arguing for less. It is clear, however, that more aid will be needed to avoid deepening the economic crisis.

This sentiment was the key discussion point among Federal Open Market Committee (FOMC) members. As noted in the minutes from July, participants zeroed in on the importance of fiscal policy in holding up spending, investment, and the labor market until a vaccine or effective treatment is found. A significant downside risk to the economic outlook is if fiscal support disappoints. At the current juncture, this seems to be a very real possibility.

In terms of monetary policy, several FOMC participants agreed that without convincing fiscal support, more stimulus may be needed to promote the economic recovery. They debated the use of forward guidance and yield curve control, with the former getting more attention among members. Fed Chairman Jerome Powell will likely provide more insight into these issues as well the broader wrap up of the comprehensive monetary policy framework review next week at the Fed’s annual Jackson Hole Symposium.

Sri Thanabalasingam, Senior Economist | 416-413-3117

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Could the Roth 401(k) Be Right For You?

Could the Roth 401(k) Be Right For You?

Understanding the differences between the traditional and Roth 401(k)

While the Federal government has created a number of tax-advantaged savings accounts designed to help lower- and middle-income workers save for retirement, these plans tend to be less useful for employees earning larger salaries.

But highly-compensated individuals currently not permitted to contribute to Roth IRAs, or younger workers expecting to be in higher tax brackets when they retire, stand to benefit when companies offer employees the option of contributing after-tax dollars to a type of plan called the “Roth 401(k).”

As the name suggests, the Roth 401(k) incorporates elements of both traditional 401(k) plans and Roth IRAs. Included in the Economic Growth and Tax Relief Reconciliation Act of 2001, the Roth 401(k) allows workers to make Roth IRA-type contributions to 401(k) plans, but without the income restrictions and contribution limits that apply to Roth IRAs.

Contribution Guidelines

Contributions to a Roth IRA are nondeductible, but earnings accumulate tax free, and qualifying distributions are also tax free. Currently, only taxpayers whose adjusted gross income falls below certain levels ($139,000 a year for single filers, and $206,000 for joint filers) are eligible to contribute after-tax dollars to a Roth IRA. These income limits do not apply to Roth 401(k)s.

Workers will also have the opportunity to save far more money in the new accounts than they could using Roth IRAs. The 2020 annual contribution limits for IRAs of all kinds are set at $6,000 for taxpayers under the age of 50, and $7,000 for older workers.

The Roth 401(k), in contrast, will be subject to the more generous elective salary deferral limits that apply to conventional 401(k)s – $19,500 for taxpayers under the age of 50, and $25,000 for older workers.

A Few Considerations

The Roth 401(k) has other advantages over the Roth IRA. Contributions are made through payroll deductions, rather than through separate arrangements with a bank. Because these plans are administered by employers, contributing to them should be more convenient for workers than opening an IRA. An employee who is currently contributing to a traditional 401(k) plan could, for example, simply opt to have his or her contributions diverted to a Roth version of the same plan.

Lawmakers have stipulated, however, that matching contributions made by employers must be invested in a traditional 401(k), not a Roth account. This means that, even if employees make all of their contributions exclusively to a Roth 401(k) account, they would still owe tax in retirement on withdrawals from funds contributed on a pre-tax basis by their employers.

Workers should also be aware that the 401(k) annual deferral limits apply to all 401(k) contributions, regardless of whether they are made on a pre-tax or after-tax basis. If employees contribute to a Roth 401(k), they may have to reduce or discontinue their contributions to their employer’s conventional 401(k) plan to avoid exceeding these limits. Provided employees comply with these limits, however, they are allowed to put money into both types of 401(k) plans.

In addition, employees considering the Roth 401(k) option should know that – like the 401(k), but unlike the Roth IRA – the Roth 401(k) will require them to begin taking distributions after the age of 70½. On the other hand, the Roth 401(k) resembles the Roth IRA in that investors will not be permitted to withdraw their money tax free until they have held the account for at least five years and are at least 59½ years old. The latter provision could make the Roth 401(k) less attractive to employees who are currently approaching retirement.

Have questions? We can help!

Wondering if a Roth 401(k) is right for you? Contact Aventus Advisors, we can answer your questions and help determine what is the best savings path for you.

“Could the Roth 401(k) Be Right For You?"Fmex 2019. https://abm.emaplan.com/ABM/api/v1/StoredFile/cda87305-6b3e-4794-9498-0552159efdd9/download

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of August 14, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets were in a good mood overall this week, despite no deal in Congress on the next round of assistance. The big political news was Biden’s historic VP pick. With 81 days until the election, the race is on!

- Inflation bounced back more quickly than expected in July, as pandemic related discounting rolled off. Core inflation at 1.6% year on year, remained unthreatening.

- Retail sales continued to improve, albeit by slightly less than analysts were expecting. The big increases due to pent up demand from the closures are in the past, but progress is still being made.

Markets Optimistic Despite No Deal Yet from Washington

On the economic data for July, inflation, as measured by the Consumer Price Index, rebounded more sharply than expected. Core inflation rose 0.6% month-over-month – the largest jump since 1991. The move was largely due to price hikes in areas that had seen significant discounting earlier in the pandemic, like motor vehicle insurance and airline fares (spending categories that also experienced steep declines in sales volumes). The acceleration in price growth has led some to raise the specter of stagflation – where higher inflation takes hold despite low growth. However, we think its bit early for that, given some of the volatility in various categories recently. Core inflation was up a modest 1.6% year-on-year in July, so there is still room for prices to normalize further before inflation gets anywhere near a level that is concerning for the Federal Reserve.

Retail sales continued to improve in July, rising 1.2% on the month. They came in below what markets were expecting, but even in the face of surging infections in many areas of the country, retailers continued to make progress. The pace of the rebound has slowed, now that the initial flurry of pent-up demand after the closures has played out. Many of the major categories are very close to or even above their pre-pandemic level of sales (Chart 1). The hardest hit categories are clothing, restaurants and bars and department stores. Restaurants and bars among the later businesses to open, and in some areas face renewed shutdowns. And demand for clothing is likely low, given many people are staying home in their sweatpants, (it has also been hit by the shift to online retailers).

This tally underscores the need for assistance from Washington. Many states’ unemployment benefit rates top out at very low levels: Florida at $275 per week and Arizona at $240 per week. Trump’s executive order funds $300 per week out of FEMA disaster relief funds. But that will likely only last about six weeks. Congress needs to act on another round of relief, particularly for state governments to forestall another round of layoffs at the state and local level which would weigh on growth over the medium term, similar to the dynamic as we saw in the 2010-2012 period.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.