Financial News for the Week of November 13, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Good news on the vaccine front cheered financial markets early in the week. However, as the week wore on and COVID-19 infections worsened, that optimism started to fray a bit.

- Many jurisdictions have increased restrictions as hospitals are feeling the impact. High frequency data are starting to show a loss of momentum, putting downside risk to fourth quarter economic growth.

- With inflation and interest rates low, now is the time for fiscal relief. Unfortunately, a deal in the lame duck session of Congress looks like a long shot.

U.S. – President-Elect Biden Has His Work Cut Out For Him

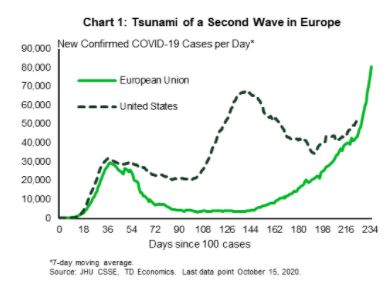

Good news on the vaccine front cheered financial markets early in the week. However, as the week wore on and COVID-19 infections worsened, that optimism started to fray. Vice President Biden was also declared President-Elect Biden over the weekend after a record-breaking voter turnout. But there is no time for him to bask in his victory. The third wave has been building speed for more than a month now and has led to increased restrictions as hospitalizations reach a new peak nationally, and in many areas are reaching the breaking point (Chart 1).

Restrictions are generally more targeted than the spring, but some jurisdictions are taking strong measures. Chicago has issued a 30-day “stay-at-home” advisory and Detroit is closing schools for two months. Many school systems in big cities, including Chicago and Philadelphia did not reopen for in-person learning in the fall, and will now be keeping students out of the classroom longer. Overall, six districts that re-opened in-person learning in the fall have since reversed course.

We economists are trying to sort out how much these restrictions will curtail spending, and economic growth. The second wave of infections in the summer did not lead to as much of slowdown as first feared. However, there are a couple of reasons why there may be more of an impact now. First, the current surge is more widespread across the country. The “second wave” was really a first wave in many states that were not hard hit in the early spring. Other regions’ case counts remained low through the summer, and were still gradually re-opening their economies, helping to keep up momentum on a national basis. The current more extensive surge seems more likely to show up in the national data.

Second, in the summer surge, Americans had recently received relief checks and people who were unemployed were still receiving a generous $600/week extra in addition to their usual benefits. This boost to income helped to offset reduced activity in some sectors. That is no longer the case, and Democrats and Republicans in Congress are still far apart on the size of a package. The need to pass a spending bill to fund government beyond December 11th presents an opportunity to tack on a relief package, but it looks like a Hail Mary pass at this point.

Still, there is a good case for additional fiscal supports. October’s CPI report showed continued softening in core services inflation, which typically reflects economic weakness more so than goods prices do (Chart 2). With unemployment still elevated and the pandemic worsening, we expect inflation pressures to remain subdued for quite some time, keeping borrowing costs low for Washington.

So far, the deterioration in the high-frequency data is modest. Weekly credit and debit card spending have started to lose momentum and passenger throughput at U.S. airports has fallen modestly for two consecutive weeks. We will be watching the weekly data closely to gauge momentum at year end. The fourth quarter got off to a strong start, and right now we are tracking a 3.7% (annualized) pace, but risks appear tilted to the downside.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 6, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Four days of vote counting has not yet produced a clear winner in the presidential election, with the Senate in a tight race and the House won by Democrats.

- There was no change to the policy announcement from the Federal Open Market Committee meeting, but policy makers remained consistent in their message of continued monetary support of the economy.

- The October jobs report was encouraging on all fronts with both employment and labor force increasing, the unemployment rate falling, and permanent layoffs easing.

U.S. - What a Year this Week Has Been

The week has been eventful enough to fill books. Limited to one page, let’s jump right into the presidential election where no winner has yet been announced. Friday morning, Biden took the lead in Georgia and Pennsylvania. Wins in these states would put him over the edge though legal challenges appear likely to leave a cloud of uncertainty over the outcome. Meanwhile, both of Georgia’s Senate races appear be heading to runoffs, making the Republican Senate majority less certain. What is certain is that Democrats retained control of the House with a smaller majority.

With the balance of power see-sawing away from a “blue-wave” outcome, U.S. equity and Treasury markets have also been volatile. Both markets took off on the morning after the election day, seemingly pricing in less fiscal support but also a lower probability of tax increases. The S&P 500 gained 6%, while 10-year Treasuries declined by almost 13 basis points. However, Friday morning markets retraced slightly as uncertainty about the outcome in the Senate increased (Chart 1).

The biggest question on investors minds with respect to government policy is the size and scope of the next fiscal support package. Assuming a Biden win and Republican Senate, the package is likely to be smaller than the roughly $2.5 million CARES act. Still, it is likely to reinstate enhanced unemployment insurance, authorize new funds for small business and provide sector-specific support. On international trade, a Biden victory is likely to mean a more conciliatory approach with America’s traditional allies but a continued assertive stance on China.

For his part, Federal Reserve Chairman Powell, made a point of not talking about the election though he could not avoid some mention of fiscal policy. On Thursday, the FOMC left policy unchanged and made very little changes to its policy statement. As in September, it emphasized downside risks, namely the increase in covid-19 infections across the U.S. In his press conference, Powell reiterated statements he has made many times in the past about the need for fiscal policy, noting that monetary policy can only go so far in dealing with the pandemic-induced shock to household and business income. In the meantime, the Fed will not let off the monetary policy gas pedal until the recovery is much more firmly entrenched.

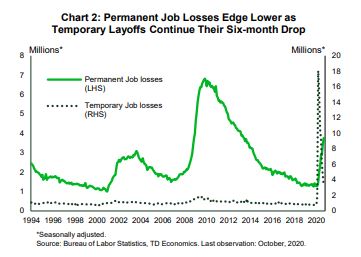

Amidst everything else, the week was also heavy on economic data, with Friday’s job report the main highlight. October nonfarm payrolls showed another month of solid gains, rising 638,000. The improvement in the unemployment rate was even more impressive, falling a full percentage point to 6.9% from 7.9%. Just as encouraging, the report showed a rebound in the labor force participation rate and decline in the permanent job losses. Permanent job losses have been rising in the past several months, flashing warning signs of employment fragility, so an improvement on this front is welcome (Chart 2).

Still, while ongoing progress is welcome it does not negate the need for additional fiscal support, especially as virus cases continue to rise and activity in high-contact areas to be scaled back. We hope to get more clarity on what the stimulus package may look like in the upcoming weeks.

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of October 30, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Financial markets tumbled this week as worsening coronavirus caseloads fueled concerns about the global economic outlook. The S&P 500 is on track to end the week 6% below last week’s close.

- The American economy rebounded sharply in the third quarter. Powered by consumer spending, real GDP increased at a 33.1% annualized rate, recovering two-thirds of the activity lost in the first half of the year.

- Boosted by supplemental payments for lost wages, personal income rebounded by 0.9% in September. Personal spending accelerated by 1.4%, while the personal saving rate remained elevated at 14.3%.

U.S. – Economic Growth Resumes in Q3

New COVID-19 cases are continuing to surge around the globe (Chart 1). Fresh daily records have prompted authorities in France and Germany to impose new lockdowns, which will notably include a month-long shutdown of bars and restaurants. Likewise, new infections are rising to new heights stateside. The overall U.S. case count crossed the 9 million mark this week, while hospitalizations are reaching levels that were last seen in August.

On the economic front, this week saw the release of real GDP data for the third quarter. As widely expected, the American economy rebounded sharply in Q3 following one of the steepest contractions on record in Q2. Economic growth accelerated at a 33.1% annualized pace (Chart 2), recovering about two-thirds of the activity lost in the first half of the year. Overall, real GDP is still 3.5% below where it was at the end of 2019. The rebound was largely powered by consumer spending (+40.7%), which was itself spearheaded by an impressive jump in durable goods spending (+82.2%). Services spending rose more modestly (+38.4%).

The remarkable recovery in the U.S. housing market was also front and center in the GDP report. Residential investment grew by 59.3% on account of expectation-defying strength in the resale market, and is now 5.1% above its pre-pandemic level. Other major GDP components also saw considerable increases with the exception of government spending, which fell by 4.5%. State and local governments, whose revenues have plummeted during the pandemic, reduced their expenditures (-3.2%) for the second straight quarter. Employment within these entities has contracted by 6% since February.

All things considered, the extraordinary pace of growth in the third quarter is unlikely to be sustained. Indeed, the splurge in durable goods spending over the summer is unlikely to be repeated, while the resurgence in new cases is placing the upswing in services spending in jeopardy. The looming expiration of eviction moratoriums across the country constitutes an additional downside risk to the near-term outlook.

With the election only a few days away, the focus will soon move back to the next installment of fiscal support. At a time when the pandemic continues to upend the livelihoods of millions, the importance of additional government support is hard to understate. Here’s hoping that Washington is able to deliver on this front, sooner rather than later.

Johary Razafindratsita, Economist | 416-430-7126

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

How to Maximize your Employee Benefits During Open Enrollment

How to Maximize your Employee Benefits During Open Enrollment

Reviewing your benefit choices to maximize what your employer offers

Open enrollment for employee benefits usually kicks off around November 1st. Before you plan your Thanksgiving menu, you should take the time to review your benefit choices.

Employee benefit experts expect benefits to change next year – given the rising costs of health care and the impact of COVID-19 on businesses this year. Even if little changed in your life in 2020, you should aim to maximize what your employer offers.

Here are a few pointers.

Medical

Even if you carry the same plan as in many past years, spend a few minutes evaluating which one is best for you and your family when you choose – especially High-Deductible Health Plans and traditional plans.

Switching from the traditional plan to a high-deductible option might save money if you don’t visit the doctor much. Perhaps too, your spouse’s company now offers a better plan and you can switch the family coverage to the better alternative.

Improved employer plan descriptions lay out plans’ differences and costs. Take advantage of their free help, online or in person.

Dental

Often you receive only one choice for dental coverage, but you might be surprised at how many people decline to pay the relatively small premium for this coverage. Even if young and cavity-free, you take care of your teeth now to potentially prevent large dental bills in retirement.

If nothing else, dental insurance provides teeth cleaning twice a year.

Vision

This benefit works great if you wear glasses or contacts and need regular eye exams. Those with perfect vision may opt out of this coverage.

Life Insurance

Most employers offer some basic life insurance, the coverage usually a multiple of your salary. If you are married, own a home, or have kids, this basic coverage usually falls short.

Consider paying extra if possible, to increase life coverage through your employer. If that’s not an option, consider supplementing this minimal coverage with a term policy from an independent provider. These policies come with set duration limits on coverage and you decide whether to renew once the policy expires.

Remember that whatever life coverage your employer pays for vanishes if you leave that company.

Long-Term Disability

Standard coverage in this category usually pays 60% to 66% of your compensation if you become disabled and unable to work.

As this coverage often comes with a cap, if you are highly compensated, this insurance might also fall short to sustain your standard of living. Estimate your minimum to live on if you become unable to work and, if that number scares you, consider purchasing a supplemental policy.

Long-Term Care Insurance

This pays for assisted living, nursing home, or in-home care late in your life.

Even as our lifespans increase, long-term care premiums escalate. If your employer offers any coverage at a relatively inexpensive group rate, consider locking in some protection. Financial advisors normally recommend LTCI when you turn age 50 – getting it while you are young and healthy under an employer plan may still make sense.

Flexible Spending Account

This savings account reduces your taxable income and funds medical co-pays, orthodontist appointments, and prescription drug orders, among other expenses.

Figure your out-of-pocket medical costs and sign up to set aside that amount, up to $3,550, pre-tax in an FSA, and $7,100 for families. Remember that if you participate in an HDHP, you maintain a related health savings account and can only take advantage of a limited FSA.

Either way, pay most out-of-pocket medical costs with pre-tax dollars

Dependent Care Flexible Spending Account

If you pay for daycare, after-school programs, or summer day camps for children under age 13 or for eldercare for a dependent parent, DCAs help you offset that cost with pre-tax dollars. Again, a working couple can set aside up to $5,000 from paychecks.

Life Planning Resources

This wide-ranging employee benefit is being offered more and more, from simple mental-health hotlines to complete menus of services.

For instance, if you lack a will, many companies now offer reduced-rate or even complimentary legal services to establish your basic estate planning documents. Others offer financial planning and weight-loss programs – sometimes even gym memberships.

How We Can Help

Finally, while your employer will offer resources to help you navigate the menu of employee benefits, it's important that you select benefits that best fit your needs and financial goals. At Aventus Advisors, our team of financial professionals can assist in selecting benefits that are consistent with your overall financial plan.

Click here to speak with an advisor today.

“Open Enrollment Season is Around the Corner". 2020. FMEXhttps://fmexcontent.s3.amazonaws.com/1289/1289.pdf

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of October 23, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Covid-19 infections continued to rise this week, nearing record highs set in July. Concerns regarding this trend weighed on markets, but progress on a new stimulus package helped improve the mood later in the week.

- Positive housing reports reinforced the sector’s position as a bright spot in the U.S. economy. Existing home sales soared 9.4% in September, blowing expectations out of the water, while price growth accelerated further.

- Fast-rising prices are good news for builders who have recognized the need to build more homes. Housing starts also pushed higher in September (+1.9%), with gains concentrated in the single-family segment.

U.S. - Housing Market Remains A Bright Spot

The September existing home sales report reinforced the notion that the housing market remains a bright spot, even as most sectors of the economy continue to struggle under the weight of the pandemic. After gains moderated in the two months prior, resale activity surged by 9.4% in September, blowing expectations out of the water. Sales are now at a new post-Great Recession high and nearly 14% above their pre-pandemic level (Chart 1). Details from the report suggested that the purchasing of homes in vacation destinations – a trend that appears to have been supported by an improved flexibility of working from home – played a part in boosting overall sales. While the latter are up 21% year-over-year (y/y), sales in vacation destination counties accelerated over the summer and are up 34% y/y according to the National Association of Realtors.

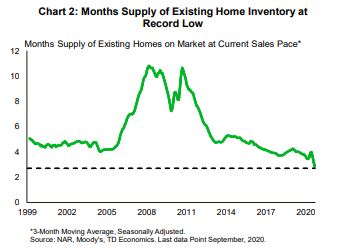

With low mortgage rates and a still-improving labor market, we expect resale activity to continue grinding higher, but at a more moderate pace. A sharp acceleration in home price growth is eroding affordability and a record-low supply of housing means that markets will remain tight. Housing inventory now sits at just 1.47 million or a record low of 2.7 months at the current sales pace (Chart 2). As a result, the median existing home price has accelerated to a sharp 15% y/y – the fastest pace since the “frothy” days of 2005.

The few remaining indicators pointed to a slowing economic recovery outside housing. Initial jobless claims fell by 55k to 787k last week – better than expected, but still slightly higher than at the start of the month. Meanwhile, continuing claims from all programs eased to a still-elevated 23.2 million at the start of the month (data is delayed). Anecdotal evidence from the Beige Book also pointed to a “slight to modest” pace of growth this fall. Coupled with the fact that the virus’ spread is nearing a record high, these elements support the case for added fiscal stimulus.

The outcome of the election, which is now a little over a week away, will have important implications for the economy (see here) and the amount of fiscal stimulus. So far, Joe Biden is leading in the polls. But, judging from what happened in 2016, it’s worth continuing to take these numbers with a grain of salt.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Retirement: Strategies for Saving in Your 50s

Countdown to Retirement: Strategies for Saving in Your 50s

Strategies for saving in your 50s

Many retirees today are redefining the “golden years.” Forget about endless days of leisure. Retirees seek adventure, travel, and new business pursuits. While these changes may redefine retirement, will retirees be able to finance their plans? Today, many people age 50 and older have not begun to save for retirement or have yet to accumulate sufficient funds.

If you’re in this age group and find yourself facing an underfunded retirement, it’s not too late to take charge. There are actions you can take today to get on the right track. Here are some retirement saving strategies:

What’s it going to take?

First, estimate how much money you will need in retirement. Once you have an idea of the amount, you can work toward meeting that goal. A good rule of thumb is that you may need 60%– 80% of your current annual income in retirement. Your financial professional can help you assess the best amount for your situation.

Maximize your contributions.

If your employer offers a retirement plan, contribute as much as the law will allow. In 2020, those age 50 and over can contribute up to $26,000 to an employer-sponsored 401(k) plan ($19,500 + $6,500 “catch-up” contribution). Many employers also offer a company match, so be sure you contribute enough to claim this “free” money, which can add up over time.

Create a spending plan.

In other words, make a budget. Many people think a budget is restrictive, but look at it this way: You can spend now, or you can have the money to afford your dream adventures later. To start, it is important that you pay down debt and avoid accruing new debt. Next, examine your spending habits and replace some of your discretionary spending with saving. Saving even $20 more per week is a step in the right direction.

Take initiative.

Besides contributing to your employer’s plan, you can save more by opening your own Roth IRA. Contributions are made after taxes, but earnings and distributions are income-tax free, provided the account is at least five years old and you have reached age 59½. Those age 50 and over can contribute up to $7,000 a year in 2020. Eligibility in 2020 for these plans begins to phase out with adjusted gross incomes of $124,000–$139,000 for single filers and $196,000–$206,000 for married joint filers.

Hang out your shingle.

Many Boomers hope to start their own businesses in retirement. Why wait? If you begin your entrepreneurial efforts now, your business has the potential to be in full swing by the time you retire, and any profits between now and then can be added to your savings.

Consider downsizing.

Your home may have significantly increased in value since you first bought it, and you may have already paid off the mortgage. With children at or near adulthood, do you really need all that space? Selling now and moving to a smaller, more affordable location may allow you to transfer some of the equity in your home into a savings vehicle.

Reconsider your retirement age.

If you want to cushion your retirement savings, consider staying on the job longer. Some people actually leave retirement to reenter the workforce because they feel more fulfilled while working. Others seek part-time work, consulting, or entrepreneurial endeavors. Such options may enable you to earn more money to save, which may help to postpone spending down your savings.

Regardless of which options you choose, you can benefit from time and compounding interest. Every year that your savings remain untouched allows more time for growth. It is never too late to start preparing for your future. So, take action now to get on track to saving for your retirement.

Have questions about your current retirement saving strategy? Give us a call at 704-237-4207 or contact us here.

“Countdown to Retirement: Strategies for Saving in Your 50s" 2018. Liberty Publishing, Inc. FMEX Editor.https://fmexcontent.s3.amazonaws.com/1289/1289.pdf

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of October 16, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Covid-19 infections are surging in much of the world, prompting new restrictions in Europe and dampening market sentiment early in the week.

- U.S. data painted a clear picture of pandemic life. Inflation pressures for services hard hit by social distancing have cooled notably.

- Meanwhile, American consumers continue to snap up goods that will help them to enjoy life at home. That strength in September retailing put markets in a better mood late in the week.

U.S. - Global Infections Surge

Earlier in the week, the IMF released their updated global forecast. It emphasized that the recovery will be long, uneven and uncertain. Their forecast contraction for 2020 (-4.4%) is slightly smaller than expected back in June, but the rebound is also shallower. So long as the pandemic is controlled next year, it expects the global economy to rebound 5.2%. Unfortunately, at the moment in many areas of the globe, the pandemic is far from controlled.

Infections have been on the upswing in Europe, where daily infections are well above their spring peaks, and have recently surpassed the U.S. (Chart 1). As a result, countries have imposed new restrictions to turn the tide, from curfews in France’s largest cities, to curbs on socializing indoors in London. New restrictions are more targeted relative to the spring, and therefore, the economic impact is likely to be much less severe. However, it still casts a pall over the outlook for Europe.

In the U.S., the latest inflation report should quiet the stagflation chatter that had emerged after a couple of hot months for core inflation. Both headline and core CPI rose a middling 0.2% in the month of September. However, removing an outsized 6.7% month/month increase in used vehicle prices leaves core inflation flat on the month.

The good news came from consumers, who ramped up their spending at retailers in September. Retail sales rose 1.9% on the month, driven by a big jump up in clothing purchases (+11% m/m), department stores (+9.7% m/m), sporting goods, hobby, book and music stores (+5.7% m/m) and vehicle sales (+3.6% m/m). There is some speculation that the strength in clothing may be due to the delayed back-to-school in many parts of the country. Even removing that influence, it was a strong month, and puts some upside risk to our forecast for consumer spending in the third and fourth quarter.

Like price patterns, the trend in retail sales also tells the tale of pandemic life (Chart 2). The hardest hit area is restaurants and bars, which have faced closures and restrictions. Since most consumers are staying home a lot more, there is also less of a need to get dressed up to go out, and even with September’s jump, clothing sales are below their pre-crisis level, as are department stores which would include a fair amount of clothing purchases. The strongest areas, apart from online shopping in general, are for things that make staying home a bit more appealing, such as new gym equipment or other hobbies and materials for home and garden improvement projects.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of October 9, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Fiscal policy (or lack thereof) drove much of the news cycle this week. On the same day the Federal Reserve Chair made the case for more fiscal support, President Trump tweeted that negotiations were being cut off.

- Trump changed his mind later in the week, and talks appear to have restarted. Still a deal will require the support of Senate Republicans, and with just over three weeks until the election, time is running out.

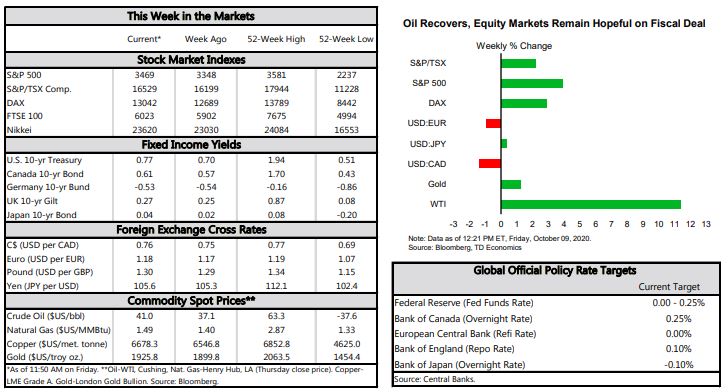

U.S. - Fiscal Deal or No Deal

Assuming a deal can be done between the Trump administration and the House Democrats, it may still have difficulty passing the Senate. On Friday, Senate Majority Leader, Mitch McConnell expressed his doubts, saying he still thought a deal was unlikely over the next three weeks.

For his part, Federal Reserve Chair Powell made a strong case for additional fiscal support in a speech this week. He noted that despite the rebound seen so far, the economy is still in a precarious state. Any slowing in the pace of recovery at this stage risks triggering “typical recessionary dynamics, as weakness feeds on weakness.” It would also exacerbate inequalities, a tragedy in the Fed chair’s view, “especially in light of our country’s progress on these issues in the years leading up to the pandemic.”

Indeed, there is much to laud in the fiscal policy response to date. Looking back on the last several months, the success of monetary and fiscal policy in supporting the recovery is everywhere to be seen in the economic data. The support to household income allowed for a swift recovery in goods consumption and production. Retail sales are now higher than pre-pandemic levels – a forecast few would have had a few months ago. While the recovery in service consumption has lagged, this is due to health crisis itself, which makes it impossible to go back to normal in close-contact businesses like restaurants, gyms, movie theatres.

For what its worth, our economic forecast assumed a modest fiscal deal that allows for another round of relief checks and additional unemployment benefits of $300 per week (half the amount under the CARES Act) to be delivered before the end of the year. This still seems possible – the fireworks this week notwithstanding – but if it does not occur, economic growth could get dangerously close to stall speed in the quarters ahead. Activity could still bounce back, particularly if a vaccine becomes widely available by mid-year, but the downside risks are clearly higher the longer it takes for policy makers to reach an agreement.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Why Should You Start Saving for Retirement Now?

Why Should You Start Saving for Retirement Now?

You are busy dealing with life’s day-to-day issues. To you, retirement may seem like a long way off. But preparing now for your financial future is essential because what you do today can help ensure a secure retirement tomorrow.

Although time may be on your side, there are four factors you will need to consider when planning for your retirement.

1. Inflation.

You may be aware that, over time, inflation can erode your savings. But, many people don’t realize the potentially serious effects of inflation. At 3% inflation, $100 today will be worth only $67.30 in 20 years—a loss of one-third of its value. At 35 years, this amount would be further reduced to just $34.44. Thus, it is important to seek retirement savings vehicles that have the best chance of outpacing inflation.

2. Taxes.

Your present income level, tax bracket, and the types of tax-deferred retirement savings plans that are available can all play an integral part in how much money you can save for retirement. By maximizing your pre-tax contributions to employer-sponsored plans and Individual Retirement Accounts (IRAs), you can take advantage of the tax-deferred benefits of such plans.

3. Compound Interest.

Becoming a disciplined saver is one of the key components of retirement plan success. By making regular contributions to your employer-sponsored retirement plan and your IRA, you can maximize the power of compound interest (the interest earned not only on the initial principal, but also on the accumulated interest from prior periods). With consistent contributions, your retirement savings have a greater chance of accumulating to meet your long-term goals.

4. Personal Savings.

Considering the effects of inflation, it is possible that your retirement plan income may fall short of your needs, especially during a long retirement. Furthermore, Social Security generally provides only a base level of retirement income. Thus, to avoid a potential shortfall, start planning to supplement your retirement income with personal savings.

While understanding these principles is no guarantee of future success, they can get you started down the right path. The sooner you recognize the effects that economic forces can have on your retirement income, the more likely you may be to adopt strategies that can help you achieve your long-term objectives. Being proactive today can help increase your retirement savings for tomorrow.

Have questions about your current retirement saving strategy? Give us a call at 704-237-4207 or contact us here.

“Why Should You Start Saving for Retirement Now?" 2018. Liberty Publishing, Inc. FMEX Editor.https://fmexcontent.s3.amazonaws.com/1289/1289.pdf

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of October 5, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Following a four-week losing streak, U.S. financial markets regained some gusto, buoyed by optimism on the prospect of a new stimulus package.

- The labor market continues to mend, albeit at a decelerating pace. The American economy added 661,000 payroll jobs in September, down from 1.5 million in August. Meanwhile, the unemployment rate fell to 7.9%, in part because of a pullback in the labor force participation rate.

- The House passed a $2.2 trillion coronavirus relief bill this week, but it will not pass the Senate. Talks between Speaker Pelosi and Treasury Secretary Mnuchin continue, but a deal has yet to be reached.

U.S. - Healing, but Slowing Labor Market

The release of employment data for the month of September was this week’s main economic highlight. The report showed ongoing, albeit decelerating progress in the labor market recovery. Indeed, 661,000 payroll jobs were added last month, down from 1.5 million in August. Overall, 51.5% of non-farm payrolls lost since the pandemic began have been recovered. The unemployment rate fell from 8.4% to 7.9% in September, a welcome improvement, but a markedly slower pace than in previous months. More concerning, the drop was due in large part to a pullback in the labor force participation rate (Chart 1) rather than strength in job growth.

The theme of a stalling labor market recovery was also borne out in the jobless claims data. Indeed, new filings for unemployment benefits have held stubbornly close to the 900,000 per week mark since the end of August, signaling that businesses continue to lay off workers at an elevated rate. While continuing claims have trended lower over the past few weeks, they remain well above pre-crisis levels.

Similar concerns were echoed in the September ISM Manufacturing report. The Index registered a worse-than-expected 0.6 point retreat to 55.4, pointing to a slower pace of expansion in the manufacturing sector. The details of the report showed a recovery that remains uneven, with a slew of industries continuing to contend with sluggish demand.

On a more positive note, new vehicles sales soared by 7.6% month/month in September to 16.3 million units. Alongside home sales, auto sales are one of the few economic indicators to have exhibited a “V-shaped” recovery and are now within 2.5% of their pre-crisis level from February.

All things considered, the balance of risks to the economic outlook remains tilted to the downside. The absence of a new stimulus package is beginning to take a toll on the recovery. Talks between House Speaker Pelosi and Treasury Secretary Mnuchin continued this week, but a deal has, so far, remained out of reach. Here’s hoping that Democrats and Republicans can close the gap and come to an agreement sooner rather than later.

Johary Razafindratsita, Economist | 416-430-7126

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.