Sick and Family Leave for the Self-Employed

Sick and Family Leave for the Self-Employed

New form available from the IRS to claim sick and family leave tax credits

The Bureau of Labor Statistics counts self-employment in different ways, but estimates that there are close to 10 million, with projections that this number will grow by 8% each year for the foreseeable future. And while much of the COVID-relief packages have been focused on businesses and families, little media attention has been paid to relief offered to those who are self-employed.

But in February of 2021, the Internal Revenue Service announced that a new form is available for eligible self-employed individuals to claim sick and family leave tax credits under the Families First Coronavirus Response Act.

Sick and Family Leave

According to the IRS:

“Credit for Sick and Family Leave. An employee who is unable to work (including telework) because of coronavirus quarantine or self-quarantine or has coronavirus symptoms and is seeking a medical diagnosis, is entitled to paid sick leave for up to ten days (up to 80 hours) at the employee’s regular rate of pay, or, if higher, the Federal minimum wage or any applicable State or local minimum wage, up to $511 per day, but no more than $5,110 in total.

Caring for someone with Coronavirus. An employee who is unable to work due to caring for someone with coronavirus, or caring for a child because the child’s school or place of care is closed, or the paid child care provider is unavailable due to the coronavirus, is entitled to paid sick leave for up to two weeks (up to 80 hours) at two-thirds the employee’s regular rate of pay or, if higher, the Federal minimum wage or any applicable State or local minimum wage, up to $200 per day, but no more than $2,000 in total.

Care for children due to daycare or school closure. An employee who is unable to work because of a need to care for a child whose school or place of care is closed or whose child care provider is unavailable due to the coronavirus, is also entitled to paid family and medical leave equal to two-thirds of the employee’s regular pay, up to $200 per day and $10,000 in total. Up to ten weeks of qualifying leave can be counted towards the family leave credit. “

For Self-Employed Individuals

The following are excerpts from the IRS press release:

“Eligible self-employed individuals will determine their qualified sick and family leave equivalent tax credits with the new IRS Form 7202, Credits for Sick Leave and Family Leave for Certain Self-Employed Individuals. They'll claim the tax credits on their 2020 Form 1040 for leave taken between April 1, 2020, and December 31, 2020, and on their 2021 Form 1040 for leave taken between January 1, 2021, and March 31, 2021.

The FFCRA, passed in March 2020, allows eligible self-employed individuals who, due to COVID-19 are unable to work or telework for reasons relating to their own health or to care for a family member to claim refundable tax credits to offset their federal income tax. The credits are equal to either their qualified sick leave or family leave equivalent amount, depending on circumstances. IRS.gov has instructions to help calculate the qualified sick leave equivalent amount and qualified family leave equivalent amount. Certain restrictions apply.

Who May File Form 7202

Eligible self-employed individuals must:

- Conduct a trade or business that qualifies as self-employed income, and

- Be eligible to receive qualified sick or family leave wages under the Emergency Paid Sick Leave Act or Emergency Family and Medical Leave Expansion Act as if the taxpayer was an employee.

Taxpayers must maintain appropriate documentation establishing their eligibility for the credits as an eligible self-employed individual.”

“Sick and Family Leave for Self- Employed". FMEX 2021 https://fmexcontent.s3.amazonaws.com/11856/11856.pdf

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

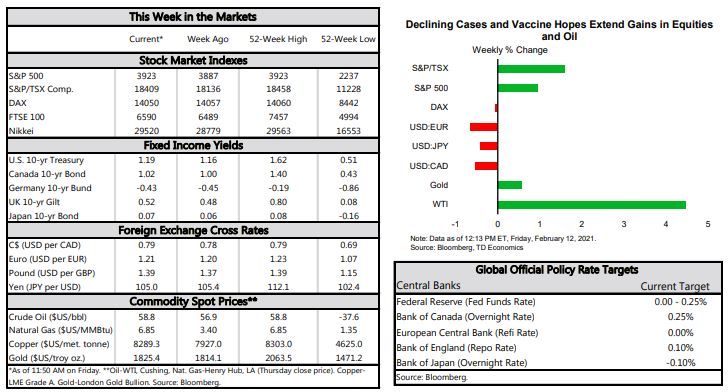

Financial News for the Week of February 12, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

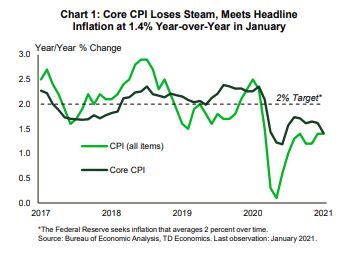

- The headline Consumer Price Index rose 0.3% in January and was up 1.4% year-on-year. Removing food and energy prices, the core index was flat on the month and slowed to 1.4% year-on-year from 1.6% in December.

- Small business optimism deteriorated for the third month in a row in January. Underneath the headline, the employment indicators remained broadly positive. Initial jobless claims also edged lower to 793k last week.

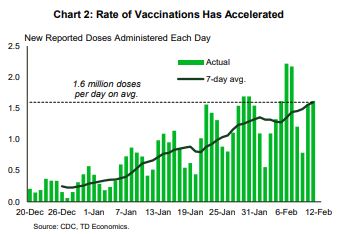

- Health metrics moved in the right direction this week. New COVID-19 cases continued to trend down, falling below 100k per day. Meanwhile, the vaccine rollout continued to pick up, averaging 1.6 million per day.

Moving In The Right Direction

Given the scope of fiscal and monetary policy supports to-date and the large fiscal package currently in the works, a lively debate is taking place in economic circles regarding the potential for inflation to accelerate beyond desirable levels. As we discuss in a recent report, a pickup in inflation is highly likely as economic restrictions are lifted. But, given where inflation stands today, there is some room for it to run before it reaches a concerning pace. Supporting the narrative of higher inflation is the fact that many small businesses plan to raise prices. According to NFIB data, the share of firms planning to do so rose by 6 points to 28% in January – among the highest levels in the post-Great Recession period.

Speaking of small businesses, the headline NFIB confidence measure ticked down modestly for the third consecutive month in January. Pullbacks in the expectations subcomponents were the biggest drags on the headline measure. But, in what can be viewed as a sign of underlying resilience, the employment metrics remained broadly positive. Hiring plans held steady in January, while job openings and the share of firms raising and planning to raise worker compensation ticked up.

While the U.S. labor market struggles to dig itself out of the winter slowdown, there appears to be a light at the end of the tunnel. New COVID-19 cases continued to trend down this week, falling below 100k per day recently for the first time this year. At the same time, the pace of vaccinations is accelerating, with daily jabs averaging 1.6 million in recent days (Chart 2). The vaccine rollout should continue to gather speed (see report released today), hastening the end of the pandemic.

With health metrics continuing to move in the right direction, a loosening of restrictions and stronger consumer confidence should follow. Coupled with another likely jolt of fiscal stimulus, this bodes for the U.S. economy to expand at a solid clip this year. If the full $1.9 trillion American Rescue Plan package is passed, real GDP growth could run as high as 6% through 2021, enough to bring the level of GDP back to its pre-crisis trend by the end of the year. New COVID-19 variants are the main downside risk to this positive outlook. For now, their spread remains low, but it is increasing in several key states. This is something that we’ll be keeping a close eye on.

Admir Kolaj, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Filing your 2020 Taxes

Filing Your 2020 Taxes

Tips for paying taxes soon and what to do if you can’t pay on time

When should you file your income tax? The earlier, the better; before the end of February – if you expect to get a refund. If you file by the end of February, you should receive your check within six weeks. But, if you delay and file in April when the Internal Revenue Service is inundated by forms from other last minute taxpayers, you could face a long wait for your refund.

If you are in line for a refund, avoid congratulating yourself too enthusiastically. That only means you have given the government free use of money that was rightfully yours. If you want to put those extra dollars to work for you instead of Uncle Sam, simply reduce the amount withheld from your paycheck. You do that by completing a W-4 Form and increasing your number of allowances on it.

If you have the money to pay but just cannot complete your tax return by the April 15th deadline, the IRS will extend your day of filing to August 15th. You must, however, send in an extension form – IRS Form 4868 – and an estimated payment of your taxes by April 15th. You or your accountant can estimate your income for last year and subtract any deductions and credits you expect to take. Then, by referring to the tax tables in the 1040 instruction booklet, you pay the amount you owe.

If you underestimate the income tax due, you may have to pay the one-half percent-a-month penalty – plus interest – on your outstanding balance. But, if you send in your return late without having filed for an extension, the IRS will be much less forgiving.

Here is another matter to watch: Even if you file an extension form, you must still make your past year's contribution to your Individual Retirement Arrangement by April 15th.

If you have omitted information, or would like to add information to your tax return after you have filed it, you may prepare amended federal and state returns. Generally, the IRS allows up to three years from the original filing date to amend a return.

What if You Can’t Pay on Time? According to the most recent data from the IRS, Americans owed over $131 billion in back taxes just last year. What should you do when you discover that you owe the government more than you can possibly pay by the due date?

Experts advise that you should file your tax return on time and send in as much as you can, otherwise you will be faced with paying larger penalties.

First, you will be liable for a fine of at least 5 percent and not more than 25 percent of your tax liability each month for late filing of your form plus one-half percent each month for late payment. Second, you may be charged about 10 percent annual interest compounded daily. You can avoid tax fines by filing a timely extension and paying at least 90 percent of your total tax liability. You still will have to pay interest on any balance due.

The IRS has a number of options available if payment is not made. They can attach your paycheck and seize your bank accounts and home, but they almost never take such drastic action if you earnestly try to pay your debts

Communicate, Communicate, Communicate

The key is communication. If you do not enclose a check when filing your return, you will eventually receive a letter demanding payment within ten days. The best advice here is: do not ignore this notice. The IRS becomes tougher with every passing day. Just be sure to telephone or visit the IRS office listed on the delinquency notice. Do that immediately after receiving the first notice instead of waiting for the fourth and final one about three months later.

It is also wise when meeting with the IRS to take along a professional tax advisor. An advisor often has the ability to get the IRS to agree to better terms than you can.

Once you have finalized your arrangements with the IRS, make a point of preventing it from happening again. If you are a wage-earner, take fewer withholding allowances at work so more money for taxes will be deducted from your pay; if you are self-employed, increase your quarterly estimated tax payments.

As the old saying goes, "the only two sure things in life are death and taxes."

“Late January is a Great Time to Pay Your Taxes". FMEX 2021 https://abm.emaplan.com/ABM/MediaServe/MediaLink?token=2413c4591fc244308c341dd784b6eafa

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of February 5, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Economic data released this week was balanced enough to re-ignite optimism in financial markets without calling into question the next fiscal support package.

- Job market data showed a third consecutive decline in the weekly jobless claims as well as moderate progress in payrolls and an unexpected drop in the unemployment rate.

- Assuming continued progress on the health front, another round of substantial fiscal supports could push the American economy from stall speed to an outright sprint in the second half of this year.

A Cautiously Optimistic Week

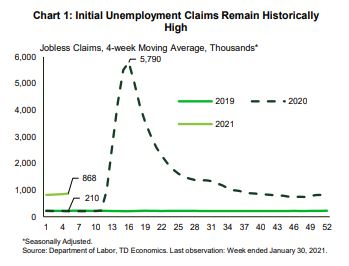

At present, the job market shows tepid signs of improvement. On Thursday, the Department of Labor reported a third consecutive decline in the weekly number of Americans seeking unemployment benefits. Recent reports come with the caveat of considerable revisions due to difficulties in adjusting the historically-high level for seasonal factors. Even when smoothed over four weeks, claims remain around 650 thousand higher than a year ago (Chart 1).

Likewise, today’s employment report for January showed moderate progress, with payrolls rising by 49 thousand, while the unemployment rate unexpectedly fell to 6.3% from 6.7% in December. Despite this progress, the economy has thus far recovered just over half of jobs lost during the initial lockdown period. The pandemic continues to inflict disproportional pain on the services sector, deepening inequality (see report). One particularly dire spot remains the leisure & hospitality sector, which reported another month of losses in January. With the setback, employment in the sector is now 22.9% below its pre-pandemic level (Chart 2).

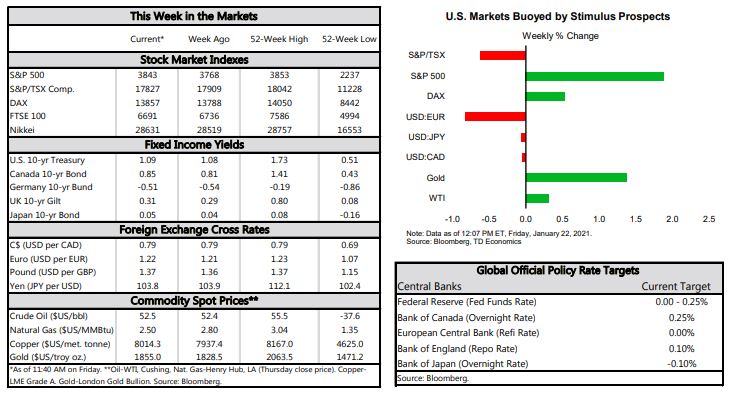

On the financial front, economic data was balanced enough to re-ignite optimism in financial markets without calling into question the next fiscal support package. The S&P 500 index ended the week 4.7% higher than the previous week and the 10-year U.S. Treasury rose to 1.15% from 1.08%.

This week, a report by the Congressional Budget Office estimated that the recently passed $900 billion stimulus package (signed into law at the end of December) would raise the level of GDP by 1.5% in 2021 and 2022, with most of that boost occurring this year. At $1.9 trillion, the next proposed round of fiscal support is even bigger. The income supports in the package will go a long way to bridging the gap to the other side of the health crisis and, with additional funding for vaccine distribution and testing, hopefully speed it along. Assuming continued progress on the health front, there is a good chance that the economy moves from stall speed to an outright sprint in the second half of this year (see report).

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 29, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Data on U.S. fourth quarter GDP showed the economic recovery continuing, but at much slower pace (4% annualized) than the previous quarter (33.4%).

- The Federal Reserve held its policy rate unchanged, and committed to doing all it can to support the recovery. It warned economic momentum has weakened with the spread of the virus.

- Vaccinations offer the best hope for faster growth. Assuming vaccine campaigns are successful, several months of cabin fever could lead to an even faster unleashing of spending than expected in the second half of this year.

Looking Back, Looking Forward

Not that anyone necessarily wants to remember it, but 2020 was a year for the record books. With U.S. GDP data for the fourth quarter released this week, we now have a complete picture of the economy’s performance during the pandemic-ridden year.

It was a wild ride. As lockdowns took effect in March, economic activity fell sharply. From the fourth quarter of 2019 to the second quarter of the year, real GDP declined by 10.5%, with the biggest drop over the March and April period. The rebound was almost as sharp, at least initially, with growth of 7.5% (non-annualized) registered in the third quarter. Progress, however, slowed in the fourth quarter to just 1.0%, as the virus spread worsened.

When all was said and done, the American economy ended the year 2.5% smaller than it started (Chart 1), though with huge disparities between industries and sectors. Parts of the economy least impacted by the virus – the production of things that you can consume at home (including the services provided by homes themselves) did even better than they would have without the health crisis. Durable goods consumption, including new and used vehicles, and new and existing home sales were particular bright spots. Higher-contact services, on the other hand, never had much of a recovery and are still well shy of pre-crisis levels (Chart 2).

This was the message delivered by the Federal Open Market Committee (FOMC) and its Chairman, Jay Powell, this week. While the Fed is aware of the potential light at the end of the tunnel, it is setting policy as if it is not sure when or if we will get there. As long as economic activity is weak, the policy rate will remain at rock bottom levels and asset purchases will continue apace.

Eventually, the Fed will have to go further in recognizing the potential upside to growth and inflation possible, as restraints on activity diminish. However, it has updated its strategy to allow itself to be more reactive than proactive to this change. With a short-term goal of pushing inflation above its medium-term 2% objective, the Fed is less concerned about allowing the economy to run hot.

This suggests a new balance of risks around the economic outlook. Assuming vaccination campaigns are successful, the second phase could surprise on the upside. Households with ample savings and several months of cabin fever could unleash an even faster pace of spending than expected. With businesses also shut down for several months, getting back up to capacity could be challenging. And, if you can’t meet all the demand at current prices, why not raise them?

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Exiting with Style - Business Succession Planning

Exiting with Style

For many small business owners, the sale of their company is the foundation of their retirement plan. Learn how the right business succession plan can help you secure your retirement. Contact us today to get started.

Financial News for the Week of January 22, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- President Biden’s inauguration was the marque event this week. Previous market optimism on the stimulus potential of the new administration seemed to run out of steam at week’s end.

- The current administration has ambitious plans for further Covid-19 relief, but it remains uncertain what Congress will agree to. In our recent report, we outline some potential scenarios for upside risks to economic growth.

- The housing market hasn’t run out of steam, with starts activity rising to new heights. It will be clearer in the coming months if the pandemic’s race for space and low mortgage rates have kicked off the next leg up in the housing market.

Biden’s Stimulus Would Boost Growth

President Biden’s inauguration was the marque event this week. Since the Georgia Senate run-off elections gave the Democrats a razor thin majority in Congress, equity markets have cheered the changeover in power. However, towards week end, sentiment soured a bit, perhaps as investors question how far the rally has gone.

Equity markets had been pricing in greater optimism on the American economy, hopeful that Democratic control in Congress would mean more fiscal stimulus and a faster recovery. However, it is still too early to determine what size of package will get through Congress. In a recent report we looked at three different scenarios for the next round of Covid-19 relief ranging from $500 billion to $1.9 trillion, and estimate the potential growth responses of each. The range of forecasts is shown in Chart 1.

These scenarios do not include a larger plan that the administration could pursue later in the year encompassing spending on campaign commitments such as infrastructure, and health and education, funded by higher taxes. These could have further implications on medium-term growth, particularly infrastructure spending, which has been shown to have some of the highest growth multipliers, particularly when the economy is weak.

The area of the economy that has rebounded most strongly from the pandemic-driven weakness in the spring is the housing market. Housing starts beat expectations in December, rising 5.8% to 1.67 million units (annualized), the highest level in 14 years. Once again, single family starts led the way, as demand for space has intensified since the pandemic, and inventory in the resale market remains drum-tight.

It is uncertain how long the current pace of construction can be sustained. In the 12 months prior to the pandemic, housing starts averaged 1.36 million. In the March through June period they ran well below that level, creating a backlog of pent-up demand. Since then, housing starts have been mainly above this trend, but have not quite yet made up for the ground lost in the spring. Once the backlog has been made up, we would expect starts to move toward their previous trend level.

Still, it is also possible that rock-bottom interest rates, increased confidence among homebuilders, and price pressures in the resale market will lead to a higher level of construction than we had anticipated pre-pandemic. The demographic fundamentals are certainly a positive factor as the largest segment of millennials is 25-29 years old, just starting to enter the peak phase of household formation. The next few months will be key to see if the construction industry can keep up the current pace.

Thankfully, infections have been trending down. The pace of the vaccine rollout has fallen short of the initial goal, but the country is doing well relative to its advanced economy peers. Regardless of what is achieved in terms of further stimulus from Congress, we expect the U.S. economy will see a much faster pace of growth come the second quarter, as people are able to resume more of their pre-pandemic behaviors.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Retirement Income Education

Retirement Income Education

Do you understand your retirement options? Working with a professional can help you understand the risk and reward associated with retirement strategies. Contact us today to learn more.

Saving for College

Saving for College

Higher education provides your children with lifelong advantages. This video explains the importance of getting started with a college savings strategy as soon as possible. Contact us today to learn more.

Retirement Education

Retirement Education

It’s never too early to start saving for your retirement – but it can be too late. Find out why you need to start saving for your retirement now in this video. Contact us today to learn more.