Financial News for the Week of April 16, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Headline inflation jumped in March, but it’s too soon to sound the alarm. Economic slack is still high, inflation expectations benign, and the Fed unlikely to sit on the sidelines if they drift up persistently.

- Retail sales surged in March, thanks to massive income supports, accelerated vaccine rollouts and loosening restrictions

U.S. - Much to Cheer About

Who said the stock market rally was over? After a slow start to the week, the S&P 500 hit another all time high. As of writing, the index is up 1.3% compared to last week’s close. Equities were helped by strong earnings and better than expected economic data. But interestingly, bond yields dropped on the news. At the time of writing, the 10-year Treasury yield was down nine basis points compared to last week. Usually, bond yields rise in response to strong data. The fact that yields drifted lower might seem like an anomaly but is likely due to the market already having priced in the economic recovery and inflation expectations. Meanwhile, growth stocks behaved as expected. Lower yields tend to increase future earnings of growth-oriented companies. So, tech stock rebounded as yields dropped.

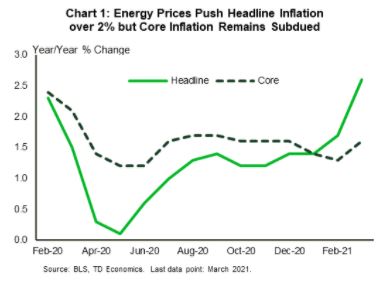

On to one of economists’ favorite topic these days, inflation! Consumer prices jumped in March (Chart 1). Inflation rose 0.6% month-on-month (m/m), pushing headline inflation to 2.6% year-on-year (y/y). Meanwhile, core inflation (ex. food and energy) was up 0.3% compared to the previous month and 1.6% higher compared to a year ago. The rise in inflation was mostly due to energy prices which went up 5.0% on the month. Energy prices will continue to keep the headline inflation number elevated over the next few months. In fact, year-on-year inflation numbers are likely to push through the 3% mark given the drop in prices in the second quarter of 2020.

Still, its too soon to sound the inflation alarm. The unemployment rate is still 2.5 percentage points (ppts) higher than its pre-recession level and there are roughly eight million fewer jobs. The 5-year U.S. breakeven – a measure of inflation expectations based on the spread between nominal and inflation adjusted Treasury yields – has cooled since hitting its highest point since 2008 in March. Rest assured the Federal Reserve is watching this and other measures of inflation expectations closely. In fact, Fed Vice Chair Richard Clarida said that if inflation expectations were to “drift up persistently […] that would indicate to me that policy would need to be adjusted.” Clarida also added that the Fed’s “metrics of success” on inflation is keeping inflation expectations anchored at 2%. According to the Vice Chair, inflation expectations most recently stood at 1.96%.

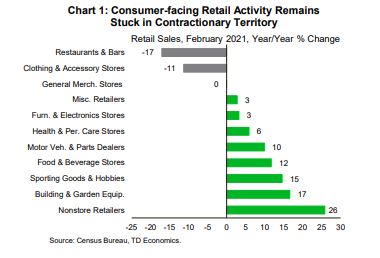

Meanwhile, income supports, accelerated vaccine rollouts and loosening restrictions helped retail sales end the first quarter on a high note (Chart 2). Retail sales surged by 9.8% month-on-month in March, almost four ppts more than market expectations. The level of retail sales was a whopping 17.1% higher than February 2020, just before pandemic-induced restrictions took hold. Going forward, spending is likely remain robust as the job market strengthens and Americans tap into accumulated savings.

Sohaib Shahid, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Small Business Owners - Building on a Strong Foundation

Building on a Strong Foundation

Small business owners face unique challenges. Learn about strategies and resources that can help you plan for your future. Contact us today to learn more.

Financial News for the Week of April 9, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S. equities jumped early this week and continued to move higher over the course of it despite the prospect of higher corporate taxes announced by the Biden administration.

- A few dark spots in the short-term outlook are supply chain disruptions, which are pushing up prices and weighing on deliveries in the services sector, as well as imports and exports.

Spring is Just Around the Corner

The economic calendar, meanwhile, was marked by reports on business activity, production prices and international trade. The Institute for Supply Management’s (ISM) service-sector index pleasantly surprised, hitting an all-time high. All 18 industries reported a revival of activity thanks to warmer weather and an accelerating pace of vaccinations. The rebound lifted the employment sub-index to 57.2, the best reading since June of 2019. Prospects for sustained reopening and a surge in demand could provide businesses with incentives for pre-emptive hiring, provided another wave of the virus does not lead to further restrictions.

Still, several factors warrant caution. First, the uptick in the supplier deliveries index indicates supply chain disruptions are spreading beyond manufacturing sector to services. Respondents in the accommodation & food services, arts & entertainment and information industries all commented on delays (Chart 1). Logistical challenges may result in product shortages and a reduce the ability of businesses to meet rising consumer demand.

At the same time, February’s trade report is a reminder that until the whole world is over the pandemic, supply challenges and halting global demand will remain an important macro theme. The U.S. trade deficit rose to a record $71.1 billion, as exports declined more than imports (Chart 2). With major trading partners still struggling to contain the spread of the virus, demand for U.S. exports fell. At the same time, shipping congestion in ports of Los Angeles and Long Beach contributed to the decline in trade in the month. This has not yet been resolved, and alongside the disruption at the Suez Canal, will continue to show up in the economic statistics in the month ahead.

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

2020 Tax Filing Deadline for Individuals is Extended to May 17th

2020 Tax Filing Deadline for Individuals is Extended to May 17th

But ask yourself whether there is any real benefit to waiting to file your taxes

The U.S. Department of the Treasury is delaying the April 15th deadline to file and pay taxes until May 17th, giving individuals and businesses another month to file and then pay the government what they owe. The IRS will be providing formal guidance in the coming days.

From the IRS press release dated March 17th:

"This continues to be a tough time for many people, and the IRS wants to continue to do everything possible to help taxpayers navigate the unusual circumstances related to the pandemic, while also working on important tax administration responsibilities," said IRS Commissioner Chuck Rettig. "Even with the new deadline, we urge taxpayers to consider filing as soon as possible, especially those who are owed refunds. Filing electronically with direct deposit is the quickest way to get refunds, and it can help some taxpayers more quickly receive any remaining stimulus payments they may be entitled to."

Directly From the IRS

“Individual taxpayers can also postpone federal income tax payments for the 2020 tax year due on April 15, 2021, to May 17, 2021, without penalties and interest, regardless of the amount owed. This postponement applies to individual taxpayers, including individuals who pay self-employment tax. Penalties, interest and additions to tax will begin to accrue on any remaining unpaid balances as of May 17, 2021. Individual taxpayers will automatically avoid interest and penalties on the taxes paid by May 17.

Individual taxpayers do not need to file any forms or call the IRS to qualify for this automatic federal tax filing and payment relief. Individual taxpayers who need additional time to file beyond the May 17 deadline can request a filing extension until Oct. 15 by filing Form 4868 through their tax professional, tax software or using the Free File link on IRS.gov. Filing Form 4868 gives taxpayers until October 15 to file their 2020 tax return but does not grant an extension of time to pay taxes due. Taxpayers should pay their federal income tax due by May 17, 2021, to avoid interest and penalties.

The IRS urges taxpayers who are due a refund to file as soon as possible. Most tax refunds associated with e-filed returns are issued within 21 days.

This relief does not apply to estimated tax payments that are due on April 15, 2021. These payments are still due on April 15. Taxes must be paid as taxpayers earn or receive income during the year, either through withholding or estimated tax payments. In general, estimated tax payments are made quarterly to the IRS by people whose income isn't subject to income tax withholding, including self-employment income, interest, dividends, alimony or rental income. Most taxpayers automatically have their taxes withheld from their paychecks and submitted to the IRS by their employer.”

State Tax Returns “The federal tax filing deadline postponement to May 17, 2021, only applies to individual federal income returns and tax (including tax on self-employment income) payments otherwise due April 15, 2021, not state tax payments or deposits or payments of any other type of federal tax. Taxpayers also will need to file income tax returns in 42 states plus the District of Columbia. State filing and payment deadlines vary and are not always the same as the federal filing deadline. The IRS urges taxpayers to check with their state tax agencies for those details.”

What Should You Do? Putting off paying taxes until right before the deadline is human nature. In fact, according to statistics from the IRS, in most years 70 million individuals had already filed their tax returns by mid-March. And that’s only about 45% of the returns the IRS expects to receive.

For those who haven’t filed yet, here are two reasons to convince you to have your taxes done professionally:

- The IRS estimates that the average person will require about 11 hours to prepare a tax return

- According to a survey by the National Society of Accountants, the average charged for filling out your basic federal and state returns is $261

So it is most likely worth your time and money to have an expert prepare your tax return or at least look it over for you.

Taxes are Complex

Preparing your own returns can take a lot of time, but the exact amount of time depends on the complexity of your finances.

You already know that the federal, state and local tax laws are complex, and constantly changing. But remember, the Tax Cuts and Jobs Act made some significant changes to the tax code when it went into effect. In fact, most consider the Tax Cuts and Jobs Act to be the biggest tax reform legislation in more than 30 years.

Should You Delay or Not?

The answer to that question, of course, depends on your situation. But it’s likely that for a lot of people, it makes sense to just stick to the original schedule and file and pay taxes by April 15th. Ask yourself this question:

“Is there any real benefit to waiting until May 17th?”

When you’ve answered that question, make sure you talk to your financial advisor to confirm that the tax decisions you make are consistent with your overall financial plan.

Have questions? Contact Aventus Investment Advisors, we can help!

“Tax Day for Individuals is Extended to May 17th ". FMEX 2021 https://abm.emaplan.com/ABM/MediaServe/MediaLink?token=9d28fc21b72645a7a30a3086753bd738

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of March 19, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Most Federal Open Market Committee members see no interest rate hikes until at least 2024 despite a sharp upgrade to the growth outlook.

- Retail sales weakened on the back of frigid temperatures, but additional support to households through the American Rescue Plan is likely to support retail activity in the coming months.

- Housing starts fell for the second straight month in February, but homebuilding activity is expected to remain elevated in the near-term.

Spring is Just Around the Corner

On the monetary policy front, the Federal Reserve sharply upgraded its growth outlook. The median projection among FOMC members is for the economy to expand 6.5% (from 4.2%) this year due to stimulus and vaccine rollout. Still, the Fed maintained its current monetary policy stance. This includes keeping the federal funds rate at the current 0% to 0.25% range and a commitment to purchase at least $80 billion Treasuries and $40 billion mortgage backed securities per month. The Fed’s projections also showed the majority of members do not expect to raise the federal funds rate until at least 2024.

In terms of economic data, retail sales declined by 3.0% month-on-month in February (Chart 1). This was worse than the consensus estimate for a 0.5% drop. The decline comes on the back of unseasonably cold weather that shut down many of the southern states. It also comes on the heels of a strong and upwardly revised reading in January. The good news is that spring is just around the corner and optimism is growing. The timing of the $1.9 trillion American Rescue Plan couldn’t be any better. It comes at a time when cases are declining and lockdowns are being eased. This will make spending easier, allowing retail sales to recover in the coming months.

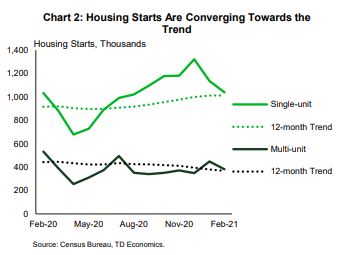

Turning to the real estate sector, housing starts fell by around 10% in February, declining for the second straight month (Chart 2). Housing starts dropped to 1.42 million units (annualized) from 1.58 million in the previous month. The fall in housing starts and building permits was seen across both single-family and multi-family segments. The decline was also seen across most regions but was concentrated in the Northeast, which saw a staggering 40% drop. Despite the slow start to the new year, we expect homebuilding activity to remain elevated near current levels. This is thanks to a low inventory environment and the fact that housing demand will improve as the labor market heals.

Meanwhile, new COVID-19 cases continue to fall. And the vaccine rollout is only getting faster. So far more than a 115 million doses have been administered, a 14% increase compared to last week. States are easing restrictions and air travel is picking up. There is plenty of reason to be optimistic, but states need to tread carefully. As long as the virus is still with us, reopening economies too quickly could still lead to a surge in cases.

Sohaib Shahid, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of March 12, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- One year after the start of global lockdowns, it is starting to feel like the end is finally approaching. The new fiscal package signed into the law will continue to support a stronger economic recovery and the financial resilience of American households.

- The Consumer Price Index (CPI) came in on market expectations, while core CPI edged lower in February, giving inflation anxiety a short break.

- The 10-year U.S. Treasury yield is on the upward trend again, but the Fed’s primary concern remains a sustained labor recovery. With the virus still spreading, the recovery remains fragile and unequal, requiring policy to remain accommodative.

A Year of COVID

This week marks one year since the start of global lockdowns and economic disruptions due to the coronavirus pandemic. And while no one can say that the crisis is over, it is starting to feel like the end is finally approaching. Thanks to unprecedented policy support, the economic slump has been short-lived, and prospects for recovery look much brighter than initially predicted. We expect that the American Rescue Plan, signed into effect on Thursday, will lift economic growth to roughly 6% this year, the highest rate since 1984.

The new fiscal package is huge. It provides a fresh round of $1,400 checks starting as early as this weekend, extends unemployment benefits of $300 per week until September, increases the child tax credit (and makes it fully refundable), provides aid to states and local governments, supports schools and expands vaccination efforts.

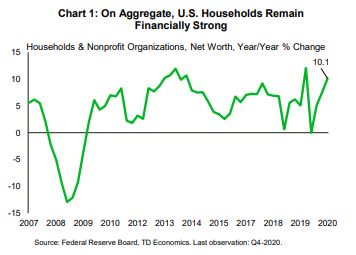

Substantial income supports have enabled Americans to maintain strong balance sheets through this crisis. According to the Fed’s data released yesterday, U.S. households’ and non -profit organizations’ net worth reached a record high of $130 trillion, growing 10% in the last quarter of 2020. (Chart 1). Nevertheless, income and wealth disparities, exacerbated by the crisis, continue to pose risks to the recovery.

On the economic front, data was scarce this week. A highly anticipated Consumer Price Index (CPI) report came in on market expectations. Gasoline and food prices continued to rise, driving the headline index 1.7% higher over the past year. Still, core inflation (excluding these volatile categories) remained soft, rising by 0.1% on the month and edging lower on the year-on-year basis to 1.3% from 1.4% in January.

Still, a closer look at the core prices reveals a shift in recent trends. Supported by the housing component of the index, the decline in core services prices was halted at 1.3% year-on-year (Chart 2) in February. Indeed, strong demand for housing has lifted home prices by at least 10% since 2019, even as rents in major urban centers have gone in the opposite direction. Goods’ price growth, on the other hand, softened in February reflecting a pull-back in used car prices, one of the biggest price outperformers of the pandemic.

The news of muted price growth gave the market’s inflation anxiety a short break. The 10-year U.S. Treasury yield subsided from its last week’s peak of 1.60% to just under 1.50%, before bouncing back to almost 1.62% at the time of writing. Despite solid demand in this weeks’ three U.S. Treasury auctions, investors are increasingly betting on higher inflation. As we wrote recently, the Fed will be mindful of mounting price pressures, but its new framework gives it more wiggle room for letting inflation move above 2%.

The Fed’s primary concern remains a sustained labor recovery. With the strongest economic growth in recent history, this should be achieved over the next two years. In the meantime, with the virus still spreading, the recovery remains fragile and unequal, requiring policy to remain accommodative.

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Facing Down the Fear of Running out of Money in Retirement

Facing Down the Fear of Running out of Money in Retirement

Tips to avoid one of the biggest retirement worries that all of us will face

Retirement is a major milestone that brings many life changes. One thing that doesn't change for most people: the fear of running out of money. In fact, one of the most frequently reported retirement worries is outliving savings and investments. And interestingly, this is a concern across all ages – many don’t think they’ve built a nest egg large enough to last through retirement.

Now is the time to face your fears. Yes, there are a lot of ways you could go broke in retirement, but many can be averted with careful planning. Here is a list of seven common mistakes in retirement – and ways to avoid them.

Abandoning Stocks

Yes, stocks are risky. Just look at 2020 as an example. We saw an end to the longest bull-market in history, two market corrections, a legitimate bear market and then a spectacular bounce from the bottom. And all that happened in a single year. But if you’re retired, you might have been inclined to move your money out of stocks altogether and instead focus on preserving your wealth.

But that might have been a mistake.

Without stocks, you might not get the growth that you need. You need your money to continue to grow through those 20 to 30 or even 40 years of retirement to outpace inflation and help maintain your lifestyle.

Spending Too Much Money

This one seems so obvious, but all of us are guilty of making this mistake (whether or not we’re retired). And according to the Employee Benefit Research Institute, almost half of retirees spent more annually in their first two years of retirement than they did just before retiring. So for retirees on a fixed income, this is a problem, making budgeting more important than ever.

Abandoning Insurance

Sure, eliminating costs in retirement is a good idea, but eliminating your insurance might not one of them. In fact, having adequate health coverage is essential to helping prevent a devastating illness from wiping out your retirement savings. And don't just think about health insurance either.

Whether you want to admit it or not, our chances of having a car accident increase as we get older. And one car accident-related lawsuit could drain your retirement savings.

Planning on Just One Source of Income

In retirement, having multiple income streams is almost always better than just one. Think about this: many retirees consider Social Security to be their primary source of income, but do you worry that Social Security will be reduced or cease to exist in the future? And many retirees rely on pensions as a source of income, but how secure might that be? Or are you counting on a big inheritance?

Forgetting About Taxes

But when you include each of the above income streams are combined together along with what you saved for retirement, in 401(k)s and IRAs, then you have more stable and diversified income streams to rely on in your retirement years.

Ok, maybe this mistake won’t make you broke, but without a smart withdrawal strategy you will end up losing more than you should. Maybe a more tax-efficient way might be to draw down the principal from maturing bonds and certificates of deposit first, since they are no longer bearing interest. Then maybe sell from your taxable accounts, for which you only have to pay the capital-gains tax and end with withdrawing from your tax-deferred accounts.

Not Accounting for Where You Live or Vacation

Where you live impacts what you pay in taxes big time. That's why so many people move to Florida and Arizona after they retire. Besides the sunshine, both states are tops when it comes to offering more tax-friendly environments for retirees.

But, if you’re like most people who think about where to live, you’re also probably imagining traveling during your retirement years. But before you book your next five trips, you must make sure your finances can handle your trips because seeing the world isn’t cheap.

To plan your retirement vacations, you can do a couple of things to better afford your travels: either increase your spendable income (but be careful here, especially in the first few years of retirement) or you can reduce your travel expenses.

Relying Exclusively on Bonds

In today’s low- (or no-) interest world of bank accounts, increasing income can be a huge challenge. You either risk your savings in the stock market, which has a low dividend yield of about 1.5%, or you go into bonds.

Except bonds might well be headed for trouble. If interest rates finally rise from today’s historical lows, which is likely, bond values will decrease – maybe even substantially. You could end up with a big loss after just a small increase in rates.

How We Can Help

Running out of money is a really big worry in your retirement years. And layering on the unpredictability of investing, you might ask yourself how you prepare your retirement portfolio for all of it? Well, one major key to successful planning for your retirement lies in following wise strategies.

At Aventus Advisors, we understand these strategies and can help create a retirement income plan that works for you. We prepare for the best – and the worst – of anything. The world is just too unpredictable to do less. Have questions? Contact us!

“Facing Down the Fear of Running out of Money". FMEX 2021 https://abm.emaplan.com/ABM/MediaServe/MediaLink?token=f459aa6daf2a4d8eb5ce6c5f5ebe5329

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of March 5, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The ISM indexes diverged in February, with manufacturing improving and services falling on the month. However, both remain well in expansionary territory. Vehicle sales, meanwhile, fell 5.7% to 15.7 million (SAAR) units.

- U.S. job growth picked up steam in February, with payrolls rising by a better-than-expected 379k. Gains were concentrated in the leisure and hospitality sector. The unemployment rate fell slightly from 6.3% in the month prior to 6.2%.

- President Biden’s $1.9 trillion stimulus package cleared hurdles toward passage this week. The added stimulus will boost economic growth but could also lead to more inflation. The Fed expects inflation’s rise above target to be transient.

Coming Out of the Winter Lull

The first week of March offered a rich buffet of economic data. While it was not all positive, overall it indicated that the U.S. economy continued to come out of its winter lull. The ISM indexes diverged in February, with manufacturing improving and services falling on the month. However, at levels of 60.8 and 55.3 respectively, both indexes remain well in expansionary territory (above the 50-point threshold). Vehicle sales, on the other hand, fell 5.7% to 15.7 million units in February – a reading that was on par with expectations. Severe winter storms that left many Texans without power, among other things, likely played a role in the pullback by reducing foot traffic to dealerships.

Unfavorable weather conditions, however, did not prevent the hiring pace in the U.S. economy from accelerating last month. In fact, payrolls rose by 379k in February, a better outturn than expected (Chart 1). Data revisions also added 38k jobs to the two months prior. Gains in February were concentrated in the leisure and hospitality sector (+355k), which appears to have benefited from eased COVID-related restrictions. The unemployment rate, meanwhile, fell slightly from 6.3% in the month prior to 6.2%.

Improvements in public health conditions build the case for a stronger economic rebound in the months ahead as the economy reopens further. COVID-19 cases have flatlined at around 65k per day recently. Vaccinations, on the other hand, continue at a brisk pace, averaging two million per day. The recent approval of the Johnson & Johnson (J&J) vaccine should be another shot in the arm for vaccinations, given that it requires only one dose and can be stored more easily than the vaccines currently in use. With firm commitments from Pfizer-BioNTech, Moderna and now J&J, President Biden has stated that vaccines should be available to every adult American by the end of May, sooner than initially anticipated.

The likely approval of the $1.9 trillion stimulus package in the days ahead will be an added boon to the economy. Having passed the House, the American Rescue Plan Act is now being debated in the Senate. Some changes have taken place in recent days. For instance, President Biden has agreed to stricter income-eligibility limits for the $1,400 stimulus checks, which means that fewer Americans will receive direct payments this round. The bill could see some more tweaking. The goal is to have it on the President’s desk before the enhanced jobless benefits expire in mid-March.

The added stimulus will hasten the economic recovery, with growth expected to accelerate to nearly 6% this year. This level of activity will be accompanied by stronger inflation and higher bond yields. Price pressures have been on the rise in recent months, a message also echoed by the ISM price subindexes (Chart 2). Long-term Treasury yields, meanwhile, continued to climb higher this week, with the 10-year rate sitting at 1.57% as at the time of writing. The Fed is aware that inflation could rise above the 2% target. But, as reiterated by Fed Chair Powell yesterday, it expects this to be ‘transient’. As such, the Fed appears poised to remain patient in keeping monetary policy accommodative for some time (for more, see our Dollars & Sense publication).

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

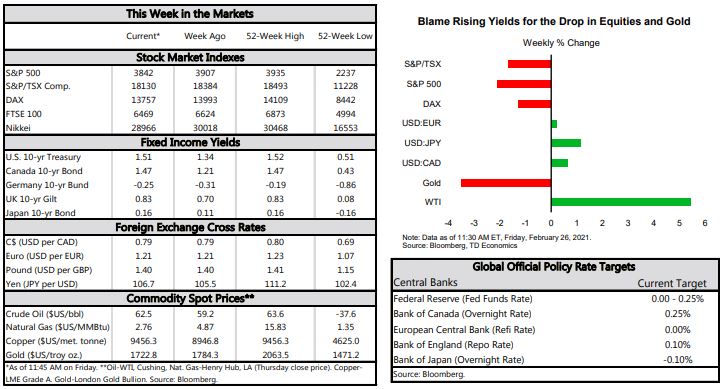

Financial News for the Week of February 26, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Federal Reserve Chairman Powell reassured markets that there will be no early tightening of monetary policy or drawdown of asset purchases even with a brighter economic outlook.

- Consumers remain at the forefront of the recovery, as personal income surges and spending rebounds on the back of income support measures.

- Jobless claims fell more than expected this week but remain three times higher than pre-pandemic levels.

The American Consumer is Back

For a change, the S&P 500 did not have the best week. As of writing, it was down 2.4% compared to last week’s close. Blame the Treasury yield. The 10-year Treasury yield hit the highest point in a year amid a more upbeat global economic outlook and rising concerns over inflation. The decline in equities was primarily led by large cap technology stocks, which have so far made major gains during the crisis. Still, the S&P 500 is 3% higher than where it was at the start of this year.

On the monetary policy front, the Federal Reserve’s Chairman Powell probably had the most optimistic assessment of the economy since the start of the pandemic. He told Congress that there was “hope for a return to more normal conditions”. Still, Powell signaled he is in no rush to tighten monetary policy or drawdown asset purchases even with a brighter economic outlook. The Chairman also reassured markets on the inflation front. He said that inflation dynamics do “not change on a dime” and that “the economy is a long way from our employment and inflation goals”.

In terms of economic data, personal income surged by 10% month-on-month in January, in line with market expectations. The strength was primarily due to the 52.6% increase in social benefits which include stimulus checks and expanded unemployment insurance benefits. Meanwhile, personal spending rose by 2.4% and was led primarily by goods which went up 5.8% (Chart 1). The rise in goods spending was seen across the board, with recreational goods and vehicles driving most of the gains. The services sector also showed resilience, eking out a 0.7% growth in spending. Gains were mostly led by food services and accommodation, the industry which has been in the line of fire right from the outset of this pandemic.

Turning to the labor market, jobless claims fell far more than expected (Chart 2). Initial claims came in at 730k, down 111k from the prior week, and beating the consensus of 825k. This was the largest weekly drop since the end of August. But not all states performed the same. California and Ohio registered the biggest declines while Illinois and Missouri recorded notable growth. Continuing claims came in at 4.4 million, 41k less than the consensus and down 0.1 million from the week before. Still, both claims are almost three times higher than their pre-pandemic levels. The labor market remains the weak link in an otherwise stronger-than-expected start to the new year for the economy.

Meanwhile, revisions to the second GDP release were relatively minor. The economy grew 4.1% annualized in the final quarter of last year, slightly higher than the initial estimate of 4.0%. Government and household spending were both revised down 0.1 ppts. Meanwhile, non-residential fixed investment was adjusted up 0.2 ppts, driven by stronger spending on equipment and intellectual property products. Residential investment was also revised higher by 0.1 ppts. Given the relatively minor adjustments to the quarterly data, there were no changes to the annual GDP, which shrank 3.5%.

Sohaib Shahid, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of February 19, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The week’s data confirmed that the U.S. economy continued to make progress early in 2021.

- That progress looks likely to get a substantial shot in the arm from the $1.9 trillion American Rescue Plan in the coming weeks. We have upgraded our U.S. forecast to include the impact of the plan.

- Retail sales and the housing market continued to show strength in January, as consumers’ preference for all things “home” remained well entrenched.

Economy Progresses in January

That progress looks set to get a substantial shot in the arm. With the impeachment trial over, House Speaker Pelosi expects a vote on President Biden’s American Rescue Plan by the end of next week. Given the high likelihood of passage, we have updated our U.S. forecast to include it (see update). In combination with the $900 billion package in late 2020, the lift to growth is substantial, adding over 1.5 percentage points to real GDP growth over the course of 2021.

January’s retail sales report provided evidence that Keynesian economics works. If governments deposit money in Americans’ accounts, they will spend it. Retail sales rebounded strongly in January, up 5.3% month-on-month, well above market expectations for a 1.1% increase. This is the first month of growth since September, as the rising numbers of Covid-19 infections and waning government income support programs dampened momentum in the final months of last year.

After such a strong January, some weakness in February retail sales would not be surprising. Still, we expect a strong quarter for consumer spending given the healthy starting point and an increasing number of jurisdictions lifting restrictions as Covid-19 case counts fall. In addition to the latest round of assistance from Washington, consumers are sitting on approximately $1.6 trillion in excess savings from 2020, presenting upside risk to the spending outlook.

As consumers focus their spending on the home, the housing market has been another area of strength. Housing starts gave back some of their gains in January, but the trend remains strong, particularly for single-family homes (Chart 2). The permits data suggests the lull should be temporary, with authorizations up sharply on the month. Single-family home construction, in particular, has been re-energized during the pandemic. This is likely due to a combination of low interest rates, homebuilder confidence in the durability of demand for lower-density housing, and potentially greater availability of workers. While we expect some deceleration from the recent vigorous pace of housing starts aver the coming months, our forecasted level of construction is higher than it was a year ago.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.