2021 Tax Rates and Deductions

The New IRS Tax Rates and Deductions for 2021

Although a year away, your 2021 tax planning should have already started

Amidst all the pandemic news and 2020 election drama, many might have missed that the IRS also quietly published new 2021 tax rates in late October and there are plenty of changes that will impact taxpayers in 2021.

While it’s more than a year away (these changes are for 2021 returns filed by taxpayers in 2022), there are a few changes that you should know about.

Rules Not Yet Extended

It is very important that taxpayers realize that the 2020 rules enacted during the pandemic – namely the rules surrounding borrowing, distributions and the waiver of Required Minimum Distributions – will not be effective in 2021 unless Washington passes new legislation.

Standard Deductions

In very simple terms, the standard deduction is a specific dollar amount that reduces your taxable income.

- The standard deduction for 2021 will be $25,100, an increase of $300, for married couples filing joint returns;

- The standard deduction for 2021 will be $12,550, an increase of $150, for single taxpayers’ individual returns and married individuals filing separately;

- The standard deduction for 2021 will be $18,800, an increase of $150, for heads of households.

2021 Tax Brackets

The tax rates and tax brackets for 2021, adjusted for inflation, are provided as follows:

Medical Savings Accounts

Certain thresholds and ceilings for participants in Medical Savings Accounts will also be increased:

- For self-only coverage, the plan’s annual deductible for 2021 must be at least $2,400 and no more than $3,600 with a maximum out-of-pocket expense of $4800, an increase of $50 for each amount.

- For family coverage, the deductible must be at least $4,800 but no more than $7,150, an increase of $50 for both amounts.

- The out-of-pocket expense maximum for family coverage will increase by $100 to $8,750 for 2021.

Retirement Plan Contributions

The IRS also announced the 2021 limitations on retirement plan contributions and their phase-out ranges. The limitations for employee contributions to employer retirement plans will remain at $19,500, and the catch-up contributions for those 50 and older will remain at $6500. For SIMPLE retirement accounts, the limitation will remain $13,500.

Although the deductible amount for IRA contributions will remain at $6000 (with catch-up contributions for those 50 and older remaining at $1,000) the phaseout levels have adjusted upwards. And the phase-out levels depend on whether or not one is also an active participant in another employer retirement plan.

- If an individual is an active participant in an employer retirement plan, the deduction phases out for adjusted gross incomes between $66,000 and $76,000 for single individuals and heads of households, and between $105,000 and $125,000 for married couples filing joint returns.

- For an IRA contributor who is not an active participant in another plan but whose spouse is an active contributor, the phase-out ranges from $198,000 to $208,000.

- For a married active contributor filing a separate return, there is no adjustment and the phase-out range will remain $0 to $10,000.

These phase-outs do not apply if neither are covered by an employer-sponsored retirement plan.

How Aventus Advisors Can Help

The fact is that the CARES Act was by far the largest economic bill in America's history and the second COVID relief details are part of a bill that is over 5,000 pages long. Further, with a federal tax code that is over 2,500 pages, no wonder tax strategies can be overwhelming.

So, before you go down a path that might not be in your best interest long–term, make sure you consult with a financial advisor to determine how the new tax changes and new tax bills might impact you and your family. If you need help with any of your planning decisions, don’t hesitate to contact Aventus Advisors.

“The New IRS Tax Rates and Deductions for 2021". FMEX 2021https://fmexcontent.s3.amazonaws.com/11800/11800.pdf.

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of January 15, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- President-elect Biden unveiled a proposal for a new relief package this week. The $1.9 trillion plan includes additional one-time stimulus checks, unemployment benefit supplements and funding for state and local governments.

- Additional fiscal support will help bolster a faltering economy. Initial jobless claims rose by 181k last week to levels

not seen since last summer, while retail sales fell 0.7% last month, their third straight month of decline. - This week, Fed Chairman Powell brushed aside concerns about higher inflation and reiterated the central bank’s commitment to maintain an accommodative monetary policy stance until the economic recovery is complete.

New Year, New Stimulus

This week offered some welcome respite following the turbulent events that marked the start of the year. From an economic standpoint, the biggest news came from President-elect Biden’s address on Thursday as he unveiled a new $1.9 trillion coronavirus relief plan. The proposal, which will need to go through Congress, notably includes a round of $1,400 stimulus checks for individuals with expanded eligibility, a $400-per-week unemployment insurance boost through September, as well as funding for state and local governments. With eviction and foreclosure moratoriums set to expire later this month, Mr. Biden also called to extend these measures until September.

Additional fiscal support will go a long way toward breathing new life into a faltering economic recovery. Indeed, the heavy toll of the third wave of COVID-19 infections was on full display in economic data released this week. Initial jobless claims rose by 181,000 last week to levels not seen since last summer (Chart 1). This marked the largest weekly increase since last spring and suggests that layoffs are picking up speed. The near-term outlook is not particularly bright. The U.S. economy already lost 140,000 payroll jobs last month, mainly in the leisure and hospitality industry, which was hit hard by restrictions imposed across the country to curb the spread.

These difficult conditions are weighing on business confidence. In December, the NFIB small business optimism index plummeted by 5.5 points to 95.9 – one of the steepest drops in the survey’s history. The decline was driven by lower expectations for real sales, earnings trends and economic improvement in the near-future. This downbeat tone was also echoed in last month’s retail sales report. Sales contracted by 0.7% in December from the previous month, marking their third consecutive month of decline. They fell the most at nonstore retailers (-5.8%), electronics and appliance stores (-4.9%) and food services and drinking places (-4.5%). By contrast, sales at gasoline stations increased by 6.6% on the month.

Alongside stronger gasoline sales came higher prices at the pump, which lifted overall consumer prices in December. The headline Consumer Price Index (CPI) rose by 0.4% month/month, while the core series – which excludes volatile food and energy items – was more muted at 0.1% (Chart 2). On the whole, the pandemic continues to dampen consumer price growth, particularly for core services, which are now trailing their goods counterpart. This is a notably rare occurrence, which usually manifests itself on the heels of an economic recession.

Inflation will likely pick up later this year as vaccination rates increase and the economy gets back on track, but the Federal Reserve is in no rush to shift away from its accommodative monetary policy stance. This week, Chairman Powell brushed aside concerns about higher inflation, noting that the central bank has the tools to stave off unwelcomed price growth, though he doesn’t expect to use them anytime soon. What is more, Mr. Powell indicated that the U.S. economy is still a long way from a complete recovery. The message was clear – interest rates will remain low for the foreseeable future.

Johary Razafindratsita, Economist | 416-430-7126

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 8, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Unprecedented events rocked the U.S. Capitol this week. Ultimately, Congress certified Joe Biden as the next President and President Trump agreed to a peaceful transition of power.

- The Democrats took control of the Senate by prevailing in both Georgia runoff elections. With all three levels of government now in the hands of Democrats, President-elect Biden will have a better shot at implementing his agenda.

- Economic data was a mixed bag. Vehicle sales ended 2020 on a solid footing and ISM indexes remained well in expansionary territory. However, job creation came to a halt in December, with payrolls falling by 140k.

Holiday Shopping Blues

Along with personal resolutions, the New Year tends to usher in a sense of hope. But, as the last few days have demonstrated, simply flipping the calendar does not guarantee a fresh start. Many of the issues that made 2020 a challenging year linger on. The health crisis is (still) front and center, with positive cases and hospitalizations surging to all-time highs (Chart 1).

Meanwhile, the unprecedented events at the U.S. Capitol on Wednesday shocked the country and the world. Still, in terms of the economic outlook, the biggest development on the political front was that Democrats narrowly took control of the Senate by prevailing in both Georgia runoff elections. With all three levels of government now in the hands of Democrats, Joe Biden will have a better shot at implementing his agenda.

The Biden election platform promised an ambitious spending agenda, funded by higher taxes (see report). A thin Senate majority will pose a challenge to several elements on the list, but increased spending to support the economy through the pandemic appears likely. Tax changes, such as the planned tax hikes on corporations and high-income individuals, appear less likely. While they can be rolled through in the budget reconciliation process with a simple majority, more conservative-leaning Democratic Senators would have to be on board, making it a harder sell than temporary supports to bridge the economy while vaccines continue to be rolled out.

Economic data was not all negative – vehicle sales ended 2020 on a solid footing and ISM indexes remained well in expansionary territory. However, after a solid seven-month run, job creation came to a halt in December, with payrolls falling by 140k (Chart 2). While plenty of industries still added jobs, including professional and business services, retail trade and construction, increased restrictions took a heavy toll on the leisure and hospitality industry (-498k), with the decline concentrated in bars and restaurants.

To surpass this latest pandemic-induced hurdle, the economy will need all the help it can get. The $900 billion relief bill that was passed in late December, which extends special emergency unemployment benefits for 11 weeks through to mid-March and provides $600 stimulus checks to both adults and qualifying children, will go a long way to supporting the economy in the near-term as restrictions keep many businesses shuttered. More help is likely on the way, with the new administration having pledged to boost the size of the stimulus checks to $2,000, among other things.

Overall, the combination of vaccinations and increased spending, suggests that 2021 should be a much better year than the one we left behind. Markets certainly seem to be in tune with this view, with risk assets shrugging off this week’s turmoil in the Capitol. That said, we are not out of the woods yet and there could be additional bumps along the road. New COVID-19 variants, which appear to spread more easily, pose an added downside risk. The new administration certainly has its work cut out for it.

Adkmir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 18, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Prospects for fiscal stimulus drove volatility in equity markets this week. Policymakers are reportedly closing in on a much-needed relief package following several months of gridlock.

- Economic data released this week were less cheerful. Jobless claims rose to levels last seen in early September, while retail sales declined by 1.1% in November. Housing starts were the exception, increasing by 1.2% last month.

- The Fed reaffirmed its pledge to support the economy. It maintained its current policy stance this week, keeping the fed funds rate near zero and committing to more asset purchases.

Holiday Shopping Blues

It was a busy week for economic data. Financial markets, however, devoted their attention to the brightening prospects for a new stimulus bill. Indeed, following several months of gridlock, this week saw considerable progress on that front. News broke that lawmakers are racing to finalize a deal before next week’s recess, which helped lift market sentiment. At the time of writing, the S&P 500 was on track to end the week 1% higher.

By contrast, economic data released this week was decidedly less cheerful. Outside of a positive surprise coming from housing starts, the data continued to paint the picture of a faltering recovery. As discussed in our Quarterly Economic Forecast, a slowdown has been expected, given the surge in new coronavirus cases and the growing number of restrictions being implemented across the country. On the bright side, rollouts have officially begun for Pfizer’s vaccine. Meanwhile, Moderna’s is expected to receive approval very soon and could be made available as early as this weekend.

Back to the data, the strength in residential construction continues to impress. Housing starts rose by 1.2% in November, their seventh consecutive month of increases (Chart 1). Overall, starts have now rebounded within 1.3% of their healthy February-level. Unlike previous months, multi-family starts powered the gains last month, jumping 4% from October. As we discuss in a recent report, this segment of the market continues to face challenges due to shifting housing preferences toward bigger homes and more outdoor space. Nonetheless, single-family starts saw a more muted increase last month (+0.4%).

Despite its resilience, the construction sector’s outlook is softened by deteriorating affordability. In fact, construction costs have risen at the same time as inventories remained low. These factors could weigh on housing demand in 2021.

By all accounts, the third wave of COVID-19 infections is weighing on this year’s holiday shopping season. Sales declined the most at clothing stores, alongside food services and drinking places which are most susceptible to be impacted by restrictions. By contrast, food and beverage stores, as well as building material retailers recorded positive sales growth last month.

The fragility of the economic recovery was acknowledged during this week’s Federal Reserve Open Market Committee (FOMC) policy announcement. Members unanimously voted to maintain the current policy stance, keeping the fed funds rate at its effective lower bound and committing to more asset purchases. The Fed reaffirmed its pledge to use the full array of policy tools at its disposal to support the economy until the recovery is complete. The missing piece of the puzzle is additional fiscal support. But, with that likely on the way, coupled with vaccines, the light at the end of the tunnel is finally looking a little brighter.

Johary Razafindratsita, Economist | 416-430-7126

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Year-end Financial Checklist for Working Professionals

Year-end Financial Checklist for Working Professionals

Set yourself up for success in the new year with a financial checkup. Here are some essential year-end tax, planning, and financial housekeeping items to consider.

1. Maximize contributions to tax-advantaged retirement savings accounts including 401(k), HSA, or IRA accounts

2. Reduce taxes by offsetting capital gains with losses from stocks, bonds, mutual funds, and exchange-traded funds (ETFs)

3. Evaluate the progress of your investments toward your retirement, college, and personal savings goals.

4. Consider a 401(k) rollover or a Roth conversion to lay the groundwork for tax-efficient withdrawals in retirement.

5. Think about giving to charity and track all forms of donation to qualify for tax deductions.

6. Talk to your family about your legacy goals and gather your legal, financial and health-related documents.

7. Simplify your financial record-keeping by taking advantage of direct deposits, online statements, automatic payments, and retirement investment contributions.

8. Check your credit reports. Each of the credit reporting companies is required to provide you with a free copy of your credit report once every 12 months.

9. Create or update a family or personal budget.

10. Revisit your life and automobile insurance coverage.

If you need help with any of your planning decisions, don’t hesitate to contact Aventus Advisors.

“Year-end Financial Checklist for Working Professionals". ABM 2020.https://fmexcontent.s3.amazonaws.com/1289/1289.pdf

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Estate Planning Must Dos

Estate Planning Must-Dos

12 Estate Planning Activities to Consider

Many of you already have estate documents, probably executed many years ago. You need an estate attorney to look over your documents every 10 years or so. Here are a dozen points to review.

1. Do you have a will and powers of attorney for health care and property? These are part of every complete estate plan. With health-care power, you choose an agent to act on your behalf if you become unable to make your own decisions. With durable power for property, you select an agent to act if you are incapacitated and can’t sign a tax return, make investment decisions, make gifts or handle other financial matters.

Make sure your health-care power addresses the Health Insurance Portability and Accountability Act. This governs what medical information doctors can release to someone other than the patient.

2. Do you need to change any beneficiaries, executors, trustees, guardians or others named in your documents? Are all still living? Can someone you recently found fill a role better?

3. Any updates needed to addendums to your will that specify who gets what of your personal property?

4. Did you move to a different state since the execution of your estate documents? If so, seek out a local estate attorney to check any legal differences for planning between your old and new states.

5. Do you still need your trust documents or can you decant, which allows you to change some provisions? Consider this technique of emptying the contents of an irrevocable trust into another newly created trust if you are unhappy with your irrevocable trust. Not all states allow decanting.

You may also want to discuss possibly moving assets out of a living trust (where a trustee holds them, a technique sometimes used to avoid probate) and holding them in the name of an individual.

This discussion will weigh the income tax benefits of a step-up in cost basis, the original cost of an asset, versus other reasons to keep the trust. (“Step up” means that the cost basis of an asset resets to the fair market value of the security as the date of the holder’s death - potentially a much higher value than when they bought the security.) The higher the cost basis, the less capital gains tax your heirs pay when they sell the asset.

You may also want to see whether you need an irrevocable life insurance trust, a device once used to move assets, typically life insurance, out of a taxable estate. Now that thresholds are higher - individuals can leave $11.58 million and married couples $23.16 million tax-free - you may not need to move assets.

Also check when your life insurance expires. Consider how long to keep it if you think you might outlive the policy.

6. Have your children passed the ages specified in a children’s trust (in which you designate money for such specific purposes as education, home down payments or weddings once the kids reach stipulated ages)? If your estate documents call for a trust to give children access to money at certain ages after you die, you may be able to delete that language if the kids are older than the specified ages.

7. What happens if one of your kids gets divorced? A trust can help you protect assets for your child or grandchild.

8. Do you have heirs with special needs? Don’t assume typical estate documents help such an heir. Seek out a financial advisor and attorney who specialize in this planning.

9. Check beneficiary designations on brokerage accounts, insurance policies and retirement accounts. Anybody you don’t want there?

10. If you filled out a brokerage account application (or any beneficiary designation), understand the firm’s policy when one beneficiary dies before the others. If you want the share of the assets to pass by bloodline - to the deceased’s children, for example - you may need to put in language specifying per stirpes (distribution of property when a beneficiary with children dies before the maker of the will).

Otherwise, the remaining listed beneficiaries may simply divide the assets.

11. Often a parent names a child on a bank account so the child can access or use the money if the parent can’t act. Understand that if you name your child as a joint owner on an account, the money passes to your child no matter what your will dictates.

The child splitting the money with someone else constitutes a gift, though one probably not subject to gift tax now that gifts of less than $5.34 million aren’t taxed. Still, think carefully so you keep the family peace.

12. Do your heirs know where to find all your important information? Let someone know the password to the app where you keep all your passwords - you must remember digital assets now, too.

Have questions? Click here to contact us.

“12 Estate Planning Must-Dos". AdviceIQ FMEX 2020.https://fmexcontent.s3.amazonaws.com/1289/1289.pdf

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of December 11, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The S&P 500 edged lower this week on the back up in weekly jobless claims and sentiment that negotiations over the additional relief package have come to a standstill.

- On the economic front, besides jobless claims, optimism among small businesses was dialed back, and the consumer price index rose more than expected.

- The pandemic continues to dictate the path of economic recovery in the short run. The lack of progress on the stimulus package creates a risk of setting back the hard-won progress the U.S. has made over the past six months

Economic Progress Shows Signs of Waning

The week was a relatively quiet one on economic and financial fronts. Wall Street was chasing unicorns as share prices of home-sharing Airbnb and food-delivery DoorDash apps surged in their first days of trading. Nonetheless, the broad market edged lower this week on rising jobless claims and the sense that negotiations over a fiscal relief package have come to an impasse.

Besides the weekly release of jobless claims, the economic calendar was marked by reports on small business confidence and consumer price inflation. Optimism among small business owners pulled back by 2.6 points in November, reflecting the resurgence in COVID19 cases. The share of businesses expecting economic improvement declined, while the proportion of firms anticipating rising price pressures picked up on expectations of lower earnings and increased operating costs.

As if in corroboration of this sentiment, the consumer price index rose one tick higher than expected with a bump of 0.2% month-on-month but remained flat at 1.2% year-on-year (Chart 1). The core index, which excludes food and energy, remained unchanged from the prior month at 1.6% on a year-on-year basis. Inflation is still not a pressing concern, but it is worth paying attention to it. The economic shock also has supply-side implications – as noted by small businesses – which could show up in higher inflation even in the absence of robust economic growth.

This in turn could muddy the waters for the Fed. Today, markets expect that the policy rate will not see a hike until 2024. That’s a long time from now and if inflation does pick up, it could very well move sooner. Still, with the Federal Reserve signaling an increased willingness to tolerate inflation above its 2% it will take a convincing move to budge expectations.

In the meantime, the unexpected acceleration in weekly jobless claims shows that the economy is far from a full recovery. Initial unemployment claims jumped by 137,000 to 853,000, while claims under the Pandemic Unemployment Assistance program (supporting self-employed and contract workers), increased by 139,000 to 427,000 (Chart 2). These were the highest increases since September. Unfortunately, the upward trend is likely to persist as restrictions increase.

This proves that the pandemic continues to dictate path of economic recovery. This week, an unprecedented record of 3,088 deaths on December 9th was yet another macabre reminder of the toll of the virus. The Institute for Health Metrics and Evaluation estimates that the need for hospital resources, such as intensive care units and invasive ventilators, has surpassed mid-April’s highs and is expected increase further. Tighter hospital capacity appears likely to force local governments to increase business restrictions further.

While the vaccine offers a light at the end of the tunnel, without some additional supports the economy’s resilience will once again be tested by the virus. Here’s hoping an agreement can be reached that maintains the solid progress made to date.

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

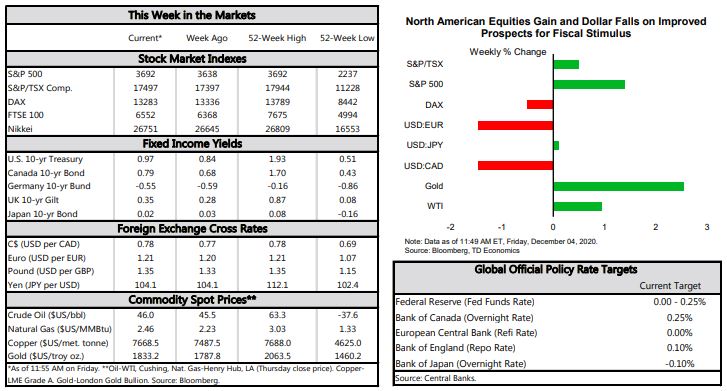

Financial News for the Week of December 4, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Financial markets remained upbeat this week, looking past the near-term risks associated with the ongoing health crisis.

- Economic data delivered a mixed bag. Both ISM activity indexes remained in expansionary territory and jobless claims showed improvement, but nonfarm payrolls disappointed with lower-than-expected gains in November.

- The surge in infections is expected to continue until early January. Fortunately, prospects for additional fiscal supports brightened this week, which would go a long way to supporting the recovery into the New Year

U.S. – December Calm Before the Storm

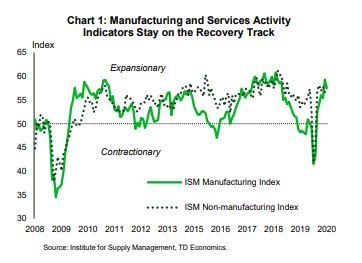

The first week of December brought a mixed bag of economic and financial data. On the financial front, the S&P 500 continued to defy gravity, setting a record high almost every day of the week despite soaring cases of coronavirus infections and related deaths. Markets looked past the near-term risks associated with the continued health crisis and focused on the positives. The “reopening trade” that started with positive vaccine news continued into the fourth week, while renewed hopes of an additional fiscal package added fuel to the fire. The likelihood of a deal before the end of the year improved this week, as news broke of a $908 billion compromise offered by a bipartisan group of Senators.

On the economic side, the data was rich this week. The Institute for Supply Management released November updates for its manufacturing and non-manufacturing purchasing managers indexes. Both indexes posted moderate declines but remained in expansionary territory, indicating a slowing but still positive pace of improvement (Chart 1). The slowdown in manufacturing was driven by new orders, production and inventories, while the employment sub-index moved back into contractionary territory just one month after posting an above-50 reading in October. Overall, the index remains at the high end of historical readings, suggesting that manufacturing demand remains strong for most sectors. The recovery in services, meanwhile, continued for the sixth month in a row despite increased restrictions across several states in November. Sectors sensitive to social distancing measures remain in contraction and are unlikely to get a recovery boost until more progress is achieved in defeating the pandemic.

On the employment front, the data was mixed. Last week’s jobless claims declined after a two-week consecutive increase. However, the reading may be overstated due to processing complications during the Thanksgiving holiday. To make matters worse, the weekly claims report came under scrutiny due to a GAO report noting “flawed estimates of the number of individuals receiving benefits.”

The November nonfarm payrolls report was more in tune with the epidemiological data. Employment rose by 245k – roughly half the amount that economists expected. Employment gains were particularly modest in the leisure and hospitality sector, which remains one of the most badly hit sectors of the economy (Chart 2). The unemployment rate fell to 6.7% from 6.9% but was marked with a sizeable decline in the labor force. The number of people not counted as unemployed but who want a job rose by almost 450 thousand to 7.1 million, 2.2 million more than in February 2020.

Moderate employment data provides more evidence of a bifurcated recovery, suggesting that more relief measures are required to support American households that are struggling in this pandemic. According to the most recent Household Pulse Survey 32% of families reported some difficulty paying for usual household expenses during the coronavirus pandemic. As the surge in infections is not expected to wane until at least early January, there is a strong case for additional fiscal supports. Fingers crossed the message appears to be getting through.

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

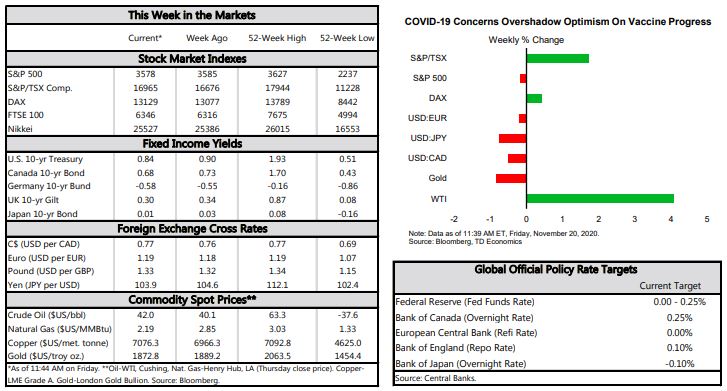

Financial News for the Week of November 20, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- COVID-19 concerns took center stage again this week as cases surged to new daily records. This overshadowed optimism on vaccine progress and mostly positive economic data, with U.S. equity markets trending modestly lower as a result.

- Retail sales grew by 0.3% in October, extending their winning streak. Housing market data meanwhile continued to surprise on the upside, with existing home sales up 4.3% on the month and housing starts up 4.9%.

- Signals from the labor market were not quite as upbeat, with initial jobless claims recording a mild increase to 742k last week from 711k the week earlier.

It’s Always Darkest Before the Dawn

Concerns around the spread of COVID-19 took center stage once again this week as infections surged to new records. Optimism over vaccine progress and broadly positive economic data generally played second fiddle. Equity markets trended modestly lower on the week as a result.

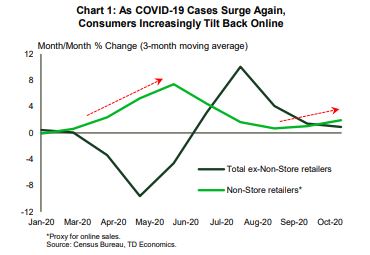

On the economic data front, retail sales improved by 0.3% in October, extending their winning streak to six months. The outturn, however, was below market expectations and a marked deceleration in the pace of gains from the 1.5% averaged in the three months prior. Within this slowing trend, there’s a noticeable shift toward online shopping. Sales at non-store retailers, a proxy for online sales, appear to be taking the lead once again as in-store sales moderate – a divergence that is in line with the third wave of COVID cases (Chart 1).

Home sales, meanwhile, continued to be robust in October. Existing home sales defied market expectations, rising by 4.3% (Chart 2). The growth in resale activity over the past several months has been nothing short of remarkable. Sales are now up nearly 27% from year-ago and 19% from the pre-crisis peak. The number of homes for sale, on the other hand, is in short supply. At the current sales pace, there is just 2.5 months of supply on the market - a record low. With such little product for homebuyers to choose from, the median sales price accelerated further, to 15.5% year-over-year. The strong acceleration in home price growth has overwhelmed the positive impact of record-low mortgage rates on housing affordability. The combination of deteriorating affordability and low supply is likely to lead to a more moderate pace of sales growth going forward.

The good news is that new supply does appear to be responding to these market forces. With builder confidence riding high, housing starts also defied expectations in October, rising a better-than-expected 4.9%. The increase was driven entirely by single-family starts – a clear signal of the shift in housing preferences during the pandemic.

Signals from the labor market were not as upbeat. While continuing jobless claims trended lower at the beginning of the month, initial jobless claims recorded a mild increase to 742k last week from 711k the week earlier. The still-elevated level of initial claims, a proxy for layoffs, points to softer labor market momentum. The rising spread of COVID-19 is an added near-term risk. With hospitalizations also trending higher, several jurisdictions throughout the U.S. are leaning more heavily on containment measures, which will weigh on business activity and hiring. What’s more, with the virus spreading out of control, stronger measures, such as lockdowns, cannot be ruled out for some parts of the country.

With more containment measures, no new fiscal supports, and the expiry of several Fed emergency lending programs (corporate credit, municipal lending and Main Street Lending programs), the near-term outlook is looking darker. Indeed, it appears that a sustained improvement in economic activity will likely have to wait for a vaccine. Fortunately, there is a light at the end of the tunnel. Major positive developments on the vaccine front in recent days suggest potentially earlier availability and the return to normal in 2021. It’s always darkest before the dawn.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Determining When to Take Social Security Benefits

Determining When to Take Social Security Benefits

The benefits of postponing until your full retirement age

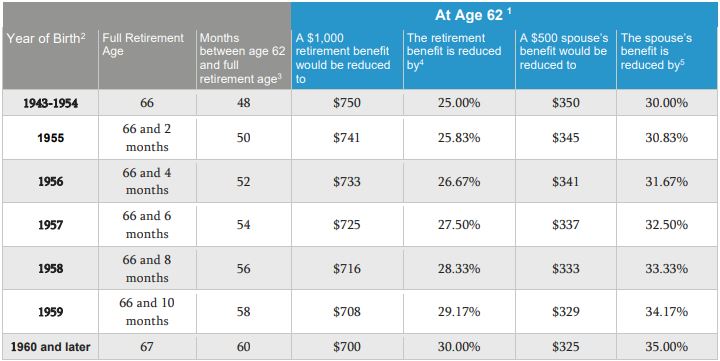

Social Security is an asset that is taken for granted by many folks. If you are tempted to take Social Security early, when first eligible at age 62, think again: your check will be lower if you don’t wait until what’s called full retirement age. Further, married couples benefit additionally from Social Security planning strategies that can provide additional income.

The Social Security Administration is not allowed to advise on strategies to maximize your benefits, so don’t expect to learn about this from the government. But a financial advisor can help you determine how long you should work and what you should do in retirement to avoid outliving your assets.

Before You Make a Decision

As with everything in life, there are advantages and corresponding disadvantages to every decision and that is true when you are deciding whether or not to take your social security benefits before your full retirement age. On the one hand, if you do take your benefits before your full retirement age, then you can collect benefits for a longer period of time. How much longer? Well, that answer is unknown, unless you for sure know your life expectancy.

The disadvantage to taking your retirement benefits before your full retirement age is that your benefits will be reduced. Reduced by how much? Take a look at the chart below to find out.

The decision on when to take your social security benefits is a personal one – there is no “perfect age” for everyone. But remember that when you decide to take your social security benefits, the amount you receive when you first get benefits will set a baseline for the amount you will receive for the rest of your life.

So you need to ask yourself at least these three questions:

- Do I plan to continue working?

- How is my health?

- Are there other family members qualifying for benefits based on my decision?

Full Retirement and Age 62 Benefit by Year of Birth

Speak with an Advisor

Again, the Social Security Administration is not allowed to advise on strategies to maximize your benefits, but a financial advisor is. A financial advisor can run different retirement scenarios based on different variables such as: where you are today, how long you might work, projected rates of returns, and future living expenses, while also factoring in rising health care costs, among other things. Ultimately, the decision is, of course, yours. However, a financial advisor can help you make the most informed decision based on your personal goals and objectives.

Click here to speak with an advisor today.

1 You must be at least 62 for the entire month to receive benefits

2 If you were born on January 1st, you should refer to the previous year.

3 If you were born on the 1st of the month, we figure your benefit (and your full retirement age) as if your birthday was in the previous month. If you were born on January 1st , we figure your benefit (and your full retirement age) as if your birthday was in December of the previous year.

4 Percentages are approximate due to rounding.

5 The maximum benefit for the spouse is 50 percent of the benefit the worker would receive at full retirement age. The percent reduction for the spouse should be applied after the automatic 50 percent reduction. Percentages are approximate due to rounding

“Open Enrollment Season is Around the Corner". FMEX 2020.https://fmexcontent.s3.amazonaws.com/1289/1289.pdf

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.