Financial News for the Week of January 28, 2022

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The Fed left the policy rate unchanged at this week’s FOMC meeting but signaled that a rate hike was imminent come March. Uncertainty on the pace of hikes post March remains elevated, contributing to stock market volatility this week.

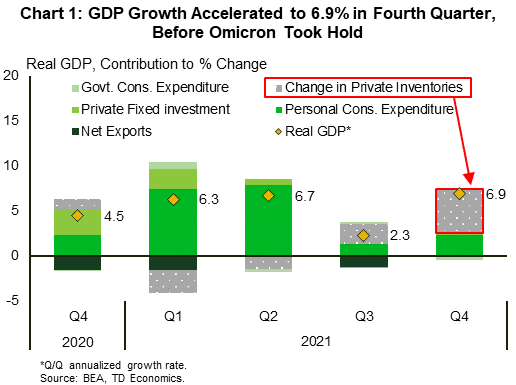

- The U.S. economy grew at 6.9% (annualized) in the final quarter of 2021 – a notable acceleration from the 2.3% pace in the in the quarter prior. Powering growth was a buildup of inventories.

- Consumer spending ended the year on a soft note, with real spending down 1.0% (m/m) in December. Pending home sales also ended the year on weak footing, falling 3.8% last month.

U.S. -Fed Sets the Stage for Rates to Liftoff Soon

The last week of January was rich on data reports, but the FOMC meeting absorbed much of the limelight in financial news. While the Fed left its policy rate unchanged, it delivered its clearest warning yet of imminent rate hikes. A March rate hike is now almost guaranteed, with market odds currently pegged at over 95%. That is likely just the start in what is sure to be a sequence of hikes. Concerns about future monetary tightening contributed to stock market volatility this week. Ultimately, the pace of rate hikes will depend on the pandemic, global supply chains and how aggregate demand reacts to higher rates.

The economy ended last year on a solid note, with a 6.9% annualized jump in fourth quarter real GDP. The acceleration in growth was powered by substantial inventory restocking. Inventories contributed 4.9 percentage points to the headline tally – accounting for over 70% of growth in the quarter (Chart 1). The inventory buildup was led by the retail and wholesale trade industries, with retail auto inventories leading the charge. Business investment (+2% annualized) and consumer spending (+3.3%) also contributed to growth, while a decline in government spending (-2.9%) was a small detractor.

Last quarter’s strong showing largely reflects activity before the Omicron infection wave took hold. Other data this week also pointed to slowing economic momentum at the turn of the year. December’s personal income and spending report showed that real spending fell 1.0% on the month, due primarily to a pullback in goods spending. Services spending remained in positive territory, but spending at restaurants and bars declined, likely reflecting consumer caution due to the rapid increase in COVID-19 infections. Close-contact services are likely to see further weakness in January as high-frequency indicators point to softening in things like air travel.

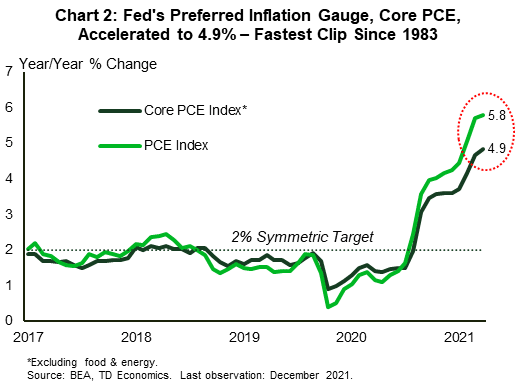

Inflation is adding to consumer woes in financial news. Echoing the acceleration in the Consumer Price Index, inflation as measured by the personal consumption expenditures (PCE) price index rose to 5.8% year-on-year (y/y) in December. Meanwhile, core PCE – the Fed’s preferred inflation gauge – accelerated to 4.9% y/y, moving further away from Fed’s target (Chart 2).

Second-tier data reports also point to slower near-term growth. Pending home sales fell 3.8% in December, marking the second consecutive monthly decline for the series. Pending sales lead actual (closed) sales by 1-2 months, with the recent weakness pointing to a soft start to the new year. A dearth of housing inventory is a key factor behind the weaker year-end trend. Looking at the start of this year, higher mortgage rates and uneasiness among prospective buyers during a surge in COVID-19 infections, are also likely to weigh on activity.

The good news is that the Omicron wave is likely to prove a temporary hurdle to economic activity. New infections in the U.S. appear to have crested. As the economy clears this hurdle, growth should rebound from a modest sub-2% pace this quarter to a much faster clip come spring. Inflation, however, is likely to remain elevated through 2022, even as it decelerates from the current highs (see here).

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 21, 2022

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Early signs of the pandemic’s toll on economic activity were evident in softer-than-expected home sales and a deceleration in regional manufacturing surveys.

- The current soft patch will likely prove temporary, and the broader economic trend is still one of robust growth.

- With strong demand showing increasing resilience to new pandemic waves, the Fed will remain on course to raise the federal funds rate.

U.S. -Momentum Slows Amid Pandemic Wave

This week’s data releases showed some slowing in U.S. economic momentum through the winter months in financial news. In line with last week’s reported pullback in retail sales, existing home sales took a tumble in December. The soft patch looks to have continued at the start of the year, with both the Empire State and Philadelphia Fed manufacturing surveys weakening to multi-month lows in January.

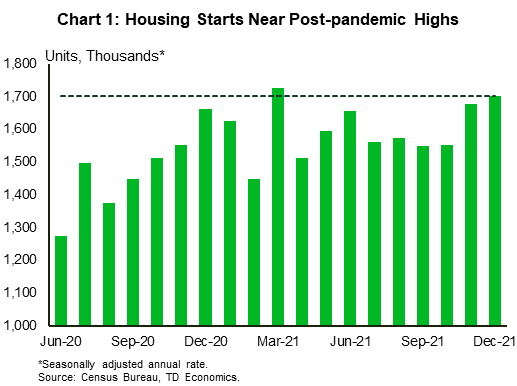

Fortunately, it wasn’t all bad news as housing starts exceeded expectations, hitting their highest level in nine months in December. The virus-induced demand slowdown is likely to prove temporary, and the supply side of the economy is still playing catch up. The Federal Reserve is likely to signal as much at its meeting next week, setting the stage for policy rate liftoff at its following meeting in March (link).

First up, the good news. Wednesday’s release of December’s housing starts data showed homebuilders are adding supply to a market in dire need of it (Chart 1). Starts rose to 1.7 million units (annualized) in December, a 1.7% increase over the prior month. The gain built on upward revisions of 49k units in the prior two months. The improvement was entirely in the multifamily segment, which posted a 51k unit increase (+10.6% m/m), while the single-family segment pulled back 27k units (-2.6% m/m). As starts perked up, so did permitting activity. Permits were up 9.1% for the month, rising to 1.9 million – the highest reading since July 2020. As with starts, this was mostly a multi-family story as permitting in the segment rose 21.9%, dwarfing the 2.0% lift in the single-family segment.

Homebuyers, on the other hand, showed some hesitancy in December. Existing home sales fell 4.6%, undershooting the market consensus for a 0.5% pull back. Surging Covid cases and a lack of inventory explain the setback. At the current pace of sales there exists only 1.8 months’ supply of homes – half the 3.9 months’ average in the three years before the pandemic.

This is an extraordinarily tight housing market, and with demand still strong it’s no surprise that the median transacted price again registered double-digit year-over-year gains – accelerating to 15.8% from 14% in November. The sharp rise in prices has worsened affordability in financial news. Higher interest rates will exacerbate this challenge and are likely to slow demand growth over the next year. The silver lining is that higher prices and higher carrying costs should lead to more supply in both the existing and new market, helping to rebalance the market.

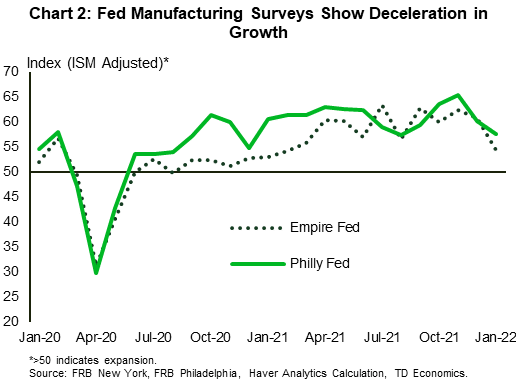

Finally, softening economic conditions were reflected in the Empire State and Philadelphia Fed Manufacturing surveys in January. On an ISM adjusted basis, both pulled back for the month registering 54.4 and 57.6, respectively. While readings above 50 imply the expansion continued in January, the Empire state index is now at its lowest level since January of last year, while its counterpart out of Philadelphia is now at its lowest level since August.

That said, this week’s data reflect a temporary blip in the path of the recovery. The Fed will remain focused on the broader trends – strong growth and persistent shortages – as they start the rate hiking cycle in the coming months.

Andrew Hencic, Senior Economist

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 14, 2022

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Equity markets saw further losses this week, following more hawkish messaging from the Fed. Between Powell and Brainard’s confirmation hearings and other Fed speakers, the signals for a March rate hike are flashing loud and clear.

- December’s inflation data supported the case for a rate hike, with headline inflation reaching 7% year-on-year (y/y). Core inflation also surprised to the upside, and is now up 5.5% y/y – the highest reading in 30 years.

- Retail sales showed a loss of momentum to end the year, as inflation erodes consumer purchasing power. Consumer spending is looking weaker in both the fourth quarter of 2021 and the first quarter of 2022 relative to our latest forecast.

U.S. - Eyeing Inflation Like a Hawk

Equity markets experienced further losses this week in financial news, following more hawkish language from Fed officials that signaled rate hikes could kickoff as early as March. The S&P500 has fallen just over 3% from the beginning of the year. Treasury yields continue to march higher as markets adjust their expectation for monetary policy.

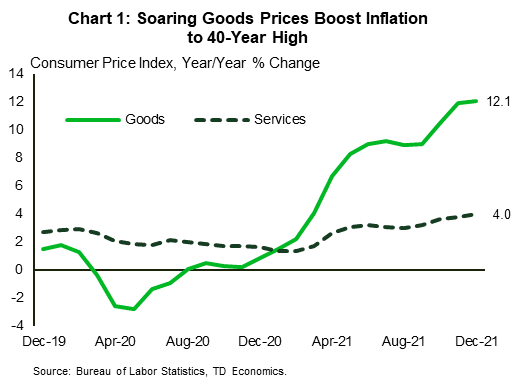

Looking at the recent inflation data, the case for rate hikes is clear. Headline CPI ended the year up 7% year-on-year (y/y), the fastest pace since 1982. In December, the month-on-month pace of inflation cooled slightly to 0.5%, as energy prices were a drag on the headline for the first time since April. But, core inflation was even hotter, up 0.6% m/m, driven by strong increases in shelter inflation and another jump up in used vehicle prices. While those items were the biggest contributors, prices were up strongly for a host of goods and services, continuing a trend of broadening price pressures that has been evident since October – the same month that Fed Chair Powell changed his tune on whether the run up in inflation is transitory.

Accelerating goods prices take much of the blame for inflation’s 40-year record high (Chart 1). You have to go back to 1980 to see goods prices rising 12% in one year. Goods prices should cool over the coming year as production, inhibited by the pandemic and global input shortages, begins to normalize. But, just as it does, service price growth looks to accelerate. Services prices were up 4% year-on-year in 2021, an acceleration from a 3% pace immediately prior to the pandemic, but not out of line with past periods of economic strength. This is likely to move even higher in 2022, keeping pressure on the Fed to tighten policy.

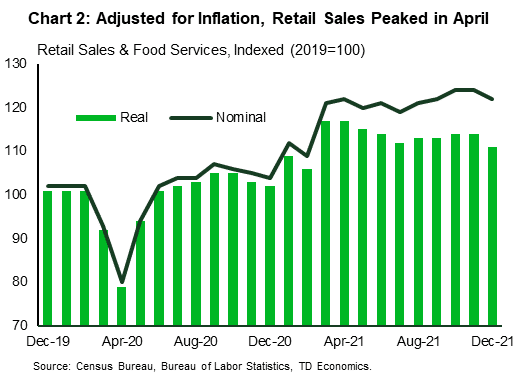

The impact of elevated inflation is already evident in retail sales. Retail sales surged in the spring as a third round of stimulus payments from Washington hit Americans’ bank accounts. Nominal sales have plateaued, in part as consumption shifts away from goods, which dominate retail sales, and towards services. However, when you compare to sales adjusted for overall inflation, you see how price growth has increasingly eroded consumer purchasing power (Chart 2). Given that goods prices are up more than services, the picture is even more dire.

Any way you slice it, December’s retail sales data showed that consumer spending lost momentum towards the end of the year. Our December forecast projected real personal consumption expenditure growth around 6% in the fourth quarter. The data released since suggests that it is going to be closer to 4%. It also provides a soft starting point for the first quarter, where spending is likely to slow to 2% as consumer caution on Omicron weighs on close-contact services.

Inflation is also cutting into wage growth in financial news, something that has not gone unnoticed by Fed officials. At his Senate confirmation hearing, Fed Chair Jay Powell delivered his most hawkish messaging on inflation yet. Fed Governor Lael Brainard, who is the nominee for Vice Chair of the FOMC to succeed Richard Clarida, echoed his remarks, mentioning that workers are worried about how far their paychecks would stretch. Other Fed officials who spoke this week similarly signaled that interest rates are forthcoming, likely beginning as early as March.

Leslie Preston, Senior Economist | 416-983-7053

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 7, 2022

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The U.S. economy kicked off the New Year with an unprecedented surge in COVID-19 cases. While a return to lockdowns is not expected, rising cases could lead to greater absenteeism, as workers self-isolate due to exposure, putting pressure on already-tight labor supply.

- On the upside, several metrics suggests that the supply chain bottlenecks are beginning to ease. Specifically, supplier deliveries in both the manufacturing and services sector were faster in December than they have been in recent months.

- On the labor front, employment came in softer than expected with 199k jobs added in December. The unemployment rate however continued to trek lower, hitting 3.9% (from 4.2%) while the labor force participation rate held steady at 61.9%.

U.S. - Supply Chain Strains Show Signs of Easing

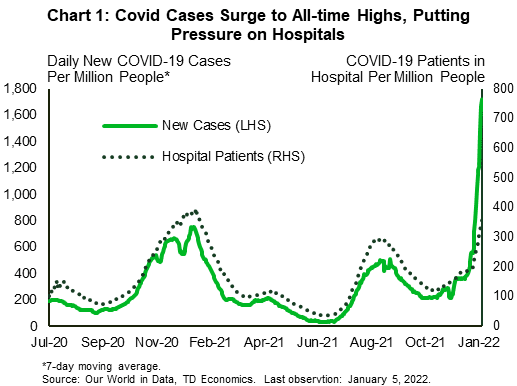

The economic calendar was jammed packed to start the new year in financial news. First up, a rapid increase in COVID-19 cases is quickly dwarfing all previous waves (Chart 1). Fortunately, hospitalization rates are not rising as swiftly, but are still ticking up at the same time that healthcare capacity is constrained by staffing shortages. The surge in cases has prompted airlines to cancel flights and companies to cut services and reduce hours as infected workers self-isolate (though for fewer days than past waves). With worker shortages already a pressing issue, the current wave is likely to weigh on near-term business performance and slow the recovery in high-contact services.

Adding to business challenges, workers are quitting their jobs at record rates, while job openings remain near all-time highs. Employers continue to add jobs, but job growth in December came in notably shy of the 450k anticipated by the market, at 199k. The disappointment was softened somewhat by a net 141k upward revision to the two previous months. The unemployment rate also fell from 4.1% to 3.9%, narrowing in on its pre-pandemic level of 3.5%. With high demand for workers and increasingly limited supply, it is little surprise that wage growth remains hot. Average hourly wages were up 4.7% from year ago levels in December, slowing slightly from 5.1% in November.

Such strength in the labor market, combined with more persistent inflationary pressures has added urgency to the Federal Reserve’s task of curtailing pandemic-induced support measures. Minutes from the most recent FOMC meeting showed that more members are inclined to accelerate the pace of policy normalization. This culminated in the Fed’s decision to speed up the taper of their Quantitative Easing program and possibly faster rate increases.

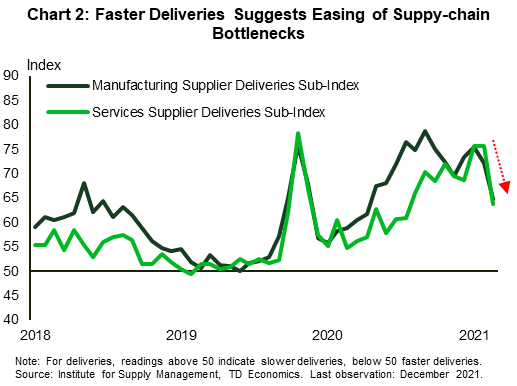

On the production side, there was some good news on easing supply constraints. The ISM manufacturing index slipped to 58.7 in December from 61.1 in November. Despite the slip, manufacturing activity is still expanding at a healthy clip. More encouragingly, there were hints that supply-chain problems could be easing as the supplier delivery sub-index fell to 64.9 in December from 72.2 the previous month (Chart 2). The decline suggests that delivery times are improving, which is a relief given the severe bottlenecks that manufacturers have been facing.

There was also a pullback in the ISM services index to 62 from 69.1 in November. The outturn however was not unexpected, given that the previous reading hit a record. The service sector also saw improvement in supplier delivery times as the index fell by 11.8 percentage points to 63.9 – the lowest reading in the past eight months.

Further good financial news saw vehicle production levels in December improve from their September lows – inching back closer to the 1.1M recorded in November. While still well below the pre-pandemic level, the improvement points to further easing in supply constraints in this key economic sector. Unfortunately, all of this data is for a time before the latest pandemic wave, and we could very well see a reversal in the months ahead. Still, with evidence this wave is progressing even faster than past waves, its peak should also not be too far in the future, allowing with any luck for the continued return to economic normalcy.

Shernette Mcleod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 17, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

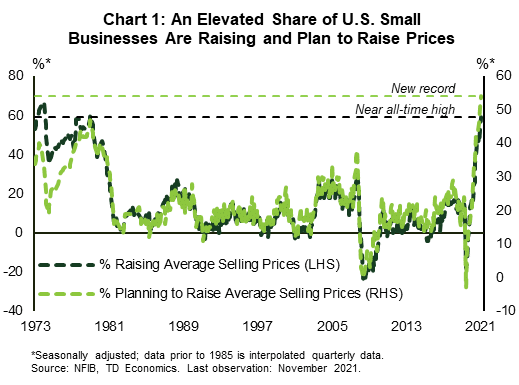

- Evidence of accelerating price pressures continued to trickle in this week. Producer prices accelerated to 9.6% year-on-year in November. This was accompanied by an elevated share of small businesses raising prices (+6 points to 59%).

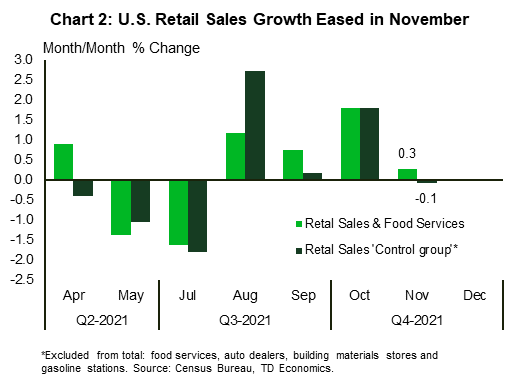

- After a strong gain of 1.8% in October, U.S. retail sales growth slowed to 0.3% (month-to-month) in November. Excluding the more volatile categories, sales in the “control group” fell 0.1% on the month.

- The Fed left the policy rate unchanged at this week’s FOMC meeting, but accelerated the taper of its Quantitative Easing (QE) program. This puts QE on track to end by March of next year, opening the door for rates to lift off soon after.

Slaying the Inflation Dragon

Inflation remained the focus of financial news markets this week, with economic data providing continued evidence of accelerating price pressures. Producer prices picked up steam, rising to 9.6% year-on-year in November from 8.8% in the month prior. The acceleration indicates broad-based price pressures throughout the supply chain. Small businesses are also cranking up the pressure. The National Federation of Independent Businesses optimism survey showed that in November, 59% of businesses had raised average selling prices and another 54% plan to raise them further in the months ahead. The former metric is near its all-time high set in the 1970s and the latter is at a new record (Chart 1).

Inflationary pressures also featured prominently in the retail sales report. Sales rose 0.3% in November, below the consensus forecast for a 0.8% print (Chart 2). A strong 1.7% showing in sales at gasoline stations, which reflects hefty energy price gains, helped drive up the headline. Excluding the more volatile categories (including gasoline), sales in the “control group,” used to estimate personal consumption expenditures (PCE), were down 0.1% on the month. The soft November print can be partially explained by some pull-forward in activity, with consumers starting their holiday shopping early given expected shortages and delays. Less generous holiday discounts relative to what consumers may have been accustomed to are also likely to have played a role in last month’s slow-down. A further moderation in activity is likely in December, given the added hurdle of a worsening epidemiological situation.

New COVID-19 infections have risen across much of the country and hospitalizations have followed suit. The infections trend is likely to worsen further with the spread of the much more transmissible Omicron variant, which has been detected in most U.S. states (see here). This is expected to weigh on consumer and tourism-related activities.

The Fed is well aware of the above two competing forces – rising inflationary pressures and a worsening public health situation. Economic projections from this week’s FOMC meeting show that most committee members expect the setback from the latest infection wave to prove short-lived. The median forecast calls for the unemployment rate to fall further, reaching 3.5% by the end of 2022. Another potential obstacle to growth, the country’s debt ceiling, was neutralized with the swipe of the pen on Thursday, with President Biden signing a $2.5T ceiling increase into law.

Continued progress toward maximum employment will allow the Fed to focus its efforts on slaying the inflation dragon. It is already moving in that direction. The Fed left the policy rate unchanged at this week’s FOMC meeting, but accelerated the taper of its Quantitative Easing (QE) program. The Fed will reduce the monthly pace of purchases of Treasuries securities by $20 billion and agency mortgage-back securities by $10 billion. This puts QE on track to end by March of next year, opening the window for rates to lift off soon after. This is in line with our expectations. In our updated forecast published earlier this week, we pulled forward our call for the first rate hike to the second quarter of next year, with two more hikes to follow later in the year. This will still leave monetary policy in an accommodative stance, but should help to stem the inflationary tide.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 10, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

• Consumer prices continued to accelerate in November. On year-on-year basis, headline CPI was up 6.8% (from 6.2%

previously), the highest in nearly forty years in financial news. Core inflation (ex. food and energy) also accelerated, hitting 4.9% (from

4.6% in October).

• This week’s jobs data signaled more tightness with weekly jobless claims dropping to 184,000 and the ratio of unemployed

to job openings falling to a new historic low.

• Wage pressures are creeping higher. The possibility of faster wage growth become entrenched in prices may motivate the

Fed to move even faster.

All About Inflation

It’s inflation week! Anticipation of today’s CPI report created some anxiety in financial markets but ultimately left them back to where they started on Monday. In financial news equity markets appear to have shrugged off Omicron concerns and remains driven by still-solid expectations for earnings. The bond market appears more cautious on the outlook, with long-term yields well below late November levels, even as Fed communication turns more hawkish.

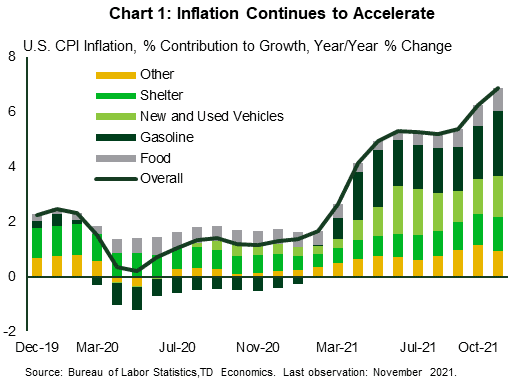

Consumer prices continued to accelerate in November. On a year-on-year basis (y/y), headline CPI was up 6.8% with gasoline prices growing by 58% relative to last year and adding 2.3 percentage points to the headline reading (Chart 1). Food prices remained the second biggest contributor to growth, rising at 6.1% y/y.

Meanwhile, strong demand for goods amidst ongoing supply shortages, continued to drive core prices (ex. food and energy), which picked up to 4.9% y/y. A key source of core price pressures was new and used vehicle prices, which expanded by 11.1% and 31.4% y/y, respectively. In terms of service prices, the shelter cost component continued to accelerate, rising by 3.8% y/y (up from 3.5%). Market-based home prices of the largest metros suggest that there’s more upside for shelter costs ahead (see report), which could lead to more persistent elevated inflation in 2022.

On the labor side of the Fed’s mandate, this week’s jobs data signaled more tightness, with weekly jobless claims dropping to 184,000 – the lowest level since September 1969. Meanwhile, the Job Opening and Labor Turnover Survey (JOLTS) reported 11 million available jobs in October. This number is close to its record high in July and higher than the 6.9 million of workers who were unemployed that month. In fact, the ratio of the unemployed to job openings dropped to an historical low in the month. Adding marginally attached workers back to the labor force, the ratio of unemployed to job openings is slightly higher, but still in line with the average observed in 2019 when the labor market was the healthiest it had been in fifty years.

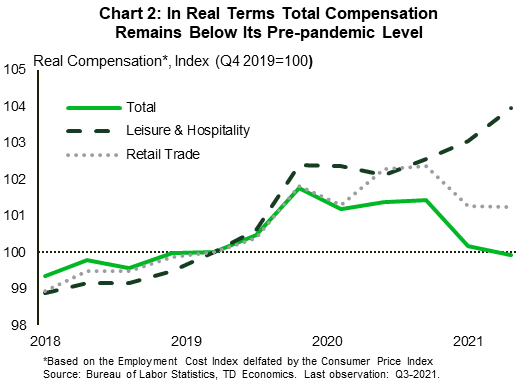

Another reason for labor market tightness is an elevated number of people who are quitting jobs. This fell in October to 4.2 million (from 4.4 million in September), but remains well above pre-pandemic norms. The number of quitters was particularly high in leisure & hospitality and retail trade sectors, which collectively accounted for 40% of quits in October. Notably, these sectors are among the lowest paying and experienced the highest growth in real compensation over the period of the pandemic (Chart 2). Considering that workers in these sectors are in close contact with consumers and face the highest health risk, further increases may well be in store in the coming quarters.

Indeed, inflation is currently rising much faster than wage growth. The story is worse if you consider that total hours are still most depressed at the low end of the wage spectrum, inflating the aggregate reading. The risk of workers demanding higher wages to compensate for the increase in prices (thereby entrenching higher inflation) is becoming a risk the Federal Reserve can no longer ignore and is likely to lead to a faster pace of asset purchase tapering and the start of rate hikes by the second quarter of 2022.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 3, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

• The ISM manufacturing index showed signs of easing supply chain conditions in financial news. Supplier delivery times shortened while

production, employment and new orders indexes all increased.

• This week’s payrolls report left something to be desired, but a pop in household employment and a rise in the labor force

participation rate are welcome signs of a recovery in labor supply.

• While the first glimmers of abating supply side issues have emerged, the Omicron variant threatens to undo the progress.

U.S. - Supply Issues Easing, but Omicron Looms

Volatility was the name of the game this week in financial news as markets whipsawed on news of the Omicron variant’s identification in the U.S., and Chairman Powell’s more hawkish stance. Inflation remains front and center as Chairman Powell retired the term “transitory” when describing recent price gains. That said, November’s data offered signs that supply chains challenges have begun to ease, offering some promise of inflation relief.

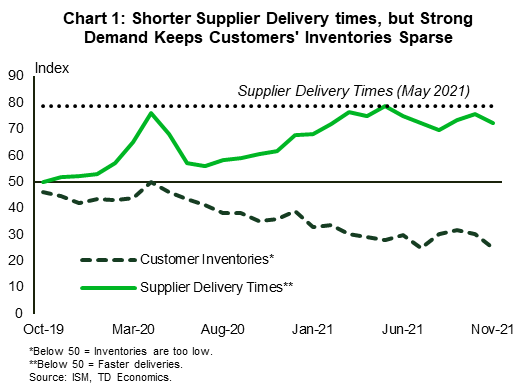

This week’s release of November’s ISM manufacturing survey gave one such signal. The report showed growth accelerating as the expansion carried on for its 18th consecutive month. The details provided further reasons for optimism. The supplier delivery times subindex remained extremely high (you have to look back to the late 1970’s to find a comparable lead time prior to the pandemic), but it pulled back for the first time in three months (Chart 1). Alone, this move doesn’t mean much, but the production, employment, and new orders indexes also all moved higher in November. An environment where production, orders, and employment growth are increasing while supplier delivery times are narrowing is a signal that some of the bottlenecks we’ve been seeing are beginning to clear.

Alas, not all of the news was good. Customer inventories continue to languish at low levels and the index pulled back on the month. This is likely a reflection of continued strong demand that has left producers trying to keep up. Indeed, this month’s vehicle sales report was a reflection of those tight conditions, as monthly sales disappointed, falling to 12.9 million units (at a seasonally adjusted annualized rate). Automotive production ticked up in October, but remains well below underlying demand, which is likely closer to 1.45 million per month. This means inventories will remain scarce for the time being.

At the same time, this week’s payrolls report showed a slowing in the pace of job growth. Markets had expected north of 500k jobs to be added to payrolls, so the 210k realized in November missed the mark.

Despite the disappointing print in the payrolls report there were several reassuring details in the household survey. Household employment increased by 1.1 million people, taking the employment to population ratio up to 59.2%, and continuing its steady improvement. An additional million people working is a good sign, but the increase in the labor force participation rate is another welcome sign for the supply side of the economy (Chart 2). To alleviate reported labor shortages the number of Americans active in the labor market has to increase, and nearly 600 thousand added their names to the hat in November.

This year has been characterized by ample demand and a virus-induced supply shock that has pushed inflation to multi-decade highs. November’s data started showing us signs that the supply side of the economy has begun to recover. The data are reassuring for now, but the emergence of the Omicron variant could derail the fragile improvements that have been made. Even without lockdowns in the U.S., restrictions in less vaccinated nations, or worker fears of infection, could pinch the supply of inputs and labor, pushing prices higher.

Andrew Hencic, Senior Economist

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 26, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

• President Biden removed months of speculation by announcing his nomination of current Fed Chair Jerome Powell

for a second term to head the Central Bank. He will be joined by Governor Brainard who the President nominated

for Vice-Chair. The appointments eased one area of uncertainty around future monetary policy.

• U.S. personal income and outlays gave a reassuring picture of economic momentum heading into the fourth quarter.

Spending on both goods and services accelerated notably in financial news.

• Inflation, as measured by the personal consumption expenditure (PCE) deflator continued to accelerate in October.

Core PCE – the Fed’s preferred gauge of inflation – rose to 4.1% year-on-year, adding to concerns depicted in the

FOMC’s November meeting minutes that price pressures were more persistent and pervasive than previously thought.

U.S. - Consumer Spending Powers

In a week shortened by the Thanksgiving holiday, the U.S. economic calendar was packed. Let’s kick things off with the BEA’s second estimate for third quarter GDP. Economic growth was revised up one tenth of a percentage point to 2.1% annualized. This represents a slowing of economic activity from 6.3% and 6.7% in Q1 and Q2 respectively. The marginal revision reflected a small upgrade to consumer spending that was partially offset by a downward revision to business investment. Given the strength of consumer spending in October (discussed below), we expect a rebound in fourth quarter GDP more in line with the numbers reported for Q1 and Q2.

Up next in Financial News is October’s personal income and spending. The data showed that personal income rose by 0.5% month-on-month (m/m), with the gain primarily reflecting an increase in compensation of employees (up 0.8%) and income receipts on assets (up 0.9%). These were partly offset by a decline in current transfer receipts (down 0.5%). Unfortunately, inflation ate away those nominal gains. Real personal disposable income fell by 0.3% in October, an improvement from the 1.6% decline posted in September.

Nominal personal spending rose by 1.3% m/m in October (up 0.7% in real terms). Goods spending accelerated to 2.2% (from 0.9% in September) and spending on services rose by 0.9% (up from 0.5% in September). Spending on durable goods continued to exceed its pre-pandemic share with consumers spending about 13% of their total expenditures on durables – up from an average of 10% in 2019.

The personal consumption expenditure (PCE) price deflator rose by 0.6% m/m in October. Year-over-year (y/y) it was up 5.0%, 1.2 percentage points below the CPI inflation rate (Chart 1). Excluding food and energy, core PCE inflation rose 0.4% m/m and accelerated to 4.1% y/y (from 3.7%) – like its CPI counterpart, hitting a fresh 30-year high. The core PCE deflator has been running ahead of the Fed’s long-term 2% target since April of this year.

With spending outpacing income, the personal saving rate dropped to 7.3% in October from an upwardly revised 8.2% in September (Chart 2). The figure now stands below the pre-pandemic average of 7.5%, as consumers drawdown excess savings amassed during the pandemic to compensate for months of restricted economic activity (see report).

To wrap things up we turn to activities at the Fed. President Biden announced that he will nominate Jerome Powell to retain his seat at the head of the central bank, with Lael Brainard joining him as Vice-Chair. The announcement ends months of speculation and signals continuity in U.S. monetary policy amid public concerns about inflation.

The central bank also released minutes of its November meeting. The minutes showed continued concerns about widespread price pressures. Chair Powell noted that inflation came in higher than expected and supply bottlenecks were more persistent than initially thought. ‘Uncertainty’ and ‘flexibility’ were key themes. With the potential for a new more contagious COVID-19 variant emerging, the Fed has positioned itself to respond quickly should the realized path of economic activity diverge from expectations.

Shernette McLeod, Economist , 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 19, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

• October retail sales rose a better-than-expected 1.7% on the month. Sales in volatile categories were up robustly, but

sales in the control group also rose a strong 1.6%. Leading the charge on this front was a 4% gain in non-store sales.

• Housing starts fell 0.7% in October as starts in the larger single-family segment declined for the fourth straight month.

Improved homebuilder sentiment in recent months indicates that this sector too may soon turn a positive corner.

• President Biden signing the Infrastructure Investment and Jobs Act (IIJA) into law. The legislation will channel $550

billion in new spending on transportation and other critical infrastructure over the next several years. In addition,

the larger Build Back Better (BBB) social spending and climate bill cleared the House and is headed for the Senate.

U.S. - Infections Trend up as Holidays Approach

Last week’s hot inflation report raised plenty of eyebrows, but this third week of November was more balanced on the data front. Retail sales rose a better-than-expected 1.7% month-to-month (m/m) in October. Sales in volatile categories – gas stations (+3.9%), building materials (2.8%), and autos (1.8%) – were up robustly. Receipts at bars at restaurants, meanwhile, were flat on the month. Sales in the remaining subsectors, known as the ‘control group’, did not disappoint, rising a healthy 1.6%. While most categories recorded an improvement, non-store retailers (a good proxy for online sales) led the charge, up 4%.

The healthy gain in the control group together with the October increase in auto sales points to a healthy start to goods spending in the fourth quarter. Scratching beneath the surface, however, reveals a more nuanced backdrop. The sales gain appears to reflect some pull-forward in activity from the busy holiday season. Consumers have been consistently warned about supply chain issues and possible shortages and many appear to have got an early start to their holiday shopping as a result. A recent survey showed that roughly half of holiday shoppers planned to start shopping before November. The strength in non-store retail sales, a very popular holiday shopping channel, adds credence to this view. While overall spending should remain healthy, it may slow closer to end of the year, reflecting this pull forward. The rise in new COVID-19 infections is an added risk to consumption growth, given that it could further delay the expected rotation in spending toward services (Chart 1).

Tilting to the housing market, homebuilding activity continued to lose steam in October, with starts down 0.7% on the month. Given the myriad of hurdles faced by builders, such as supply-chain disruptions, higher material costs and a shortage of workers and serviceable lots, it should be no surprise that homebuilding has eased a bit in recent months. Starts in the larger single-family segment have been the main contributor to recent downward trend. A steady recent improvement in homebuilder confidence indicates that this sector should turn a positive corner in the near-term (Chart 2). While the upcoming removal of monetary stimulus will pose a hurdle to housing demand in the quarters ahead as it weighs on already-stretched affordability, homebuilding activity is likely to remain well-supported given exceptionally low housing inventory.

The other big developments this week were on the political front, as President Biden signing the Infrastructure Investment and Jobs Act (IIJA) into law. The legislation will channel $550 billion in new spending on transportation and other critical infrastructure. This type of spending tends to carry high economic multipliers, resulting in a larger economic impact than the initial dollar amount spent. And, by raising the stock of productive capital, it may even raise the potential growth rate of the American economy. Still, given that the investments are spread out over several years and that such projects take time to be rolled out, the boost to the economy is likely to be modest and will take time to trickle in. In contrast, the larger $2 trillion social spending and climate bill, which passed the House late in the week, would provide a more noticeable near-term boost to growth in 2022. This package, however, faces a divided Senate and is still far from a done deal.

Admir Kolaj | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 23, 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Without much noteworthy economic data this week, market sentiment soured on a leaked Biden administration proposal to raise the maximum tax rate on capital gains of high-income taxpayers.

- First quarter GDP data and a rate announcement from the Federal Reserve are also on the docket next week. Growth in the first half of this year is coming in faster than we expected, raising the risk of earlier Fed hikes.

Big Events Next Week Drive Markets

Without much noteworthy economic data this week, market sentiment took its cue from policy announcements that are expected next week from the Biden administration. Sentiment seemingly soured on the news that the spending under the American Families Plan will be funded by tax hikes on higher income taxpayers. President Biden had outlined his intention to raise taxes on higher incomes in his campaign platform (see details). Particularly relevant for investors is the proposal to tax capital gains at 39.6% (up from 20%) for people with incomes above $1 million, which would be the same rate as the top marginal rate on income under Biden’s proposals (Chart 1). That would match the late 1970s, the highest rate historically, however, Bloomberg estimates this would only affect about 0.3% of the population.

These changes need to be passed by Congress, and so will either require Republican support or budget reconciliation. The latter is more likely, and therefore the support of moderate Dems, like Joe Manchin and Kyrsten Sinema, may mean tax hikes could be watered down before they are passed. The White House is still finalizing the details of its plan. The key spending items will likely include funding for platform promises like: paid family leave, child care, universal pre-K and free community college.

{kind=link}

There is also some big economic news coming next week: first quarter GDP and a Federal Reserve interest rate announcement. We expect economic growth to accelerate to a 6% annualized pace in Q1, up from 4.3% in Q4 (Chart 2). This acceleration will be largely due to jump up in consumer spending – from 2.3% in Q4 to 10% in Q1. The second wave of Covid-19 infections and associated restrictions had held back spending at the end of 2020, but fiscal stimulus that has come in two waves over the course of Q1 has boosted spending. Recall eligible Americans received $600 payments back in January, and a further $1400 in late March. We have seen in retail sales and high-frequency data that consumers haven’t hesitated to spend these windfalls.

Personal income and spending details for March will also be released on Friday, which will tell us a lot about momentum heading into Q2. We expect it to be healthy. Overall, growth in the first half of the year is tracking better than we expected in March, and on its own is enough to raise 2021 real GDP growth forecast from 5.7% to 6.2%.

This upgrade to economic growth raises the risk the Fed will hike rates sooner than we expected in March. So we will be listening very closely to how Chair Powell talks about the outlook on Wednesday. This is not a meeting with a summary of economic projections but shifts in messaging will be closely parsed. We will be publishing Dollars and Sense next week – so stay tuned for our updated view on the Federal Reserve.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.