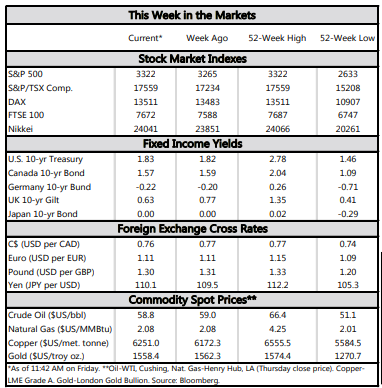

Financial News for the Week of August 7, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Despite a surge in COVID-19 cases in July, economic data remained broadly positive. Vehicles sales rose 11.3% to a better-than-expected 14.5 million (SAAR). The ISM indices also ticked up on the month and beat expectations.

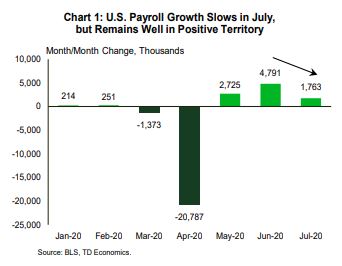

- Importantly, the employment report confirmed that the jobs recovery continued in July, albeit at a slower pace. The U.S. added a better-than-expected 1.8 million jobs, while the unemployment rate fell to 10.2% from 11.1% in June.

- A downward trend in new infections in very recent days marks another positive development. Hopes are also high for a new stimulus package. But, it is unclear if an agreement regarding the stimulus can be achieved in short order.

Historical Decline in GDP As Virus Struck in Q2

Auto sales continued to improve for the third consecutive month in July, rising by 11.3% to a better-than-expected 14.5 million (SAAR) units. In similar fashion, the ISM indices made gains on the month and came in better than expected. The manufacturing index rose 1.6 points to 54.2 in July, with broad-based gains across subcomponents. Its non-manufacturing counterpart did not exhibit the same breadth of gains, but the headline still ticked up one point to 58.1, thanks to a sizable pickup in new orders. While the ISM indices are signaling an expansion at the fastest pace since early 2019, it is important to recall that both sectors are coming out of a very low activity period.

When it comes to gauging the overall health of the labor market, the monthly employment report takes the cake. The July report showed that the recovery in jobs continued last month, albeit at a slower pace (Chart 1). The economy added 1.8 million jobs, beating market expectations. Gains were concentrated in leisure & hospitality, government and retail trade. This brought the three-month tally to 9.3 million, which means that a little over 40% of the jobs lost in the March-April period have been recovered.

The unemployment rate, meanwhile, improved further in July, falling to 10.2% from 11.1% in June, as the number of unemployed persons fell by 1.4 million. The theme of more Americans being called back to work remained evident in July as the number of people on temporary layoff fell 1.3 million to 9.2 million, while the number of those on permanent layoff was virtually unchanged at 2.9 million.

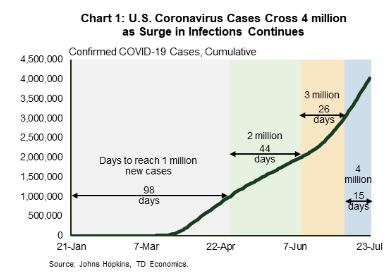

Despite everything, there are indications that this latest health-induced hurdle too shall pass in time. For instance, over the last several days, infections appear to be slowing again on a trend basis (Chart 2). If sustained, this downward trajectory will eventually help grease the wheels of the reopening process.

At the same time, a new stimulus package that’s being negotiated in Washington is expected to lend another hand to the recovery. Hopes are high for stimulus on several fronts (enhanced unemployment benefits, stimulus checks, aid to small business and state and local governments, along with rent, mortgage and food assistance). But, given large outstanding differences in Congress, it is unclear if an agreement can be achieved in short order. Timing is of the essence to avoid further financial stress and to support the confidence channel.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of July 31, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Real GDP fell by an historic 9.6% in the second quarter (32.9% annualized), led by declines in spending on services as the economy locked down in March and April.

- The fall was deep but short. Spending rebounded in both May and June. Consumer spending rose 5.2% in June, with all major categories seeing improvement.

- Income supports go a long way in explaining the resurgence in consumer spending. The expiry of extended UI benefits at the end of July puts this at risk and represents a clear and present danger to the economic recovery

Historical Decline in GDP As Virus Struck in Q2

This was a unique economic decline. Falling consumer spending on services made up nearly 70% of the drop in GDP in the quarter. Typically in recessions, services spending is relatively unscathed. Amazingly perhaps in a health crisis, spending on healthcare made up nearly a third of the overall decline in GDP. The pullback reflects the exceptional circumstances brought on by the virus and the sudden lockdown of the economy in the final weeks of March, including non-essential medical procedures. The pace of decline was fastest in April, the first month of the second quarter. Spending rebounded in May and June as the economy re-opened.

Indeed, June income and spending data, also released this week, showed consumer spending growing by 5.2% in the month (non-annualized), with all categories seeing gains. Spending increases were led by goods categories, especially durables, which rose 8.8%. As of June, goods spending was nearly 5% higher than its pre-crisis level, with durable goods spending 9.5% above its February level. Services spending, however, still has a way to go, down close to 12% from its pre-pandemic level.

This speaks to the importance of fiscal supports in maintaining the economic recovery. Negotiations in Washington on the next wave of support are ongoing but stalled this week. This as extended unemployment benefits expired on July 31st. As a result of the expiry, income will fall further in August for the close to 30 million people currently receiving this life line. Without additional supports, spending will retrace the improvement seen in May and June and set the recovery back.

In fact, warning signals that the economic recovery is tapering off in July continued to build in other indicators this week. Weekly jobless claims rose in the week ending July 25 for a second straight week. There is an important caveat to this data – it is seasonally adjusted to reflect typical July patterns, which may be less accurate in the current environment. Unadjusted, claims fell in the week. However, even here, the improvement appears to have stalled at a level still consistent with a deep economic contraction. The rise in COVID cases and slowdown in economic progress has not gone unnoticed. Consumer confidence pulled back in July, falling six points to 92.6, moving it further away from its peak of 132.6 in February.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

COVID Forcing Some Colleges to Close Forever

COVID Forcing Some Colleges to Close Forever

College savings tips – because the costs of college are not going down

As if the country needed another divisive topic, the debate about reopening schools this fall is splitting communities, educators and families. According to a recently released poll by the Kaiser Family Foundation, 60% of parents want schools to delay openings whereas 34% prefer schools open on time. Want more divisiveness? The KFF reports that Democrats (87%) are overwhelmingly in favor of delaying the start of the school year.

While parents of children in K-12 are struggling with this decision, parents of college-aged kids have another disaster looming large this fall: will their college/university even survive? Consider that revenues are already down for most colleges and universities, no one knows how many kids will even come back to college this fall, and some colleges were really struggling to survive prior to COVID-19, it’s a topic that must be addressed – because no one thinks college costs will decline next year.

10-20% of Colleges to Close?

You have likely seen the news reports that so-called “experts” are predicting that approximately 10% to 20% of colleges will have to close their doors permanently due to COVID-19. But a more detailed analysis by a New York University professor actually names which colleges might go belly-up.

New York University professor Scott Galloway analyzed the 437 colleges and universities in the US News and World Report’s Top National College Rankings and separated them into four quadrants to see which ones were more vulnerable to COVID-19. Each school went into a quadrant titled: Struggle (131 schools); Thrive (88); Perish (89) or Survive (128).

Here are Professor Galloway’s quadrant descriptions, taken directly from his blog:

- Thrive: The elite schools and those that offer strong value have an opportunity to emerge stronger as they consolidate the market, double down on exclusivity, and/or embrace big and small tech to increase the value via a decrease in cost per student.

- Survive: Schools that will see demand destruction and lower revenue, but will be fine, as they have the brand equity, credential-to-cost ratio, and/or endowments to weather the storm.

- Struggle: Tier-2 schools with one or more comorbidities, such as high admit rates (anemic waiting lists), high tuition, or scant endowments.

- Perish: Sodium pentathol cocktail of high admit rates, high tuition, low endowments, dependence on international students, and weak brand equity.

Nevertheless, one thing is for sure: the cost of college will not be cheaper next year, and parents should be prepared to pay more.

Think 529

When it comes to 529 college savings plans, the best strategy is to start early and start big. Don’t wait to set up an account until your teenager is starting to wonder which schools might offer skateboarding scholarships. These accounts are excellent vehicles to save for college, in large part because of the taxfree growth they offer. Here are some suggestions for getting the most benefit from a 529 plan.

Start as early as possible. The best time to start a 529 plan is at birth. Well, maybe a few weeks later because you do need to wait until your kid gets a Social Security number. The earlier an account is established, the more years of growth it provides. Ideally, the plan and the child grow together.

In the early years, invest more aggressively. It would be a shame to open a plan for a two-year-old and put everything in a money market fund or bonds when the goal in the early years should be growth. Invest heavily in equities for about the first 10 years then gradually move to bonds and other low-risk options. Many plans have an age-based option that does this automatically.

Fund the plan as much as you can when the child is young. Obviously, this can be a challenge for young families. If you can, however, it’s good to start with higher monthly amounts, even if you need to taper off your contributions as the child gets older. The goal is to get as much into the plan as you can.

Pay attention to fees and performance. Investment firms sell many 529 plans, and the commissions you pay them vary. Some offer mutual funds with relatively high annual fees. Fees are required to be clearly disclosed. Look at the performance of the fund managers too.

Compare several state plans. While some states do offer tax breaks for residents who use their 529 plans, you aren’t limited to the plan from your own state. You can open new accounts in or move existing accounts to other states.

Avoid Short-Changing Your Retirement

Don’t get so excited by the idea of maximizing a 529 plan that you forget one essential guideline: Parents should fund their own retirement accounts ahead of funding college accounts for the kids.

There are many places to find a little extra money for kids’ 529 plans. A few possibilities are cash gifts from relatives, contributions from grandparents, tax refunds, or bonuses. But the worst place to find that money is your own retirement fund. It isn’t wise to sacrifice a healthy retirement plan in order to create a healthy 529 plan.

Finally, make sure you talk to your financial advisor in order to confirm that the college savings decisions you make are consistent with your overall financial plan.

Have questions? We can help!

Wondering what the best way to fund your child's education is? We are here to help, contact us for more information.

“COVID Forcing Some College to Close Forever"FMEX 2020. https://abm.emaplan.com/ABM/api/v1/StoredFile/cda87305-6b3e-4794-9498-0552159efdd9/download

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

8 Exit Strategies for Business Owners

8 Exit Strategies for Business Owners

Are you a business owner thinking about exiting your company? Which exit strategy will benefit you most? It’s a tough move to undo, and you should know the pluses and minuses going in.

While the number of exit routes seems unending, you generally choose from only eight:

- Transfer the company to a family member.

- Sell the business to one or more key employees.

- Sell to employees using an employee stock ownership plan.

- Sell to one or more co-owners.

- Sell to an outside third party.

- Engage in an initial public offering.

- Become a passive owner.

- Liquidate.

While your emotions during the exit process can overwhelm you at times, your decision making can be relatively straightforward, so long as you keep the end in mind and do some up-front planning.

Planning early is key

First, establish personal and financial objectives to identify the best buyers of your business. Second, determine the value of your company. Finally, evaluate tax consequences of each exit path. Let’s explore the eight business exit strategies.

Transfer to a family member

Owners usually consider transferring businesses to family members for non-financial reasons. Among the advantages, this transfers the company to a known entity, provides for the well-being of your family, perpetuates your company’s mission or culture and allows you to remain involved in the business.

Disadvantages include:

- little or no cash from closing available for retirement

- increased (and continued) financial risk

- required owner involvement in company post-closing

- children’s inability or unwillingness to assume the ownership role and

- the family issues that surround treating all children fairly or equally.

Transfer to key employee(s)

With this type of transfer, you hope to achieve the same objectives as when transferring the business to a family member, with the added goal of achieving financial security (albeit potentially over time).

Disadvantages of this route resemble those in family transfers and include employees’ possible inability or unwillingness to assume ownership.

Transfer via ESOP

These qualified retirement plans must invest primarily in the stock of the sponsoring employer. In addition to the advantages of a standard transfer to key employees, you enjoy tax benefits as well as cash at closing.

Again though, not all aspects of this route benefit you. ESOPs are costly and complex, offer limited company growth due to the borrowing necessary to buy the owner’s stock, net less than full value at closing compared with third-party sales, and use company assets as collateral.

Sale to co-owners. Advantages again resemble those of transferring your business to a family member. Disadvantages include the need to typically take back an installment note for a substantial part of the purchase price and, as in other avenues, increased financial risk, owner involvement past closing, and normally netting less than full fair market value.

Sale to a third party

This generally offers your best chance at receiving the maximum purchase price for your company and the maximum amount of cash at closing. This route appeals to owners intending to leave after they sell and to owners who want to propel the business to the next level with someone else’s financial support. It also allows you to control your date of departure.

Disadvantages include:

- potential loss of your personal identity as the business owner

- potential loss of your corporate culture and mission

- potential detriment to employees if you sell to a party that seeks consolidation and

- part of the purchase price may be subject to future performance of the company after the sale.

IPO

This route offers high valuation and cash for the business. Unfortunately, an IPO comes with significant disadvantages—just ask Elon Musk of Tesla. The disadvantages of this route are primarily:

- limited liquidity at closing

- not a full exit at closing

- loss of full control and

- additional reporting and fiduciary requirements

Your company needs to be worth over $250 million in order for the IPO route to be considered an appropriate exit option.

Passive ownership

This attracts owners who wish to maintain control, become less active in the company, and preserve the company culture and mission. Your disadvantages stem from you never being able to permanently leave the business, you receive little or no cash when you leave active employment, and you continue to carry the risk associated with ownership.

Liquidation

Only one situation justifies this route: You want, or need, to leave the company immediately and have no alternative exit strategies. Liquidation offers speed and cash, but can bring enormous disadvantages:

- yields less cash than any other exit route

- comes with a higher tax burden than any other type of sale/transfer and

- has a potentially devastating effect on employees and customers.

Have questions? We can help!

We are available to offer guidance, examples, and market perspectives as well as help you carefully compare each path in relation to your final objectives. Contact us for more information.

“The 8 Exit Strategies for Business Owners"ABM. https://abm.emaplan.com/ABM/api/v1/StoredFile/cda87305-6b3e-4794-9498-0552159efdd9/download

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.

Financial News for the Week of July 24, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A tug of war between encouraging vaccine news and hopes of new economic stimulus, and early indications that the recovery might be stalling, is fueling financial market volatility.

- Jobless claims rose to 1.42 million last week after declining for 15 consecutive weeks, suggesting that the labor market recovery might be weakening. By contrast, the housing sector continues to impress as existing home sales soar by 20.7%.

- Congress returned to work and is crafting the next installment of aid to household and businesses. Divergences remain, but an agreement is expected over the next few weeks. Likewise, the Fed is set to deliberate on the next steps of its policy response at its scheduled meeting next week

Recovery Risks Stalling Out as Pandemic Worsens

The pandemic marked another gloomy milestone in the U.S. as confirmed coronavirus cases breached the four million mark. This represents a sharp acceleration from just two weeks ago when cases topped three million (Chart 1). From a regional standpoint, California has now surpassed New York for the highest number of cases at over 430,000. With cases continuing to soar in several states, reopening plans are increasingly being rolled back and restrictive measures reintroduced to curb the spread. In one of the latest developments, bars that do not serve food are no longer permitted to offer indoor seating in Chicago, while parties are now limited to six people at restaurants.

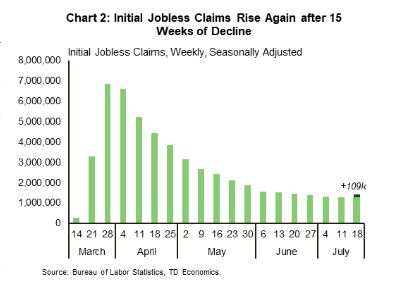

The surge in infections is weighing on economic activity, and this is starting to come through in high-frequency indicators. Initial jobless claims, which had declined for fifteen straight weeks, rose for the week ended on July 18, 2020 (Chart 2). Indeed, filings for unemployment insurance increased by 109,000 to 1.42 million last week, up from 1.31 million in the week prior. While the latest reading is still far below the late-March peak when weekly filings topped 6.9 million, it suggests that the recovery may be losing steam. The historical relationship between claims and employment suggests that employment growth will slow in July relative to the strong gains seen in June and May. This view was also echoed in the Census Bureau’s Household Pulse Survey, which points to increased job losses in July.

With risks increasingly tilted to the downside, policymakers are working on the next set of measures to help support the economy. Across the Atlantic, hard-fought negotiations between EU leaders finally came through earlier in the week in the form of a €1.8 trillion stimulus package. Closer to home, Congress returned to work this week and is crafting the next installment of aid to households and businesses. While divergences over the scope and the size of the next package remain, an agreement is expected over the next few weeks. Likewise, the Fed is set to deliberate on the next steps of its policy response at its scheduled meeting next week. Here’s hoping that the next array of policy responses is enough to keep the recovery on track.

Johary Razafindratsita, Economist | 416-430-7126

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of July 17, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Despite the continued surge in new infections in the U.S., financial markets were on the upswing this week on positive economic data and encouraging news on a vaccine.

- Internationally, the Chinese economy resumed growing in the second quarter. However, the recovery in the second quarter was uneven, with consumers reluctant to spend.

- In the U.S., retail sales and housing starts both rebounded sharply in June. Consumer price pressures in previously weak areas also perked up.

Economic Rebound Continued Through June

The big news internationally was that the Chinese economy resumed growing in the second quarter. After a 6.8% year/year decline in the first quarter, real GDP increased by 3.2% versus a year ago. However, the recovery in the second quarter was uneven, with investment outpacing consumption. Consumers have been reluctant to spend even though most businesses have reopened, reflecting the intensity of the demand shock and consumer scarring, which may take time to heal.

American consumers, on the other hand, continued to ramp up spending at retailers in June (+7.5% month-on-month). May’s gain was also revised upward, and total sales are now only 0.6% below February’s level. The rebound in sales has been uneven across categories, but even lagging areas like restaurants and bars and clothing had big double-digit rebounds in June (Chart 1).

However, retail sales only accounts for about 43% of consumer spending. Many services, like housing and medical care are not captured. This includes some of the hardest-hit areas: air travel, hotels, car rentals, child care, haircuts, movies and live entertainment. So, consumers have more money to spend on retail items because they can’t spend on these other areas. It also means the rebound in total consumer spending is likely to lag the retail front.

Turning to the housing market, starts jumped 17.3% in June (Chart 2). Momentum in single-family home construction looks to continue in July, with building permits up. Not surprisingly, multifamily permits fell. These projects typically involve greater risk, and given social distancing, are likely less desirable in the current climate. While starts are 24% below February levels, those were boosted by unseasonably warm weather, and are only down 3.4% versus a year ago.

Consumer prices rose again in June for the first time since the pandemic hit. A 0.2% m/m increase in core CPI in June provided some reassurance that earlier deflationary forces have ebbed. However, some of the more persistent categories, like shelter, continued to cool in June. With shutdowns returning across many parts of the country, prices may see renewed downward pressure. All told, we expect inflation to remain muted over the next couple of years.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

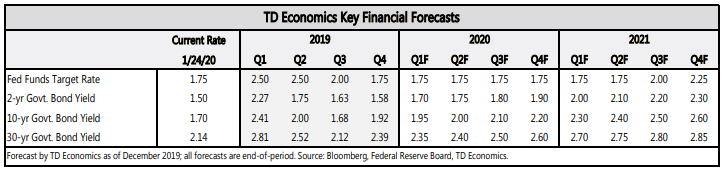

Financial News for the Week of January 24, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets were focused on the progress of the new coronavirus in China, with few economic headlines in the U.S.. It is still early days, but it is likely the important efforts to contain the disease will crimp economic growth in China.

- Existing home sales more than recouped November’s decline in December. Unseasonably warm weather likely was a factor, but it sets up strong momentum in residential investment heading into 2020.

- Next week features the Fed meeting and our first peek at fourth quarter economic growth. The Fed is likely to leave rates on hold as it assesses the potential upside from the trade deal with China. A solid headline of around 2% growth is likely to mask softer domestic details.

All Quiet Ahead of the Fed

The European Central Bank left its low policy rates unchanged this week. Activity in the Euro Area appears to be stabilizing, albeit at a lower level. Christine Lagarde, the new ECB President, also set out the framework for the ECB’s first strategic review in 16 years. It will reconsider the inflation target and the tools used to achieve it. Notably it will also examine how other considerations, like climate change and environmental sustainability can be relevant to the ECB’s mandate.

Existing home sales jumped up 4% in December, more than recovering from the 1.7% decline in November. Activity was likely boosted by unseasonable warm weather in December, so we will likely see some softness in the months ahead. Overall, however, the story of 2019 was a resurgence in housing in the second half of the year (Chart 1). The main reason was rising affordability due to lower mortgage rates and accelerating income.

In fact, home sales could have been even higher if not for constrained housing supply, which is driving up prices. All in, as we outlined in our recent report, we expect existing home sales to continue to improve, but at a more subdued pace this year.

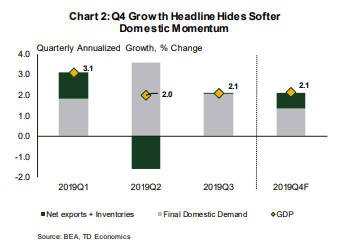

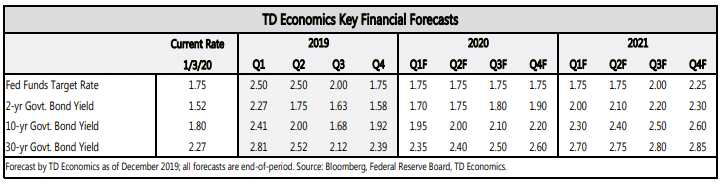

Fourth quarter economic growth is forecast to post a respectable 2.1% annualized gain on the surface. However, the details are likely to show the U.S. economy ended 2019 on a soft note. Consumer spending is tracking below 2%, and business investment is looking flat to slightly negative. Residential investment is one area expected to be quite bright, but it is relatively small. A large drop in imports is the main factor keeping growth above 2%, but that is not a positive sign for demand (Chart 2). Trade is often a trickier component to predict, so there is a bit more uncertainty than usual on the quarter’s forecast. Domestic demand should look a bit better in Q1, but overall our latest forecast calls for relatively modest growth in 2020 of around 2 percent.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

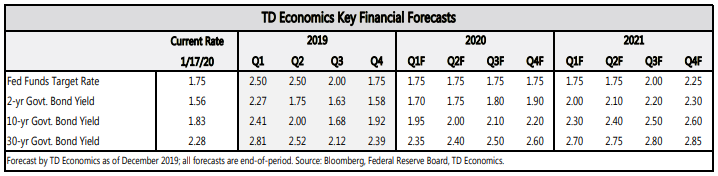

Financial News for the Week of January 17, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Data releases over the week reinforce the main themes in the U.S. economy: solid consumption, housing market recovery, faltering business investment and soft inflation.

- The phase one trade deal was formally signed, committing China to increase its imports of U.S. goods and services to $200 billion more than the 2017 level. Reaching this target will be a difficult task

- While the agreement gives short-term relief, this is only the first phase. The likely difficulty in implementing the current accord combined with the more-difficult issues still to be discussed, mean that trade uncertainty is likely to continue to be a factor in the outlook.

Phase One Complete, But Can It Hold?

From a data perspective, 2019 ended with more of the same for the U.S. economy. Consumption likely remained solid in the fourth quarter, as evidenced by the healthy rise in retail sales in December. Retail sales advanced by 0.3% month-on-month, and November’s figure was also revised higher. There were gains in nearly every category, underlining the robust nature of the increase.

The housing market also continued its good run, with housing starts surging last month. Construction in both singles and multifamily units picked up in December, sending the overall level to its highest point in 13 years (Chart 1). Taking together, housing data for the fourth quarter implies that residential investment is on track to continue its upward climb heading into 2020.

On the flipside, we saw the NFIB’s small business optimism index move in the other direction in December. The decline is likely attributable to heightened policy uncertainty, a theme that has plagued businesses, big and small, throughout 2019 (see report).

Despite the increasing pressure on economic capacity, inflation remains stubbornly soft. December’s core consumer price index, which strips out the impact of energy and food prices, remained at 2.3% year-over-year, unchanged since October. On an annual basis, core CPI inflation was only a tick higher in 2019 at 2.2%. Looking ahead, price pressures may continue to be subdued especially with the U.S.-China phase one trade deal effectively cutting the existing tariff rate, while also removing the threat of additional tariffs at least for the time being.

This takes us to the big headline for the week, the U.S.-China phase one trade deal. On the face of it, the agreement could be a positive for U.S. growth as it commits China to purchasing an additional $200 billion worth of U.S. goods and services over the next two years (see commentary). But the big question is: can China adequately ramp up its imports to reach this target? The answer is probably not. Quarterly import growth would have to average above 10% for every quarter from now until the fourth quarter of 2021 to reach this goal (Chart 2).

The agreement also included a dispute mechanism. In the event China doesn’t meet its import commitments, the U.S. can resort back to imposing tariffs and if China responds, the deal would be nullified. Indeed, the agreement gives short-term relief, but its sustainability is still an open question.

Sri Thanabalasingam, Economist | 416-413-3117

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 10, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The U.S. economy continued to churn out jobs at a solid pace. Non-farm employment grew by 1.6% over 2019, marking only a slight deceleration from the 1.7% recorded in 2018.

- The services side of the economy also continued to fare better than its manufacturing counterpart. The ISM Non-Manufacturing Index edged 1.1 points higher, to its highest level in seven months.

- The U.S. trade deficit dipped to its lowest level in three years as tariffs, among other factors, shifted trade flows.

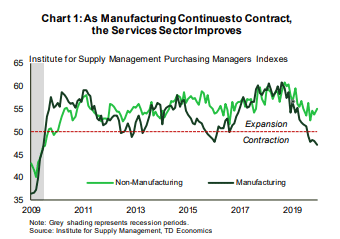

Services Keep the Economic Engine Humming Along

Despite the overall positive tenor of the report, there are warning signs on the horizon as the U.S. population in 2019 grew at the slowest pace in about a century. Though the economic impact of this development may be slow to materialize, it does have implications for the availability of workers, taxpayers and consumers to fuel future growth.

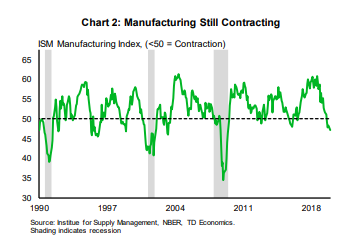

The employment numbers suggest that U.S. service sector activity has been resilient. This was echoed in sentiment, where the Institute for Supply Management’s Non-Manufacturing Index diverged from its manufacturing counterpart in December. The index edged 1.1 points higher to 55.0 – its highest level in seven months. Healthy consumer fundamentals and less exposure to trade tensions helped the services sector, which accounts for a larger proportion of the U.S. economy, remain in expansionary territory throughout 2019. This is in contrast to the manufacturing sector, where activity has been contracting for the past five months and in December slumped to its lowest level since June 2009 (Chart 1).

On the trade front, U.S. tariffs contributed to a slide in imports (down 1% month-on-month) in November while exports picked up (up 0.7% m/m), pushing the trade deficit to its lowest level since October 2016 (Chart 2). The goods and services deficit decreased by 8.2% to $43.1bn in November, down from $46.9bn in the previous month. Of note, the country’s merchandise trade deficit with China fell for a fourth consecutive month reflecting tensions between the two countries. A preliminary trade deal however, expected to be signed next week, should bring improvements in bilateral trade relations. Despite this, the impact of potential tariffs on goods from other trading partners such as the EU and Latin America cannot be discounted, and may result in further data distortions in the months ahead.

Overall, the U.S. economy has managed to exit a tumultuous 2019 relatively better-off than most other advanced economies. While U.S. growth is expected to slow in 2020 as detailed in our latest forecast, it will still lead the G7 pack, notwithstanding continued trade policy uncertainty.

Shernette McLeod, Economist | 416-415-0413

Financial News- January 10, 2020

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

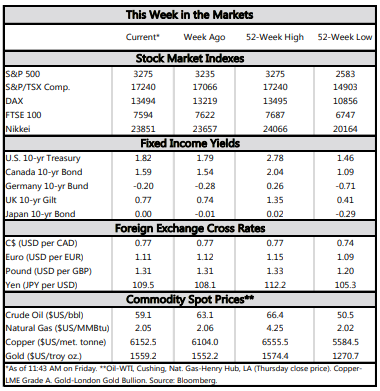

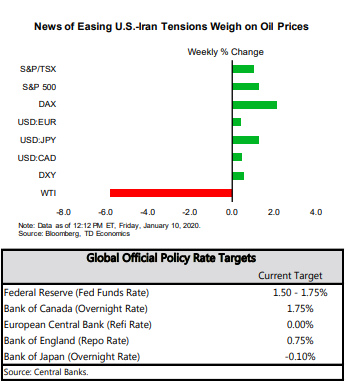

Financial News for the Week of January 3, 2020

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- It was a relatively light week on economic data. The merchandise trade deficit narrowed in November, suggesting some upside risk to real GDP growth in the fourth quarter. Still, activity in the manufacturing sector continues to come in on the weak side, with the ISM index falling again in December to its lowest level since 2009.

- The phase one trade deal between China and the U.S. looks to be signed later this month. Details are still scant and time lines around commitments uncertain.

- News that a U.S. airstrike in Iraq had killed a top Iranian military leader caused oil prices to spike, global stock markets to sell off and bonds to rally on Friday.

A Risk-Filled Start to the Year

Alas, this optimism did not last long. Markets were roiled on Friday by news that a U.S. airstrike in Iraq had killed Qassim Suleimani, a top Iranian military leader. Fears of retaliation and further escalation caused oil prices to spike, global stock markets to sell off and bonds to rally, with the 10-year yield falling seven basis points to 1.81% as of writing.

Outside of the torrid developments in the Middle East, the U.S. and China appear to be moving forward on signing ‘phase one’ of their trade deal. Earlier in the week, President Trump announced that he would sign the deal on January 15th. Details of the final deal are expected in the next several days. Early indications are that the text of the deal could remain vague on the exact amount and timing of China’s commitments to purchase additional agricultural and other U.S. goods for fears that specific details could distort markets.

Elsewhere on the economic front, global manufacturing activity continued to struggle through the end of last year. In the U.S., the ISM manufacturing index fell to 47.2 in December from 48.1 in November. The decline was contrary to the median economist forecast for an increase in the index. The ISM index has now been in contractionary territory for five consecutive months and at its lowest point since the recession in 2009. Manufacturing sectors remain weak the world over. The Markit PMI index in Germany edged lower in December as well. While still above its trough, it remains in contractionary territory where it has been through all of 2019.

The data flow will pick up next week with the release of the ISM non-manufacturing index and December employment data. So far, the troubles in the manufacturing sector have remained contained therein while broader services expansion has remained unharmed and, importantly, has provided enough support to the job market to support ongoing consumer spending. We will be watching for any developments on this front in the jobs data next week, as well as the impact of new (and old) geopolitical flare ups.

James Marple, Senior Economist | 416-982-2557

Financial News- January 3, 2020

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.