Financial News for the Week of July 19, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

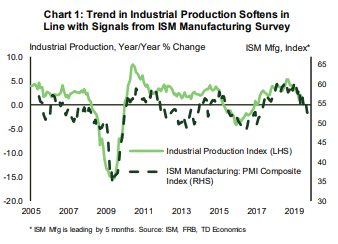

- Chinese economic growth slowed 6.2% y/y in the second quarter of this year, as rising trade tensions weighed on activity. Signs of wear are also showing in the U.S., where industrial output continued to grow at a slow pace in June.

- U.S. housing data remains soft. Starts eased in June, while permits dropped precipitously (-6.1% m/m), pointing to more weakness in the pipeline. That said, the services side of the economy continues to hold up well, with consumption providing a major helping hand. Retail sales rose by 0.4% in June, extending the winning streak to four straight months.

- The resilience of the American consumer suggests less urgency for the Fed to cut rates later this month. But, Fed speakers pushed back against that notion this week, emphasizing the need to get ahead of any potential weakness.

Resilient Consumer Unlikely To Change Fed’s Mind

The trade blows are inflicting wounds on both sides. Figures out this week showed that Chinese economic growth slowed to 6.2% year-on-year – the slowest pace in 27 years, with output in secondary industries (construction and manufacturing) decelerating to 5.6% from 6.1% in the first quarter. In the U.S., industrial output continued to grow at a slow pace in June, in line with signals from the ISM manufacturing survey (Chart 1). The impact of the trade conflict is not confined to manufacturing. An annual NAR survey showed that Chinese home purchases in the U.S. fell by 56% in the 12-months ending in March.

Housing data, on the other hand, remains soft. Starts edged lower in June (-0.9%) and have generally moved sideways in recent months. Building permits, however, fell precipitously on the month (-6.1% m/m), suggesting some weakness is still in the pipeline. Despite a favorable demand backdrop and relatively low and falling interest rates, new construction is struggling to kick into higher gear. A lack of buildable lots, labor shortages and increased production costs remain key hurdles.

Looking past housing challenges, the resilience of the American consumer suggests less urgency for the Fed to cut rates later this month. However, several Fed speakers pushed back against that notion this week, emphasizing the need to get ahead of any potential weakness. Still, should the data continue to hold up, the case for limited stimulus (i.e. only 1-2 cuts) is likely to prevail.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of July 12, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- In a busy week for Fed communication, Chair Powell gave his semiannual testimony to Congress where he confirmed

that crosscurrents hitting the outlook would likely require some additional accommodation. - The Fed Chair also noted that he doesn’t see the labor market as particularly hot and, with wage growth subdued, has

more room to run. - Powell also noted the risk that weak inflation could prove more persistent than anticipated. That risk diminished somewhat with the June CPI report, which showed core inflation firming across both goods and services.

Markets Celebrate The U.S.-China Trade Truce

The key takeaway from Powell’s prepared remarks was that the Fed Chair still sees crosscurrents and uncertainty as weighing on the outlook. Given that this was the key factor behind the FOMC’s increased willingness to provide additional accommodation, this was as clear a signal as any that a July rate cut is happening. Nailing the coffin closed, when the Chair was asked if the strong June jobs report had done anything to change his mind, he replied, “a straight answer...is no.”

Between now and the July 31st meeting there are data on retail sales, housing starts, home sales, durable goods orders, and a few others. Even relatively positive outcomes on all these reports are unlikely to move the Fed off that 25-basis point cut. They could, however, go a long way to moving market pricing for additional cuts (almost three by the end of this year). In the meantime, Fed speakers have one more week to communicate their take on economic data before the quiet period preceding the July meeting.

The other message in the Fed’s accompanying Monetary Policy Report as well as Powell’s Q&A sessions was the recognition that inflation is weak, and the labor market may still have some room to grow – even with an unemployment rate at 3.7%. Perhaps the most interesting response Powell gave over the two days of testimony was to a question about the possibility that lower interest rates would cause the labor market to run hot. His response was: “you know, I guess I would start by saying we don’t have any basis for calling this a hot labor market.”

Nonetheless, sometimes the data zigs just when everyone expects it to zag. While the Fed Chair cited the risk that weak inflation would prove more persistent than anticipated, the CPI out this week showed prices rising firmly in June. Core CPI (excluding food and energy) rose 0.3% on the month – the strongest gain since January 2018. Price growth firmed for both core goods and services (Chart 2). Still, with the year-on-year headline rate at just 1.7% and core at 2.2%, the firetrucks can stay parked for now.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

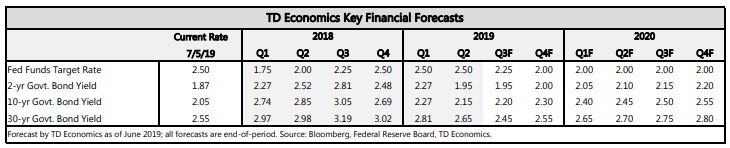

Financial News for the Week of July 5, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

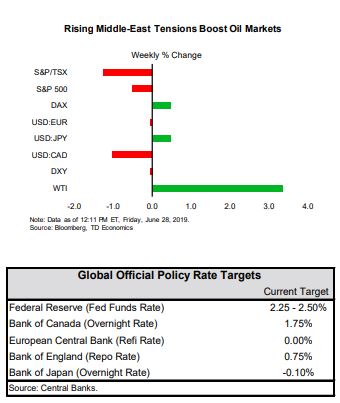

- News of a trade truce between the U.S. and China buoyed equity markets at the start of the week. The ceasefire put additional tariffs on hold, and there were some modest concessions on both sides.

- On the economic front, messages were decidedly mixed this week. The ISM manufacturing and non-manufacturing indexes moved lower in June, while the payroll report showed a reacceleration in hiring with 224k jobs created last month.

- Given the balance of risks, there is still a solid case for a 25- basis point “insurance” cut when the Fed meets later this month. But, insurance is likely to mean one or two rate cuts this year and not four or five as markets are pricing.

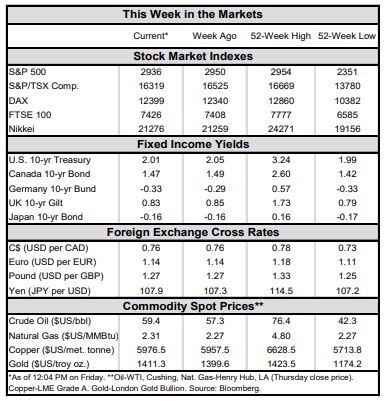

Markets Celebrate The U.S.-China Trade Truce

On the economic front, messages in this week’s data releases were decidedly mixed. The ISM manufacturing and non-manufacturing indexes moved lower in June and are significantly below year-ago levels. Still, both remain in expansionary territory, implying slower, but not negative economic growth (Chart 1). More concerning is that the greatest weakness was in the forward-looking indicators. The new orders subcomponent narrowly avoided contraction in June, while pending orders have already slipped below the 50-point threshold.

It is not surprising that activity is slowing from its 3%-plus, stimulus-fueled pace of a year ago, but it makes reading the economic tea leaves more difficult. It is hard to know in real time if the economy is returning to a healthy trend-like pace or pushing past it into a slump. Tariffs and trade uncertainty further cloud the mix, and signs globally point to a less benign slowdown.

The best evidence that the American economy is headed for a soft landing is the continued resilience in the labor market. That had been brought into question with the May payroll report (job growth slowed to just 72k), but doubts were assuaged with this week’s report showing a reacceleration to 224k in June. The only fly in the ointment was that there were no signs of faster wage growth. Instead average hourly wage growth remained unchanged at 3.1% for the third consecutive month.

Given the balance of risks, there is still a solid case for a 25- basis point “insurance” cut when the Fed meets later this month. But, as long as signs point to continued, albeit slower, economic growth, insurance is likely to mean one or two rate cuts and not four or five as financial markets are currently pricing. Fed speeches over the next two weeks will be key in communicating this to the public and financial market participants.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

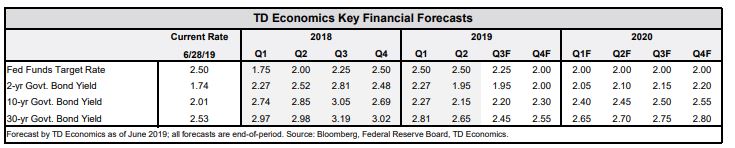

Financial News for the Week of June 28, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A light week on economic data was filled with Fed speeches and a trickle of news flow on the upcoming meeting between Presidents Trump and Xi. We do not expect to see a major breakthrough this weekend, but rather an agreement to continue talking (forestalling at least for now the threat of additional tariffs).

- Chair Powell reiterated comments in his press conference last week that crosscurrents to the economic outlook had arisen relatively swiftly over the past month, leading the Fed to shift toward an increased willingness to cut rates.

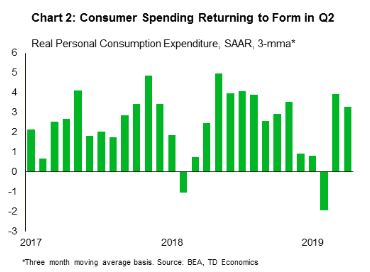

- Economic data was mixed, with home sales and confidence falling, but consumer spending rising. With revisions, second quarter personal consumption is likely to top 3% annualized, enough to push economic growth to the 2% mark.

Presidents Xi and Trump Meet As Crosscurrents Blow

Following the FOMC meeting last week, Fed speakers were out in full force explaining and defending the committee’s shift from patience to willingness to do more. Most notably, Chairman Powell reiterated that significant crosscurrents had hit the U.S. outlook in the period between the FOMC’s May and June decision. Among these, deteriorating business sentiment and slowing global growth rang the loudest.

Powell did not mention it explicitly, but the breakdown in trade negotiations between China and the U.S. was a key driver of the change in tack. That puts the focus squarely on the leaders of the two countries as they meet in Japan this weekend. Prior to the meeting, optimism that the two sides were getting close to a deal were stoked by Treasury Secretary, Steve Mnuchin, who said they were 90% of the way there. But, just as soon as he said this, doubt was cast by President Trump’s own interview that dangled the possibility of additional tariffs. At the same time, reports that China would come to the meeting with preconditions of its own, including the removal of all existing tariffs and restrictions imposed on Huawei, reined in optimism that a significant breakthrough is imminent. All in all, we expect little to come out of the meeting except an agreement to keep on talking.

On the bright side, consumer spending is still holding up. Real personal consumption rose by 0.2% in May, and was revised up to 0.2% growth in April from a previously flat reading. With two of three months of the second quarter now recorded, spending growth looks to advance by well over 3% (annualized - Chart 2). Even with some weakness in investment and trade, second quarter economic growth appears likely to come in near the 2% mark.

Evidence that economic growth is holding up suggests that even as the Fed considers insurance cuts, it need not have to bring out the bazooka. While a 25-basis point cut in July seems increasingly likely, the Fed should be able to afford to save at least some of its bullets and refrain from a larger 50-basis point cut, as futures markets have begun to price. Still, we would hold off betting the farm on it until after next week’s June payroll report.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 21, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The biggest event this week was the Fed’s pivot away from patience. It is now poised to act in the event of a further deterioration in the outlook. This cheered markets, with stocks and bonds rallying.

- The Fed’s dot plot also showed that the majority of FOMC members judge the funds rate to already be at its long-run neutral level, and expect to lower rates next year.This is a seismic shift from expecting hikes back in December.

- Our new forecast released this week, calls for the Fed to cut rates twice this year, as insurance against the downside risks that have accumulated due to trade tensions, and a late-cycle economic slowdown.

The Powell Pivot

At the same time, the Fed’s expectations for economic growth have shifted a lot less. The median FOMC forecast for growth is 2.1% this year and 2.0% next year, down only slightly from 2.3% and 2.0% back in December. Looking only at growth expectations it is hard to justify the pivot in interest rates. However, the updated growth forecasts incorporate a lower path of interest rates. Previously, the FOMC believed the economy would grow at that pace as it continued to raise rates. Now it expects that a cut will be required to sustain that near-trend pace.

A big part of the pivot is the continued miss on its inflation forecast. In December, the FOMC expected inflation to be back at 2% by the end of this year, and now that isn’t looking too likely. Given the difficulty sustaining the 2% inflation target, it has lowered its estimate of the “neutral” rate to 2.5%. That is the level at which the rate neither stimulates, nor stifles economic growth. Clearly the Fed has come around to the view that rates over the past little while have been less stimulative than they previously believed.

A majority of FOMC members now believe that at least one rate cut will be required to keep inflation at target and promote maximum employment, and seven out of 17 members judge that it will need two quarter-point rate cuts.

Our recent forecast (Chart 2) lowered our fed funds rate call for this year, adding in two insurance cuts (see report). We expect cuts are needed to keep growth on track, as persistent trade uncertainty weighs on business sentiment and investment. The upside to rate cuts is that they should provide a bit of fuel for the housing market, which has been largely moving sideways over the past year. Housing data for May showed that while construction activity remains lackluster, the resale market increased 2.5% on the month. That suggests the drop in mortgage rates over the past six months may finally be lifting activity. And a more modest path for rates ahead will help improve affordability.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 14, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A potential trade war between U.S. and Mexico was averted, but global trade uncertainty remains.

- Despite markets pricing in rate cuts, domestic indicators suggest that the U.S. economy is on decent footing. Inflation remains stubbornly low, however.

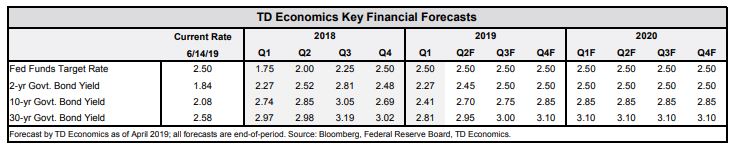

- The Fed rate decision next week is clouded by conflicting signals, but we believe it will likely feature an easing bias.

Conflicting Signals Cloud Fed Rate Decision

This week was a perfect example of the conflicting signals faced by the economy. We began the week with a quick extinguishing of a possible trade war with Mexico, but trade uncertainty still looms large. Indeed, the trade conflict between the U.S. and China is not subsiding. Earlier this week, President Trump warned that if President Xi did not meet with him at the upcoming G20 summit, he would immediately slap 25% tariffs on the remaining un-tariffed $300 billion of Chinese imports.

Markets are pricing in the risks emanating from the trade conflicts, resulting in a continued inversion of the yield curve (3-month to 10-year), and an expectation of at least two Fed rate cuts by the end of the year.

However, trade uncertainty does not yet seem to be weighing on business optimism. The NFIB small businesses optimism index improved for the fourth consecutive month as businesses anticipated an improvement in economic conditions and more capital expenditure in months to come.

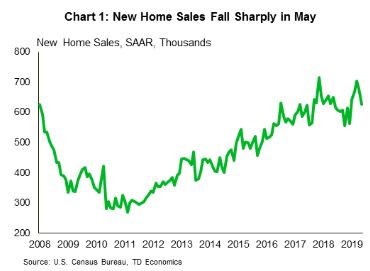

Moreover, U.S. consumers displayed their strength again, with solid retail sales growth in May alongside a significant upward revision to April data (Chart 1). Consumption growth may now exceed the 3% (annualized) mark in Q2.

The Fed will no doubt take notice of the weakness in inflation in the FOMC meeting next week. But they will also have to consider all other developments as well. Despite rising downside risks, the domestic economy appears to be chugging along. All told, we expect the Fed to convey an easing bias, but not move on rates at next week’s meeting.

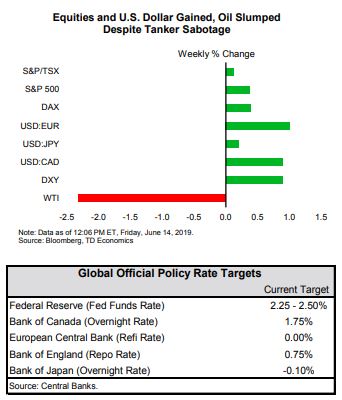

We also saw a rise in global political risks rise this week as two oil tankers were attacked in the Gulf of Oman. After falling through much of the week on the back of concerns about global growth, Brent oil prices jumped by around 5% on Thursday (with a similar move in the WTI contract), not quite enough to offset losses earlier in the week (Chart 2). With the relationship between the U.S. and Iran increasingly strained, oil markets may get caught in the middle.

Sri Thanabalasingam, Economist | 416-413-3117

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 7, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Trade tensions continued to dominate economic headlines, with U.S.-Mexico taking center stage. It remains unclear if a deal can be reached by Monday. The US-China spat also resurfaced, with signs that it is spreading beyond goods trade.

- Fed Chair Powell noted that the Fed was monitoring trade developments closely, and was ready to “act as appropriate to sustain the expansion”. This appeared to soothe equity markets, which rebounded to a three-week high.

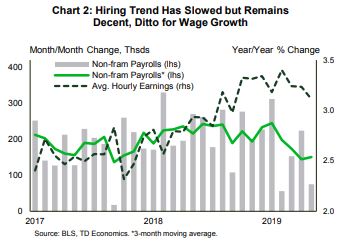

- The May jobs report disappointed expectations, with payrolls up only 75k. Looking through the recent volatility, the hiring trend has slowed but remains decent, averaging 151k in the last three months. The unemployment rate held steady at 3.6% and wage growth, while slowing a touch, held above 3% y/y.

Tariff Threats Muddy the Economic Waters

Trade tensions continued to dominate economic headlines this week, with the U.S.-Mexico quarrel taking center stage. Mexico sent a senior delegation to D.C. to try to address President Trump’s concerns regarding illegal migration, and to defuse the impending tariff threat. While some progress has been made, as at the time of writing, it is unclear if a deal can be reached by Monday’s deadline.

The uncertainty generated by these events has kept the Fed on high alert. Among several Fed speeches this week, Fed Chair Powell noted that the Fed was monitoring trade developments closely, and was ready to “act as appropriate to sustain the expansion.” Chair Powell’s emphasis on the Fed’s flexibility appeared to soothe equity markets, which rebounded to a three-week high.

With the broad economic backdrop still decent, trade and global growth remain the ultimate wildcard. Mexico is the second biggest source of goods entering the U.S. after China. As such, the impending 5% tariff will be problematic, particularly for products that cross the border multiple times (i.e. auto parts). Prospects for an increase in the tariff rate to 25% are more daunting, with supply chain disruptions, reduced market access and the hit to confidence all more acute. A simultaneous escalation in tensions with Mexico and China would accentuate these risks further. In the event that tensions escalate in this fashion, the Fed will have little choice but to act.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 31, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S.-China trade tensions continued to dominate headlines as both countries dig in for another round of negotiations under more strained circumstances. U.S. tariffs against Mexico appear to also be in the works.

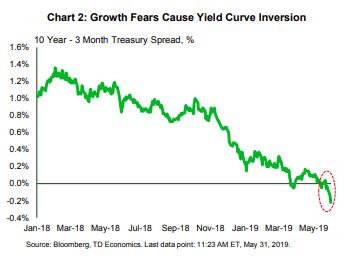

- As trade tensions flare, investors have run for cover, driving up bond prices and sending the yield curve into inversion territory.

- U.S. Q1 growth was revised marginally lower (3.1% vs. 3.2%), and Q2 is projected to be lower still (below 2%). Inflation however managed to edge marginally higher with core PCE at 1.6% year-on-year in April.

Trade Tensions Still in the Spotlight

In other trade news, just as the U.S. and Mexico took steps this week to ratify the USMCA, President Trump threatened to impose a 5% tariff on all Mexican imports starting July 10th. The President wants Mexico to do more to deter illegal migration from Central America. These tariffs, alongside prolonged Chinese negotiations, complicate trade relations even further. The heightened bout of uncertainty is likely to dent already shaky business confidence.

China has responded to U.S. rhetoric with both direct and indirect threats. The country suggested that they too may influence global supply chains through their dominance of “rare earth” exports – a group of 17 minerals used in the production of most modern electronic devices. A ban on exports to the U.S. could disrupt production and affect prices of many products ranging from smartphones to satellites. There are also indications that China may have once again halted purchases of U.S. soybeans after previously resuming purchases as a sign of goodwill during negotiations.

Meanwhile, on the domestic data front, home price appreciation continues to moderate. Data for March showed that home prices grew 3.7% year-on-year, lower than the 3.9% recorded in February (Chart 1). Price growth has been decelerating since April last year, suggesting that even with lower mortgage rates and rising wages, past price growth may have stretched affordability for many potential buyers.

With concerns of lower growth and heightened trade tensions, investors pushed the yield on 10-yr Treasury notes to the lowest close since September 2017 this week. This caused the yield curve to invert as it dipped below the three-month note (Chart 2). While inversions tend to precede recessions, the phenomenon would need to be sustained and observed among other maturities before the indicator signals an imminent risk and materially affect decisions at the Fed. All said, the reignited trade tensions have skewed the risks to both U.S. and global growth further to the downside – a development which will no doubt receive close monitoring by central bank officials.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 24, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Pessimism dominated markets this week, as negative headlines about U.S.-China trade relations continued.

- UK PM Theresa May announced her resignation after repeated attempts to get her negotiated Brexit deal through parliament failed.The pound fell this week as markets worry about a no deal Brexit on Oct. 31st.

- Indicators from the U.S. factory sector continue to point to a weakening trend in the face of softer foreign demand and sentiment.

Trade Woes Weigh on Markets

To top it all off the Brexit saga came back to the fore, as Prime Minister Theresa May announced her resignation. May had been unable to get her negotiated Brexit deal through parliament. The way forward on Brexit remains unclear, and the new Conservative leader, who should be selected by the end of July, will not have a lot of time to chart a new course before the Oct 31st deadline for Britain to leave the EU. In the meantime, the cloud of uncertainty continues to hang over the UK economy, and the increased probability of a no-deal Brexit has weighed heavily on the pound over the past week.

The sour news continued with the April durable goods orders report, which showed total orders fell 2.1% in April. Nondefense capital goods orders ex-aircraft – a closely watched gauge of business capital spending – was also down in April (-0.9%). Durable goods orders are quite volatile month-to-month, but on a trend basis (the six month moving average) orders have gone sideways at best since late 2018 (Chart 1). This is consistent with the theme discussed in last week’s Bottom Line, that cracks continue to appear in the US manufacturing sector: foreign demand has cooled, and uncertainty on the trade front weighs on business sentiment and willingness to spend on new equipment.

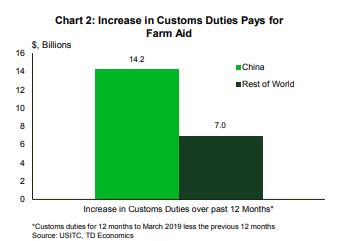

The President has recognized the impact trade conflicts are having on at least one sector of the economy. He formally announced a $16 billion aid package for farmers hurt by Chinese retaliatory tariffs on key agricultural exports from the U.S. This amount is slightly larger than last year’s aid package (around $12 billion). The combined cost of these packages more than outweighs the increase in customs duties the U.S. has collected since the Administration started ratcheting up import tariffs early in 2018 (Chart 2), erasing any fiscal benefits of the tariffs.

Amidst the headlines on ongoing trade tensions between the world’s largest economies, the minutes from the most recent FOMC meeting already seemed a bit stale. These deliberations occurred before the latest increase in the tariff rate on certain Chinese imports. The minutes showed the FOMC’s commitment to patient monetary policy, and a significant discussion on whether the recent softness in inflation is transitory, or a more persistent trend. The Committee is clearly divided on that topic, and a couple more months of data is likely to settle the debate. Inflation aside, given a building cloud of global economic uncertainty, a prolonged pause on rates seems a wise course of action.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 17, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Equity markets rebounded this week as the U.S. administration delayed its decision on auto tariffs for six months.

- Housing starts and retail sales data for April support the narrative of healthy domestic spending this quarter.

- That said, externally oriented industries appear to be getting caught in the downdraft of weak foreign demand.Formerly resilient, U.S. manufacturing activity has softened this year, in line with global developments.

Domestic Resilience, But Weakness Abroad Taking a Toll

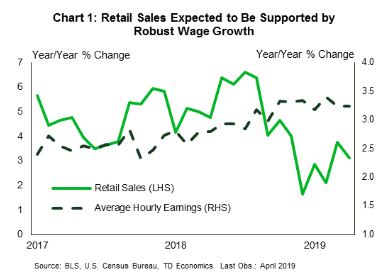

Unease about U.S. economic performance is building for good reason. Economic growth is set to moderate this year after a blowout, stimulus-fueled 2018. Foreign demand remains weaker than last year, while geopolitical risks and trade policy uncertainty appear to be on the rise. Moreover, high frequency indicators are beginning to diverge. Domestic demand remains resilient, but externally oriented industries are combatting stronger headwinds.

Data for retail sales and housing starts for April support the view that the domestic economy remains healthy. Although retail sales pulled back in

Housing starts, on the other hand, surprised to the upside. After December’s dip, housing starts appear to have regained stronger footing, but activity has been choppy through April. Home builder sentiment is improving as well, reaching a 7-month high in May. Moderating home price growth, combined with lower mortgage rates, rising wage growth, and decades-low vacancy rates should support more homebuilding in the months to come.

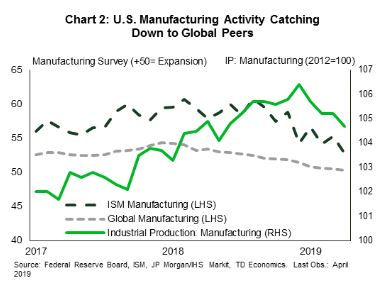

All told, the data this week remains consistent with our forecast for the U.S. economy to expand at a 2% annualized pace this quarter, largely on the back of a more confident consumer. That said, signs continue to build that this may be as good as things get for the rest of this year. Cracks are beginning to appear in what was previously a very resilient manufacturing sector. Industrial production contracted 0.5% in April, the third contraction monthly contraction this year. This mirrors the declining pace of output reported in the ISM manufacturing survey (Chart 2). Softer auto sales are partly to blame, as motor vehicle assemblies have fallen 12.8% since December’s peak.

Although manufacturing is a relatively small share of the U.S. economy (about 11%), its performance is still considered a harbinger of the direction of the U.S. economy largely due to its sensitivity to changes in foreign demand. On that front, there are some signs that the global economy is gradually improving. However, escalating trade and geopolitical risks threaten to derail this nascent recovery.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.