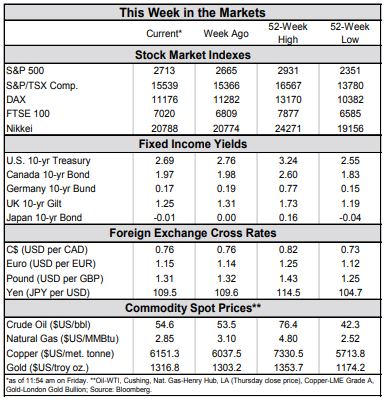

Financial News for the Week of March 1, 2019

HIGHLIGHTS OF THE WEEK

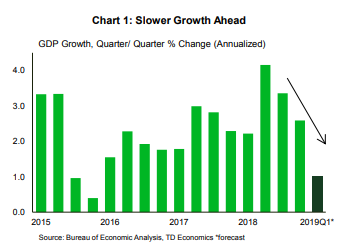

- The U.S. economy grew a robust 2.9% in 2018, the best performance since 2015, but growth moderated at the end of the year and at the start of 2019. The government shutdown and soft consumer spending in December are expected to translate into near 1% growth this quarter.

- Extending the barrage of negative housing data, housing starts plunged by 11.2% (m/m) in December to 1.08 million (annualized).

- Manufacturing data remained soft. The U.S. ISM manufacturing index declined in February, and manufacturing contraction in Europe and Asia broadened further. Soft global activity reinforces the Fed’s patient stance.

Strong 2018 Finish But a Soft Start to 2019

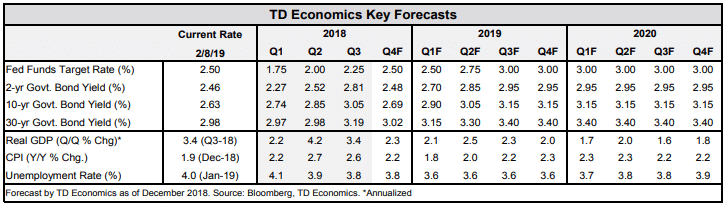

The fourth quarter GDP report painted a picture of solid but moderating growth. For the year as a whole, the economy expanded by a robust 2.9% in 2018. However, the headline conceals the fact that growth moderated as the year progressed, slowing to 2.6% (annualized) in Q4 from the 3.4% and 4.2% pace seen in Q3 and Q2, respectively. Looking at the individual components, consumer spending moderated to 2.8% in Q4 from 3.5% in Q3. Business investment surprised to the upside, with growth accelerating to 6.2% from a 2.5% pace in the previous quarter. However, trade and residential investment were a drag on growth both in Q4 and for the year as a whole.

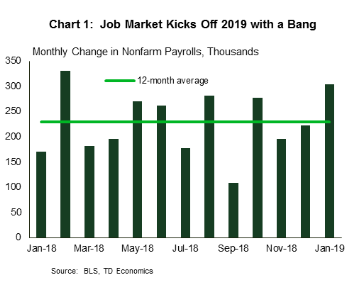

A solid end to 2018, but momentum has clearly waned at the start of this year. Consumer spending data for December confirmed that the weak retail print was not a fluke, as the negative mood led consumers to hold on tight to their wallets. In what’s become a recurring theme, first quarter growth will be bleak. The government shutdown and soft consumer spending translate to growth slowing to 1% in Q1 (Chart 1). However, as in prior years, the slowdown should prove temporary, with output forecast to rebound to an above 2% pace in the second quarter.

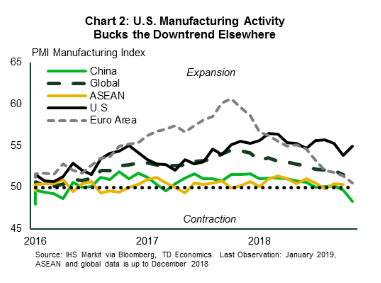

Less hopeful is the underwhelming manufacturing data from this morning that suggests that the global manufacturing rout is not easing. The U.S. ISM manufacturing index declined in February, falling to the lowest level in more than a year, but remaining firmly in expansionary territory. Trade and Brexit uncertainty are a bigger drag on business sentiment in the Euro Area, where a broadening contraction in manufacturing PMIs is underway. Ditto for Japanese, Chinese, and ASEAN manufacturers.

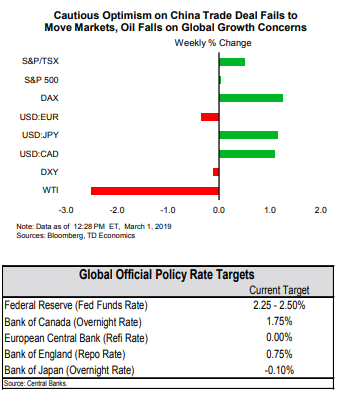

On a positive note, trade tensions with China appear to be easing somewhat. Substantial progress on a trade deal has been made and the scheduled March 1st increase in tariffs on imports from China has been suspended. However, the progress on talks may have come too little too late, and the tariff cloud may continue to cast a shadow on global economy for some time, reinforcing the Fed’s patient stance.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

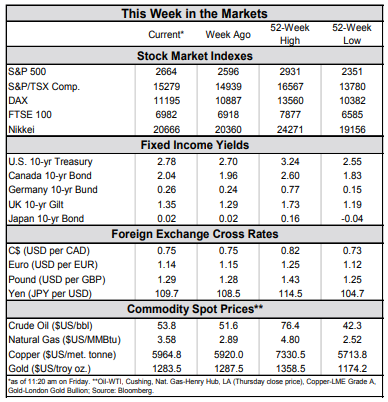

Financial News for the Week of February 22, 2019

HIGHLIGHTS OF THE WEEK

- The barrage of negative U.S. data continued this week, with weakness in December durable goods orders and a decline in existing home sales in January.

- Still, markets were hopeful that progress would be made in the China-U.S. trade talks, which could help remove a cloud of uncertainty that has weighed on investment.

- The data affirms that the Fed made the right choice to shift off of gradual rate increases, and wait patiently to see if the U.S. economy remains resilient in the face of global weakness. We expect these signs to become clearer in the spring.

U.S. - Awaiting Signs of Spring

Overall durable goods orders rose 1.2% in December, but the underlying business-investment gauge – nondefense capital goods orders ex-aircraft – declined 0.7%, the fourth decline since August. Capex spending had already slowed in the third quarter of 2018 after a period of strength (Chart 1), and the durables data suggests a similarly modest pace in Q4. That lines up with our capital expenditure tracker, (based on Fed sentiment surveys) and points to more modest growth into early 2019 as well.

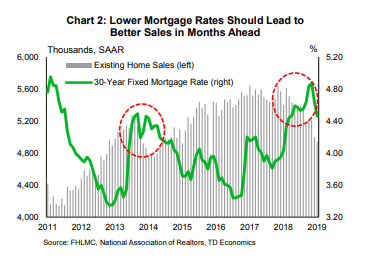

Deteriorating affordability has cut into housing demand over the past year, but mortgage rates have dropped about 60 basis points since late 2018, which should show up in improved sales in the months to come (Chart 2). Homebuilder confidence also improved in February, supporting a more positive housing narrative ahead.

Finally, on the data front, the delayed fourth quarter GDP report is released next week. We expect growth moderated to 2.2% in Q4, after running above 3 ½% through the middle of the year. With the government shutdown and the continued phenomenon of residual seasonality, the first quarter of 2019 is likely to be even weaker at 1.6%. For now, this lackluster data affirms that the Fed made the right choice to shift off of gradual rate increases, and wait patiently to see if the U.S. economy remains resilient in the face of global weakness. The minutes from the January FOMC meeting showed members debating whether further rate hikes will be necessary, but not contemplating cuts. Members continued to view sustained expansion strong labor market conditions, and inflation near 2% as the most likely path ahead. We too expect economic momentum to improve in the spring, and remain modestly above trend through the remainder of 2019. As long as there are no curve balls, the Fed is likely to raise rates once more in the latter half of the year.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

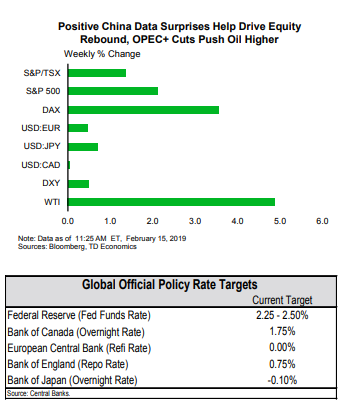

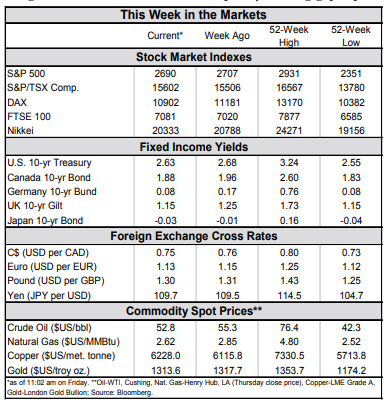

Financial News for the Week of February 15, 2019

HIGHLIGHTS OF THE WEEK

- December retail sales came in significantly weaker than expected, falling 1.2% m/m, with the decline being broad-based. Consumption in Q4 is now tracking around 2.6% annualized – softer than expected, but still a pretty good showing.

- The retail sales report provides a weak handoff to 2019. The fact that the government shutdown extended into January and consumer confidence retreated on the month, further reinforces the notion for a soft print in first-quarter spending and GDP.

- Core inflation remained at 2.2% (y/y) in January, where it has sat for five of the past six months. And there is little indication that it will move in either direction soon. This should provide comfort for the Fed to remain patient.

Wall of Uncertainty

The weak report raised a few eyebrows, with its reliability in question among economics circles. December’s result is hard to square with other industry reports, such the Redbook index, which shows same-store sales accelerating in year-over-year terms in December. The fact that non-store sales (-3.9%) weren’t spared from the pullback also raises some suspicion. This category is largely made up of online sales, where there were no other major signs of stress during holiday season. Still, giving the Commerce Department the benefit of the doubt here, it would appear that the threat and subsequent materialization of the late-year government shutdown, together with a sharp selloff in equity markets amidst elevated trade tensions with China, prompted Americans to keep a tight grip on their wallets.

Similar to last year, however, we don’t expect the first-quarter performance to set the pace for the rest of the year, so long as a resilient labor market shores up spending. Consumption is expected to rebound in the second quarter, provided that there is no major disruption on the trade front or another government shutdown. Progress appeared to have been made on both of these areas this week. Reports indicate that Chinese and U.S. negotiators made headway in agreeing on broad principles, with negotiations to continue next week in Washington. It appears that President Trump will get his border wall funding by declaring a national emergency, and is also expected to sign a bipartisan spending bill that will avoid a second shutdown.

This week’s developments reinforce the notion that the Fed will stay put until muddy waters begin to clear. The other part of the Fed’s calculus, inflation trends, provide added comfort for patience. Core CPI has been holding at just above the Fed’s target recently (2.2% y/y), with little indication that it will shift in either direction. For now, it’s all about keeping the faith and playing the waiting game.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

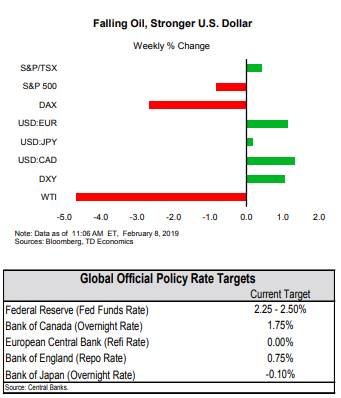

Financial News for the Week of February 8, 2019

HIGHLIGHTS OF THE WEEK

- Global central banks have followed the cue set by the Fed, as they too take a break from tighter monetary policy to assess mounting risks to global growth.

- Activity in the U.S. services sector cooled a bit in January as government-funding uncertainty and trade tensions weighed on business sentiment. Nonetheless, non-manufacturing activity remained well in expansion territory.

- Senior U.S. trade officials are off to Beijing next week to work on a trade deal, even as a meeting between the two countries’ presidents seems unlikely before the March 2nd deadline. All eyes will be on Washington to avert yet another government shutdown as the temporary funding gap expires on February 15th.

Central Banks Have Cause For a Pause

In a week where economic data was sparse (partly due to delayed releases as a result of the government shutdown), global developments filled in the gap. On the heels of the Fed’s decision last week, the Bank of England (BoE) and the Reserve Bank of Australia (RBA) both left policy rates unchanged this week.

The BoE cited the likelihood of slower growth due to elevated financial uncertainty on the possibility of a no-deal Brexit, while the RBA highlighted trade-related downside risks to global growth. Elsewhere, the European Commission also significantly reduced its GDP outlook for the euro zone in 2019 and 2020 as it expects growth in the bloc’s largest economies to be held in check by global trade tensions.

The decidedly dovish shift in U.S. and global central banks’ statements reflects the turn south in economic and inflation momentum in the latter half of 2018, as well as the accumulation of event risks over the next several months. Among these, trade tensions between the U.S. and China looms largest.

As long as the economic tea leaves remain cloudy, expect data-dependent central bank officials to remain cautious, taking the time to evaluate the cumulative impact of tighter financial conditions and slowing trade (see here). Stateside, this will have to be balanced against economic data that so far has continued to show resilience. As expected, initial jobless claims fell by 19k back towards post-recession lows during the week ended Feb 2nd as the effects of the longest U.S. government shutdown faded. In conjunction with the jobs report released last week, the data points to continued labor market strength.

Still, there are signs that the shutdown has had a negative impact on activity. The pace of expansion in the services sector decelerated in January. The ISM non-manufacturing index fell to 56.7 in January from 58.0 in December, reflecting concerns about the government shutdown, which negatively impacted new orders (Chart 2).

In his State of the Union address President Trump pleaded for unity, but continued to press a hardline on border security and immigration. All eyes will be watching the February 15 deadline for a longer-term funding package to avert yet another government shutdown that could take an additional toll on U.S. economic growth.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of February 1, 2019

HIGHLIGHTS OF THE WEEK

- Financial markets extended their gains this week. The re-opening of the U.S. government, the dovish FOMC statement, progress in the U.S.-China trade talks and a strong January payroll report all helped to boost sentiment.

- Global growth concerns persisted this week, but the U.S. economy continued to move along nicely. The labor market added 304k new jobs in January, and the ISM manufacturing index improved after a sharp decline in December.

- Even as domestic economic performance remains solid, global growth slowdown did not go unnoticed by the FOMC. The Committee left the fed funds rate unchanged, and went to great lengths to emphasize patience.

The Fed’s Rate Hikes: A Pause or A Stop?

Concerns about slowing global growth continued to linger this week. Even so, financial markets had a lot to be cheerful about: the U.S. government re-opened, the FOMC was dovish, the U.S.-China talks made progress and January payroll report showed blockbuster job growth. After a brutal December, this week’s trading capped the best monthly performance for the S&P 500 since October 2015.

Top of the list, the longest shutdown in U.S. history has ended – for now. A short-term spending bill keeps the government funded until February 15th. Still, the damage has been done. Various estimates suggest that the shutdown has shaved between 0.2-0.4 percentage points off first quarter GDP growth, which is tracking 1.6% (annualized). While most of the lost economic activity will be recouped in the following quarter, some of the loss will be permanent.

Global growth slowdown considerations did not go unnoticed by the FOMC. As widely expected, the Committee left the target range for the fed funds rate unchanged at 2.25%-2.5%, but the statement itself was very dovish. In particular, the committee acknowledged that, while domestic economic activity has been “rising at a solid rate”, risks to the outlook have increased, which would necessitate patience and flexibility on the Fed’s behalf. Any mention of “gradual” rate increases has been removed, suggesting the Fed is prepared to be patient for some time until the fog clears and its gets a better reading on global and domestic economic conditions.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 25, 2019

HIGHLIGHTS OF THE WEEK

- Global equity markets are up on the week, despite some negative economic news, and continued dysfunction in Washington. The ECB characterized the economic risks as to the downside, and will be more cautious removing stimulus.

- Amidst the U.S. partial government shutdown there was little data to unpack. Home sales showed a sour end to 2018 for real estate. Negotiations in Congress continue, but there is no clear end to the impasse at time of writing.

- Next week we get some key events - an FOMC rate decision with a press conference, and a payrolls report. Furloughed federal workers are expected to lift the unemployment rate, but should not affect the payrolls tally.

Markets Up Despite Lack of Good News on the Economy

We also got confirmation that China’s economy slowed dramatically in the second half of 2018 (Chart2). The rebalancing of China’s economy towards domestic consumption is underway, but the downward pressure from weaker construction and infrastructure investment on headline growth is being exacerbated by unanticipated declines in consumer and business sentiment resulting from trade tensions with the U.S.. So far the data remains consistent with our December forecast that calls for Chinese economic growth to slow further to 6.2% in 2019.

With the U.S. partial government shutdown affecting some government statistical agencies, there was little economic data this week. We did see that the resale housing market ended 2018 on a weak note, but we don’t know what the housing starts or permit picture looked like.

The Federal Reserve will still meet next week amidst the shutdown. We will get to hear from Chair Powell at a post-meeting press conference, as the Fed moves to holding a press conference at every meeting. The Fed is widely expected to keep rates steady, consistent with recent speeches, which emphasized the ability to be patient to see how the economy fares in the wake of slower global growth and the deterioration in sentiment.

Fortunately, we are not in a total data vacuum. Next week, the BLS will release employment data, where we will see if the blistering hiring activity in December carried over into January. As legislation has been passed guaranteeing furloughed federal workers back pay to cover the shutdown, these workers will not dampen the payrolls tally. However, they are still likely to boost the unemployment rate. The reference week for the Household survey was January 6-12th, and furloughed federal employees (0.2% of the labor force) would be classified as unemployed. Assuming federal workers are appropriately sampled in the survey, this could result in a 0.2 percentage point boost to the January unemployment rate. Meanwhile, the economic hit from the shutdown continues to mount. Growth in the first quarter is looking soft at 1.4% (annualized), assuming a 0.2%-pt direct hit from the shutdown if it lasts to the end of January.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 18, 2019

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The government shutdown extended to its 28th day, making it the longest on record with no clear end in sight.

- The White House upped its estimate of the impact of the government shutdown to a 0.5ppt drag on 19Q1 growth after

four weeks.This is much higher than private sector estimates of between -0.1 to -0.2 ppts. - As expected, the Brexit withdrawal agreement was soundly rejected by UK parliament. With the March 29th deadline

fast approaching, it looks increasingly likely that the UK will have no choice but to seek an extension from the EU.

Dysfunctional Governments on Parade

The shutdown is exacting a toll on those least responsible for it. Anecdotes continue to highlight the hardships that furloughed federal employees are experiencing. These include workers turning to payday loan companies and food banks, while also taking on side hustles, such as driving for Uber, in order to make ends meet. Although federal employees will eventually be paid for lost wages, the near-term pain is clearly taking a toll.

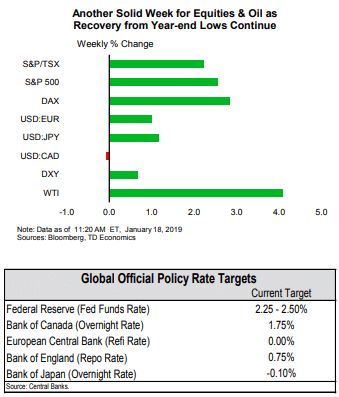

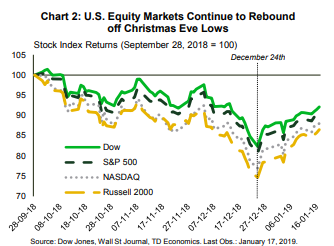

Despite the government dysfunction on display on both sides of the Atlantic, financial markets were largely unfazed. U.S. equity indexes have soared since the New Year, and are now back at levels seen in early December (Chart 2). There’s good reason for optimism. Data still being reported, such as weekly initial jobless claims, continued to signal a healthy economy. Trade talks with China are ongoing, with the next round set to take place on January 30th in Washington. Although little progress has been announced so far, news that U.S. officials were discussing ratcheting back some of the tariffs on Chinese imports in order to encourage an agreement helped to stoke a global rally in risk assets. Perhaps more importantly, Federal Reserve Presidents were out delivering speeches that reinforced the Fed’s willingness to be patient before the next rate hike. Indeed, patience is warranted given uncertainty about the economic impact of the government shutdown, and ongoing concerns about the health of the global economy.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 11, 2019

HIGHLIGHTS OF THE WEEK

- U.S. equity markets built on last Friday’s gains, firming up for the second consecutive week. Seemingly-fruitful trade negotiations between the U.S. and China offered notable support.

- With respect to data, both the ISM non-manufacturing index and small business confidence have eased from recent highs, but remain in healthy territory. Inflation data came in as expected, with core CPI holding steady at 2.2% y/y.

- The government shutdown, which is on track to become the longest in U.S. history, may test the Fed’s wait and see approach to monetary policy, given data distortions and delays. If it ends soon, we expect its impact to be quite modest. But each passing week has the potential to amplify the impact.

Of Mending Bridges and Building Fences

On the domestic data front, the numbers this week did little to rock the boat. After a hot three-month streak, the ISM non-manufacturing index descended below the 60-point threshold in December. But, at a reading of nearly 58, the index still points to a healthy pace of expansion for the lion’s share of the economy. Similarly, small business confidence eased off at the end of 2018, but remained quite upbeat relative to history. Employment indicators from the small business survey also reaffirmed the strength the U.S. labor market (Chart 1).

What truly dominated headlines this week were negotiations related to border security that hold the key to ending the partial government shutdown. Talks this week have so far failed to yield positive results. The current shutdown has already matched the longest 21-day closure of 1995-96 and appears likely to extend further.

Ultimately, the length of the shutdown will determine the overall impact. If it ends over the weekend, we expect the impact to be fairly modest, with the closure shaving off about 0.1 p.p. from first quarter economic growth. But the impact could prove to be non-linear, meaning that the economic costs rise with time. With respect to data, if the shutdown extends to next week the jobless rate could tick up by 0.2 p.p. as some 380k furloughed workers are counted as unemployed, though January payrolls should be spared the distortion. Delays will add to the fog. So far, only second tier indicators such as factory orders and new home sales have been affected. Among primary releases, the retail sales report is next in line to be taken off of the queue, with more releases impacted and uncertainty mounting the longer the shutdown continues.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 4, 2019

HIGHLIGHTS OF THE WEEK

- The New Year came with baggage from the old for thousands of federal employees caught in the middle of a budget tug-of-war between Congress and the White House that has led to a partial government shutdown.

- The volatility in stock markets continued early in the week as a slew of weaker-than-expected economic data and signs of a slowing China roused investor concerns that global growth may be slowing faster than expected.

- Fortunately, a strong payrolls tally lifted investors’ spirits by week’s end. Employment rose 312k and the unemployment rate edged up to 3.9% as more people joined the workforce. Hourly earnings growth also topped 3% (year-on-year) for a third consecutive month.

The Shutdown Slowdown

Set to enter its third week, the shutdown is expected to negatively impact consumer spending and business activity. Assuming it ends soon, it is projected to lower first quarter GDP growth by 0.1 percentage points. Once resolved, federal employees will receive back pay, (though workers on contract will not), and this should boost economic activity in the second quarter. The question that remains is how long it will last. The longest government shutdown was for 21 days in 1995 (Chart 1), but workers and businesses who depend on their spending, are hopeful that such a scenario will not be repeated.

By the end of the week, a nod to “patience” by Fed Chair Powell and a strong December jobs report helped pull equity markets back into positive territory. Non-farm payrolls exceeded expectations, adding 312K jobs in December. This resulted in 99 straight months of expanding payrolls – the longest stretch on record. Even the uptick in the unemployment rate to 3.9% resulted from a labor force rising participation rate. Such dynamics suggest that even amid the tightest labor market in decades, the U.S. economy is still able to pull workers off the sideline and into the job mix. Wages also surprised to the upside, growing by 3.2% year-on-year (Chart 2) – the best full-year gain since 2008.

The employment data should serve to calm concerns that the American economy is quickly running out of steam. While growth in 2019 is projected to be lower (see forecast), we still expect it to remain above the economy’s trend pace. All in all, government showdowns aside, consumers remain on firm footing, supported by the most favorable labor market in decades.

Shernette McLeod, Economist | 416-415 0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

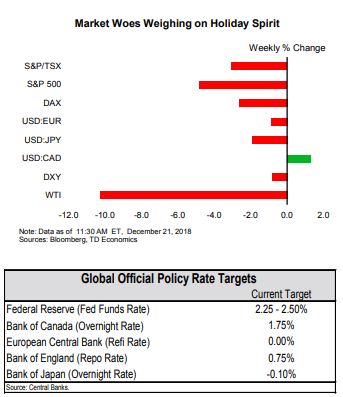

Financial News for the Week of December 21, 2018

HIGHLIGHTS OF THE WEEK

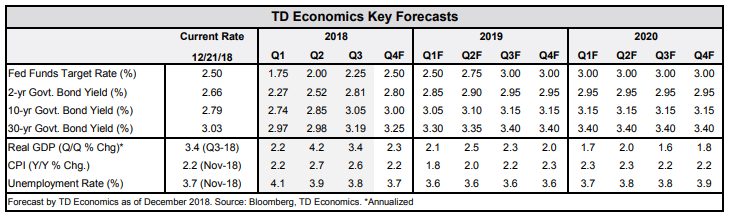

- As widely expected, the Fed hiked rates once more this year. At the same time, the Fed’s dot plot moved lower over the forecast horizon. These changes are consistent with a softer inflation and economic outlook.

- Data came in broadly positive, with housing starts and home resales both defying weaker market expectations. Consumer spending remained hot in November, with consumption looking set to advance by a sturdy 4% (annualized) in Q4.

- The late-year equity market sell off continued this week, with looming risks for a partial government shutdown marking the latest in a series of factors that are likely to weigh on sentiment through the New Year.

U.S. - Fed Set To Walk On Data Talk

The Fed’s dovish tone with respect to future hikes did little to appease investors. Both U.S. and international equity markets extended their losing streak on the news. It should be noted, however, that the path of interest rates is not set in stone, with the Fed placing a greater emphasis on data-dependency. As Fed Chair Powell put it, from this point on “we’re going to be letting the data speak to us”.

Third, the housing market remains soft but recent improvements are encouraging. Both housing starts (3.2%) and existing home sales (1.9%) rose in November, besting market expectations. On a less positive note, starts were propped up by the volatile multifamily segment (single-family starts fell for a third straight month), while home resales are still down between 3% and 15% year-on-year across major U.S. regions.

As the sugar high from monetary and fiscal stimulus wears off, we expect growth to slow to a still-healthy 2.5% in 2019. But, several potential potholes lie in the path ahead (see here). The latest spending bill impasse, which could lead to a partial government shutdown, is but one example. Given that shutdowns typically prove to be short-lived, history suggests limited economic impact. However, the hit to market confidence could prove more damaging.

Given expectations for slowing growth and the pronounced late-year selloff in equity markets (Chart 2), the “recession” word has gained traction recently. Our recent look at a broad range of indicators points sees little evidence for this in the economic data. That said, negative expectations have the potential to become self-fulfilling. But for now, the only thing we have to fear is fear itself.

Admir Kolaj, Economist | 416-944-6318

Overall, the U.S. economy is strong, and the Federal Reserve is well justified in raising rates another quarter point at its meeting next Wednesday. The real question is how the FOMC’s views have changed about how much further rates need to rise. Given the fairly benign inflation backdrop recently, we expect the Fed to hike rates more gradually in 2019.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.