Financial News for the Week of September 28, 2018

HIGHLIGHTS OF THE WEEK

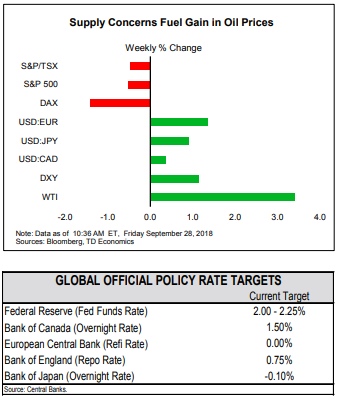

- Fed hiked rates by 25 bps this week as widely expected. But, the communiqué dropped the reference to policy remaining “accommodative”. Interpretations regarding this change led to volatility in bond yields and equities.

- The debate on textual changes in the Fed statement detracts from the main point: the Fed remains committed to additional tightening – a message echoed by a broadly-unchanged rising interest rate path in the Fed dot plot.

- Despite not being all positive, economic data reaffirmed the notion that the U.S. economy remains on solid footing. Of note, real personal spending rose 0.2% in August, keeping our tracking for Q3 consumption above 3% (ann.).

Don’t Let Textual Changes Get in the Way of Rate Hikes

Market focus however, gravitated more toward what was not in the Fed statement, rather than what was in it. The communiqué dropped the reference to policy remaining “accommodative”. This received a dovish interpretation initially under the premise that the Fed may be getting close to the end of the hiking cycle, leading to volatility in bond yields and equities.

The debate around textual changes in the Fed communiqué appears to detract from the main point – the Fed remains committed to further gradual tightening given its conviction for well-anchored inflation expectations and a positive view of the economy. Economic data in the week remained broadly in line with this narrative. The Fed’s preferred measure of inflation held right on target for the fourth straight month in August. Meanwhile, real personal spending was up 0.2% in the same month. While this marks a slight moderation in the monthly pace of spending, it’s sufficient to keep our tracking for third quarter consumption growth north of 3% annualized. A solid rise in wholesale and retail inventories added to the positive tally.

Putting all the pieces together, the economy is still on solid footing, with over 3% growth expected in the third quarter. With price pressures holding near target, this should indeed be sufficient for one more hike before the end of the year. Beyond this point, however, there is significantly more uncertainty, as trade disputes pose significant downside risk to the economic outlook.

The U.S.-China trade conflict saga continued to play out in the background, given other more salacious domestic political developments. China scrapped talks with the U.S. as tariffs on $200 bn of Chinese goods came into effect. Meanwhile, President Trump accused China of attempting to interfere in the upcoming midterm elections, given his stance on trade. With the two economic heavy-weights on a hard-to-avoid collision course, we see this dispute as a key risk to growth. Tariffs in effect and those threatened could knock off up to 1 p.p. from U.S. and 0.3 p.p. from global economic growth (see here).

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of September 21, 2018

HIGHLIGHTS OF THE WEEK

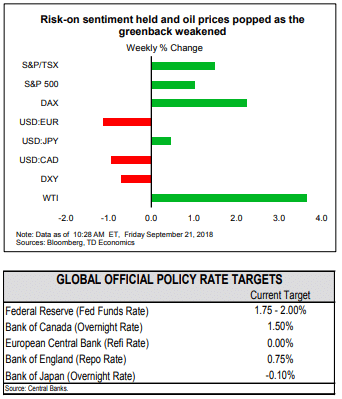

- U.S. equity markets were unbowed by escalating trade actions between the U.S. and China this week. The S&P500 reached new highs bolstered by healthy earnings reports and growth in share buybacks.

- Equity market optimism is backed up by an economy set to grow by an impressive 2.9% this year, boosted by fiscal stimulus. The Fed is expected to respond to consistently above-trend growth with another 25 basis point rate hike next week, taking the upper limit of the fed funds rate to 2.25%.

- Our latest forecast does not include the impacts of the latest tit for tat tariffs between the U.S. and China. If the current tranche plays out as planned, it could weigh notably on growth at the same time as the fiscal sugar rush fades.

Market Optimism Unbowed by Trade Risks

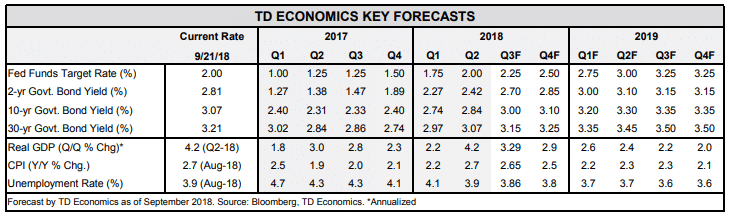

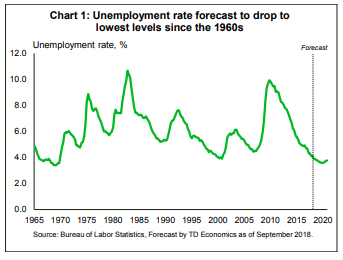

Strength in equity markets is backed up by a very healthy U.S. economy. Our latest Quarterly Forecast outlines how fiscal stimulus is helping to boost real GDP growth to 2.9% this year. Growth well above potential is expected to push the unemployment rate to the lowest level since Woodstock (Chart 1). With the economic party raging, the Federal Reserve is widely expected to drain some more punch from the bowl next Wednesday. A 25 basis-point rate hike will raise the fed funds rate to 2.00-2.25%, marking the eighth rate hike since 2015. We expect the Fed to hike four more times over the next year, placing the fed funds target at a peak level of 3.25% in 2019.

Next week’s decision looks like a done deal, but the Fed’s economic forecast will still be closely watched. Now that another tranche of tariffs on Chinese imports and China’s retaliatory measures are on the books, it will be interesting to see how FOMC members adjust their outlook, if at all. Our forecast calls for growth on a quarterly basis to slow from roughly 3% in the second half of 2018 to below 2% by 2020. Those numbers do not include the impact from the latest round of tit for tat tariffs.

In the event of full escalation of the U.S.-China trade war, where the administration follows through on its threat of tariffs on a further $267bn in Chinese imports, the economic hit would double to 0.8 percentage points in total. That could push US growth closer to 1%. For now, it seems financial markets do not think that this outcome is too likely, but forecasters are becoming increasingly concerned about the risks to growth in 2019. The OECD lowered its targets for global growth slightly in its outlook published this week. It now expects the global economy to grow by 3.7% next year, down two ticks from its 3.9% forecast back in May citing downside risks from trade.

We also expect global growth to moderate next year to 3.6%, due to weakening emerging market momentum, without the impact from escalating China-U.S. trade tensions. The path forward on tariffs is not written in stone, and hopefully if the political rhetoric cools down after the U.S. mid-term elections in November, cooler heads might also prevail at the trade negotiation table.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

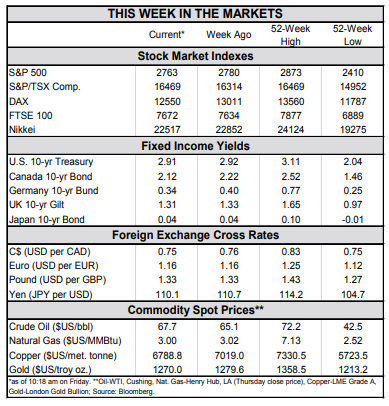

Financial News for the Week of September 7, 2018

HIGHLIGHTS OF THE WEEK

- Concerns about emerging markets continued to weigh on investor sentiment this week, with the selloff in EM assets and currencies spreading beyond Turkey and Argentina.

- Meanwhile, domestic data remained positive. ISM indices for both manufacturing and services sectors rose handsomely in August. The payroll report delivered another batch of good news with 201k new jobs created on the month and wage growth accelerating.

- All told, the U.S. economy continues to boom, giving the Fed little reason to alter its interest rate normalization plans that include another increase on September 26th.

Summer's Ending, But the U.S. Economy Still Shines

Trade developments and payrolls stole the limelight in this busy, holiday-shortened week. Concerns about emerging markets continued to weigh on investor sentiment with the selloff in EM assets and currencies spreading further beyond Turkey and Argentina. Meanwhile, the increased risk of another round of economic sanctions has sent the Russian ruble lower. While selling pressure eased somewhat by the week’s end, headwinds battering emerging markets are unlikely to dissipate soon. U.S. expansionary fiscal policy is buoying domestic growth, putting upward pressure on the dollar, inflation, and interest rates. At the same time, trade spats with China and other U.S. trade partners are weighing on overseas currencies and global growth. As a result, dollar strength coupled with worries about trade should continue to fuel investor flight from emerging markets.

Strong sentiment and economic momentum is boosting hiring, as evidenced by today’s payroll report, which showed that 201k new jobs were created in August. With the jobless rate hovering at historic lows, it is becoming increasingly difficult to find workers to fill positions. This continues to draw in workers from the sidelines (Chart 2) and also motivating firms to raise wages. As a result, the closely watched average hourly earnings measure rose 0.4% in August, accelerating to 2.9% on a year-over-year basis. This is the fastest pace of wage growth of the recovery, and may prove to be the start of the long-awaited sustained pickup in wage growth.

Clearly the U.S. economy is barreling full steam ahead, and the estimated impact of tariffs has so far been quite small. The $50 bn in import tariffs on China and the steel and aluminum tariffs may shave roughly 0.2 ppts off U.S. real GDP growth in about years’ time, and add two tenths of a point to inflation. However, as we note in our report, the tariffs in place are only the tip of the iceberg relative to those under review or threatened. So far the U.S. has levied tariffs on $107 bn of imports into the U.S., but the total tariff action under consideration amounts to $715 bn. If implemented, they could place about 1.2 ppts of U.S. and 0.4 ppts of global growth at risk.

All told, an escalation in the trade spat with China and waning global demand may yet test the durability of the current expansion. However, for now the U.S. economy continues to boom with little reason for the Fed to alter its interest rate normalization plans that include another quarter point increase on September 26th.

Ksenia Bushemenva, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 31, 2018

HIGHLIGHTS OF THE WEEK

- Markets reacted positively to developments that the U.S. and Mexico had reached a trade deal. Details still need to be finalized, including Canada’s position. A revised, trilateral agreement looks unlikely to be achieved today.

- Data was broadly positive this week. Second quarter GDP was revised up slightly, and after-tax corp. profits rose to the highest y/y pace since 2012. A 0.2% July rise in real spending marks a good start to third quarter consumption.

- Core PCE rose 2% y/y in July. Steady inflation, holding at or near target since March, gives the Fed scope to continue on with its gradual reduction in stimulus. The next Fed hike is expected to come in September.

Inflation is just where the Fed wants it to be

The U.S.-Mexico trade agreement was welcomed by markets this week. Coupled with positive data flow, U.S. equities made further gains midweek. The agreement included augmented rules of origin for autos, strengthened intellectual property protections, and enhanced protections for labor and the environment (for a complete list see here). Details still need to be finalized, including Canada’s position. Today’s deadline for a tri-party agreement looks unachievable. An updated NAFTA agreement would allow the U.S. to shift focus back to resolving its trade dispute with China. News reports anticipate that President Trump will impose tariffs on an additional $200 bn of Chinese imports next week, helping pare back equity gains by week’s end.

Personal income and spending data for July also proved positive. Nominal income (+0.3% m/m) and spending (+0.4%) recorded solid gains that were in line with prior months. On an inflation-adjusted basis, spending rose 0.2% m/m, extending the streak in real gains to five months and marking a good start to the third quarter. Last quarter’s 3.8% rebound in consumption will be hard to repeat. Nevertheless, upbeat consumer confidence, which is sitting at an 18-year high, along with continued employment gains and rising incomes all point to healthy consumer spending growth in the 2½ to 3% range for the rest of the year.

Although the U.S. economy is experiencing a goldilocks moment, the same cannot be said for many of its international counterparts. Financial troubles in Turkey and Argentina have policymakers there battling plunging currencies and surging inflation. Argentina’s central bank hiked its policy rate to 60% this week – the highest in the world. All told, although the impact of trade policy uncertainty and turmoil in some emerging markets has been limited thus far, they remain clear downside risks to the domestic, and global, economic outlook.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 24, 2018

HIGHLIGHTS OF THE WEEK

- Financial markets jitters have eased somewhat this week as concerns about emerging countries have temporarily subsided, helped in part by a lower U.S. dollar.

- Economic data was mixed. U.S. business investment remained upbeat in July, with new orders of capital goods (ex. aircraft) rising 1.4% m/m. Meanwhile, the housing market disappointed yet again in July.

- On the policy front, FOMC meeting minutes and a speech by Chairman Powell noted the recent strength in economic performance and confidence in the outlook, signaling continued gradual interest rate increases.

FOMC Signals Continued Gradual Rate Hikes

Financial markets’ jitters eased somewhat this week as concerns about emerging countries have temporality subsided. This was helped by the lower U.S. dollar, which has reversed some of its recent strength following president Trump’s comments that he was “not thrilled” about the Fed’s interest rate increases.

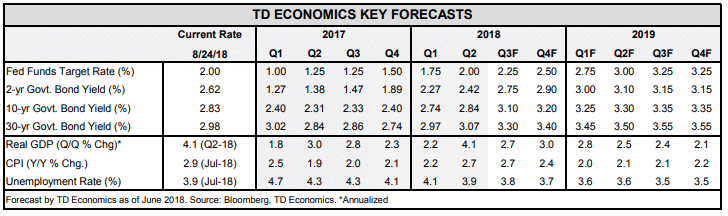

While the U.S. economy, broadly, is running at full throttle, the housing market has hit a speed bump (see Chart 1). Both new and existing home sales failed to make headway in the first half of the year, and this week’s data suggests that the softness has extended into the third quarter. Existing home sales declined for a fourth consecutive month in July (-0.7% m/m), while sales of new homes slipped by 1.7% m/m, suggesting residential investment could again weigh on GDP growth in Q3.

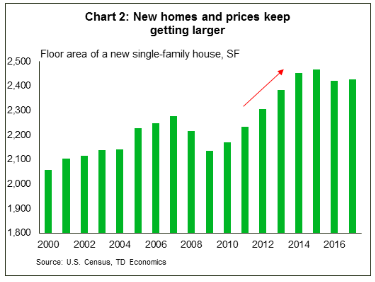

It is hard to square the housing market underperformance amid strength in other sectors of the economy as well as rising employment and incomes. Most commentators chalk tepid sales to low inventory, particularly in the entry-level segment. While new construction has been rising, it has been skewed toward higher end of the market with houses getting progressively larger during the recovery. Square footage of the median house was 13% larger in 2017 than it was back in 2004 (see Chart 2). Rising home prices and mortgage rates, which are up nearly 60 basis points since last year, have also dented affordability. These and other headwinds are likely to persist in the near term, however, but there are also some silver linings: price growth appears to be slowing and housing inventory finally stopped shrinking in July (on a y/y basis), stabilizing for the first time since the end of 2014..

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 17, 2018

HIGHLIGHTS OF THE WEEK

- Concerns about Turkey drove market volatility this week, but U.S. equity markets managed a rebound.

- Strong retail sales and historically-high small business optimism suggest a strong economic expansion in the U.S. this quarter.

- Although concerns eased by week’s end, Turkey is not out of the woods yet. It remains in the early stages of a balance of payments crisis, and is likely to trigger further bouts of market volatility.

Markets Brush Aside Emerging Market Fears For Now

Like Argentina, Turkey is too small in the scope of the global economy to trigger a broader global crisis. Turkey’s economy is responsible for about 1.7% of global annual output (2016 purchasing power parity), a little more than Canada at 1.4%. Contagion risk via trade linkages is low, although Europe is most exposed. Similarly, financial contagion is limited, with Spanish, Italian, and French banks at risk to lose a tiny proportion of foreign loans.

That said, contagion to other economies can still occur through confidence and sentiment channels. That was evident this week with the turmoil in global financial markets that drove a selloff in risk assets and emerging market currencies, and a bid for developed market bonds. Further bouts of volatility are likely as emerging market economies with large imbalances are targeted one-by-one by increasingly discerning investors.

Although concerns eased by week’s end, Turkey is not out of the woods yet. It remains in the early stages of a balance of payments crisis. A sudden stop to capital inflows has occurred, and the next step for Turkey involves spending cuts and an emphasis on boosting exports to help generate foreign currency required to pay for its large external obligations. The medicine will be bitter, but the sooner Turkish authorities follow through with interest rate increases, capital controls, and fiscal spending cuts, the more likely they can mitigate the economic fallout.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

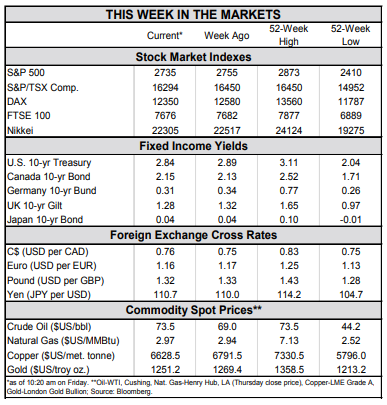

Financial News for the Week of July 13, 2018

HIGHLIGHTS OF THE WEEK

- For the second week in a row, action on Chinese import tariffs dominated the economic news, but markets remained positive overall, likely reflecting relief that oil prices have come off their recent highs.

- Since China retaliated to the first salvo of U.S. tariffs, the U.S. is moving ahead with the process to impose a further 10% tariffs on $200 bn of Chinese goods, after a two-month consultation period. Tariffs will make the Fed’s job of reading inflation signals more difficult.

- So far June CPI data showed inflation rising steadily, as expected. But, it is still too early to see much impact from tariffs in consumer prices.

Tariffs Make Fed’s Job Tougher

President Trump had previously threatened that if China retaliated to the first tranche of U.S. tariffs, he would order further 10% tariffs on $200 bn worth of Chinese imports. China indeed retaliated, and so this week the U.S. Trade Representative (USTR) started the process of making good on this threat by publishing a list of goods which would be subject to a 10% tariff. To be clear, these tariffs are not immediate; they need to go through a two-month process before being enacted. The USTR will hold a public consultation period ending on August 30th.

These tariffs will raise input prices for many American businesses, but the extent to which they are passed on to consumer prices will depend on the competitive environment of the industry. If businesses can’t pass on price increases to their customers (for fear of losing too much market share), they may have to cut costs by reducing staff or planned investments. Both of these actions will crimp growth in the overall economy. If tariffs are fully passed on to consumers you get higher inflation, and slower growth by a different channel. The federal government may mitigate the negative impact by funneling the tax revenues back into the economy.

In a perfect world, the Fed will look through one-time price increases caused by tariffs. However, if tariffs are placed on a wide variety of goods further up the supply chain, it makes it difficult to disentangle how much inflation is due to a hot economy, and how much is the result of tariffs. That raises the risk the Fed misinterprets the inflation signal.

This suggests the Fed is likely to be very cautious. This week’s June CPI data was too early to pick out evidence of import tariffs. Overall the data showed yr/yr inflation continued to rise as expected, reaching 2.9% (Chart 1). Core inflation was 2.3% yr/yr, having risen steadily for the past year. The upswing in annual inflation in part reflects comparisons to low readings last year. Monthly increases look steadier (Chart 2), with little acceleration in June.

Next week Chair Powell testifies before Congress on the economy. It should have been a straightforward good news story of a strong economy, with inflation rising in a non-threatening way and gradual increases in interest rates. Now, he is likely to face questions on the impacts of tariffs, which are both uncertain and hard to forecast.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

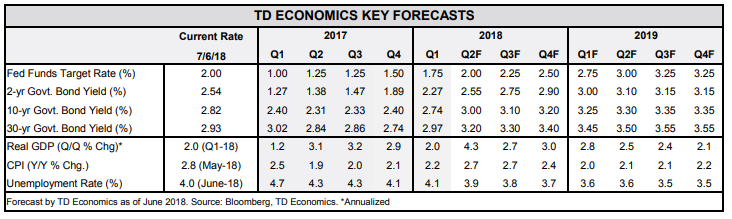

Financial News for the Week of July 6, 2018

HIGHLIGHTS OF THE WEEK

- A holiday-shortened week was nevertheless chock-full of data releases that confirmed the U.S. economy continues to expand at a strong above-trend pace.

- Economic activity remains robust, but there are signs that trade uncertainty may be impeding further improvement.

- Tariffs on $34 billion in goods from China, and on U.S. goods to China, take effect today. Although these tariffs remain a downside risk to our economic outlook, further escalation could prove direr.

China Tariffs Likely to Impede Economic Momentum

Escalating tensions between Canada’s two most important trade partners weighted on sentiment, but economic data has so far remained intact. Hiring resumed in June with the Canadian economy adding 32k jobs last month. Gains were led by construction and manufacturing, while services disappointed, losing jobs on net for the first time in five months. Despite the job creation, unemployment ticked higher by 20bps to 6.0% as more than 75k people entered the labour force – a six year high. Average wages decelerated, down some 30bps, but at 3.6% y/y remains near a decade-high (Chart 1).

Canadian trade figures were less inspiring with the deficit in May widening to $2.8bn. Imports were up 1.7% and 1.2% in nominal and real terms, respectively. They were somewhat boosted by airliner and gasoline imports, but strength was broad-based across categories, indicative of healthy domestic demand. Exports, on the other hand were weak, remaining flat in nominal terms while volumes fell 1.0%. While much of the weakness was related to transitory factors including supply disruptions in automotive parts and work stoppages in iron mines, exports are unlikely to surge going forward. Alongside ongoing NAFTA uncertainty, the imposition of tariffs in June will have a severe impact on the Canadian metals industry, with potential for downstream effects a real risk.

Risks related to trade and housing will surely be top of mind for the Governing Council when it meets next week to discuss monetary policy. But, until they are seen as likely to materialize they will not drive monetary policy. This is set on incoming data and the outlook, which are relatively sanguine. From that standpoint, another 25 basis point hike next week is the most appropriate move.

Michael Dolega, Senior Economist | 416-983-0500

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 29, 2018

HIGHLIGHTS OF THE WEEK

- The BEA’s third estimate of Q1 real GDP downgraded growth slightly to 2.0%, from 2.2% previously. May data did show flat real personal spending, but strength in March and April still set Q2 consumption up for a decent rebound.

- The Fed’s preferred measure of inflation, core PCE, hit its 2% target in May. This supports our forecast for continued gradual monetary policy tightening, as the focus shifts to containing upside risks.

- Shifting headlines on trade were a key driver of stock market activity. Foreign policy also got in on the action, with crude prices surging on the anticipation of tougher U.S. sanctions on Iran.

BULLSEYE!

Consumer spending should continue to follow a decent 2.5% growth path in the second half of 2018, bolstered by a tight labor market and tax cuts, which will continue to support incomes. The latter will feature favorably for housing demand, even as interest rates rise. But a lack of inventory will constrict the sales pace. On this front, pending home sales – a solid gauge of near-term activity – retreated in May, marking the second consecutive monthly decline and weakening a previously improving trend.

With little else in the way of primary data, shifting headlines on trade remained an important driver of stock market activity. Markets opened lower on Monday after indications that the U.S. planned new curbs on Chinese investment in U.S. tech firms. Foreign policy also got in on the action, with crude prices surging on the anticipation of tougher U.S. sanctions on Iran. The rollercoaster ride in equities continued, with the President seemingly taking a softer stance on Chinese tech investment, but then hinting at the possibility of protectionist action on autos.

Ultimately, trade spats with a number of important trading partners risks siphoning away much of the economic boost from fiscal stimulus by way of higher consumer prices, reduced exports, supply chain disruptions, and by denting consumer and business confidence. Under the presumption that the tougher trade rhetoric is simply a negotiating tactic, there is still hope that common sense will prevail, and tensions will de-escalate. The risk, however, is that once the wheels have been set in motion, tensions can quickly escalate to a full-out trade war. China, Mexico and the EU have already retaliated to some degree, while Canada is announcing a detailed list of U.S. products to be slapped with retaliatory tariffs at the time of writing, which will take effect over the weekend. The U.S. may up the ante, further reinforcing the negative feedback loop.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 22, 2018

HIGHLIGHTS OF THE WEEK

- The U.S. economy is barreling ahead with more momentum than we had expected. Our latest forecast upgrades real GDP growth to 3.0% in 2018, from 2.7% in March.

- 3% is difficult to sustain over the medium term. As the fiscal boost fades, higher interest rates weigh and structural constraints bind, growth in 2019 is set to slow.

- Even with slower growth, the U.S. is still set to out-perform its G7 peers. The main downside risk to the outlook is an escalating trade war. While this presents a serious risk to its trading partners that are dependent on access to the U.S. market, America has sufficient cushion to withstand the hit.

Let the Good Times Roll!

A healthy economy is set to push the unemployment rate even lower over the coming quarters. This in turn will add to inflation pressures. Stronger economic momentum and firming inflation have prompted us to edge up our rate-hike expectation by an additional 25 basis points for this year, taking the upper end of the policy range to 2.5% by year end (see Financial Outlook).

At the risk of sounding like a broken record, 3% growth is difficult to sustain beyond a near-term cyclical updraft. The boost from tax cuts and government spending increases will start to fade next year. Add to that the reduced lift from monetary policy. The Fed has raised its policy rate 150 basis points over the past 18 months, and is expected to raise it 125 more over the next 18 months (Chart 1). Higher oil prices than in our previous forecast will also nip at consumer and businesses’ purchasing power. These cyclical concerns add to the underlying structural dynamics of the US economy. Even with an expected improvement in productivity growth, an aging population holds potential growth in the economy to roughly 2%.

Now is the time in the economic cycle where so –called “animal spirits” can lead to excess risk taking, and sow the seeds of the next recession. For the U.S. it is as yet unclear what these unknowns might be. Indeed the factors that cause the next recession may come from outside the U.S.’s borders. But one potential risk is self-inflicted. An escalating trade war is a clear downside risk, particularly for the U.S.’s key trading partners (see impacts of auto tariffs on Canada), which would have knock on impacts at home. Even so, with the economy doing so well, it has sufficient economic cushion to absorb some negative shocks.

In an otherwise quiet week for economic data, we did get an update on the trigger of the last recession – the housing market. There a few signs of froth there. Housing starts continued their gradual upward trend in May. Residential construction has been on a stronger footing this year after weakness in multi-unit structures drove a lull in 2017. The existing home market, on the other hand, was a bit disappointing in May. Sales have trended down recently, as the market struggles with a lack of listings. Forward looking indicators suggests activity should improve in the months ahead. In time, construction of new homes should help, but improvement is expected to be gradual as affordability constrains demand.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.