Financial News for the Week of April 6, 2018

HIGHLIGHTS OF THE WEEK

- Trade developments captured headlines this week. The U.S. disclosure of detailed plans regarding the tariffs on $50bn worth of Chinese imports led Beijing to retaliate with planned tariffs on $50bn of U.S. exports. The hardened Chinese stance led President Trump to threaten additional tariffs on $100bn worth of Chinese goods.

- While the announced tariffs are likely to merely shave off about 0.2pp from annualized GDP growth in the U.S. over the next two years, the potential for the conflict to escalate to a full-scale trade war is much more concerning.

- Economic data came in healthy with the ISMs holding near recent highs while auto sales came in slightly better than expected in March. Payrolls disappointed despite a healthy ADP print, but wage growth accelerated on the month.

Retaliating on Retaliation: Trade War Drums Beating

It is important to distinguish between tariffs that we already have details on and the latest inflammatory rhetoric. The former are not overly concerning. We estimate that the U.S. tariffs (including enacted tariffs on steel and aluminum) could shave off about 0.1 pp from annual GDP growth over the next few years, and could add up to 0.1 pp annually on inflation. Depending on what’s finally enacted following a consultation period, the price and demand impacts could be somewhat more pronounced if the tariffs are applied largely on consumer goods rather than business investment goods. On the other hand, China is targeting roughly 38% of American goods exports to China, which represent only about 0.3% of U.S. GDP. We estimate that these tariffs would reduce U.S. growth by up to 0.1 pp annually for the next two years. In this vein, slightly weaker U.S. demand could also act to offset some of the price pressures from the U.S. import tariffs.

Developments on the trade front overshadowed decent signals from the economy. Auto sales came in slightly better than expected in March, and the ISM indices remained well in expansionary territory, despite easing off slightly (Chart 1). Payrolls gains slowed to 103k on the month, but this came atop of a very strong showing in February at 326k (Chart 2). Looking past the monthly noise, the underlying job market remains healthy, as demonstrated by increased wage gains – up 2.7% y/y.

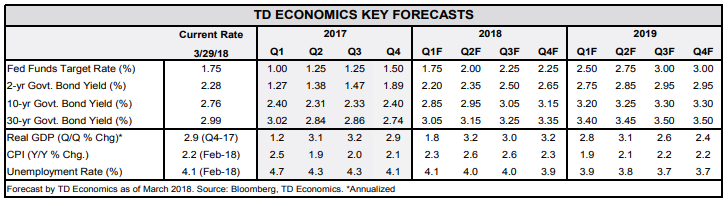

Tax cuts and increased government spending are expected to add fuel to the labor market and the economy, with the latter expected to run at roughly 3% over the next few quarters (see forecast). In short, the U.S. economy remains on a solid course, but further escalation in the trade conflict poses a material downside risk. The hope and expectation is for the conflict to be resolved through the ‘The Art of the Deal’ rather than ‘The Art of War’.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of March 29, 2018

HIGHLIGHTS OF THE WEEK

- Investor optimism recovered following the softening of China’s stance to the recent U.S. tariffs while the renegotiated KORUS trade deal with South Korea also bodes well for stateside producers.

- February’s consumer spending report indicated progress on the inflation front. However, weak consumer spending will weigh on GDP growth in the first quarter which is expected to advance by less than 2%.

- Consumer strength should reassert itself as the year progresses alongside a tightening labor market and tax cuts, enabling the Fed to raise rates two more times this year.

Soft Spending Suggests Another Weak Q1

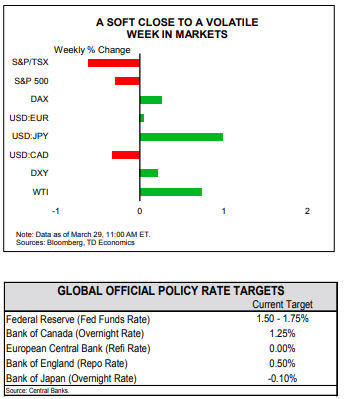

Global equity markets fared better as trade tensions thawed. However, trade uncertainty still lingers in Europe, with only four weeks until a temporary exemption from U.S. imposed steel and aluminum tariffs expires. The EU is contemplating lowering tariffs on a range of U.S. goods including cars, machinery, pharmaceuticals, and food in hopes of averting a trade war. However, the “carrot” approach is not favored by all members of the EU, including France. That could result in higher volatility in global equity markets in the weeks ahead.

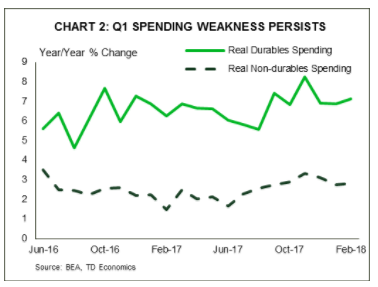

February’s consumer spending report indicated progress on the inflation front. Core PCE inflation ticked up slightly (Chart 1), with price gains over the recent three months averaging 2.3% in annualized terms. We expect this strength in inflation to continue, supported by diminishing slack in the U.S. economy, rising global economic activity, a relatively weak USD, and the fading of idiosyncratic factors. However, other details of the report were less encouraging. Consumer spending came in soft (Chart 2), adding to January’s disappointment, and weighing on GDP growth in the first quarter, which is still expected to advance by less than 2%. Still, we believe that consumer strength will reassert itself as the year progresses alongside a tightening labor market and tax cuts. Such a backdrop should enable the Fed to continue gradually raising interest rates this year, with another two hikes expected this year before 75 basis points of increases during 2019.

Katherine Judge, Economist | 416-307-9484

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of March 23, 2018

HIGHLIGHTS OF THE WEEK

- Markets have swung from euphoria over tax cuts, to the protectionism pits, as the White House announced imminent tariffs on up to $50 billion in Chinese imports. China has also announced modest retaliatory measures

- It remains to be seen what kind of actions will ultimately be taken. As the scope of steel and aluminum tariffs is continually narrowed, the White House’s bark on tariffs may prove worse than its bite.

- As expected, the FOMC hiked rates 25 basis points, but more importantly, it upgraded its outlook for growth and inflation. The median “dot” now suggests three rate hikes in 2019, up from two in the last forecast. This suggests the Fed will continue to be cautious in the face of fiscal stimulus.

Markets Hurt by Tough Trade Talk

Despite good news on the U.S. economy, the announcement of potential tariffs on Chinese imports dented sentiment and took equities sharply lower on the week. Over the past three months, markets have swung from euphoria over tax cuts, to the protectionism pits, as the White House followed up the announcement of forthcoming steel and aluminum tariffs with a 25% tariff on up to $50 billion in Chinese imports.

As expected, China has announced how it would retaliate, with 15% tariff on U.S. imports of steel pipes, fruit, wine and other products, and 25% on pork and recycled aluminum, all in targeting about $3 billion in U.S. goods. The relatively modest size of the planned retaliation suggests China is willing to pursue dialogue with the U.S. to address trade disputes about the continuous violation of intellectual property rights of U.S. firms that operate in China. It’s not clear when or even if the announced tariffs will come into effect. We have already seen the U.S. walk back the scope of recently announced steel and aluminum tariffs, by exempting more countries, suggesting that this week’s announcement is an opening gambit.

However, as demonstrated by markets this week, it is the indirect effects of a more adversarial global trade environment and the uncertainty it breeds that could hamper investment and trigger volatility on financial markets. And it is unfortunate that these threats come just as growth in global trade flows has accelerated (see Chart 1).

That bias was demonstrated in just one additional hike by the end of 2019 as a result of its upgraded outlook. This forecast is consistent with our own view. That said, seven of 15 FOMC members now have four hikes penciled in for 2018, up from four in December, suggesting that it won’t take much to tip the number of hikes expected in 2018 from three to four. For now though, the Fed doesn’t look keen to get too far in front of the expected pickup in economic growth, but is happy to make sure its outlook is realized before increasing the speed of rate hikes. Given the risk that too much fiscal stimulus in a hot economy could result in the Fed raising rates too quickly, and contributing to a recession, this cautious approach is reassuring.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of March 16, 2018

HIGHLIGHTS OF THE WEEK

- Our outlook for the U.S. economy through 2019 got revised up this week, as additional fiscal stimulus helps boost the outlook for domestic demand growth.

- The inflation reading for February remains consistent with the view that price pressures are gradually building.

- The sunny outlook is not without downside risks. Higher interest rates have a tendency to expose vulnerabilities, and the threat of a global trade war is becoming more real.

Economic Boom to Last Through 2019

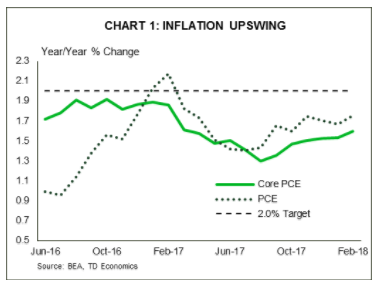

With economic growth expected to average close to 3% over the remainder of this year, capacity pressures are expected to build. Not only should this incent firms to invest, but scarcer labor should support wage growth. Our outlook anticipates that underlying inflation in the U.S. will hit the Fed’s target of 2.0% before the end of the year, and stay slightly above target through 2019 (Chart 1). The CPI data for February supports this view, as price pressures ticked up a touch. Headline inflation rose to 2.2% y/y (+0.1 from 2.1% in January), while core inflation held at a 1.8% y/y pace.

After February’s consensus-busting job gains of 313k, we anticipate monthly job gains of 200k in upcoming months, roughly in line with its average since the Great Recession’s end. This should push the unemployment rate, which already sits at an eighteen-year low of 4.1%, even lower, reaching 3.7% by the end of 2019. Moreover, rising wages should encourage greater labor force participation enough to offset the drag from population aging.

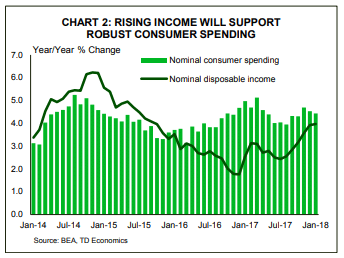

In contrast to the very strong medium-term outlook, the outlook for the first quarter of 2018 is somewhat weaker. Retail sales in the first two months of this year have disappointed expectations, suggesting much softer consumer spending in the first quarter than the 3.8% (annualized) growth recorded at the end of 2017. We anticipate spending growth to re-accelerate in the second quarter, supported by the receipt of tax refunds, strengthening wage growth, and reduced personal income tax rates.

Booming economic activity together with building price pressures suggest that the Federal Reserve is likely to continue to raise interest rates this year and next. With three rate hikes on tap this year, the upper end of the range of the Fed’s policy rate should rise to 2.25% by year end. Moreover, better growth for 2019 suggests an additional 75bps of rate hikes, bringing the upper end of the range to 3.0% at the end of 2019.

Fotios Raptis, Senior Economist 416-982 2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of March 9, 2018

HIGHLIGHTS OF THE WEEK

- President Trump announced tariffs on steel and aluminium imports to take effect in 15 days. The scope is narrower than initially announced. Mexico and Canada are exempt, and more allies may be excluded once the levies take effect.

- The American economy continues to hum along, with a very solid job report in February. The Fed’s Beige Book also painted a relatively rosy picture, but also one where businesses are starting to pass higher costs onto customers.

- Inflationary pressures are building in the U.S., and import tariffs will increase the force. This presents a challenge for the Fed which will have to incorporate the uncertain impacts of fiscal stimulus, and now tariffs into its forecast.

All Signs Point to Higher Inflation

However, trading partners are expected to retaliate, levying tariffs on U.S. exports. Economic studies have shown that the overall costs to the economy from these trade battles outweigh the job gains in the protected sector. Our own estimates for the steel and aluminum tariffs specifically suggest the overall growth impacts in the large U.S. economy would be fairly modest, but that they could raise inflation a couple of tenths of a percentage point.

This week’s economic data certainly doesn’t suggest the U.S. needs economic protection. Payrolls grew by an impressive 313k jobs in February. The unemployment rate stayed at its 17-year low of 4.1%, where it has been since October. Hiring has accelerated in recent months, driven by the goods sector, which had stumbled somewhat in the wake of the oil price crash, but is now making up the lost ground. Wage growth cooled slightly, with average hourly earnings up 2.6% versus a year ago, down from 2.8% in January. However, when this volatile series is smoothed, wage gains have been steady at around 2.6% for about a year, and have been outpacing inflation for over three years.

The Fed’s Beige Book also painted a picture of an economy that is humming along. Fed districts universally reported labor market tightness and heightened demand for qualified workers. Several districts reported increasing compensation as a result of the tax cuts that came into effect at the start of the year. The report also suggested that businesses are increasingly passing on increases in input prices. A variety of forces are expected to push inflation higher this year, the only question is how quickly.

The risks that inflation will accelerate faster than the Fed currently expects are mounting. The FOMC’s next announcement is on March 21st, and a hike at the meeting is essentially a lock. We currently expect three 25-basis point moves in 2018, but the risks are skewed to more hikes rather than fewer.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of March 2, 2018

HIGHLIGHTS OF THE WEEK

- Markets sold off sharply this week, following a somewhat hawkish assessment of the U.S. economy from the Fed’s new chair Jerome Powell and the announcement of steep tariffs on steel and alumimium imports by Donald Trump.

- Despite the market reaction to Powell’s comments, there was not much in the data this week to indicate that the economy is overheating. Both headline and core PCE inflation remained unchanged in January, coming in at 1.7% y/y and 1.5% y/y, respectively. Real consumer spending fell by 0.1% on the month. Vehicle sales also weakened in February.

- Both consumption and GDP will start the year on a softer footing but weakness is expected to be short-lived. Tax cuts and tightening labor market will support consumer spending and above-trend growth over the remainder of 2018.

Fears of Trade War Rattle Financial Markets

In his speech on Tuesday, Mr. Powell struck an upbeat tone on the U.S. economy and inflation, saying that his “outlook for the economy has strengthened since December.” He also highlighted potential upside risks to growth and inflation stemming from fiscal policy and the improved global economic backdrop. Without stating the exact number of rate hikes expected this year, Powell seems to have opened the door to a faster rate of normalization as long as the economic data cooperates. Markets were quick to interpret his comments as hawkish, with equities selling off and bond yields rising. New York Federal Reserve president Bill Dudley added more fuel to the fire by saying that four rate hikes by the Federal Reserve this year would still constitute a “gradual” pace of tightening.

Market losses extended further on Thursday on fears of trade wars following Donald Trump’s announcement of a 25% import tariff on steel and 10% on aluminum. While nothing has been signed yet, should these tariffs be introduced, they will lead to higher input prices for many manufacturing and construction industries which rely heavily on steel and aluminum inputs and ultimately result in higher prices for U.S. consumers, thus posing an upside risk to the Fed’s inflation outlook. The Fed may look through a one-time change in prices as a result of tariffs, but will be cautious on the impact on inflation expectations and potential economic growth – trade wars are not typically good for productivity growth.

Still, for the time being there is not much in the incoming data to indicate that the economy is overheating. Inflation-wise, both headline and core PCE inflation remained unchanged in January, coming in at 1.7% y/y and 1.5% y/y, respectively. Real consumer spending fell by 0.1% on the month, despite strong gains in real disposable income (+0.6% m/m) on the back of lower taxes. Indicators of housing activity were also soft. Coming on the heels of a decline in existing homes, January sales of new homes and the forward looking pending sales of existing homes also weakened. Ditto for auto sales, which edged down to 17.0 million units in February from 17.1 million in January. All in all, similar to the prior years, both consumption and GDP will start the year on a softer footing.

That being said, the slowdown will likely be short-lived. Some of the weakness in consumption is likely a pullback from the hurricane-induced ramp up at the end of 2017, and some due to “residual seasonality,” which has become apparent in recent years. Barring unexpected developments trade-side, tax cuts and a tightening labor market will prop up household income this year, supporting robust consumer spending and above-trend growth over the remainder of 2018.

All in all, the latest data does not change the calculus for the Fed with three rate hikes expected this year, however, the central bank will certainly need to keep a close watch of the economy, given rapidly evolving U.S. public policy.

Financial News for the Week of February 23, 2018

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Last A holiday-shortened trading week light in economic data left markets to focus on communications from the Federal

Reserve. - U.S. existing home sales slumped in January, beleaguered by low inventories and deteriorating affordability.

- The FOMC minutes revealed a Fed busy revising up economic projections, suggesting that further gradual policy firming

is warranted.

More Rate Hikes Incoming

Existing home sales for January revealed a market that is still beleaguered by low inventory, which exacerbates deteriorating housing affordability in many U.S. cities. January’s decline in existing home sales was broad-based, and concentrated in the larger single-family segment (Chart 1). Unsurprisingly, rising prices and borrowing costs are deterring first-time buyers from buying, as they accounted for only 29% of sales in January, down from 33% a year ago. Looking ahead, job gains and an optimistic outlook for after-tax earnings growth should support a rebound in home sales. What’s more, housing starts ticked up in January, possibly providing some respite for buyers particularly in those markets with a low supply of existing homes.

The firmer U.S. growth outlook has raised questions about how tolerant a Powell-led Fed would be of above-target inflation. Perhaps one of the most surprising admissions this week was from FRB Philadelphia President Harker, who is not a voting member of the FOMC but a contributor to the quarterly economic projections. He mentioned in a speech on Wednesday that he was comfortable penciling in just two rate hikes for this year, but may adjust if the evolution of the data requires it. This is somewhat counter to what most economic models would suggest, and even an often pessimistic market has moved to price-in about three rate hikes for 2018. Some economic forecasters have penciled in four rate hikes for 2018 after fiscal stimulus was announced.

Nonetheless, the FOMC minutes from its January meeting revealed a Fed busy revising up economic projections for the U.S. economy, and therefore confident that further gradual policy firming is warranted. While there is a lot of room for interpretation on what “further” implies, it’s safe to conclude that rates will rise this year. To be clear, we have stuck with our view from this past December that the economic outlook and balance of risks are consistent with three rate hikes by the Fed this year. However, the additional stimulus from the recently announced fiscal program pushes up our rate hikes for 2019 to three from two. This places the fed funds rate at 3.0% at the end of 2019, and about 20 basis points above the FOMC’s longer-run expectation.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of February 16, 2018

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Last week’s market sell-off came to a halt this week. U.S. equities staged a decent recovery, looking past January reports that pointed to higher-than-expected inflation and worse-than-expected retail sales.

- Price gains in the CPI report were broad-based, with core inflation rising by a hearty 0.3% m/m. Unfavorable base-year effects anchored the core pace at 1.8% in y/y terms, but this dynamic should turn more favorable in the months ahead.

- Despite a pullback in retail sales, Q1 consumer spending is still tracking a decent 2% (ann.). This pegs our tracking for Q1 GDP growth above 2%. Decent economic momentum and rising inflation bolster the case for a March hike.

Inflation Heats Up on Valentine’s Day

After the wage-data inspired sell-off, it was encouraging to see that markets took the CPI report in stride. Headline CPI jumped a hefty 0.5% m/m in January (2.1% y/y), boosted by a sharp gain in energy prices. But it wasn’t all energy, with price gains broad-based. In fact, core inflation also rose by a robust 0.3% m/m. While base-year effects anchored the core pace at 1.8% in y/y terms, this dynamic should turn more favorable in the months ahead. In fact, even small monthly gains could take core CPI above target in the coming months. Ultimately, inflation should continue to firm, with this narrative reinforced by a robust gain of 0.4% in the January producer price index, along with a higher share of small businesses raising (and planning to raise) worker compensation (Chart 2).

The boost from residential investment is also looking increasingly frail at the beginning of 2018. While housing starts picked up to just below their post-recession high in January, the concentration in lower value-added apartments and condos has reduced its overall GDP boost. Despite these developments, first quarter GDP is still tracking above 2% - a number that is enough to reduce economic slack. The consumer and housing sectors are likely to remain supported by a continually improving labor market, despite some headwinds ahead related to recent policy changes and rising rates. Housing should also benefit from tight inventories of existing homes for sale, with the near-term trend supported by permitting activity which reached a new post-recession high.

All in all, economic momentum remains decent and price pressures are rising – both themes that lend support for a March rate hike. Moreover, the risk that possible signs of ‘overheating’ may compel the Fed to step with a more rapid pace of hikes – a move that could stress vulnerabilities in sub-sectors of household and corporate credit (see report) – remains well in place.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of February 9, 2018

HIGHLIGHTS OF THE WEEK

- Major U.S. stock indices entered correction territory on Thursday but remain elevated relative to where they were a year ago. The sell-off was spurred by fears of higher interest rates, as the 10-year government bond yield hit a four-year high.

- The $300 billion increase in the spending cap over two years, laid out in the federal budget deal, could add to inflationary pressures at a time when the economy is already operating at close to full capacity, pressuring yields up further.

- Next week, investors will turn their attention to hard data, with advanced January retail sales providing an indication of whether or not first quarter growth will be affected by the residual seasonality.

Stocks Correct but Fundamentals Remain Solid

What’s important to note is that this sell-off was not triggered by weak economic data either for the U.S. or global economy. Indeed, we learned this week that the ISM non-manufacturing index showed an improvement in the services sector at the start of 2018, with rising price pressures mirroring its manufacturing counterpart (Chart 1).

As market volatility surged, Fed speakers this week appeared unconcerned about financial market developments, instead choosing to reinforce their positive economic outlook. FOMC members had previously noted that equities were overvalued and therefore showed no sign of concern over the widespread sell-off. Voting members Dudley and Williams noted in speeches that wage inflation had picked up as expected and that markets are now adjusting to global monetary policy accommodation removal. This may help calm investor fears of faster rate hikes than previously expected, with the first of three hikes this year expected in March.

Next week, investors will turn their attention to hard data. Of particular interest will be advanced January retail sales data that should provide an indication of whether or not first quarter growth will be affected by the residual seasonality that has led to first quarter weakness in three of the previous four years. Although tax cuts have only started to boost pay checks in February, we anticipate that household spending has continued to be propped up by jobs and wage gains and will contribute strongly to economic activity again in the first quarter.

Katherine Judge, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

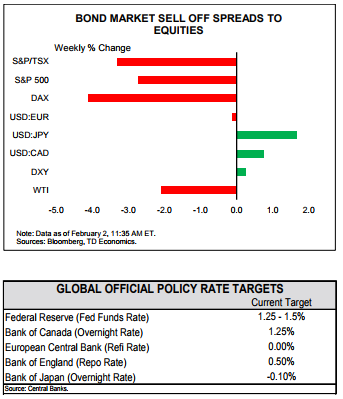

Financial News for the Week of February 2, 2018

HIGHLIGHTS OF THE WEEK

- Another week, another sell-off in the bond market. As of the time of writing the U.S. 10-year yield stood at over 2.8%, up more than 10 basis points from the end of last week.

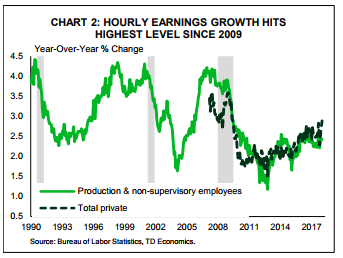

- U.S. payrolls expanded by 200k in January while the unemployment rate remained steady at 4.1%. The big story though was the acceleration in wage growth. Average hourly earnings growth hit 2.9% year-on-year, up from 2.6% and the fastest growth since 2009.

- Recent economic data cement the case for the Federal Reserve to raise interest rates at its next meeting in March. Expect at least another two rate hikes from the Powell-led Fed before the end of 2018.

Faster Growth + Inflation = Higher Bond Yields

The rise in yields is both a real growth and inflation story. On the real side, the sell-off has come as the median Bloomberg forecast for 2018 real GDP moved up 30 basis points to 2.6%, from 2.3% last October. Undoubtedly, tax cuts played a role. The biggest increases came as they were announced and then passed into law.

On the inflation side, market-based measures of inflation expectations have also moved up. The five-year forward inflation rate (an indicator of expectations for inflation five-to-ten years from now) has moved up over 20 basis points since the start of the year (Chart 1). Tax cuts are expected to push economic growth further above its trend rate and also increase the supply of Treasury securities, even as the economy approaches full employment.

The acceleration in wage growth will come as a relief to believers in the Phillips curve, giving credence to the notion that as workers become scarce, the wages offered to attract and retain them should rise. At the same time, recent data have also shown the importance of “shadow slack.” While the unemployment rate has been fairly steady, the employment to population ratio of 25 to 54 year olds has moved higher (it edged down ever so slightly in January to 79.0% from a cycle high of 79.1%). Still, its steady improvement is more consistent with the gradual rise in wage growth than the unemployment rate alone.

The increase in bond yields over the start of 2018 makes sense given these cyclical dynamics. Still, we would caution about extrapolating recent moves much further going forward. While the economic data support an ongoing expansion, the structural forces weighing on interest rates have not changed. Population aging will continue to exert downward pressure on the economy’s trend growth rate and the terminal (or neutral) level of the federal funds fate. At the same time, continued pressure on global bond yields from elevated debt levels and structural impediments to growth will keep a lid on U.S. yields.

All told, economic data and fiscal policy developments cement the case for the Federal Reserve to continue to normalize policy. Still, with a neutral rate in the neighborhood of 2.5%, three hikes in 2018 should be more than sufficient to keep a lid on inflation and allow any remaining labor market slack to be absorbed.

James Marple, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.