Financial News for the Week of February 16th, 2024

Financial News Highlights

- U.S. inflation rose more than anticipated to start the year, on a Consumer Price Index basis, largely due to greater price pressures within the services sector in financial news.

- However, retail spending surprised to the downside in January, suggesting that consumer spending may be less vigorous than the stunning pace of last year.

- A slowdown in housing starts and less optimistic small businesses also suggest that economic momentum may be cooling.

Inflation Progress Stalls and Spending Falls in January

This week saw some key data releases to help gauge the state of the U.S. economy at the start of 2024, and the likely timing of a Fed rate cut. Among them were the CPI inflation and retail sales reports for January. While inflation was higher than expected, retail spending came in notably lower. Markets reacted strongly to the inflation data with stocks falling sharply and treasury yields rising.

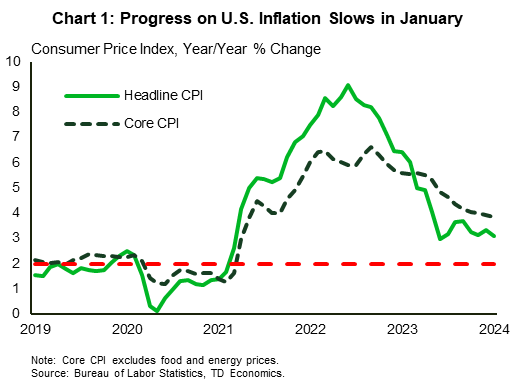

Taking a closer looker at CPI, the headline figure came in at 3.1% year-on-year (Chart 1). While this was lower than December’s 3.4%, it was higher than market expectations for 2.9%. The core measure matched December’s pace at 3.9%, but again was higher than expectations (3.7%) in financial news. The near-term movements showed that progress on the disinflation front stalled a bit, largely due to services. Both monthly headline and core inflation accelerated relative to December. Also, both the 3-month and 6-month annualized growth for core CPI accelerated, suggesting that the process to tame inflation is likely to progress in uneven spurts. The producer price index corroborated the stalled CPI signal, with the PPI rising by 0.3% m/m in January (markets expected 0.1%) relative to -0.1% in December.

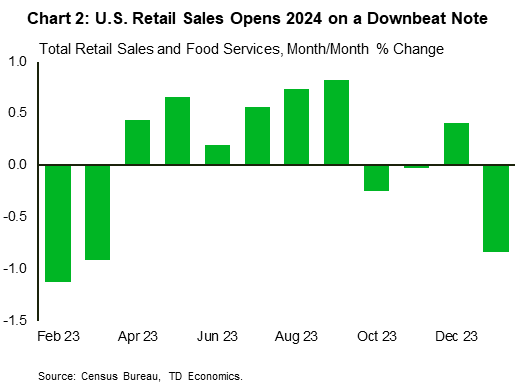

Turning to retail spending, consumers were a lot less jolly coming off the holiday season. Retail sales declined by 0.8% m/m in January (Chart 2). The sizeable decline was much larger than market expectations, however severe winter weather during January likely played a part in keeping consumers on the sidelines. Technical aspects of how the seasonally adjusted data is calculated may also have contributed to the relatively large decline. Nonetheless, the pullback suggests that consumer spending may be less of tailwind to U.S. economic resilience than it was last year.

Signals from the small business sector also suggest that economic activity might be slower in 2024. The NFIB’s small business optimism index declined to 89.9 from 91.1 in December, marking the biggest monthly decline since late-2022. On balance, small firms were generally less upbeat about their economic prospects, with the net percent of firms anticipating a better economy falling by 2 points. Given the higher exposure of small businesses to domestic economic conditions compared to larger firms, their downbeat mood points to headwinds ahead for the economy.

On the housing front, starts also disappointed expectations falling 14.8% to a five-month low (1.33 million) in January. The decline was in both the single and multi-family segments. Permits for future construction also fell on the month, implying that recovery in the housing market will be slow as buyers await lower mortgage rates.

Overall, data for January largely came in below expectations. This has left many market participants wondering what it all means for the timing of rate cuts. FOMC members have repeatedly stated that they need to see steady evidence that inflation is on a consistent path back to 2%. While the CPI and PPI data suggest that progress may be slow going for a bit, the pullback in other indicators point to an economy that is cooling. As such, Fed members may soon have the evidence that they need to begin the cutting cycle – it may just be later than markets desire.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of February 9th, 2024

Financial News Highlights

- The ISM Services index, which was on the cusp of falling into contractionary territory in December, improved notably in January, rising 2.9 points to 53.4 in financial news. The one blemish to the report was a sharp move up in the prices index.

- With little on the data front, a series of Fed speeches took center stage this week. The key message was that with the economy remaining on decent footing, the Fed could afford to show patience on rate cuts. This didn’t interrupt the uptrend in equity markets, with the S&P 500 reaching a new milestone – the 500 mark.

Fed Officials Continue to Signal Patience on Rate Cuts

Recent economic reports focusing on GDP and employment growth have driven home the point that the U.S. economy remains on solid footing. This week’s limited data provided further support to this view. In this vein, several Fed officials this week reiterated their message that there’s no rush to cut interest rates, with bond yields trending moderately higher as a result. In what appeared to be a return of ‘good news being good news again’, stock markets shrugged off the prospect of interest rates remaining higher for longer and continued to trek higher, with the S&P 500 reaching another milestone by hitting the 5000 mark.

Recent economic reports focusing on GDP and employment growth have driven home the point that the U.S. economy remains on solid footing. This week’s limited data provided further support to this view. In this vein, several Fed officials this week reiterated their message that there’s no rush to cut interest rates, with bond yields trending moderately higher as a result. In what appeared to be a return of ‘good news being good news again’, stock markets shrugged off the prospect of interest rates remaining higher for longer and continued to trek higher, with the S&P 500 reaching another milestone by hitting the 5000 mark.

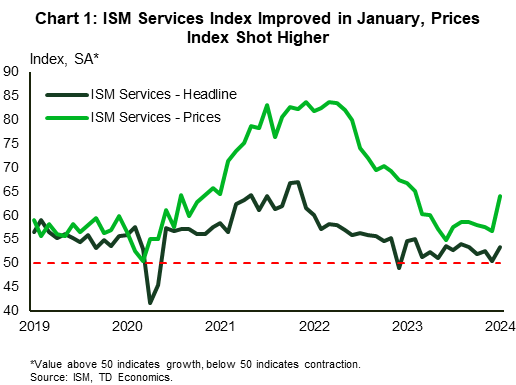

The ISM Services index, which was on the cusp of falling into contractionary territory in December, moved up notably in January, rising close to three points to 53.4. Looking under the hood, gains in three of the four main subcomponents helped lift the index higher. Of note, the employment sub-component flipped to signaling growth, as it jumped 6.7 points to 50.5. The one blemish to the report, was the fact that the prices index shot higher in January (Chart 1). A month of data does not make a trend, but the increase could signal additional inflationary pressure ahead.

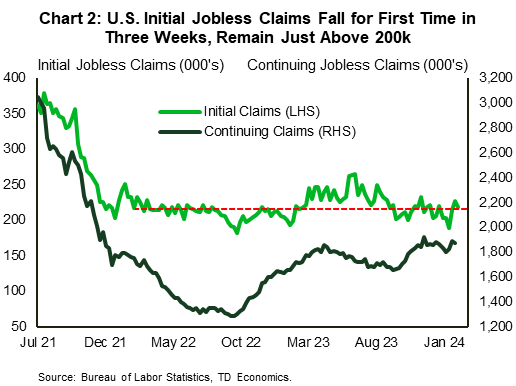

Weekly jobless claims data were consistent with a healthy labor market. Initial and continuing jobless claims continued to head lower (Chart 2). While several companies have announced plans to trim headcount this year, this is not yet being reflected in labor market data, suggesting that other businesses are growing.

With very little in the way of primary data releases, speeches from several Fed presidents and other Fed officials took center stage this week. Overall, the messaging was similar: the Fed needs to see further improvement on inflation, and with the economy on solid footing it can afford to be patient about the timing of rate cuts in financial news. Their remarks largely echoed those made by Fed Chair Powell on Sunday. Besides reiterating his message that the Fed is wary of cutting rates too soon, Powell covered a lot of ground in the ‘60 Minutes’ interview. Two comments a bit peripheral to monetary policy stood out. The first was on commercial real estate (CRE), where Powell characterized the risks as a ‘manageable’ problem for larger banks and alluded to the low probability of a repeat of the events that unfolded during the Global Financial Crisis. However, he did note that some smaller banks that have large exposures to CRE may ‘close or be merged out’.

With very little in the way of primary data releases, speeches from several Fed presidents and other Fed officials took center stage this week. Overall, the messaging was similar: the Fed needs to see further improvement on inflation, and with the economy on solid footing it can afford to be patient about the timing of rate cuts in financial news. Their remarks largely echoed those made by Fed Chair Powell on Sunday. Besides reiterating his message that the Fed is wary of cutting rates too soon, Powell covered a lot of ground in the ‘60 Minutes’ interview. Two comments a bit peripheral to monetary policy stood out. The first was on commercial real estate (CRE), where Powell characterized the risks as a ‘manageable’ problem for larger banks and alluded to the low probability of a repeat of the events that unfolded during the Global Financial Crisis. However, he did note that some smaller banks that have large exposures to CRE may ‘close or be merged out’.

The other comment from Powell that stood out was his assertion that the U.S. is on an “unsustainable” fiscal path, with debt growing faster than the economy in the long run. To this end, the Congressional Budget Office (CBO) released new 10-year projections this week, which showed that the ratio of federal publicly held debt to GDP will rise from 97.3% last year to record high of 116% by 2034.

Looking ahead to next week, January’s inflation report will take center stage. The BLS released revisions to CPI data this morning, which were relatively minor and left the year-on-year path for inflation broadly unchanged. As for January, the market consensus expects a further moderation in the core measure.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of February 2nd, 2024

Financial News Highlights

- The Federal Reserve opted to hold rates steady in their first decision of the year in order to give themselves more time to assess the sustainability of current disinflation trends in financial news.

- Employment gains in January nearly doubled expectations as strong upward revisions to December carried forward into 2024.

- U.S. Treasury markets experienced volatility this week as a decline in yields prompted by a dovish interpretation of Wednesday’s Federal Reserve decision was reversed by stronger than expected employment data on Friday.

Resilient Labor Demand and A Patient Fed

January ended with a big week for economic data, including the first Federal Reserve decision of the year and the first employment data reading in financial news. While the Fed’s statement dropped any tightening bias, Chair Powell’s press conference curtailed market hopes for a near-term pivot to less restrictive monetary policy. This saw Treasury yields fall steeply after the meeting. However, this descent was ultimately short-lived, as much stronger than expected employment data on Friday sent yields higher. At time of writing, the ten-year Treasury yield was 12 basis-points lower on the week.

January ended with a big week for economic data, including the first Federal Reserve decision of the year and the first employment data reading in financial news. While the Fed’s statement dropped any tightening bias, Chair Powell’s press conference curtailed market hopes for a near-term pivot to less restrictive monetary policy. This saw Treasury yields fall steeply after the meeting. However, this descent was ultimately short-lived, as much stronger than expected employment data on Friday sent yields higher. At time of writing, the ten-year Treasury yield was 12 basis-points lower on the week.

Overall, the messaging from the Federal Reserve on Wednesday was positive. Chair Powell stated that the committee was pleased by the progress made thus far on returning inflation to their 2% target, but noted that they would require more time to assess the sustainability of current disinflation trends (Chart 1). With economic growth accelerating last year on the back of strong consumption growth, the labor market remaining solid, and geopolitical tensions posing challenges to supply chains (and hence inflation), caution is likely wise. Chair Powell also stated that he viewed it as unlikely that the FOMC would possess the confidence to reduce interest rates by the March meeting in six week’s time.

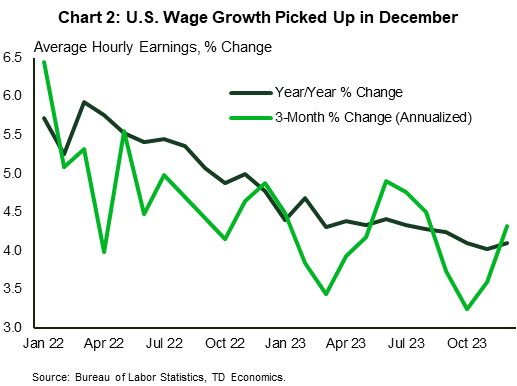

Powell’s caution was further validated when we received the January employment data on Friday. Not only did we see a very strong 353k jobs added in the first month of the year, but last year’s total job gains were also revised up to 3.1 million, well above the prior reading for 2.7 million, with much of the revised strength coming through the second half of the year (Chart 2). Furthermore, wage growth appears to be accelerating, with the three-month annualized change in average hourly wages rising to a twenty-month high in January. Although near-term strength in the labor market is expected to recede over the coming months, sustained imbalances in the labor market is a risk that the Fed is acutely aware of.

Elsewhere this week, the ISM Manufacturing Purchasing Managers’ Index (PMI) showed that industrial activity continued to contract in January, but by less than expected. Elevated interest rates continue to weigh on the sector, but demand has begun to show signs of improvement, which has stabilized aggregate production output. Forward pricing in financial markets for the eventual decline in interest rates expected this year will likely provide relief to the manufacturing sector moving forward as the demand for goods improves.

Elsewhere this week, the ISM Manufacturing Purchasing Managers’ Index (PMI) showed that industrial activity continued to contract in January, but by less than expected. Elevated interest rates continue to weigh on the sector, but demand has begun to show signs of improvement, which has stabilized aggregate production output. Forward pricing in financial markets for the eventual decline in interest rates expected this year will likely provide relief to the manufacturing sector moving forward as the demand for goods improves.

The lingering question, however, is when will the Federal Reserve begin to drawdown interest rates? Markets have broadly abandoned their hopes for a March cut after this week, with May now being the expected timeline with about 80% probability as of the time of writing. Upcoming data will likely provide greater clarity on the timing of the introduction of less restrictive monetary policy, including a 60 Minutes interview with Chair Powell on Sunday and the Federal Reserve Senior Loan Officer Opinion Survey on Monday.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of January 26th, 2024

Financial News Highlights

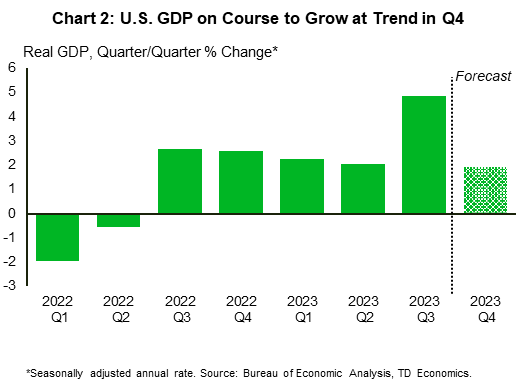

- The U.S. economy ended 2023 on a solid note, with GDP rising 3.3% quarter-over-quarter (annualized) – smashing expectations for a more moderate gain of 2% in financial news.

- The consumer remained a key factor underpinning last quarter’s strength, with spending accelerating sharply through the holiday shopping season.

- Inflation continued to drift lower in December, with the 12-month change on core PCE – the Fed’s preferred inflation measure – slipping below 3%.

The Final Approach

The latest data has shown the U.S. economy had all the markings of a soft landing as 2023 drew to a close in financial news. Economic growth held up better than expected, the labor market is coming back into better balance, and price pressures are quickly abating. Market pricing on the timing of the first Fed rate cut has seesawed between March and May in recent months, with March currently priced as a coin-toss. But with progress on the inflation front showing no signs of stalling, market sentiment remained in risk-on mode this week, with the S&P 500 edging up 1% for the week, reaching yet another all-time high. Shorter-term yields drifted a bit lower, leading to a further flattening in the yield curve. At the time of writing, the inversion of the 10Y-2Y spread had narrowed to just -20bps – well off the peak inversion of -110bps seen back in July.

The latest data has shown the U.S. economy had all the markings of a soft landing as 2023 drew to a close in financial news. Economic growth held up better than expected, the labor market is coming back into better balance, and price pressures are quickly abating. Market pricing on the timing of the first Fed rate cut has seesawed between March and May in recent months, with March currently priced as a coin-toss. But with progress on the inflation front showing no signs of stalling, market sentiment remained in risk-on mode this week, with the S&P 500 edging up 1% for the week, reaching yet another all-time high. Shorter-term yields drifted a bit lower, leading to a further flattening in the yield curve. At the time of writing, the inversion of the 10Y-2Y spread had narrowed to just -20bps – well off the peak inversion of -110bps seen back in July.

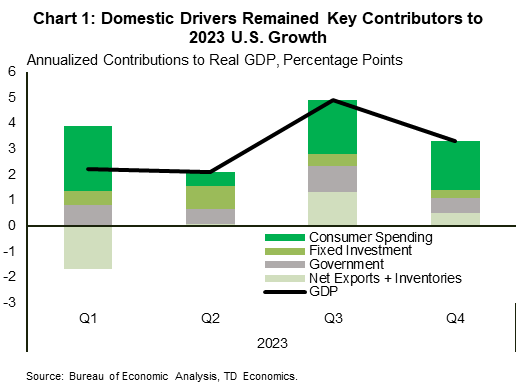

The Bureau of Economic Analysis’ advance estimate of fourth quarter real GDP came in at 3.3%, a downshift from Q3’s blistering 4.9%, but well above the consensus forecast calling for a more moderate gain of 2% (see commentary). Economic resilience remained on full display, with the consumer, private investment, and government spending accounting for the lion’s share of last quarter’s gain (Chart 1). While the rearview mirror isn’t always the best guide to the road ahead, the solid end to last year provides a more favorable starting point heading into 2024.

This is especially true for the consumer. The monthly income and spend figures for December – released a day after the GDP report – showed consumer spending accelerated sharply through the holiday shopping season. This was happening even though the tailwinds from excess savings had slowed from the gale force gust felt at the beginning of the tightening cycle to just a gentle breeze by the end of last year. At the same time, 27 million student loan borrowers were faced with the harsh reality of having to restart regular loan repayments in October following the expiration of the three-year student loan moratorium. But neither of these factors appear to have phased the consumer, as a still sturdy labor market has continued to support meaningful gains in real income and help to sustain a healthy pace of consumer spending.

This is especially true for the consumer. The monthly income and spend figures for December – released a day after the GDP report – showed consumer spending accelerated sharply through the holiday shopping season. This was happening even though the tailwinds from excess savings had slowed from the gale force gust felt at the beginning of the tightening cycle to just a gentle breeze by the end of last year. At the same time, 27 million student loan borrowers were faced with the harsh reality of having to restart regular loan repayments in October following the expiration of the three-year student loan moratorium. But neither of these factors appear to have phased the consumer, as a still sturdy labor market has continued to support meaningful gains in real income and help to sustain a healthy pace of consumer spending.

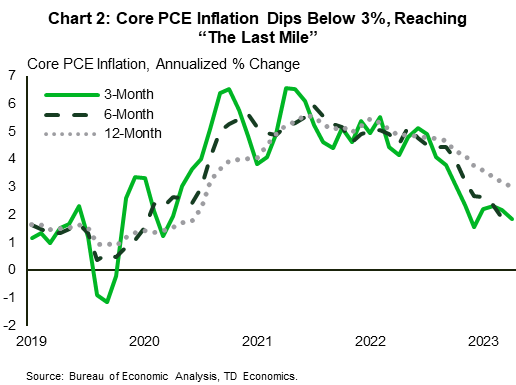

The puzzle has been on the inflation front. Despite the economy continuing to run well above its long-run potential through H2’2023, inflation has still made incredible progress. As of December, the 12-month rate of change on core PCE fell to 2.9%, while the annualized 3-and-6-month rates slipped to 1.5% and 1.9%, respectively (Chart 2). Falling goods prices and some cooling in non-housing services have both been the key contributors to the recent downward pressure on inflation.

From the Fed’s perspective, time (and the economic data) remain on their side. With the economy showing no signs of keeling over, and the labor market still relatively tight, policymakers can afford to be patient. Fed officials will want to see at least a few more ‘soft’ readings on inflation and a bit more easing in the labor market before pulling the trigger on rate cuts.

Thomas Feltmate, Director & Senior Economist | 416- 944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of January 19th, 2024

Financial News Highlights

- Higher than expected retail sales in December suggests that consumer spending remained resilient to end the year in financial news.

- Several Fed governors sought to push back against market expectations for swift and significant rate cuts.

- The housing market ended 2023 on a sour note, with both new home construction and existing home sales falling in December.

A Resilient Consumer Dims Hopes for an Early Rate Cut

Just when you think the U.S. consumer might yield to mounting pressures currently buffeting their balance sheets, they surprise by closing out 2023 on a retail spending binge. The increased spending kept the economy on firm ground and suggests a solid hand off heading into the new year. It also caused investors to pare back expectations for a March rate cut and pushed U.S. Treasury yields higher.

Just when you think the U.S. consumer might yield to mounting pressures currently buffeting their balance sheets, they surprise by closing out 2023 on a retail spending binge. The increased spending kept the economy on firm ground and suggests a solid hand off heading into the new year. It also caused investors to pare back expectations for a March rate cut and pushed U.S. Treasury yields higher.

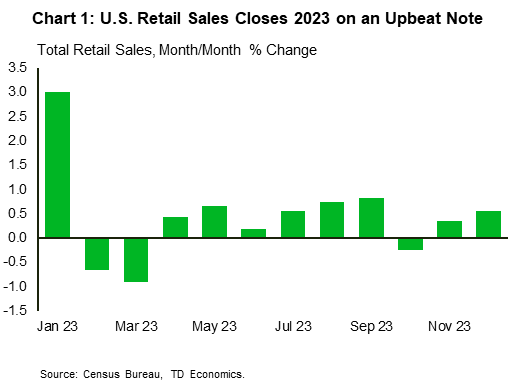

Retail sales rose 0.6% month-on-month in December, following a 0.3% gain in November (Chart 1). The breadth of the increase was also noteworthy with 9 out of the 13 categories recording gains. The “control group” which factors into the calculation of personal consumption expenditure rose an even more impressive 0.8% on the month in financial news. The stellar number suggests that consumer spending grew at a healthy clip of around 2.5% (annualized) in Q4.

The stronger than expected retail sales report has resulted in upward revisions to expectations of Q4 GDP growth. After the report, the Atlanta Fed’s GDPNow growth estimate rose to 2.4% (from 2.2%), while our own estimate currently sits at 1.9%. (Chart 2). We won’t have to wait long to know for sure though, as the BEA is set to release the advance estimate of Q4 GDP next Thursday. Given expectations for the print to be relatively strong, there is even less pressure on the Fed to entertain rate cuts over the coming months.

The slew of Fed speakers making the rounds this week were quick to reinforce that point. “With economic activity and labor markets in good shape and inflation coming down gradually” Governor Waller sees “no reason to move as quickly or cut as rapidly as in the past.” He used terms such as “carefully calibrated and not rushed” and “lowered methodically and carefully” to push back against market expectations of sizeable cuts this year. Atlanta Fed President Bostic was on a similar page. He noted that rates could be cut earlier than Q3, “but the evidence would need to be convincing.” What’s more, he urged caution given the current uncertain environment (domestic budget battles, global conflict, elections etc.), which could have unpredictable economic impacts and re-ignite inflation pressures.

Turning to the housing sector, reports out this week showed housing activity ended a tumultuous year on a sour note. Housing starts fell in December reversing a portion of November’s gain, while existing home sales declined to a 14-year low. A dearth of available inventory and historically poor affordability are to blame for last year’s weak showing. However, with mortgage rates having come down by over 100 basis points from its mid-October peak, we’ve likely reached the bottom and should see some uptick in sales activity through 2024.

Turning to the housing sector, reports out this week showed housing activity ended a tumultuous year on a sour note. Housing starts fell in December reversing a portion of November’s gain, while existing home sales declined to a 14-year low. A dearth of available inventory and historically poor affordability are to blame for last year’s weak showing. However, with mortgage rates having come down by over 100 basis points from its mid-October peak, we’ve likely reached the bottom and should see some uptick in sales activity through 2024.

Ultimately, the timing and pace of rate cuts will depend on the strength of economic growth and inflationary pressures. This week’s data indicate that economic conditions are currently resilient. Last week’s CPI print shows there is still work to be done on the inflation front. The combination means that a policy pivot to rate cuts is unlikely to be top of mind for Fed officials just yet.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of January 12th, 2024

Financial News Highlights

- An upside inflation surprise didn’t do much to move markets, as the details of the report fell in line with expectations in financial news.

- The focus remains firmly on the services sector, where housing costs continue to prop up price growth.

- Looking forward, the Fed will need to see more consistent evidence of disinflation – likely delaying any policy changes to mid-year.

The Long and Bumpy Road

Taming inflation is never easy, and usually proceeds in fits and starts in financial news. So, given the experience of the past year, this week’s hotter-than-expected print to consumer price index (CPI) inflation doesn’t come as all that much of a surprise. Indeed, the details of the report left room for optimism and meant that markets brushed off the surprise – leaving ten-year U.S. treasury yields virtually unchanged on the news. The positive developments under the hood (so to speak) fell in line with consensus expectations and meant that the focus could be kept firmly on the timing of possible Fed cuts.

Taming inflation is never easy, and usually proceeds in fits and starts in financial news. So, given the experience of the past year, this week’s hotter-than-expected print to consumer price index (CPI) inflation doesn’t come as all that much of a surprise. Indeed, the details of the report left room for optimism and meant that markets brushed off the surprise – leaving ten-year U.S. treasury yields virtually unchanged on the news. The positive developments under the hood (so to speak) fell in line with consensus expectations and meant that the focus could be kept firmly on the timing of possible Fed cuts.

Headline CPI inflation rose 0.3% month-on-month (m/m), taking the annual reading for December to 3.4%. While the print did exceed market expectations, it was the more closely watched core measure that drove the muted market response. The price index excluding food and energy matched the headline gain at +0.3% m/m – a pace it has logged in four of the past five months. This is the interesting bit, on a three-month annualized basis core CPI inflation is running at 3.3%, roughly unchanged since October and still clear of the Fed’s target.

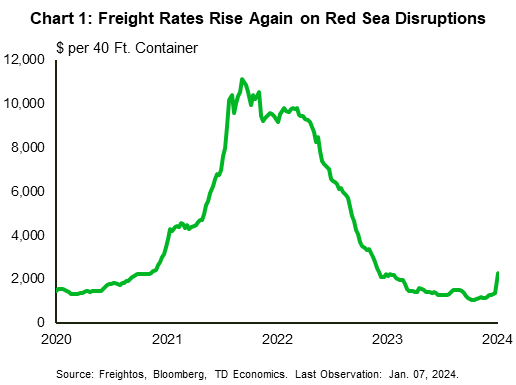

The stickiness in the core measure is slightly concerning, particularly as core goods prices remained flat, snapping a six-month run of price declines. Moreover, there is some near-term upside risk to goods prices as attacks on ships in the Red Sea affecting access to the Suez Canal have lead to a jump in freight costs (Chart 1). Despite this, what the pause in goods price deflation laid bare was the ongoing strength in services price gains.

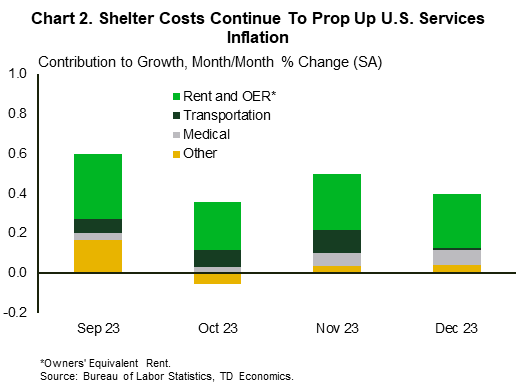

Core services prices were up 0.4% m/m in December. Moreover, the strong price gains have been persistent, with the three-month and six-month (annualized) rates of core services inflation at 5.1% and 5.2%, respectively. Yet, while these figures are significantly higher than the Fed would feel comfortable with, there are reasons to believe conditions are improving. Currently, the largest contributing factor to services inflation is the shelter component (Chart 2). On this front relief is expected as increases in observed rents (which tend to lead the measure in the CPI report)  have moderated sharply in recent months – a dynamic that is still gradually working through to the shelter component of CPI. Moreover, the slowdown in home price appreciation through early-2023 also continues to gradually work its way into the CPI.

have moderated sharply in recent months – a dynamic that is still gradually working through to the shelter component of CPI. Moreover, the slowdown in home price appreciation through early-2023 also continues to gradually work its way into the CPI.

The return to two percent inflation continues to be bumpy, but progress has been tangible and signs suggest that the Fed continues to be on course. After a few months of solid progress, optimism had begun to emerge that cuts might come sooner rather than later. However, price pressures remain sticky, and the economy continues to outperform. December job growth was above trend, and the Atlanta Fed Nowcast is expecting GDP growth of over 2% (annualized) in the fourth quarter or 2023.

A packed slate of Fed speakers is on tap for next week, and should hopefully give some additional insight into how they view the recent data. However, given this week’s developments, it will likely be mid-year before officials have sufficient evidence signs that they can begin loosening their policy stance.

Andrew Hencic, Senior Economist | 416-944-530

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of January 5th, 2024

Financial News Highlights

- Minutes from the December FOMC meeting confirmed that monetary policy was “likely at or near its peak” for this tightening cycle, but showed no meaningful discussion on rate cuts in financial news.

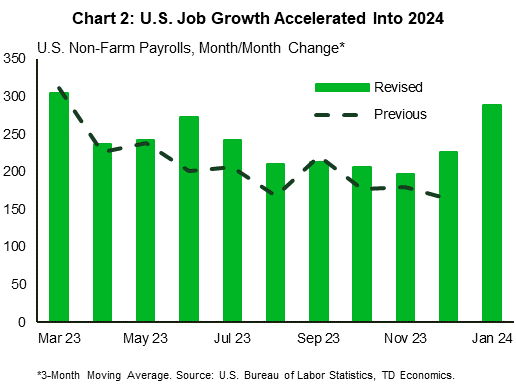

- The U.S. economy added a better-than-expected 216k jobs in December, but downward revisions to the prior two months kept a cooling trend intact. The unemployment rate held steady at 3.7%, while wage growth accelerated slightly.

- The ISM surveys overall signaled softness. Manufacturing remained in contractionary territory in December, albeit slightly less negative, while activity in the services sector slowed but remained in expansionary territory.

Rate Cut Expectations Ease Slightly at the Start of 2024

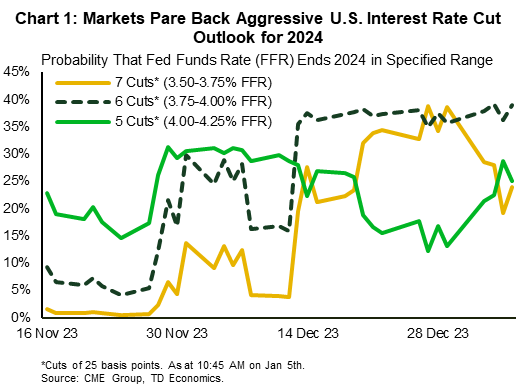

After a festive December where a sharp pullback in long-term yields sent risk assets higher, markets have gotten off to a much more sober start in 2024. Investors have seemingly adjusted their New Year’s resolutions, resulting in more moderate expectations for interest rate cuts this year. Cuts totaling 150 basis points by the end of 2024 remains the dominant scenario. The probability for more aggressive policy loosening (i.e., 7 cuts) has fallen sharply, while the probability of slightly less aggressive loosening (i.e., 5 cuts) has increased (Chart 1). In line with these developments, the 10-year Treasury yield has recouped some of the lost ground, rising from 3.8% at the end of December to near 4% recently, and equity markets have pared back year-end gains, with the S&P 500 down 1.6% from its recent peak.

After a festive December where a sharp pullback in long-term yields sent risk assets higher, markets have gotten off to a much more sober start in 2024. Investors have seemingly adjusted their New Year’s resolutions, resulting in more moderate expectations for interest rate cuts this year. Cuts totaling 150 basis points by the end of 2024 remains the dominant scenario. The probability for more aggressive policy loosening (i.e., 7 cuts) has fallen sharply, while the probability of slightly less aggressive loosening (i.e., 5 cuts) has increased (Chart 1). In line with these developments, the 10-year Treasury yield has recouped some of the lost ground, rising from 3.8% at the end of December to near 4% recently, and equity markets have pared back year-end gains, with the S&P 500 down 1.6% from its recent peak.

The minutes from the December FOMC meeting contributed to the softening in expectations for interest rate cuts this week. After the Fed signaled that the policy rate would head lower in 2024, there was an anticipation that rate cut talk may have featured heavily at the last meeting. Committee participants confirmed that the policy rate was “likely at or near its peak for this tightening cycle”, given the reduction in inflation in 2023 and “growing signs of demand and supply coming into better balance in product and labor markets”. But, meaningful debate on rate cuts was missing. Instead, the discussion was somewhat more balanced, touching on both the risks of maintaining rates in a restrictive position for too long and the risks of prematurely easing policy. Participants noted that their outlooks were associated with an “unusually elevated” degree of uncertainty and stressed the importance of maintaining a data-dependent approach to setting monetary policy.

Speaking of data, this morning’s payrolls report showed that hiring unexpectedly accelerated in December, with the U.S. economy adding 216 thousand jobs (see commentary) in financial news. However, a downward revision of 71 thousand jobs to the prior two months limits some of the enthusiasm of this upward surprise. On a three-month moving average basis, hiring is still trending lower, which suggests that restrictive monetary policy continues to work as intended, cooling labor demand. Nonetheless, other aspects of the report still play in favor of showing some caution on easing monetary policy. The unemployment rate held steady at 3.7%. With the labor market still tight, wage growth gained some ground in December (Chart 2). A recent pullback in the job ‘quits’ rate – a leading indicator of labor costs – suggests that wage growth is nonetheless poised to cool ahead.

Speaking of data, this morning’s payrolls report showed that hiring unexpectedly accelerated in December, with the U.S. economy adding 216 thousand jobs (see commentary) in financial news. However, a downward revision of 71 thousand jobs to the prior two months limits some of the enthusiasm of this upward surprise. On a three-month moving average basis, hiring is still trending lower, which suggests that restrictive monetary policy continues to work as intended, cooling labor demand. Nonetheless, other aspects of the report still play in favor of showing some caution on easing monetary policy. The unemployment rate held steady at 3.7%. With the labor market still tight, wage growth gained some ground in December (Chart 2). A recent pullback in the job ‘quits’ rate – a leading indicator of labor costs – suggests that wage growth is nonetheless poised to cool ahead.

Other data reports were a mixed bag. Consumers increased vehicle purchases in December (up 3.2% to 15.8 million annualized), although this appears to be partially related to the return of year-end discounts (see here). Meanwhile, the ISM indexes signaled softness. There was a slowdown in the expansion of the services side of the economy, and the manufacturing sector remained in contraction for the 14th month in row in December, albeit slightly less so on the month.

All factors considered, a loosening in monetary policy is coming, but we anticipate the Fed will show a bit more caution, with the first rate cut not likely to come until the second half of the year.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of December 8th, 2023

Financial News Highlights

- The U.S. economy continued to add jobs in November, while the unemployment rate dipped, and wage growth held steady in financial news.

- The JOLTS data also showed a narrowing gap between labor demand and supply, which suggests that activity in the labor market continues to normalize and come into better balance.

- The ISM services index showed that the services sector managed to maintain a modest expansion in November. Nonetheless, the trend continues to show that services sector growth is slowing.

The (Re)balancing Act Continues

The major focus on the U.S. economic data calendar this week was the labor market, with the two main reports showing labor demand and supply are gradually coming back into better balance. The service sector also continued to expand while U.S Treasury yields continued to push further below their mid-October highs.

The major focus on the U.S. economic data calendar this week was the labor market, with the two main reports showing labor demand and supply are gradually coming back into better balance. The service sector also continued to expand while U.S Treasury yields continued to push further below their mid-October highs.

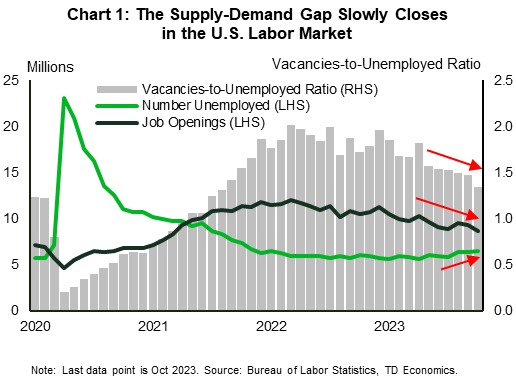

First up, the more backward-looking JOLTS data showed that the number of job openings in October fell by more than expected and slipped to the lowest level since March 2021. Although still higher than before the pandemic, at 8.7 million, openings are down notably from a record high of 12 million in March 2022. To be sure, there were still plenty of jobs available relative to the more than 6.5 million unemployed job seekers in October. However, the gap has narrowed with the vacancies-to-unemployed ratio falling to 1.34 from 1.47 in September — its lowest reading since August 2021. Other elements of the report also supported a softening labor market narrative – lay-offs held steady at 1.6 million and the quit rate remained unchanged at 2.3% for the fourth consecutive month (in-line with where it was immediately prior to the pandemic). Further evidence of labor demand cooling has been seen in continuing jobless claims, which have ticked higher over the past month, suggesting workers are finding it a bit harder to find a new job.

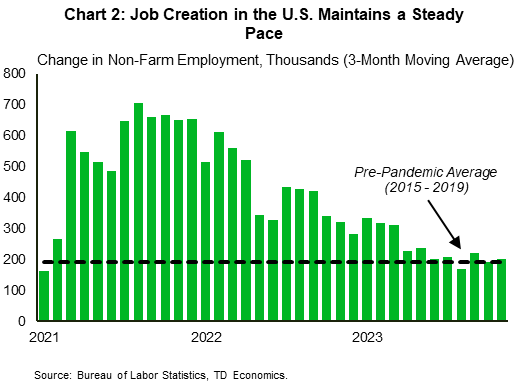

The signal from the more recent November payrolls report was generally in line with the JOLTS data in financial news. The economy added 199k jobs in November, largely in line with its pre-pandemic average and up from 150k the previous month (Chart 2). The unemployment rate dipped to 3.7% as the labor force participation rate edged higher. Annual wage growth held constant at 4.0%, down from the highs seen last year, but still above what’s consistent with 2% inflation.

The signal from the more recent November payrolls report was generally in line with the JOLTS data in financial news. The economy added 199k jobs in November, largely in line with its pre-pandemic average and up from 150k the previous month (Chart 2). The unemployment rate dipped to 3.7% as the labor force participation rate edged higher. Annual wage growth held constant at 4.0%, down from the highs seen last year, but still above what’s consistent with 2% inflation.

The recent cooling in the labor market alongside easing inflationary pressures has pushed term yields notably lower as market participants have pulled forward the timing of when the Fed could begin cutting rates. Since their recent peak in October, yields have retreated closer to levels seen in September. Given the resilience of the economy thus far however, a further easing in financial conditions could provide a stimulus to demand that could reignite price pressures and prompt further Fed action contrary to market expectations.

On the production side, the services sector of the economy managed to eke out a continued expansion with the ISM services index rising modestly to 52.7 in November. The lackluster growth suggests that activity in the sector is slowing down, which could help to keep a lid on service sector inflation and help wage inflation continue to cool.

The resilient labor market that supported an unexpectedly strong U.S. economy this year is showing signs of cooling. The latest signs that it is coming back into greater balance will be welcomed at the Fed, which will be meeting next week for their final policy decision of the year. When Fed Chair Powell noted that the central bank can “let the data reveal the appropriate path”, this week’s data points to a steady course. All eyes will be on next week’s CPI release to see if it corroborates that plan of action.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of December 1st, 2023

Financial News Highlights

- A second reading on U.S. GDP showed that the economy expanded by an even more impressive 5.2% (annualized) last quarter, a 0.3 percentage point upgrade from the initial reading in financial news. Government spending and business investment were revised up, but consumer spending was revised down slightly.

- October’s real consumer spending data showed that growth eased at the start of the fourth quarter. Core PCE inflation, the Fed’s preferred measure, also cooled to 3.5% year-on-year from 3.7% in September.

- The National Association of Realtors pending home sales index fell to a record low in October.

Moving Toward Target

The U.S. economy grew at an even better pace than initially reported in the third quarter. But, a moderation in consumer spending in October coupled with some progress on the inflation front, reinforced market expectations that the Fed has likely reached the end of its tightening cycle. That said, Fed speak out this week was somewhat mixed, with some suggesting that today’s policy rate is sufficiently restrictive while others still feel it’s too early to call it quits. In his speech on Friday, Chair Powell called talk of cutting rates ‘premature’.

The U.S. economy grew at an even better pace than initially reported in the third quarter. But, a moderation in consumer spending in October coupled with some progress on the inflation front, reinforced market expectations that the Fed has likely reached the end of its tightening cycle. That said, Fed speak out this week was somewhat mixed, with some suggesting that today’s policy rate is sufficiently restrictive while others still feel it’s too early to call it quits. In his speech on Friday, Chair Powell called talk of cutting rates ‘premature’.

The second reading on U.S. GDP showed that the economy grew by 5.2% (annualized) last quarter, an upgrade of 0.3 percentage points from the initial reading. The upward revision reflects improvements in government spending and fixed investment. One major category going against the grain was consumer spending, which was revised slightly lower to 3.6% from 4% previously. Stepping into the fourth quarter, the personal income and outlays report, added another layer of moderation for the consumer. Nominal spending rose 0.2% month-over-month (m/m) in October, a deceleration from 0.7% in September. The spending slowdown was less pronounced on an inflation-adjusted basis, with growth easing to 0.2% from 0.3% in the month prior.

Given a reduction in credit availability and the drawdown of pandemic era ‘excess savings’, the American consumer will have to rely more closely on income growth to fund its spending (see here). As such, any softness on the labor market should filter through to weaker spending. Peeking into the labor market, continuing jobless claims rose to 1.93 million in mid-November. This is the highest level since late 2021 and an added sign that the labor market is gradually cooling. Overall, we expect consumer spending to remain buoyant over the holiday period, but the momentum is likely to fade, with consumption growth likely to slow to around 2% this quarter.

Given a reduction in credit availability and the drawdown of pandemic era ‘excess savings’, the American consumer will have to rely more closely on income growth to fund its spending (see here). As such, any softness on the labor market should filter through to weaker spending. Peeking into the labor market, continuing jobless claims rose to 1.93 million in mid-November. This is the highest level since late 2021 and an added sign that the labor market is gradually cooling. Overall, we expect consumer spending to remain buoyant over the holiday period, but the momentum is likely to fade, with consumption growth likely to slow to around 2% this quarter.

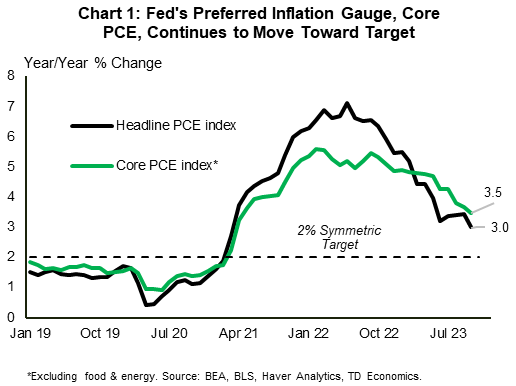

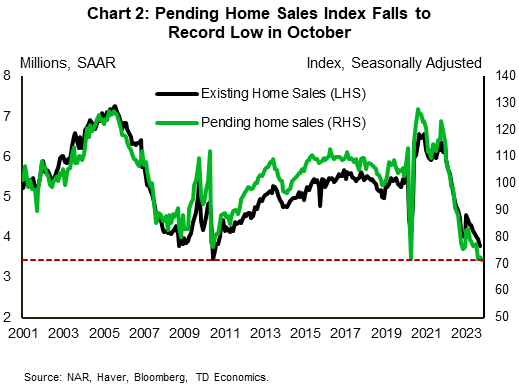

The monthly personal income and outlays report also carried some good news on the inflation front. The highlight was a continued deceleration in core PCE – the Fed’s preferred inflation gauge – which slowed to 3.5% year-on-year in October from 3.7% in the month prior (Chart 1) in financial news. Interest rates have eased alongside this continued progress toward the Fed’s 2% target, and so have mortgage rates. The 30-year mortgage rate is currently hovering near 7.2% – some 80 basis points lower than the 8% peak in mid-October. This pullback appears to be providing some relief on housing, with mortgage purchase applications ticking higher for the fourth week in a row last week. But, the impact of interest rates tends to be felt with a lag, so this will take some time to be manifested in sales activity. To that end, pending home sales fell to an all-time low in October, indicating that things are likely to get worse before they get better (Chart 2).

All in all, higher interest rates are working as intended with inflation gradually easing toward target, but the Fed can’t let its guard down prematurely and is likely to maintain a hawkish tone until it is convinced that the inflation is decisively moving back towards 2%.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Featured Article: Don't Miss Out on Your 2023 Tax Breaks

Don't Miss Out on Your 2023 Tax Breaks

It’s time to shake a leg on year-end tax planning.

As usual, most moves affecting 2023 taxes must be completed before Jan. 1, just weeks away. Here are areas to tackle now—and a few that can slide.

Check withholding and estimated taxes

On Oct. 1, the penalty on tax underpayments rose to a stiff 8% and may hold there. This is worth avoiding, so review your paycheck withholding or quarterly estimated taxes—especially if your income has been uneven or included a windfall like a bonus.

To avoid underpayment penalties, most filers must pay 90% of their taxes long before the April deadline. The due date is Dec. 31, 2023 for employees and Jan. 16, 2024 for those making quarterly payments. The IRS has posted a calculator to help employees figure the right amounts.

Need to pay more? Try to fill the gap by withholding either from your paycheck or your taxable IRA payout. Under little-known tax rules, these moves can wipe out or reduce underpayment penalties, even if the catch-up payment is made late in the year.

Taxpayers can also bypass penalties by paying an amount equal to either 100% or 110% of their 2022 taxes, if they do it on time. (IRS.gov/directpay is a useful option.) In most cases, the 100% threshold applies to filers with adjusted gross income of $150,000 or less, while the 110% threshold applies to those with more.

Standard deduction or itemized?

Filers can reduce their taxable income either by subtracting one overall amount—the standard deduction—or by listing itemized deductions for mortgage interest, state and local taxes, charitable donations, medical expenses and others on Schedule A. Before the 2017 tax overhaul nearly doubled the standard deduction, about 30% of filers itemized.

Now, less than 10% do.

The standard deduction is $27,700 for married joint filers and $13,850 for singles this year, and next year that rises to $29,200 and $14,600 respectively. Filers age 65 and older each get at least $1,500 more.

Some taxpayers will want to switch back and forth from standard to itemized to maximize overall deductions. If so, it can make sense to “bunch” deductions either by accelerating or delaying them into years when you’ll itemize.

Often the best candidates for bunching are charitable donations (see below), but don’t overlook unreimbursed medical expenses. They’re deductible above 7.5% of adjusted gross income, a hard threshold to surmount. For those who do, a wide variety of expenses can count, including Medicare premiums, contact-lens solution and home modifications like an elevator or even a swimming pool.

Optimize charitable donations

Givers should focus on three key tax breaks for donations, as there’s no $300 or $600 deduction for non-itemizers this year.

One is to bunch gifts and itemize deductions in some years but not others. Example: Margaret is a single filer, age 67, who gives $5,000 a year to charity. But that and her other deductions will come to less than her 2023 standard deduction. By making two years of donations either this year or next, Margaret could take the standard deduction one year and itemize for the other to maximize overall tax breaks.

Another is to donate appreciated investments held longer than a year. Donors can often take a deduction for the full fair-market value of an asset without owing tax on its growth—although conditions and limits apply.

Donors who bunch deductions or give appreciated assets may want to use a donor-advised fund, or DAF. These enable the giver to take an upfront deduction and wait till later to direct donations to specific charities. Such funds are often convenient but have fees.

Finally, taxpayers age 70 ½ and older have a highly useful option: qualified charitable distributions, or QCDs, of traditional IRA assets. Each IRA owner can transfer up to $100,000 this year ($105,000 in 2024) directly to one or more charities. The donation can count toward their required minimum payout, if any.

Donors using QCDs don’t get a deduction, but the gifts don’t count as taxable income, either. That can help reduce income-adjusted Medicare premiums and other taxes—and still allow the donor to take the standard deduction.

Watch for large mutual-fund payouts

Investors holding mutual funds in taxable accounts should check whether their funds will make large capital-gains payouts for 2023.

Mark Wilson, a financial adviser who tracks large payouts at CapGainsValet.com, expects large payouts from fewer than 100 funds this year. That compares with about 360 last year, when markets tumbled and some managers sold holdings to meet redemptions.

Still, he says that so far five funds have announced payouts greater than 30% of net asset value, including the BNY Mellon U.S. Equity Fund. Another dozen will be making payouts greater than 20% of assets, including J.P. Morgan’s Tax Aware Equity fund and the DWS Equity 500 Index fund.

Usually investors have time after the announcement to make strategic moves before the payout. These include harvesting losses elsewhere to offset the gains or donating the holding to charity for a deduction.

Plan electric-vehicle purchases

There are lots of factors to consider. One is that buyers who wait until 2024 can receive a tax credit up to $7,500 at purchase, while those who buy this year can’t claim the credit until they file 2023 tax returns.

On the other hand, the list of eligible vehicles could shrink in 2024 after the IRS issues guidance on certain provisions. One of them excludes vehicles with battery components from certain countries, perhaps including China. Income limits of $150,000 for singles and $300,000 for couples filing jointly could also matter, so check the details if you’re close.

Note that many of these constraints don’t apply to leases, which have become more popular as a result. Due to excess inventory, many automakers and dealers are also discounting prices.

Take required IRA distributions

Owners of traditional IRAs born in 1950 or earlier typically must take required withdrawals for 2023 by Dec. 31, 2023. The payouts are based on the account value as of Dec. 31, 2022.

Many heirs of traditional IRAs whose owners died in 2020 or later would normally have to take a required withdrawal this year. However, the IRS is allowing these heirs to skip it for 2023.

Know what can wait

Contributions to traditional IRAs, Roth IRAs, and health-savings accounts for 2023 can typically be made until the tax deadline of April 15, 2024 (April 17 in Maine and Massachusetts). Some self-employed filers can make 2023 contributions to Solo 401(k)s until Oct. 15, 2024.

Write to Laura Saunders at Laura.Saunders@wsj.com

To see more fantastic articles like this one, please see here.