Financial News for the Week of November 24th, 2023

Financial News Highlights

- Minutes from the Federal Open Market Committee (FOMC) meeting reinforced the Fed’s messaging that patience is warranted while the disinflation process is working in financial news.

- Existing home sales sag as high prices and financing costs make homes their least affordable since the mid-80s.

- All eyes will be on next week’s personal income and spending report for October, watching for further signs of slowing demand growth.

Looking for Signs of Slowing

U.S. Treasury yields extended their decline this week, with the 10-year now hovering around 4.5% in financial news. As economic data have decelerated, expectations for policy easing next year have helped markets continue to rally – up about 1% this week. This week, minutes from the Federal Open Market Committee (FOMC) meeting reinforced the Fed’s messaging that patience is warranted while the disinflation process is working, while housing starts data showcased that higher interest rates are working to cool the economy. Coming off the Thanksgiving holiday, all eyes are now tuned to next week’s consumer spending report for October for signs of slowing economic momentum and cooling inflation.

U.S. Treasury yields extended their decline this week, with the 10-year now hovering around 4.5% in financial news. As economic data have decelerated, expectations for policy easing next year have helped markets continue to rally – up about 1% this week. This week, minutes from the Federal Open Market Committee (FOMC) meeting reinforced the Fed’s messaging that patience is warranted while the disinflation process is working, while housing starts data showcased that higher interest rates are working to cool the economy. Coming off the Thanksgiving holiday, all eyes are now tuned to next week’s consumer spending report for October for signs of slowing economic momentum and cooling inflation.

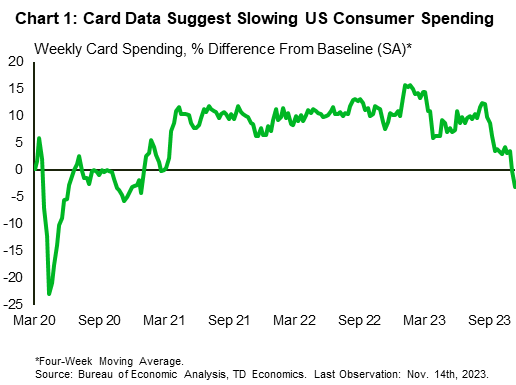

The minutes from the FOMC’s last meeting essentially backed up the hawkish signals the Fed has been putting out while they hold the policy rate fixed. Committee members noted how the economy stayed unexpectedly hot through the third quarter of the year, powered by relentless consumer spending. With the supply shocks from the pandemic and the war in Ukraine still gradually resolving themselves, persistently strong aggregate demand helped keep pressure on prices through much of the year. However, committee members judged that this may be starting to shift (Chart 1). This has left the Fed squarely focused on cooling demand to tame inflation pressures. On this front, the Fed maintains that restrictive policy rates are working, and are at an appropriate level. Moreover, with members agreeing that there needs to be clear evidence that inflation is on a solid trajectory back to 2% before easing, and upside risks ever-present, officials will be keenly looking out for any signs that more needs to be done to restore the supply-demand balance.

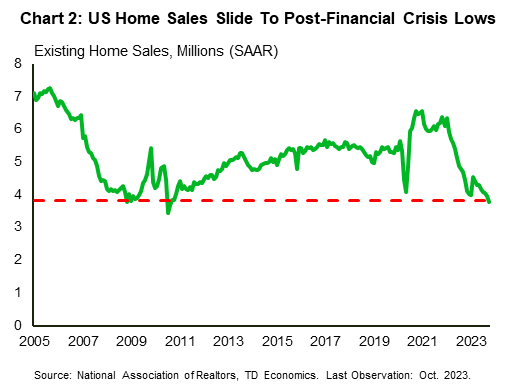

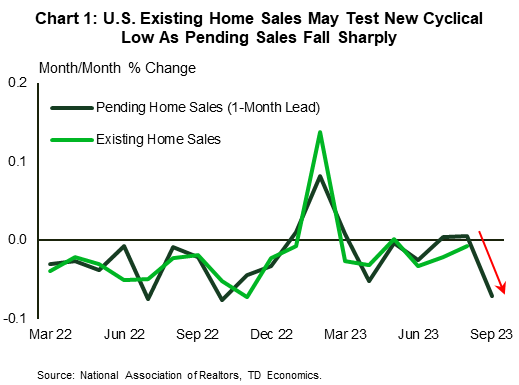

On the demand side, the housing market is clearly responding to the surge in borrowing costs since the summer, with existing home sales in October falling to their lowest level since 2010 (Chart 2). However, conditions today are drastically different than in 2010, when the housing bubble burst leading to an abundance of supply, and a tepid recovery after the Global Financial Crisis saw a drastic improvement in affordability. Today, affordability is weighing on activity as high prices and financing costs make homes their least affordable since the mid-80s. With the Fed poised to keep rates at multi-decade highs, a quick turnaround is unlikely.

On the demand side, the housing market is clearly responding to the surge in borrowing costs since the summer, with existing home sales in October falling to their lowest level since 2010 (Chart 2). However, conditions today are drastically different than in 2010, when the housing bubble burst leading to an abundance of supply, and a tepid recovery after the Global Financial Crisis saw a drastic improvement in affordability. Today, affordability is weighing on activity as high prices and financing costs make homes their least affordable since the mid-80s. With the Fed poised to keep rates at multi-decade highs, a quick turnaround is unlikely.

However, with healthy economic momentum through the third quarter all eyes will be on next week’s consumer income and spending report for signs of slowing demand growth. With payrolls growth slowing in October, consensus expectations are for real consumer spending growth to slow from 0.4% month-on-month (m/m) in September to 0.1% in October. The Fed’s preferred inflation measure, the core PCE deflator, is expected to follow suit, slowing to 0.2% m/m from 0.4% in September.

Of course, given the experience of the past year, the risks run to the upside, and that the American consumer will once again prove to be more resilient than expected. In that event, the Fed has told us it stands ready to tighten policy further if they assess that data show, “progress toward the Committee’s inflation objective was insufficient.”

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of November 17th, 2023

Financial News Highlights

- Consumer Price Index (CPI) inflation printed lower than expected in October, fueling a rally in equities and a sharp pullback in longer-term Treasury yields in financial news.

- A government shutdown was averted this week, as Congress passed another short-term funding bill that maintains current spending levels through mid-January.

- Retail sales data showed a moderation in spending activity in October, while higher frequency credit card spend data suggests the weakness has extended into November.

Extended Fed Pause Looking Increasingly Likely

Market sentiment was decisively in the risk-on camp this week, as a softer reading on October inflation and signs of slowing consumer spending fueled expectations of a longer Fed pause. Also providing a lift to equities was Congress acting to pass yet another short-term funding bill that avoids an immediate government shutdown by extending current levels of spending through mid-January. The S&P 500 is shaping up to end the week 2% higher – extending its winning streak to three-consecutive weeks. Longer-term yields traded lower, with the 10-year Treasury ending the week down 18 basis-points to 4.43%.

Market sentiment was decisively in the risk-on camp this week, as a softer reading on October inflation and signs of slowing consumer spending fueled expectations of a longer Fed pause. Also providing a lift to equities was Congress acting to pass yet another short-term funding bill that avoids an immediate government shutdown by extending current levels of spending through mid-January. The S&P 500 is shaping up to end the week 2% higher – extending its winning streak to three-consecutive weeks. Longer-term yields traded lower, with the 10-year Treasury ending the week down 18 basis-points to 4.43%.

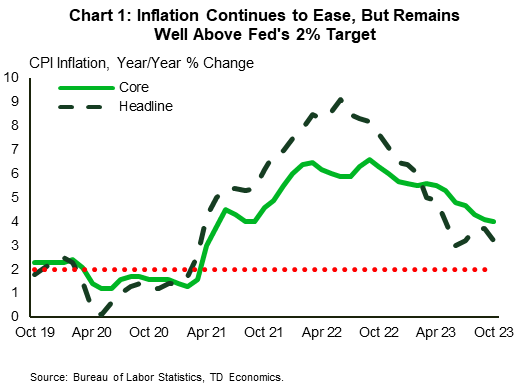

Turning to the Consumer Price Index (CPI) report, both headline and core inflation came in below market expectations. Falling energy and goods prices, a further easing on housing costs and some deceleration in the ‘supercore’ measure all contributed to last month’s softer print. On a twelve-month basis, core inflation is down 2.6 percentage points from last year’s high but, at 4%, remains well above the Fed’s 2% inflation target (Chart 1) in financial news. As noted in our commentary, the challenge for the Fed going forward is that much of the low hanging fruit on the dis-inflation front has now been picked. With supply-chain issues largely resolved, it is unlikely that falling goods prices will continue to exert as much of a drag on inflation going forward. Ultimately, this means a more pronounced slowing in consumer spending will be required to sustain continued downward pressure on inflation.

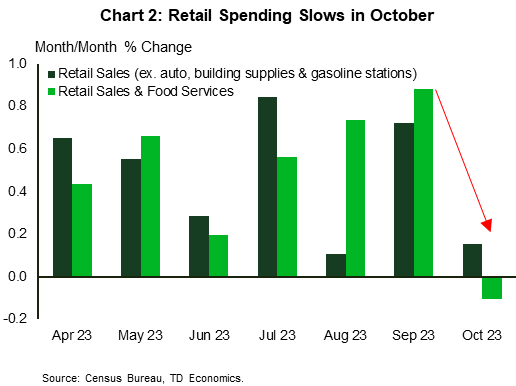

Retail sales data out this week showed that spending activity moderated in October. Although some of the weakness was attributed to a pullback in vehicle sales (possibly impacted by the UAW strike), the less volatile components still showed a meaningful deceleration in spending relative to prior months (Chart 2). Moreover, higher frequency credit card spend data reported through the first week of November has shown that spending activity has continued to moderate into the holiday shopping season.

Retail sales data out this week showed that spending activity moderated in October. Although some of the weakness was attributed to a pullback in vehicle sales (possibly impacted by the UAW strike), the less volatile components still showed a meaningful deceleration in spending relative to prior months (Chart 2). Moreover, higher frequency credit card spend data reported through the first week of November has shown that spending activity has continued to moderate into the holiday shopping season.

At this point, the tailwinds for the consumer seem to be fading. Over two-thirds of the excess savings accumulated during the pandemic have now been exhausted, with most of the remaining savings likely residing with higher income households who tend to have a lower marginal propensity to consume. This is happening at a time when 27 million borrowers have started to make regular student loan repayments amidst a backdrop of deteriorating consumer sentiment and expectations of a cooling labor market.

To that end, recent readings on initial jobless claims have already turned higher over the past month, as have continued claims – recently touching a near two-year high. This suggests that not only are more workers losing their jobs but it’s also becoming a bit harder to find another. Ultimately, the labor market remains very tight by historical standards, but the recent drift higher in claims data suggests underlying conditions are easing on the margin. Although the Fed will need to see further evidence of cooling in the months ahead to rule out another rate hike next year, the recent data flow favors the FOMC holding rates steady in December.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of November 10th, 2023

Financial News Highlights

- The risk of a government shutdown has returned as Congress has one week left before the continuing resolution passed on September 30th expires in governmental and financial news.

- The Federal Reserve’s Senior Loan Officer Opinion Survey showed that banks continued to tighten credit standards in the third quarter, as credit demand weakened further.

- Consumer credit growth eased in the third quarter as an acceleration in revolving credit growth (i.e. credit cards) was offset by a contraction in nonrevolving credit (i.e. student loans).

Government Shutdown Risk Redux

After last week’s busy slate markets took a breather to digest last week’s Federal Reserve policy decision and prepare for the risk of another potential government shutdown next Friday in financial news. On the data front, the Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) and consumer credit report both showed credit conditions remained tight and demand continues to wane.

After last week’s busy slate markets took a breather to digest last week’s Federal Reserve policy decision and prepare for the risk of another potential government shutdown next Friday in financial news. On the data front, the Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) and consumer credit report both showed credit conditions remained tight and demand continues to wane.

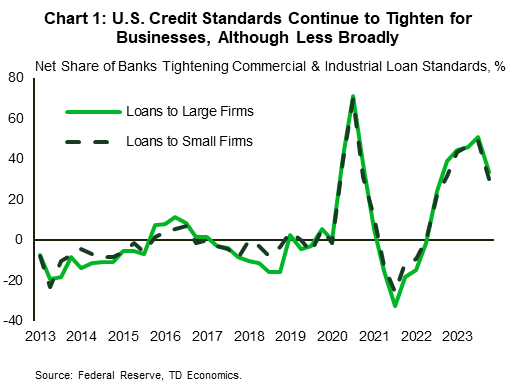

Monday’s release of the SLOOS showed that banks continued to tighten credit standards across loan categories in the third quarter and report weaker business and consumer demand for loans (see here). Although this came as little surprise considering Treasury yields rose by roughly 100 basis-points in Q3, the share of banks reporting tighter standards for commercial and industrial loans actually declined relative to the second quarter (Chart 1). This also held true for consumer credit cards and auto loans, although personal and mortgage loans each saw broader tightening relative to the second quarter. Despite the modest narrowing of credit tightening in the third quarter, the Federal Reserve’s continued signaling of rates staying higher for longer means a material loosening of credit standards likely remains a way off.

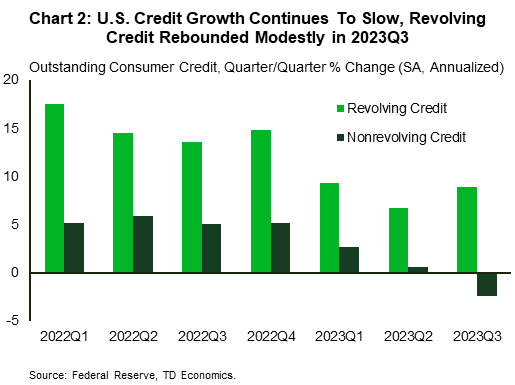

Easing consumer demand for loans was also evident in the Federal Reserve’s consumer credit data release on Tuesday which showed outstanding credit growth slowed notably relative to the second quarter. Outstanding revolving credit loans, which includes credit cards, saw accelerating growth in the third quarter of 8.6% while non-revolving credit growth, which includes student loans, declined by 2.4% (Chart 2). Under the weight of higher prices many consumers are increasingly relying on revolving credit to support spending, particularly as the moratorium on student loan repayment ends. Next week’s retail sales data will show whether the past six months of real sales growth, aided by consumer credit, continued into October despite the growing headwinds facing consumers.

In addition, updated CPI data out next week is expected to show continued easing in aggregate price pressures, supported by cooling energy prices. While this would undoubtedly be positive news, core inflation, which excludes food and energy prices, is expected to persist well above the Federal Reserve’s 2% target. A majority of FOMC members have noted that their current pause is conditional on sustained disinflation progress, with Chair Powell stating on Thursday that “if it becomes appropriate to tighten policy further, we will not hesitate to do so”.

In addition, updated CPI data out next week is expected to show continued easing in aggregate price pressures, supported by cooling energy prices. While this would undoubtedly be positive news, core inflation, which excludes food and energy prices, is expected to persist well above the Federal Reserve’s 2% target. A majority of FOMC members have noted that their current pause is conditional on sustained disinflation progress, with Chair Powell stating on Thursday that “if it becomes appropriate to tighten policy further, we will not hesitate to do so”.

Rounding out the coming week is the return of the risk of a potential government shutdown (see here) as the continuing resolution passed on September 30th expires on Friday, November 17th. Of the twelve appropriation bills that need to be passed to fund the federal government, the House has passed seven and the Senate has passed three with no consolidated bill managing to pass both chambers of Congress. This means that another continuing resolution may be used as a stopgap once again, but markets are likely to become increasingly apprehensive as Friday’s deadline approaches.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of November 3rd, 2023

Financial News Highlights

- The Federal Reserve’s policy statement took center stage this week in financial news. As expected, the Fed kept policy rates unchanged but preserved the option of hiking in the future.

- Hiring in the U.S. slowed in October, with wage gains decelerating and the unemployment rate edging up.

- Activity in the manufacturing sector continued to contract in October, in contrast to the continued expansion in the services sector (though at a slower rate).

The Fed’s Door is Still Open

The U.S. economic calendar was packed this week with a mix of key data, central bank meetings and even Treasury auction announcements. To start things off, the Treasury announced its financing requirements for the upcoming quarter. In the announcement, issuance is dominated by shorter dated securities (2-7 year), with planned 10-to-30-year range issuance less than most had expected. What’s more, Treasury’s projection that it will slow the recent flood of new long-dated debt, contributed to a rally in the bond market and a pullback in long-term yields.

The U.S. economic calendar was packed this week with a mix of key data, central bank meetings and even Treasury auction announcements. To start things off, the Treasury announced its financing requirements for the upcoming quarter. In the announcement, issuance is dominated by shorter dated securities (2-7 year), with planned 10-to-30-year range issuance less than most had expected. What’s more, Treasury’s projection that it will slow the recent flood of new long-dated debt, contributed to a rally in the bond market and a pullback in long-term yields.

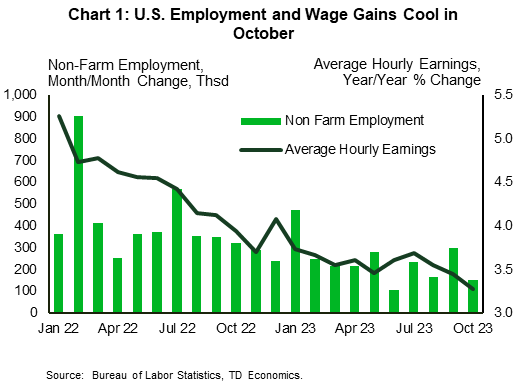

The next key focus was the labor market, with varying reports giving snapshots of the state of this important sector. November’s nonfarm payrolls, the most important, showed that hiring in the U.S. economy has slowed. Additionally, the pace of wage growth has cooled (Chart 1) in financial news. The unemployment rate also edged up slightly, bucking expectations for no change. The job opening and labor turnover survey (JOLTS) was slightly backward looking, covering September, and showed an increase in job openings, which was offset by a rise in the number unemployed, leaving the ratio of the two largely unchanged at 1.5. The pace of hiring also eased and the quit rate levelled off at its pre-pandemic rate. The employment cost index on the other hand showed that wage gains ticked up in the third quarter, but compensation growth still slowed from 4.5% to 4.3% on a year-on-year basis. Overall, the labor market metrics are consistent with what the Fed wants to see – a market that is slowly cooling with likely further deceleration in wage pressures ahead.

As widely expected, the Federal Reserve held interest rates steady at 5.25%-5.50% on Wednesday. This is the first time in the current tightening cycle that the Fed has paused for two consecutive meetings. However, the central bank still left the door wide open to potentially raising rates in the future if needed to keep the disinflation momentum going. October’s cooling in the labor market combined with expectations that economic activity will pullback in Q4, suggests that they may not need to walk through it before the year is done, but only time (and the data) will tell.

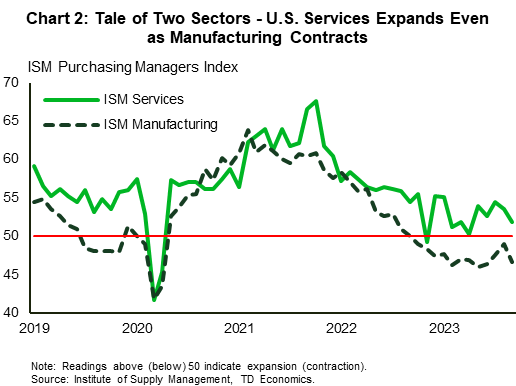

One sector of the economy that is not fairing very well is the manufacturing sector. Activity in the sector, as measured by the ISM sentiment survey, continued to contract in October, falling to its lowest level since July, on broad-based weakness. The silver lining, however, is that a pullback in raw materials prices is easing cost pressures, which should help to mitigate price pressures for consumer goods. The services side of the economy fared a bit better, with the ISM services index expanding again in October, though at a slower pace (Chart 2). Twelve out of eighteen industries reported growth; however, the softer-than-expected reading suggests that the Fed’s hiking campaign is influencing the services sector as well.

One sector of the economy that is not fairing very well is the manufacturing sector. Activity in the sector, as measured by the ISM sentiment survey, continued to contract in October, falling to its lowest level since July, on broad-based weakness. The silver lining, however, is that a pullback in raw materials prices is easing cost pressures, which should help to mitigate price pressures for consumer goods. The services side of the economy fared a bit better, with the ISM services index expanding again in October, though at a slower pace (Chart 2). Twelve out of eighteen industries reported growth; however, the softer-than-expected reading suggests that the Fed’s hiking campaign is influencing the services sector as well.

The takeaway from the week is that if the disinflationary trend remains intact, the Fed’s December decision is a tougher call. There will be several economic releases over the next six weeks that will influence the Fed’s decision. But, so far, consumer spending momentum has remained stronger than expected, risking an uptick in inflation. This still suggests that the Fed’s work is likely not done.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 27th, 2023

Financial News Highlights

- The 10-year Treasury yield briefly surpassed 5% earlier this week in financial news. Though yields have since retraced, the 10-year looks to end the week at a still elevated 4.85%.

- The advance estimate of GDP showed the economy registered its strongest gain in nearly two years in the third quarter, with most major areas of spending recording gains.

- The FOMC is expected to hold rates steady next week, but the uptick in September inflation along with any signs of continued labor market strength in next week’s data will tilt the scales in favor of another rate hike later this year.

Economic Resilience on Full Display in Third Quarter

Longer-term Treasury yields continued to creep higher through the early portion of the week, as the looming threat of a mid-November government shutdown, increased Treasury issuance, and heightened geopolitical tensions remain key drivers pressuring the term-premia higher. After briefly surpassing 5% earlier this week, the 10-Year Treasury yield has since pared its gains and currently sits at a still elevated 4.85%. Meanwhile, equities edged lower for the second straight week – down 2% at the time of writing – but remain 8% higher on the year.

Longer-term Treasury yields continued to creep higher through the early portion of the week, as the looming threat of a mid-November government shutdown, increased Treasury issuance, and heightened geopolitical tensions remain key drivers pressuring the term-premia higher. After briefly surpassing 5% earlier this week, the 10-Year Treasury yield has since pared its gains and currently sits at a still elevated 4.85%. Meanwhile, equities edged lower for the second straight week – down 2% at the time of writing – but remain 8% higher on the year.

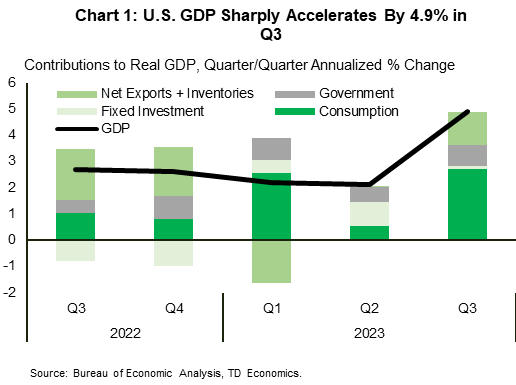

Turning to the economic data calendar, the Bureau of Economic Analysis (BEA) released its advance estimate of third quarter real GDP. The report showed economic activity accelerating at more than double the rate of expansion seen in Q2. The ongoing theme of economic resilience was on full display last quarter, with most major areas of spending recording gains in financial news. The strength in consumer spending was particularly eye-catching, jumping up 4.0% (Chart 1). The summer shopping spree was fueled by a resilient labor market and a further drawdown of the excess savings accumulated during the pandemic. Moreover, because many homeowners locked-in mortgages at ultra-low rates in 2020/21, the passthrough of higher interest rates to the consumer has been more muted relative to past tightening cycles.

Perhaps more concerning for policymakers is that spending momentum heated up at the end of the third quarter. September’s gain was the second strongest over the past eight months, and suggests consumers didn’t hold back last month, despite the looming headwind of student loan repayments restarting in October. At this point, we see Q3’s blowout numbers as the ‘last hurrah’ and expect a more tepid pace of consumer spending (1.5-2%) for Q4, before slipping sub-1% through the first half of next year.

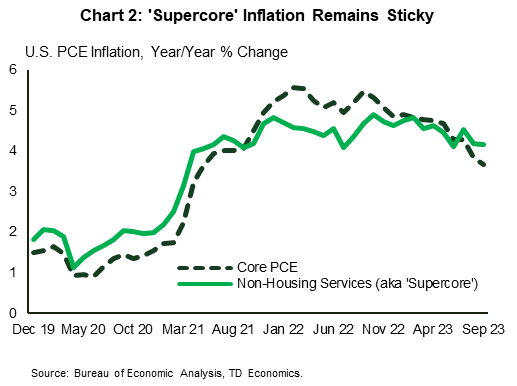

Should the consumer prove more resilient, that will spell trouble on the inflation front. In fact, core PCE inflation data for September has already telegraphed some evidence of progress stalling. Price growth picked up to 0.3% m/m (up from the 0.17% m/m gains averaged over the three prior months), with notable strength in Powell’s ‘supercore’ measure, which has barely budged from last year’s highs (Chart 2).

Should the consumer prove more resilient, that will spell trouble on the inflation front. In fact, core PCE inflation data for September has already telegraphed some evidence of progress stalling. Price growth picked up to 0.3% m/m (up from the 0.17% m/m gains averaged over the three prior months), with notable strength in Powell’s ‘supercore’ measure, which has barely budged from last year’s highs (Chart 2).

From the Fed’s perspective, nothing out this week will influence next week’s interest rate decision. At this point, markets are fully priced for the FOMC to hold rates steady, and only attach a 20% probability to another rate hike in December. However, that could quickly change over the next week should the FOMC statement and/or Powell’s press conference strike a more hawkish tone. Next week’s Employment Cost Index release for the third quarter is also important given it contains a measure of wage inflation that the Fed watches closely. As well, October’s employment figures out Friday will be closely scrutinized as usual. Unless these reports show a definitive sign that the labor market is cooling, which looks unlikely given the recent strength in higher frequency indictors including jobless claims and Indeed job posting data, another rate hike come December seems inevitable.

Thomas Feltmate, Director | 416- 944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 20th, 2023

Financial News Highlights

- Treasury yields continued their steep ascent this week, amidst a heavy week for Fed speakers in financial news. FOMC members broadly agreed that positive progress had been made on inflation, although few were willing to take the prospect of further policy tightening off the table.

- Previous increases in mortgage rates weighed heavily on the housing market in September, although new home construction rebounded from its August decline.

- The consumer appeared undeterred by higher borrowing costs in September, with retail sales growth doubling expectations.

Treasury Yields Flirt with Multidecade Highs

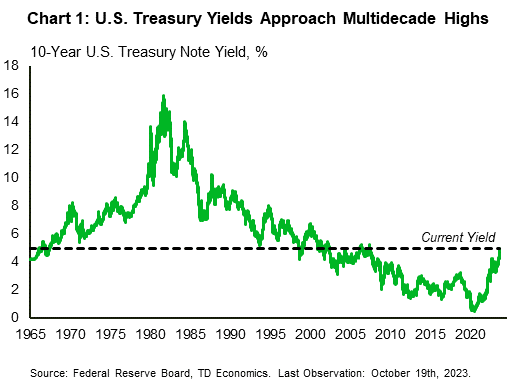

The steep ascent of U.S. Treasury yields continued unabated this week, as markets revised their expectations for yields, particularly over the longer term. The persistent political dysfunction in Congress amid rising deficits and heightened geopolitical tensions is likely playing a role in the increase in the term premium, which has recently contributed to the higher 10-Year yield. The term premium reflects the added compensation investors require for the unknowns associated with holding longer-term government debt. The 10-Year Treasury yield is now just under 5%, its highest level since before the Global Financial Crisis (Chart 1). Equities in turn fell this week, with the S&P 500 down 1.8% as of the time of writing.

The steep ascent of U.S. Treasury yields continued unabated this week, as markets revised their expectations for yields, particularly over the longer term. The persistent political dysfunction in Congress amid rising deficits and heightened geopolitical tensions is likely playing a role in the increase in the term premium, which has recently contributed to the higher 10-Year yield. The term premium reflects the added compensation investors require for the unknowns associated with holding longer-term government debt. The 10-Year Treasury yield is now just under 5%, its highest level since before the Global Financial Crisis (Chart 1). Equities in turn fell this week, with the S&P 500 down 1.8% as of the time of writing.

Outside of financial markets, the real economy has seen divergent trends between economic sectors depending on their sensitivity to interest rates. The housing market softened further in September to reach a 13 year low, reflecting the strain of higher mortgage rates (see here). While existing home inventory levels improved on the month, supply remains low, which continued to place upward pressure on housing prices. Low resale listings have in turn increased the demand for new units, but elevated rates remain a headwind to homebuilding activity as well. While housing starts rose in September, they remain well below year-ago levels, primarily resulting from weakness in the more rate-sensitive multi-family segment.

Despite higher interest rates, the health of the American consumer has remained robust (see here). Retail sales growth in September more than doubled expectations. Somewhat surprisingly, the most rate-sensitive segment of retail sales (Automobile & other motor vehicle dealers) saw its strongest growth in four months in financial news. However pent-up demand from the extended shortage of vehicles in previous years continues to be a factor. But, even excluding the more volatile categories, the retail sales “control group” was very strong on the month. All in all, the resilience of the consumer has been a key growth contributor in 2023.

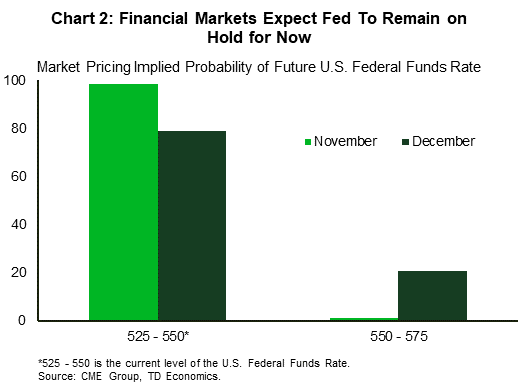

In terms of what this means for interest rate moves, we heard remarks from nearly every member of the FOMC this week, including Chair Powell. The balance of opinion was skewed towards maintaining a wait and see approach given the positive progress that has been made on inflation thus far, which pushed market pricing for a hold at the next meeting on November 1st to a virtual certainty (Chart 2). However, Powell also noted that additional evidence of persistently above trend growth or tightening labor market conditions could put inflation progress at risk and warrant further policy tightening. We currently expect that the resilience of the U.S. economy will lead to one last interest rate hike, but the recent tightening in financial conditions makes it a close call.

Next week we will see the advance estimate for third quarter GDP growth, which is expected to show eye-popping growth. Perhaps more importantly, the September consumer spending data will show how momentum is looking heading into the fourth quarter, along with the Fed’s preferred inflation metric. A moderation in both metrics would be welcome news for the Fed.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Featured Article: Smishing: A Silly Word for a Serious Fraud Threat

Smishing: A Silly Word for a Serious Fraud Risk

There was clearly something fishy afoot when Beth, a disabled 50-year-old from North Carolina, received two text messages saying she had money available to add to her phone’s digital wallet.

One message said, “Beth put this in your wallet and use it whenever.” The other said, “The balance on this account is yours. no be to share [sic].” Both messages included hyperlinks.

Beth, who asked not to use her last name, had just become the target of “smishing,” an increasingly common tactic criminals are using to commit fraud.

Instead of clicking on the embedded links, Beth deleted the messages and reported them to the Better Business Bureau, a business watchdog. “Money doesn’t just drop in your lap,” she told Consumer Reports, explaining why the messages raised her suspicions. Beth says she has been on high alert for fraud since being targeted by calls from scammers claiming to be officials from the IRS or Social Security.

The word smishing combines SMS, the primary technical format for text messaging, and phishing. As in other phishing attacks, the criminals masquerade as government workers, tech support representatives, long-lost friends, or financial institutions, and try to lure people into divulging personal details that could lead to fraudulent credit card purchases or identity theft.

Robotexts Are the New Robocalls

More than 87 billion spam texts were sent to U.S. phone users in 2021, according to RoboKiller, a spam text mitigation service—that’s 58 percent more than the prior year, RoboKiller says. And so far this year, U.S. phone users have received over 55 billion spam texts with 12.02 billion texts received in the month of June alone, according to RoboKiller.

Top Scams

Delivery scams where fraudsters impersonate Amazon, FedEx, and the U.S. Postal Service are the most prominent text scam, accounting for over 26 percent of all SMS scams in 2021, according to RoboKiller. In these scams, robotexts are sent with links that are purported to be for tracking packages or adjusting user preferences. However, they’re actually links that connect users to fake websites where the recipient will divulge their sensitive information or download malware onto their device.

COVID-19 scams were the second most common text scam in 2021, according to the company. Here, scammers offer COVID-19 tests and request personal and financial information.

In addition to those scams, text messages are also used to perpetrate intricate bank and peer-to-peer (P2P) digital payment fraud.

With some bank frauds, victims are fooled into furnishing log-in credentials, which criminals use to siphon out cash or open credit cards, whereas with P2P frauds, victims can be tricked into paying for goods and services they never receive, or sending money to people pretending to be friends or relatives. There have even been reports of identity theft in which the criminals will use someone else’s name and information to rent property.

Here are a few tips to stay safe when using text messages.

How to Avoid Smishing

- You should never reply or click on any links in an unwanted text. They can contain malicious code that could infect your mobile phone.

- Forward unwanted texts to 7726, which spells SPAM. It’s free to do and forwards the messages to your phone carrier’s spam department so that it can take action against the number. If a message is being delivered over a third-party messaging app, you’ll want to report it to the app that you use by looking for an option to report junk or spam.

- Your phone should have an option to filter or block messages from a specific number. Major providers also often have a tool or service that can block spam calls and texts that you can look for and use. Similarly you can download a call- and text-blocking app from your phone’s app market or download apps from the Apple or Google app stores.

- Beware of messages that are claimed to be from government agencies, such as the IRS or Social Security. The IRS will never send you an unsolicited text message or initiate contact via text message, email, or social media. Social Security does allow marketing firms to send emails to raise awareness of Social Security’s online services, and it uses text messages for two-factor authentication—but only if you’ve set up that security measure through your online account.

- A telltale sign that you may be under attack is that a message is trying to impart a sense of urgency. These types of scams often imply that an immediate response is required to take advantage of an offer or to avoid a penalty.

- Don’t be taken in by friendly, familiar language. Smishing text messages may use your name. While they often come from unfamiliar numbers, sometimes they seem to have originated from a phone number you recognize.

- Do not respond to suspicious text messages, even if the message says you can “text STOP” to prevent future messages. Any response on your part will confirm for the scammers that the number is in use—and you’ll just be inviting more texts.

- You should always be careful when giving out your phone number and when entering your phone number into any customer site. You should read through the commercial web forms and check for a privacy policy. In these cases you should be able to opt out of texts, but it may require you to check or uncheck a box.

- Delete all suspicious texts.

- Make sure your phone’s operating system is up to date. Android and iOS are constantly being updated with enhanced security features. On Android models and iPhones, your phone’s settings page should indicate which system you’re using and whether an update is available.

- If you get a suspicious text from an official-sounding entity and want to check it out, don’t use any information from the message itself. Instead, call or email the company or government agency directly, using an official phone number from a recent bill or another valid source of information.

- You should also alert law enforcement to the attack by submitting a report to the FCC or the Federal Trade Commission.

To see more fantastic articles like this one, please see here.

Financial News for the Week of October 13th, 2023

Financial News Highlights

- U.S. bond yields retreated from highs reached last week, as heightened geopolitical risks in the Middle East boosted investors demand for safe haven assets in financial news.

- However, the recent overall surge in yields has prompted some Fed members to pay closer attention to tightening financial conditions as they determine the most appropriate policy path for interest rate.

- Both producer prices and consumer prices suggest that the Fed still has some work to do to ensure inflation gets back to target, even as core prices continue to moderate.

Goodbye “How High”, Hello “How Long”

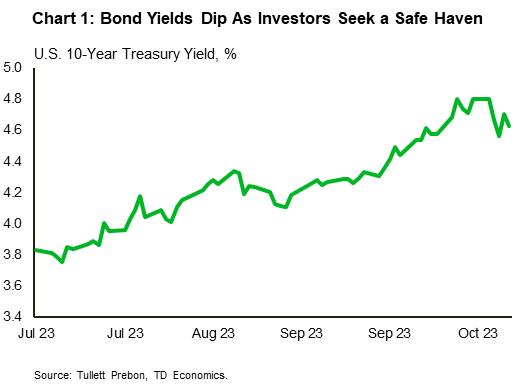

Last week’s tight financial conditions abated a bit this week, as conflict in the Middle East boosted demand for safe haven assets. As such, the 10-year Treasury yield took a reprieve from its upward trek and at the time of writing was down 17 basis points (bps) relative to the end of last week (Chart 1). Nonetheless, yields are still up 76 bps since July 26 when the Fed last raised the policy rate. Several factors have contributed to rising bond yields over the past few months including expectations of higher for longer interest rates and concerns about energy supply and prices.

Last week’s tight financial conditions abated a bit this week, as conflict in the Middle East boosted demand for safe haven assets. As such, the 10-year Treasury yield took a reprieve from its upward trek and at the time of writing was down 17 basis points (bps) relative to the end of last week (Chart 1). Nonetheless, yields are still up 76 bps since July 26 when the Fed last raised the policy rate. Several factors have contributed to rising bond yields over the past few months including expectations of higher for longer interest rates and concerns about energy supply and prices.

The relatively higher yields have prompted some Fed officials to acknowledge that higher longer-term yields may be helping to achieve their policy objective. Dallas Fed President Lorie Logan remarked that “if long-term interest rates remain elevated because of higher term premiums, there may be less need to raise the fed-funds rate.” Similar sentiments were echoed by Fed governor Christopher Waller who said that “financial markets are tightening up and they are going to do some of the work for us”. Fed Vice Chair Philip Jefferson said that he would “remain cognizant of the tightening in financial conditions through higher bond yields” when assessing the path for interest rates. That sentiment was also echoed by Minneapolis Fed president Neel Kashkari.

The minutes released from the Fed’s September meeting revealed that, prior to the most recent run-up in bond yields, a “majority” of FOMC participants believed that another rate increase might be appropriate, while only “some” viewed no further increases as necessary. The tone of the minutes, economic projections and policy guidance was hawkish with Fed members expecting rates to be kept higher for even longer. This was reflected in a shallower path of expected rate cuts (FOMC commentary).

Additionally, “several” participants commented that the Fed’s focus should be transitioning to how long to maintain restrictive policy, rather than how high to raise rates. Ultimately, all participants were in favor of maintaining restrictive policy for some time to ensure that inflation remains on a sustainable path downwards.

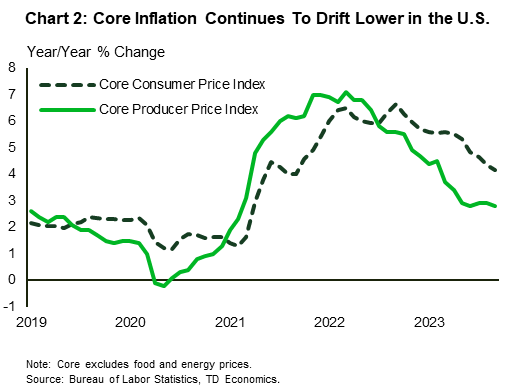

Both headline measures of producer prices (PPI) and consumer prices (CPI) show that the inflation battle is not quite over. On a yearly basis, PPI accelerated in September, while CPI held steady. The movements largely reflected gains in food and energy prices. Stripping out these volatile segments, core prices for both measures edged lower (Chart 2). While the downward tilt to core prices is sure to be welcomed by the Fed, rates are still too high for comfort given that near-term inflation expectations have inched higher in recent months and the labor market remains resilient.

American small businesses are also feeling less optimistic as expectations regarding the economic outlook and credit conditions deteriorated in September. Several firms noted that the Fed’s aggressive hiking campaign is weighing on credit with a net 26% of borrowers reporting paying higher interest rates versus three months ago. Nonetheless, the Fed will need to see a meaningful cooling in the jobs market and a sustained reduction in inflation, before shifting policy stance. As such, higher for longer may be around for some time.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 6th, 2023

Financial News Highlights

- And just like that, the Fed’s short-lived pause is likely done after a bevy of positive economic data show an incredibly resilient economy in financial news.

- This morning’s payrolls report showed a stellar 336k jobs added in September, along with an upward revision of another 119k jobs to the past two months.

- Financial conditions have tightened this week, but with such healthy economic momentum the Fed still has more work to do to cool demand and bring inflation back in line with its two percent target.

The Jobs Machine Keeps Whirring

And just like that, the Fed’s short-lived pause is likely done in financial news. Markets have responded aggressively to a bevy of positive economic data and sent ten-year government bond yields up 20 basis points since the start of the week. The bond rout had abated mid-week, only to be abruptly undone by Friday’s gangbusters payrolls report that sent yields surging. This week’s data stream shows an economy that continues to shrug off a higher policy rate, likely forcing the Fed to action before the end of the year.

And just like that, the Fed’s short-lived pause is likely done in financial news. Markets have responded aggressively to a bevy of positive economic data and sent ten-year government bond yields up 20 basis points since the start of the week. The bond rout had abated mid-week, only to be abruptly undone by Friday’s gangbusters payrolls report that sent yields surging. This week’s data stream shows an economy that continues to shrug off a higher policy rate, likely forcing the Fed to action before the end of the year.

With all eyes focused on this morning’s payrolls report, it didn’t disappoint with a stellar 336k jobs added in September, along with an upward revision of another 119k jobs to the past two months. The print for September effectively doubled up on the market’s expectations. Industry figures lined up with this week’s ISM services index, as gains were concentrated in the services sector – with leisure and hospitality leading the way.

There isn’t much need to address the details. The strong addition to payrolls squares with the Job Opening and Labor Turnover Survey (JOLTS) that came earlier this week and showed job openings jumped in August, reversing the two prior months’ declines, as firms continue to search for talent. While the number of open positions continues to trend lower from its pandemic-era surge, there remain a whopping 44% more job openings as of August than there were in December of 2019.

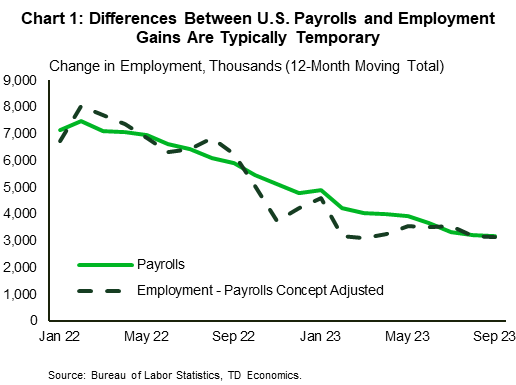

The labor market is tight with jobs aplenty. That said, one apparent contradiction in the report is the wedge between the household employment and payrolls reports. Despite the stellar jobs gains, the unemployment rate was unchanged (3.8%), the labor force participation rate didn’t budge and the number of employed people only rose by 86k. However, deviations of this size are typical and tend to even out in the long run (Chart 1), keeping the focus firmly on the headline job creation figure.

The labor market is tight with jobs aplenty. That said, one apparent contradiction in the report is the wedge between the household employment and payrolls reports. Despite the stellar jobs gains, the unemployment rate was unchanged (3.8%), the labor force participation rate didn’t budge and the number of employed people only rose by 86k. However, deviations of this size are typical and tend to even out in the long run (Chart 1), keeping the focus firmly on the headline job creation figure.

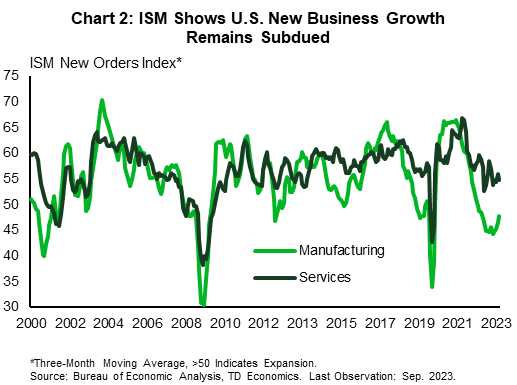

Private sector data that came earlier this week also supported the notion that the economy remains is fairly good shape despite the rate hikes. The ISM Manufacturing Purchasing Managers’ Index (PMI) firmed in the month, showing the contraction in the sector slowed. Meanwhile, its services sector counterpart held in expansionary territory despite slowing for the month. Rate hikes are clearly working as new business growth for both the manufacturing and services sectors (Chart 2) is moderating, but for all the work the Fed has done, it just isn’t proving to be enough.

Bottom line, a week of stronger-than-expected economic data have now all but put an end to the Fed’s pause. Financial conditions have tightened this week and will work to slow activity, but with such healthy economic momentum the Fed still has more work to do to cool demand and bring inflation back in line with its two percent target. This means a hike by year end is now on the table as the Fed continues its work to restore balance and slow price growth.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 29th, 2023

Financial News Highlights

- Revisions to GDP data left Q2 growth unchanged, but consumer spending growth was cut in half in financial news. Monthly consumer spending data showed that following at strong gain in July, real consumer spending slowed in August.

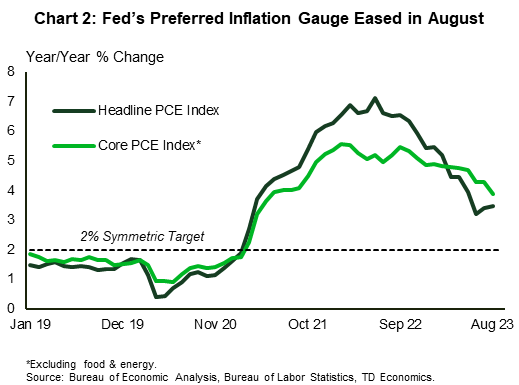

- The Fed’s preferred inflation gauge, the core Personal Consumption Expenditures (PCE) deflator, eased from 4.3% year-on-year to 3.9% in August. However, headline PCE inflation ticked up a notch as energy costs surged higher on the month.

- Pending home sales, which lead existing home sales by 1-2 months fell a sharp 7.1% in August, as mortgage rates crept above 7% that month.

Yields Realign to Higher-for-Longer

The Fed has been beating the drum to the “higher for longer” interest rate tune for a while in financial news. Following last week’s FOMC projections, investors are recalibrating their expectations more in line with this view. Long-term treasury yields pushed higher in the week, with the 10-Year yield rising temporarily to a new 15-year high on Thursday, before easing to 4.53% at time of writing – still almost 10 basis points above last week’s close. Equity markets trended lower through the week, but managed to recoup most of the lost ground after Friday’s soft inflation print.

The Fed has been beating the drum to the “higher for longer” interest rate tune for a while in financial news. Following last week’s FOMC projections, investors are recalibrating their expectations more in line with this view. Long-term treasury yields pushed higher in the week, with the 10-Year yield rising temporarily to a new 15-year high on Thursday, before easing to 4.53% at time of writing – still almost 10 basis points above last week’s close. Equity markets trended lower through the week, but managed to recoup most of the lost ground after Friday’s soft inflation print.

Revisions to GDP data led to a minor growth upgrade for the first quarter, but left the second unchanged. However, the picture was more nuanced underneath. Most notably, second quarter consumer spending growth was cut in half, to only 0.8% q/q (ann.). August’s Personal Income and Spending data out Friday help fill in the picture for the third quarter. Real disposable personal income fell for the third month in a row in August, while real spending (PCE) growth eased to 0.1% month-on-month (m/m), following a strong 0.6% m/m gain in July. That strength early in the quarter will still make for a strong showing for the consumer, however many hurdles are looming for the fourth quarter (see forecast). Our view is that consumer spending and economic growth will cool along with the weather this autumn, with September’s pullback in consumer confidence reinforcing this view.

Housing, which was the first part of the economy to weaken in the face of rate hikes, continues to struggle. Pending home sales, which lead closed sales by 1-2 months, fell a very sharp 7.1% (m/m) in August (Chart 1). This suggest that existing home sales could soon test new post-2010 lows. The shortage of existing homes for sale has been an added obstacle for transactions. Until recently, homebuyers appeared to have found some solace in the new home market, aided by healthier inventories and builder incentives. But with mortgage rates creeping above 7% in August, this sector is also feeling the pinch. New home sales (an inherently volatile series) trended lower that month. Daily measures show that mortgage rates have risen even higher recently and are now hovering in the 7.4%-7.6% range, a level that will surely further limit the pool of homebuyers.

Besides the challenges faced by the consumer, the UAW’s decision Friday to expand its strike and the increasing likelihood for a government shutdown next week, mark two other major potholes for the economy heading into the fourth quarter (see report). The shutdown would not only act as a drag on growth but would also delay access to key economic data, with next week’s payrolls report and the October 12th (CPI) inflation report the next two major items on the list. Having timely access to these reports is crucial with inflation still running well above target.

Besides the challenges faced by the consumer, the UAW’s decision Friday to expand its strike and the increasing likelihood for a government shutdown next week, mark two other major potholes for the economy heading into the fourth quarter (see report). The shutdown would not only act as a drag on growth but would also delay access to key economic data, with next week’s payrolls report and the October 12th (CPI) inflation report the next two major items on the list. Having timely access to these reports is crucial with inflation still running well above target.

Thankfully, Friday’s PCE report carried some good news on the inflation front, with the Fed’s preferred inflation gauge easing from 4.3% to 3.9% year-on-year in August(Chart 2). However, the headline measure moved in the opposite direction, given an acceleration in food and energy costs. With the price of crude oil creeping higher to $93 per barrel, energy costs are likely to continue putting upward pressure on the headline measure over the near-term. All in all, it’s still a mixed picture, one that may be further complicated by a government shutdown.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.