Financial News for the Week of July 21st, 2023

Financial News Highlights

- Retail sales disappointed market expectations overall in June, but underneath the surface sales in the control group, which are used to calculate consumption, were much stronger, rising 0.6% on the month.

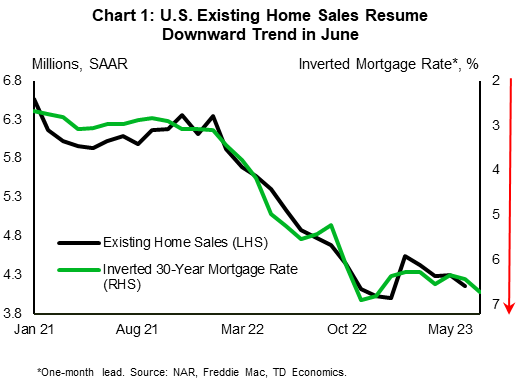

- Elevated mortgage rates and low inventories continue to weigh on existing home sales. The latter resumed their downward trend in June.

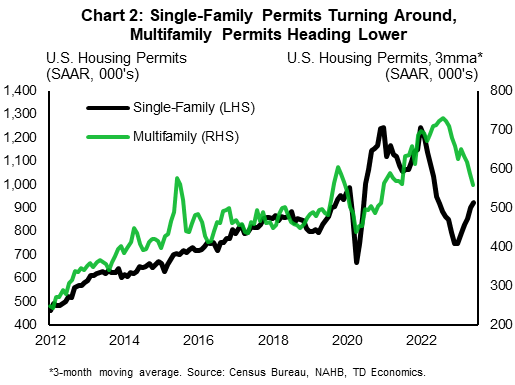

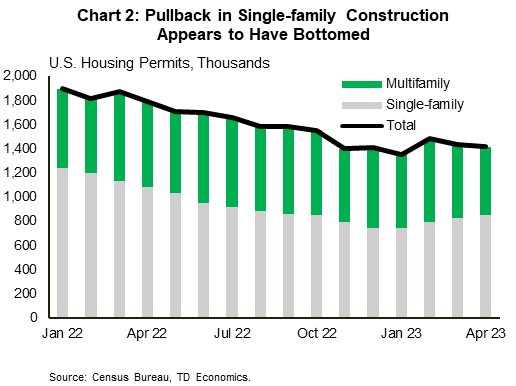

- Housing starts also fell in June. But, permitting data reveals a clear divergence between an upward trend in single-family permits and a downswing in multifamily permits.

Economic data this week wasn’t entirely positive, but it still pointed to an economy that continues to chug along at a decent clip in financial news. With no major red flags on the way, the Fed has the green light to hike the policy rate once more next week, before likely hitting the pause button.

While we expect the labor market to cool ahead, recent high frequency data still points to resilient demand for workers. Continuing jobless claims rose in the week ending July 8th, but initial claims continued to trend lower, easing for the second week in a row last week. With unemployment near multidecade lows, June retail sales suggested consumers are still spending, even as inflation bites into purchasing power. Headline retail sales growth was below market expectations, but an upward revision to the month prior helped provide some offset in financial news. The headline was dragged down by lower sales at gasoline stations, and at building material and garden equipment stores. A notable deceleration in sales at auto and food service establishments didn’t provide much support either. Stronger momentum was seen in the control group, which are used to calculate personal consumption expenditures, with sales rising 0.6% m/m – continuing a healthy pattern for the quarter.

Consumers weren’t as upbeat on homes, with existing home sales resuming their downward trend in June (see here). Elevated mortgage rates are likely to have been a major hurdle, given the tight relationship with sales recently (Chart 1). The higher rate environment has persisted through the first half of July, suggesting that there’s no turnaround in sight for the weakness in existing home sales. Low inventory is also restraining activity. There were only 1.08 million homes for sale in June – 170k less than last year and 840k less than in June 2019 – making for slim pickings.

As we note in a recent report, the tight conditions in the resale housing market are pushing more people toward the new home market. This is much to the delight of homebuilders, whose confidence has been improving rapidly since the start of the year. This optimism has been confined to the single-family segment, however. Multifamily homebuilders have been pulling back. Housing starts retreated in June in both segments, but permitting data reveals a clear divergence between the two segments (Chart 2). The recent softness in the multifamily space is consistent with a rise in the multifamily vacancy rate, and a record-setting number of units under construction in June.

All told, interest-sensitive areas of the economy remain under pressure. But with the employment backdrop continuing to hold up well, consumers still spending, and inflation appearing to move in the right direction, chances of a soft-landing look to have improved. The Federal Reserve is nonetheless expected to maintain a tightening bias over the near-term, and is almost certain to hike the policy rate once more next week. A Fed hike is fully priced in by markets at this point. Provided inflation continues to cool, this will likely be the Fed’s last hike this cycle.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of July 14th, 2023

Financial News Highlights

- Financial markets rallied this week following a string of promising data pointing to easing U.S. inflationary pressures.

- Inflation as measured by the Consumer Price Index fell to the slowest pace of growth since March 2021 in June. Core inflation also only increased modestly on the month. Input costs also trended lower last month, with the Producing Purchase Index falling to the lowest reading since August 2020.

- Though the data overwhelmingly point to easing inflationary pressures, the Federal Reserve is still expected to deliver another 25 basis-point hike later this month.

Inflation Data Brings A Healthy Dose of Optimism

Sentiment across global financial markets firmed this week following a lower-than-expected reading on U.S. inflation in financial news. Recession fears have been top of mind for investors over the past year amidst the Federal Reserve’s most aggressive tightening cycle in several decades. But signs of cooling inflation provided a dose of optimism that policymakers might achieve a goldilocks scenario of returning price stability without tipping the economy into recession. At the time of writing, the S&P 500 is up 2.5% on the week, WTI has rallied by just over 4% to $76 per-barrel, while yields across the board traded lower by approximately 20bps. The 10-Year Treasury yield currently sits at 3.8%.

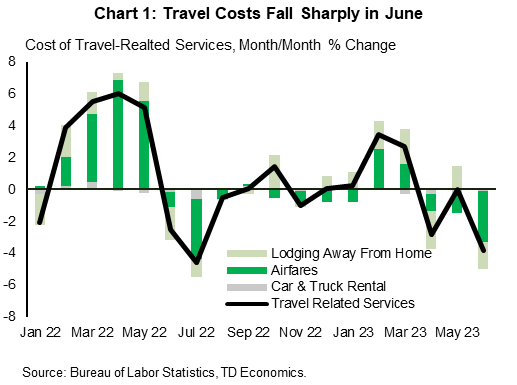

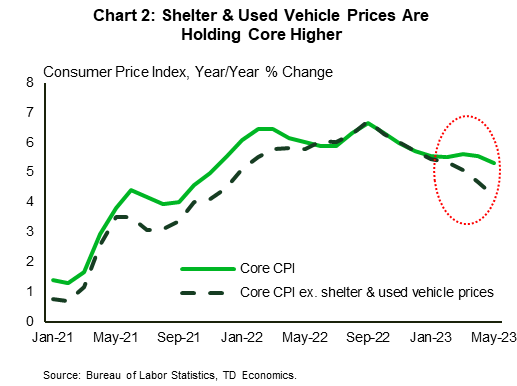

The Consumer Price Index (CPI) eased to a 3.0% pace y/y in June – the lowest reading since March 2021. But, perhaps more notable, core inflation rose by just 0.16% m/m – the slowest pace of growth in 28 months – and dipped to 4.8% y/y. A hefty decline in travel related services underpinned last month’s deceleration, as well as a continued deceleration in shelter costs (Chart 1) in financial news. Used vehicle prices also fell by a modest 0.5% m/m, which came after outsized gains in each of the two-months prior.

Looking to the months ahead, there’s good reason to remain optimistic that further progress will be made on the inflation front. For starters, the much anticipated slowing in shelter costs now appears to be firmly intact, with both owners’ equivalent rent (OER) and rent of primary residence (RPR) having decelerated in recent months. More importantly, current market-based measures of rent continue to show rental costs slowing, which means further disinflationary pressure on OER and RPR as more leases roll over.

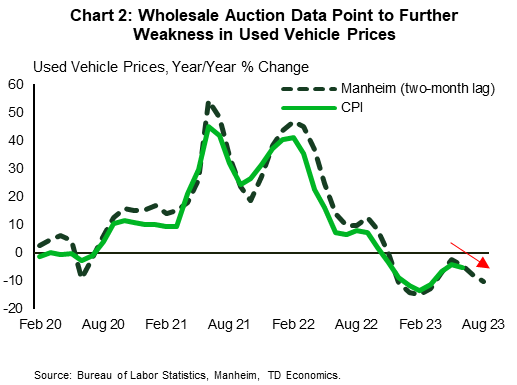

On the goods side, used vehicle prices are expected to be a source of downward pressure on inflation in the coming months. Wholesale auction data for used vehicle prices have tumbled in recent months, with the pass-through to the consumer measure typically taking 2-3 months. (Chart 2). Outside of this category, prices across all other goods have already been flat for three consecutive months and are likely to trend lower through the second half of this year alongside weaker consumer spending. Input costs are also trending favorably. The June reading on the Producer Price Index (PPI) showed that the 12-month change slowed to just 0.1% for final demand products – the lowest reading since August 2020.

Though the recent string of data overwhelming point to a continued easing in inflationary pressures, it is widely expected that Fed will deliver on another 25bps rate hike later this month. No matter which way you slice it, core inflation on a 12, 6, and 3-month annualized basis is still running at a multiple of the Fed’s 2% inflation target. And, with the labor market continuing to exude considerable resilience, policymakers will need to see more convincing evidence that the disinflationary process is firmly intact before calling it quits. Fed Chair Powell has repeatedly emphasized the risk of ‘stopping short’, so the FOMC is likely to maintain a tightening bias over the near-term as they continue to monitor incoming data and fine-tune the end point of its tightening cycle.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of July 7th, 2023

Financial News Highlights

- The week’s economic data was consistent with an economy that remains resilient, if no longer as robust as it was.

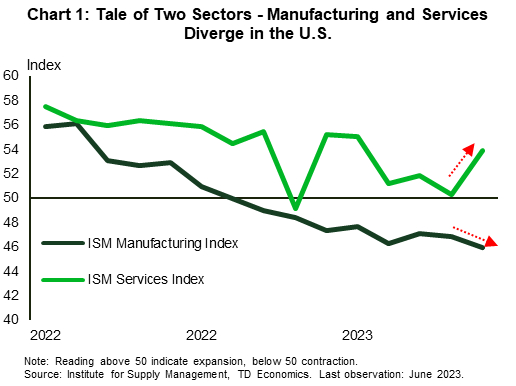

- Performance in the manufacturing and services sectors continued to diverge. The June ISM index showed manufacturing contracted for the eighth consecutive month, while services continued to expand six months in a row.

- The overall resilience will likely keep the Fed in hiking mode later this month, as the job market remains tight and wage growth stronger than the Fed would like. The FOMC minutes revealed that a few members favored a hiked at the June meeting, even if they did not formally dissent on the decision.

Job Market Cooling, But Not Enough

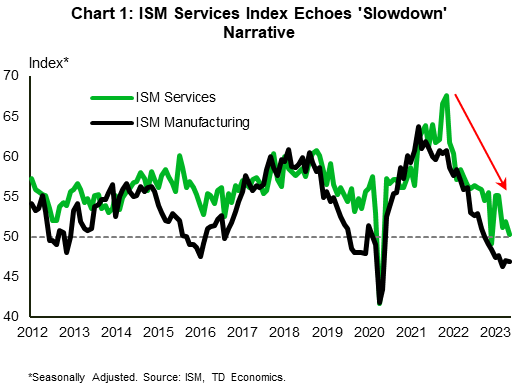

The week that was showcased a U.S. economy that while cooling, is still too resilient to achieve the Fed’s aim in financial news. First up, the ISM Manufacturing and Services Indexes showed that the goods sector continued to slow, while the service sector continued to expand, albeit at a modest pace. The manufacturing index declined again in June, falling 0.9 points to a 3-year low of 46.0. This marks its eighth consecutive month in contraction territory and points to deteriorating conditions in the manufacturing sector in financial news. The index suggests that demand remains weak in the sector, with new orders still below the 50 mark. Manufacturers have responded by cutting both production and employment (with both sub-indexes coming in below 50). The survey result is consistent with data on consumption expenditure (see here), which showed real spending flat in May and expenditure on goods pulling back by 0.4% on the month.

While a cool down on the goods side will be welcomed by the Fed, the real sticking point is still strong demand on the services side of the economy. The ISM services index remained in expansion territory for the sixth consecutive month in June, highlighting the divergence between the two indexes (Chart 1). While expanding, the services index is still off recent highs, and is consistent with a modest pace of growth in the broader economy. One factor likely to impede growth however is the looming resumption of student loan debt repayments, which combined with a softening labour market and rising interest rates, could reduce consumer spending and growth even further.

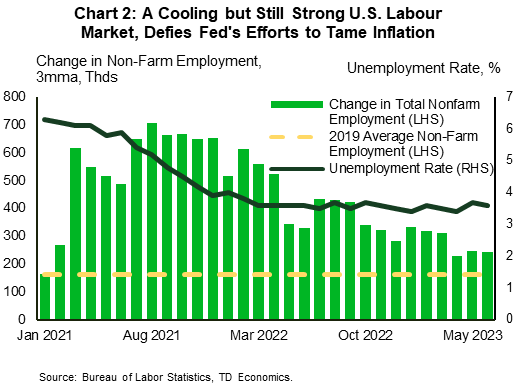

Fears about a softening labor market, however, may be more accurately characterized as normalization after the white-hot levels attained during the pandemic. The job opening and labor turnover survey for May showed that over 4 million American workers quit their jobs (250k more than the previous month) and that there were over 9.8 million job openings available. This morning’s jobs data reinforced the picture of a normalizing, but still strong labor market. The report showed firms added 209k jobs, easing from May’s 306k. The unemployment rate also pulled back 0.1 ppts to 3.6% (Chart 2). Taken together, the employment reports are indicative of a relatively resilient labor market despite a more than year-long campaign of rate hikes by the Fed to quell inflation.

In that regard, minutes of the June FOMC meeting revealed that the decision behind the Fed’s first pause may have been unanimous, but some committee members would have supported raising rates. Concerns about the effects of past rate increases though tempered desires for a hike, with the resultant “hawkish pause” in June.

With the services sector and labor market still showing resilience, the Fed is justified in signaling more hikes to come. This will have to be balanced against the hit to consumer spending from the resumption of student loan payments and a possible trade squabble with China over high tech as the two countries impose tit-for-tat measures. The balancing act the Fed is currently undertaking is a delicate one, and they will have to tread cautiously as they walk the tightrope to engineer that elusive soft landing.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of June 30th, 2023

Financial News Highlights

- A week’s worth of solid data did little to contradict Fed Chair Powell’s comments suggesting more monetary tightening is on the way.

- However, May’s personal consumption expenditure (PCE) report did provide a bit of reassurance for the Fed that demand is slowing down as real expenditure growth has been flat in three of the past four months.

- The problem remains that inflation is showing little sign of relenting and Fed officials are going to stay focused on tightening policy to cool the price pressure.

Healthy Data Keep Pressure on Fed

Fed Chair Jerome Powell noted this week that Fed officials, “believe there’s more restriction coming” from monetary policy in light of the persistently strong economic data in financial news. This week’s data stream did little to dissuade the sentiment. We got healthy prints from the housing market, consumer confidence, and manufacturing orders along with a personal consumption expenditure (PCE) report that showed little sign of core inflation abating. All told, the data underscored that the economy continues to chug along at a firm pace.

Fed Chair Jerome Powell noted this week that Fed officials, “believe there’s more restriction coming” from monetary policy in light of the persistently strong economic data in financial news. This week’s data stream did little to dissuade the sentiment. We got healthy prints from the housing market, consumer confidence, and manufacturing orders along with a personal consumption expenditure (PCE) report that showed little sign of core inflation abating. All told, the data underscored that the economy continues to chug along at a firm pace.

First up, activity in the housing market has ticked up. New home sales rose to their highest level since February 2022 in May. The market for new single-family homes troughed in July 2022 and has been trending upwards since, as inventories in the existing home market remain tight (see commentary). Sales in the existing market did move up in May as well, as a solid labor market helps drive demand.

Consumers’ moods have also been improving lately as the Conference Board consumer confidence index for June jumped up to its highest reading since January 2022. With both consumers’ assessment of the present situation and future expectations moved up on the month. Overall, consumers are not as confident as they were prior to the pandemic, likely as they contend with high inflation, but their higher spirits defy the recession warnings in financial news.

The good news didn’t just stop there. The industrial side of the economy saw manufacturers’ new orders of durable goods blow out expectations for a contraction, with a healthy advance. Taking a closer look at a key indicator of business investment, new orders excluding defense and aircraft advanced a solid 0.7% in the month, and 0.3% month-on-month when stripping out the effects of inflation.

However, May’s consumer spending report suggests that demand has paused from its strong start to the year. Real expenditures were flat for the third time in fourth months, as an advance in services spending was offset by a drop in goods spending. Moreover, it looks like consumers are adjusting habits as they save a bit more of their disposable income. The personal savings rate ticked up to 4.6% in May, nearly two percentage points higher than its low registered in June 2022 (Chart 1). With the Supreme Court striking down the Biden administration’s student debt relief plan today, and a separate student loan payment moratorium set to end, headwinds to the consumer spending outlook continue to build heading into the second half of 2023.

However, May’s consumer spending report suggests that demand has paused from its strong start to the year. Real expenditures were flat for the third time in fourth months, as an advance in services spending was offset by a drop in goods spending. Moreover, it looks like consumers are adjusting habits as they save a bit more of their disposable income. The personal savings rate ticked up to 4.6% in May, nearly two percentage points higher than its low registered in June 2022 (Chart 1). With the Supreme Court striking down the Biden administration’s student debt relief plan today, and a separate student loan payment moratorium set to end, headwinds to the consumer spending outlook continue to build heading into the second half of 2023.

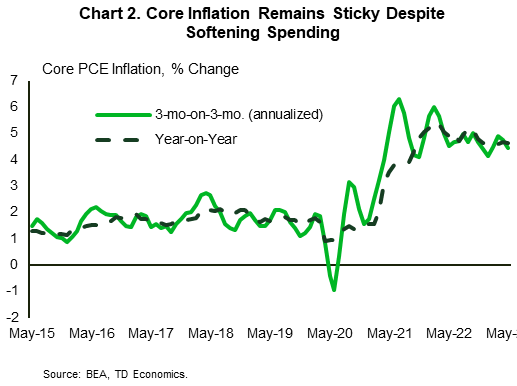

However, inflation continues to be problematic. Core PCE inflation (Chart 2) is showing little sign of relenting, up 4.6% y/y, with the near-term trend cruising along at 4.4% (annualized). Inflation has been stuck well above the two percent target, which is likely to keep officials focused on tightening policy to cool it down. Markets are looking for the Fed to hike rates again this year by another 25 basis points – taking the policy rate to a 22-year high of 5.5%. The FOMC’s next decision is at the end of July, giving it some time to see a few more readings on economic momentum before making its decision. Next week’s June jobs data is likely to be a key piece of it’s calculus.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of June 16th, 2023

Financial News Highlights

- The Federal Reserve met expectations and held the policy rate steady at 5.0-5.25%, but left the door open to further rate hikes later this year.

- The Fed’s Summary of Economic Projections underscored a more optimistic outlook, and an upward revision on the future path of the fed funds rate to 5.75% (previously 5.25%).

- Retail sales data for May came in stronger than expected, underscoring a still resilient consumer. Inflation data came in on expectations, with the headline and core measure up 4.0% and 5.3%, respectively.

Keepin’ At It… For Now

There were few surprises on the economic front this week in financial news. As widely expected, the Federal Reserve held the policy rate steady, after 10 consecutive increases over the past 15 months. Little changed in the statement, though the revised Summary of Economic Projections (SEP) underscored a more hawkish trajectory for the fed funds rate. And rightfully so. Retail sales and inflation data out this week continued to reflect a degree of inertia still present in the U.S. economy, which will likely necessitate a bit more ‘work’ from the FOMC through the remainder of this year.

Focusing on the major changes in the SEP, the FOMC revised its economic outlook higher for 2023. Real GDP growth is now expected to be 1.0% by year-end (previously 0.4%), and the unemployment rate was lowered to 4.1% (previously 4.5%). The inflation outlook was also revised higher, with the median forecast on core PCE now at 3.9% (previously 3.6%). With a stronger economic outlook and higher expected inflation, the median projection on the future path of the policy rate was raised by 50-bps to 5.6% – suggesting a terminal policy rate of 5.75%.

At the subsequent press conference, Fed Chair Powell was pressed on the timing of the potential future rate hikes. While remaining non-committal, Powell emphasized that the July meeting remained ‘live’, and the decision would ultimately be determined by the ‘totality’ of the data flow. From that perspective, a July hike seems more likely than not.

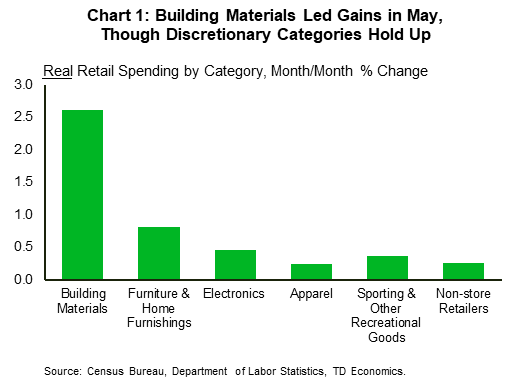

Data out this week on retail sales showed that consumer spending is still humming at a decent clip. Total retail sales rose 0.3% m/m in May, well ahead of the consensus forecast calling for a pullback of 0.2%. After stripping out food and gasoline, sales were even stronger – rising 0.4% m/m. While gains were led by building materials – an inherently volatile category – there was enough breadth across other discretionary categories to suggest that the ‘resilient’ narrative remains intact (Chart 1) in financial news. Our current tracking for Q2 spending sits between 1.5%-2%. While this represents a deceleration from Q1’s 3.8%, spending is still running far too hot to meaningfully cool inflation. This was evident in the May inflation data.

CPI rose by just 0.1% m/m, though the more subdued headline reading was the result of falling energy prices and slower food inflation. Core inflation (excludes food & energy), rose by a more notable 0.4% m/m with the 12-month change ticking down just 0.2%-pts to 5.3%. Sizeable contributions from both used vehicle prices and shelter were responsible for much of last month’s core gains. Excluding these two items shows a more subdued pace of price growth, with prices up just 0.1% m/m or 4.2% y/y (Chart 2). While stripping out individual categories is sometimes a dangerous game to play, there’s good reason to believe that both have downside over the coming months. This reinforces the notion that getting inflation down from today’s +5% reading to 3% over the next year is very feasible. It’s the last leg lower (from 3% to 2%) that will be the biggest challenge for the Fed, hence the need for policymakers to ‘keep at it’ for the time being.

Thomas Feltmate, Director | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of June 9th, 2023

Financial News Highlights

- The ISM Services index surprised on the downside, falling 1.6 points to 50.3 in May. The employment sub-index drifted below the 50-point contractionary threshold for the first time since December.

- Initial jobless claims rose by 28,000 in the week ending on June 3rd, lifting initial claims to 261,000 – the highest level in 20 months. However, this week included the Memorial Day holiday, which may have distorted the data.

- The U.S. trade deficit jumped by $14 billion or 23% in April to $74.6 billion – the widest level in six months. The widening of the trade deficit in April indicates that trade is likely to subtract from growth in the second quarter.

Mild Signs of a Slowdown Continue

In the wake of last week’s debt ceiling deal (see report), markets had the opportunity to catch their breath in a quiet week for data releases in financial news. The ISM Services report disappointed, with the headline index falling 1.6 points to 50.3 in May, instead of improving moderately to 52.4 as per market expectations. The recent downtrend reflects an economy that is gradually decelerating, echoing the ‘slowdown’ narrative advanced by its manufacturing counterpart (Chart 1). This theme was further supported by the report’s details, with all the main sub-indicators – including business activity, new orders, and employment – declining on the month. Of note, the employment index fell 1.6 points to 49.2, drifting below the 50-point contractionary threshold for the first time since December.

In the wake of last week’s debt ceiling deal (see report), markets had the opportunity to catch their breath in a quiet week for data releases in financial news. The ISM Services report disappointed, with the headline index falling 1.6 points to 50.3 in May, instead of improving moderately to 52.4 as per market expectations. The recent downtrend reflects an economy that is gradually decelerating, echoing the ‘slowdown’ narrative advanced by its manufacturing counterpart (Chart 1). This theme was further supported by the report’s details, with all the main sub-indicators – including business activity, new orders, and employment – declining on the month. Of note, the employment index fell 1.6 points to 49.2, drifting below the 50-point contractionary threshold for the first time since December.

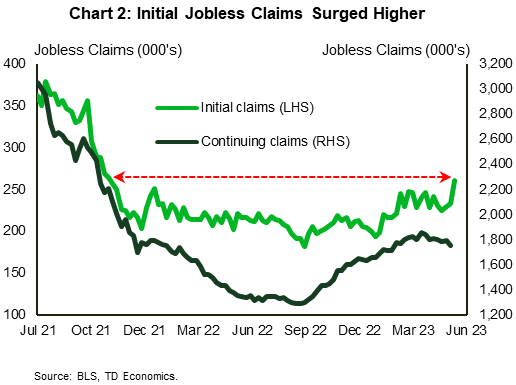

Continuing with signs for some potential softening in the labor market, initial jobless claims surged higher in the week ending on June 3rd, rising by 28,000 – much more than anticipated. This lifted initial claims to 261,000 – the highest level in 20 months (Chart 2). While the increase is substantial, for now we caution against reading too much into this in financial news. The weekly data can be noisy, and the week included the Memorial Day holiday, which may have also injected some volatility. Secondly, looking at seasonally unadjusted figures, the increase lacked breadth across states, as it was concentrated in Ohio, California, and Minnesota.

April’s international trade report did little to lift the mood. The U.S. trade deficit jumped by $14 billion or 23% in April to $74.6 billion – the widest level in six months. The most noticeable change was in the goods category. The U.S. goods deficit grew by close to 18%, as exports fell 5.3% and imports grew 2%, with the latter marking a rebound after two consecutive monthly declines. Trade made no contribution to economic growth in the first quarter of this year. The widening of the trade deficit in April indicates that it is likely to subtract from growth in the second quarter.

All told, the few reports that came out this week point to growth in the U.S. economy moderating. The Fed will take this information into account before it meets next week to set monetary policy. The last major piece of information on the docket before the Fed makes its decision is May’s CPI inflation report, which comes out one day ahead of the FOMC meeting. The market consensus forecast calls for core CPI to ease moderately to 5.3% year-on-year in May from 5.5% in April. Surprise rate hikes from the Reserve Bank of Australia and the Bank of Canada earlier this week serve as a reminder that amidst stubborn inflation there’s the potential for the Fed to opt for a hike too. That said, Fed officials have been vocal in signaling that they will forego a hike at next week’s meeting. Market odds are in tune with this view, attaching a 75% probability to a stand pat decision next week (as tracked by CME Group). However, markets still narrowly favor a hike at the next meeting in July (52% odds). In short, while next week is likely to be uneventful regarding policy changes, Fed communication may offer additional insight as to whether the FOMC sees the need for some further tightening over the near-term or not.

All told, the few reports that came out this week point to growth in the U.S. economy moderating. The Fed will take this information into account before it meets next week to set monetary policy. The last major piece of information on the docket before the Fed makes its decision is May’s CPI inflation report, which comes out one day ahead of the FOMC meeting. The market consensus forecast calls for core CPI to ease moderately to 5.3% year-on-year in May from 5.5% in April. Surprise rate hikes from the Reserve Bank of Australia and the Bank of Canada earlier this week serve as a reminder that amidst stubborn inflation there’s the potential for the Fed to opt for a hike too. That said, Fed officials have been vocal in signaling that they will forego a hike at next week’s meeting. Market odds are in tune with this view, attaching a 75% probability to a stand pat decision next week (as tracked by CME Group). However, markets still narrowly favor a hike at the next meeting in July (52% odds). In short, while next week is likely to be uneventful regarding policy changes, Fed communication may offer additional insight as to whether the FOMC sees the need for some further tightening over the near-term or not.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of June 2nd, 2023

Financial News Highlights

- Congress passes a deal to suspend the debt limit, averting the “worst case scenario” of a default.

- Today’s Nonfarm Payrolls Report featured a big jobs gain (+339k) and a pop in the unemployment rate (+0.3 percentage points).

- The health in the labor market is consistent with our view that policy easing won’t come until at least the first quarter of next year.

Labor Market Stays Hot Despite Rising Unemployment Rate

With Congress passing a deal to suspend the debt limit and avoiding a default, all eyes were focused on this morning’s non-farm payrolls report. Hiring rose by a robust +339k, which came in well above the consensus forecast of 195k in major financial news. Looking forward, markets are now expecting the Fed will have to keep rates higher for longer to cool the economy and inflation.

With Congress passing a deal to suspend the debt limit and avoiding a default, all eyes were focused on this morning’s non-farm payrolls report. Hiring rose by a robust +339k, which came in well above the consensus forecast of 195k in major financial news. Looking forward, markets are now expecting the Fed will have to keep rates higher for longer to cool the economy and inflation.

Turning to the specifics of debt ceiling deal, Congress passed the Fiscal Responsibility Act of 2023 which will suspend the debt ceiling for two years and avert a default on U.S. debt (link). The deal caps discretionary spending for 2024-2025 and will have a modest effect on reducing the deficit over that time horizon. Moreover, the overall impact on the economy should be modest with the peak impact coming in 2024 and the possibility of shaving 0.1% off GDP growth.

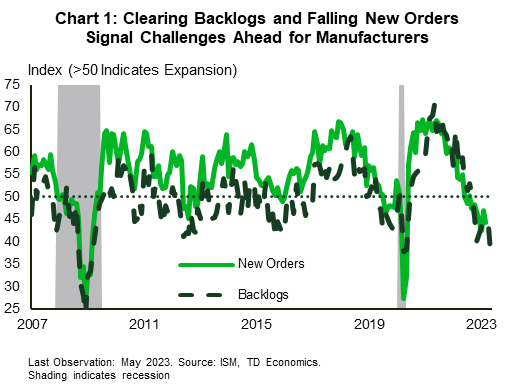

The economic data out this week showed U.S. manufacturing activity continues to feel the pinch from higher rates and a pullback in demand. The ISM manufacturing index registered a 46.9 reading – well short of the 50 print indicating growth. This is now the seventh consecutive month of contraction for the sector and the outlook in the coming months is decidedly gloomy in financial news. New orders contracted again (at a faster pace than the month prior) and the backlogs in business that have helped keep factories humming cleared at their fastest pace since the Global Financial Crisis (Chart 1). There was a silver lining to the report as the transportation sector did report an expansion for the month of May – helping it continue its recovery amid ongoing tight supplies. Indeed, despite vehicle sales in May coming in slightly below expectations (15.1 million annualized vs. the 15.3 million annualized expected) the details of the report show that pent-up demand is still being cleared and the industry remains undersupplied.

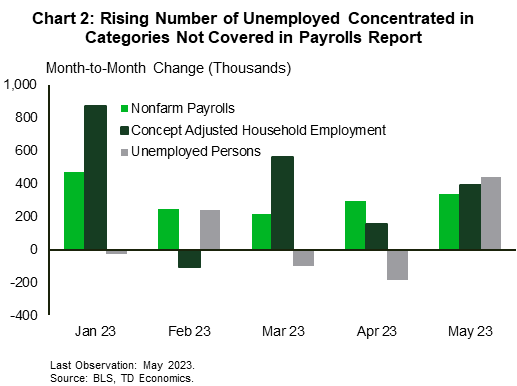

The weakness in the manufacturing sector was expected and stands in stark contrast to what’s happening across the rest of labor market. Nonfarm payrolls grew by 339k position in May, blowing past expectations for a more modest expansion of 195k. The bulk of the growth came from the services side – adding 257k positions in May – though construction (+25k) and government (+56k) all chipped in with healthy gains. However, this blowout print was accompanied by a 440k increase in the number of unemployed in the household survey – lifting the unemployment rate 30 basis points to 3.7%. Excluding the lockdown phase of the pandemic, this is the steepest rise in the jobless rate since November 2010. However, take the rise with a grain of salt, as the concept adjusted household employment that excludes categories like agricultural and household workers and adds in multiple job holders to make it comparable to the payrolls numbers, showed a still healthy 394k gain (Chart 2).

The weakness in the manufacturing sector was expected and stands in stark contrast to what’s happening across the rest of labor market. Nonfarm payrolls grew by 339k position in May, blowing past expectations for a more modest expansion of 195k. The bulk of the growth came from the services side – adding 257k positions in May – though construction (+25k) and government (+56k) all chipped in with healthy gains. However, this blowout print was accompanied by a 440k increase in the number of unemployed in the household survey – lifting the unemployment rate 30 basis points to 3.7%. Excluding the lockdown phase of the pandemic, this is the steepest rise in the jobless rate since November 2010. However, take the rise with a grain of salt, as the concept adjusted household employment that excludes categories like agricultural and household workers and adds in multiple job holders to make it comparable to the payrolls numbers, showed a still healthy 394k gain (Chart 2).

With this backdrop markets are as bracing for the possibility of another Fed hike by mid-summer and a delayed start to rate cuts. The need for rates to remain in restrictive territory for longer is in line with our view that policy easing won’t come until 2024Q1.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of May 26th, 2023

Financial News Highlights

- Negotiators appeared close to a deal to raise the debt ceiling and set spending levels. However, the deal does not address Washington’s medium-term fiscal challenges, which were part of the reason Fitch put the U.S. on a negative watch.

- Consumers continued to spend at a healthy clip in April, contributing to sustained inflation pressures. We continue to expect spending to cool as the year goes on, helping to ease inflation, eventually.

- In the meantime, the Fed is in a tough spot. It will need courage to pause and wait for the full impact of its past tightening to show up.

“Discretion” Is the Better Part of Valor in Washington

Thankfully, negotiators appeared close to a deal to raise the debt ceiling as of Friday morning in financial news. It looks like the two-year deal would cap discretionary spending and raise the debt ceiling through the 2024 election, avoiding the worst-case scenarios. However, ratings agency Fitch had cited the “failure of the U.S. authorities to meaningfully tackle medium-term fiscal challenges” as a reason for putting the U.S. on a negative watch, and this deal does not change that.

Thankfully, negotiators appeared close to a deal to raise the debt ceiling as of Friday morning in financial news. It looks like the two-year deal would cap discretionary spending and raise the debt ceiling through the 2024 election, avoiding the worst-case scenarios. However, ratings agency Fitch had cited the “failure of the U.S. authorities to meaningfully tackle medium-term fiscal challenges” as a reason for putting the U.S. on a negative watch, and this deal does not change that.

Congress has taken the Shakespearean proverb “discretion is the better part of valor” literally. The Bard’s original intention was a criticism of a lack of honour and courage in focusing on discretion. The debt ceiling deal only tinkers around the edges of the larger issue of a structural deficit on the order of 6% of GDP.

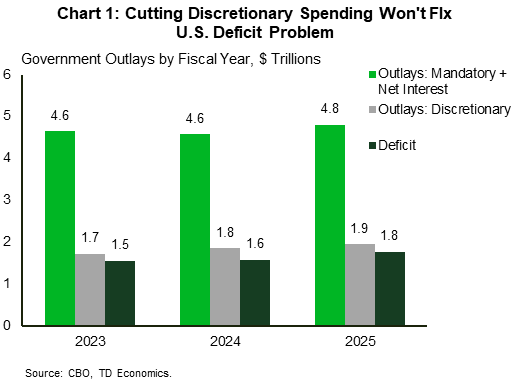

Discretionary spending accounts for only 27% of total federal government outlays, and the federal deficit is estimated to be $1.5 trillion in 2023. As shown in Chart 1, Congress would need to cut discretionary spending nearly to zero to balance the books if they only address discretionary spending. To seriously address the deficit, it needs to take the more courageous steps and look at mandatory spending – namely entitlements like social security and Medicare. Or, it needs to find a way to grow revenues at the same pace as population aging. Alas, courage seems in short supply in Congress these days.

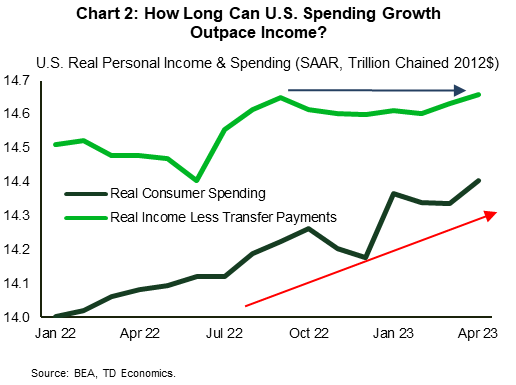

Speaking of discretion in spending, real consumer spending was up a healthy 0.5% month-on-month in April in financial news. Spending was driven by robust gains in outlays on both goods and services. Monthly spending data has been very choppy over the past six months but comparing it to real income less transfer payments (which is a key recession indicator used by the NBER), you see that the upward trend in spending is outpacing real income growth (Chart 2).

Thanks to a strong labor market, real income gains have held up. Added to the cushion of excess savings built up during the pandemic, the consumer has been able to keep spending in the face of very high inflation, in turn contributing to demand-driven inflation pressures. Chart 2 suggests that spending is set to slow – even if the labor market doesn’t cool. About 60% of the excess savings cushion has been spent, and spending cannot outgrow income indefinitely before consumers will need to tighten their belts.

Thanks to a strong labor market, real income gains have held up. Added to the cushion of excess savings built up during the pandemic, the consumer has been able to keep spending in the face of very high inflation, in turn contributing to demand-driven inflation pressures. Chart 2 suggests that spending is set to slow – even if the labor market doesn’t cool. About 60% of the excess savings cushion has been spent, and spending cannot outgrow income indefinitely before consumers will need to tighten their belts.

We expect that belt tightening to be in greater evidence as the year goes on. After consumer spending grew by 3.8% annualized in Q1, it is tracking a more modest 2% in Q2. We expect it to fall below 1% in the second half of the year, which will help to dampen inflationary pressures. Until then, the Fed is on the horns of a dilemma.

Its preferred inflation gauge, the core PCE deflator, remained around where it has been all year at 4.7% year/year in April. Markets are judging this could mean the Fed should push a bit harder on rates, with market odds tilting slightly in favor of another hike in June. We believe that the Fed will need to hold its courage and pause and assess the impact of the significant monetary policy tightening that has not yet had its full impact on economic growth.

Leslie Preston, Managing Director & Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of May 19th, 2023

Financial News Highlights

- Financial markets remained eerily positive this week, despite the debt ceiling X-date looming with no bipartisan deal in sight.

- Retail sales data for April showed the continued resilience of the U.S. consumer, while housing starts are looking to have reached a bottom after having fallen 24% last year. Home sales were lower in April, and likely have a bit further to fall.

- Fed speakers diverged this week on the near-term trajectory of the fed funds rate. Financial markets are still pricing 50 bps of rate cuts by year-end.

Optimistic Markets Cheer the Small Wins

Risk sentiment remained eerily positive across global financial markets this week, despite the clock ticking down on the debt ceiling X-date (see report) in financial news. But instead of losing the forest for the trees, investors seemed to cheer the incremental progress made this week. President Biden and Speaker McCarthy, and their negotiators, met on Tuesday for a closed-door meeting, where there appears to be some common ground on several items including clawing back unspent pandemic relief funds, speeding up permitting of domestic energy projects, and applying stricter work requirements for some social safety net programs. However, the two parties remain deeply divided on the size of broader spending cuts. At the time of writing, equity markets are looking to end the week up 2%, while the 10-year Treasury is up 25 bps to 3.71%.

Risk sentiment remained eerily positive across global financial markets this week, despite the clock ticking down on the debt ceiling X-date (see report) in financial news. But instead of losing the forest for the trees, investors seemed to cheer the incremental progress made this week. President Biden and Speaker McCarthy, and their negotiators, met on Tuesday for a closed-door meeting, where there appears to be some common ground on several items including clawing back unspent pandemic relief funds, speeding up permitting of domestic energy projects, and applying stricter work requirements for some social safety net programs. However, the two parties remain deeply divided on the size of broader spending cuts. At the time of writing, equity markets are looking to end the week up 2%, while the 10-year Treasury is up 25 bps to 3.71%.

Turning to the economic data, retail sales data painted a picture of a still resilient consumer in April. Although headline retail sales (+0.4% m/m) came in below expectations (+0.8% m/m), this was partially the result of a pullback in gasoline sales – largely a price- driven decline. The headline was also weighed down by weaker growth in motor vehicle sales, despite wholesale auto sales showing a healthy gain last month in financial news. After removing the volatile items, the control group – a more precise measure of consumer spending – rose by a healthy 0.7% m/m. This suggests continued momentum for Q2 consumer spending, with our current tracking around 1%-1.5%.

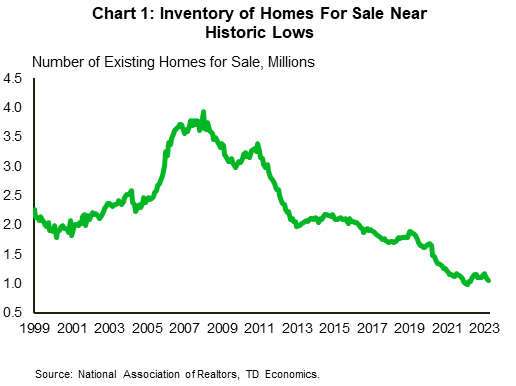

Data out this week on the housing market showed existing home sales fell by 3.4% m/m to 4.28 million units in April. The pullback comes after sales had shown signs of life earlier this year. However, much of that activity was the result of a pullback in mortgage rates that had occurred between October-January. Since then, mortgage rates have again turned higher, and at 7.1%, are not far off last year’s highs. Not only has this kept new homebuyers on the sidelines, but it has also discouraged move-up buyers from listing properties, which has kept inventory levels near historic lows (Chart 1).

Data out this week on the housing market showed existing home sales fell by 3.4% m/m to 4.28 million units in April. The pullback comes after sales had shown signs of life earlier this year. However, much of that activity was the result of a pullback in mortgage rates that had occurred between October-January. Since then, mortgage rates have again turned higher, and at 7.1%, are not far off last year’s highs. Not only has this kept new homebuyers on the sidelines, but it has also discouraged move-up buyers from listing properties, which has kept inventory levels near historic lows (Chart 1).

While home sales likely have a bit more room to fall, housing starts may have already reached a bottom. Residential construction rose 2.2% m/m to 1.4 million in April, with gains seen across both the multifamily (+3.2% m/m) and single-family (+1.6% m/m) segments. Permitting activity points to an uptick in construction in the single-family segment over the coming months, though this will likely be offset by some pullback in multifamily, which has yet to feel any correction through this tightening cycle (Chart 2).

Several Fed speakers this week showed a growing divergence among committee members on the near-term trajectory of the fed funds rate. While a few officials endorsed another rate hike, others are favoring a pause given the recent banking turmoil and the uncertainness it poses to the economic outlook. However, all officials still support rates remaining elevated through this year, which remains at odds with market pricing where 50 bps of cuts are still expected by year-end.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of May 12th, 2023

Financial News Highlights

- Inflation eased modestly in April, with headline and core CPI both ticking down by 0.1 percentage points to 4.9% and

5.5% year-on-year respectively. - The Federal Reserve’s Senior Loan Officer Opinion Survey showed that a higher share of commercial banks tightened

credit conditions in April than January. - A meeting between President Biden and Congressional leaders failed to yield any progress on negotiations to raise/suspend

the debt limit.

Inflation Continues to Cool in Earnest

On the heels of last week’s FOMC meeting, we were provided with a host of economic data this week to assess the Fed’s new wait-and-see approach, including April’s CPI report in financial news. In addition, we also received the second quarter Senior Loan Officer Opinion Survey (SLOOS) and had a meeting between President Biden and Congressional leadership as they attempt to find an agreement to raise the debt limit. Markets ended the week relatively unchanged, with the S&P 500 down 0.1% and the ten-year Treasury Yield down 4bps at 3.41% as of the time of writing.

On the heels of last week’s FOMC meeting, we were provided with a host of economic data this week to assess the Fed’s new wait-and-see approach, including April’s CPI report in financial news. In addition, we also received the second quarter Senior Loan Officer Opinion Survey (SLOOS) and had a meeting between President Biden and Congressional leadership as they attempt to find an agreement to raise the debt limit. Markets ended the week relatively unchanged, with the S&P 500 down 0.1% and the ten-year Treasury Yield down 4bps at 3.41% as of the time of writing.

Inflation eased modestly in April, as headline inflation rose by 4.9% year-on-year, down modestly from 5% in March (Chart 1). Energy prices rose for the first time in three months as gasoline jumped by 3% month-on-month (m/m), and food prices were flat for a second consecutive month. Stripping out energy and food, core inflation ticked down to 5.5% y/y, having fluctuated between 5.5-5.6% y/y since January in financial news. While we did see shelter inflation decelerate for a second consecutive month, it still rose by 0.4% m/m. This in addition to the reacceleration in core goods inflation, worked to keep core inflation elevated. Although on aggregate this report had positive developments, it reiterated the fact that the path back to the Fed’s 2% target is unlikely to be a straight line.

Of particular concern for the Fed is the potential for inflation expectations to become de-anchored. In the New York Fed’s Survey of Consumer Expectations this week, we saw three-year ahead inflation expectations rise for a second consecutive month to 2.9% in April (Chart 2). While this series has historically run slightly above the Fed’s 2% target, a sustained movement above 3% would be a concern for the FOMC.

Earlier in the week, we saw that U.S. commercial banks continued to tighten credit conditions in April in the Fed’s SLOOS. Commercial & industrial loans as well as commercial real estate (CRE) loans saw a higher net percentage of banks tightening credit standards than in January. Demand for these loans from businesses fell as a result, however household demand for consumer-facing loans (mortgages, auto, credit card, etc.) rose as credit remained relatively accessible. Further analysis of the SLOOS can be found here.

Earlier in the week, we saw that U.S. commercial banks continued to tighten credit conditions in April in the Fed’s SLOOS. Commercial & industrial loans as well as commercial real estate (CRE) loans saw a higher net percentage of banks tightening credit standards than in January. Demand for these loans from businesses fell as a result, however household demand for consumer-facing loans (mortgages, auto, credit card, etc.) rose as credit remained relatively accessible. Further analysis of the SLOOS can be found here.

Lastly, in the Oval Office this week, President Biden met with Congressional leaders on Tuesday to attempt to find an agreement to raise/suspend the debt limit. Treasury Secretary Yellen warned last week that the Treasury could run out of funds by early June, thus the impetus to reach an agreement is elevated. However, no progress has been made in the negotiations so far.

Looking ahead to next week, we will get a fresh update on the U.S. consumer with April retail sales as well as existing home sales. With the unemployment rate back down to 3.4% consumers may still have some wind in their sails, but we expect that this will be short-lived as past rate hikes continue to filter through the economy.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.