Featured Article: In Retirement, We Have More Time Than Ever. But We Want to Use It Wisely.

In Retirement, We Have More Time Than Ever. But We Want to Use It Wisely.

We have fantasized about this moment for decades. The trick is learning how to savor it.

Steve

Stephen Kreider Yoder

For the first time in many years, time isn’t money.

That was never more clear one afternoon earlier this year when we were gazing down at the Mediterranean Sea while sipping coffee in a cafe in the town plaza in Bejaia, Algeria. We had no fixed plans for the day or the next week—just as planned.

We suddenly have time in abundance, now that we’re both retired, and we’re learning how to spend this currency that for decades has been so scarce. We can now linger where we want to be and dally over what we want to do.

Algeria was an ideal place to test this new reality. We had visited in 2019, but could afford only two weeks, what with full-time jobs—far too short for a country roughly 3.5 times the size of Texas. “We need more time there,” I said as we flew home.

This year, we could take nearly twice as long to immerse ourselves in what the country offered: a green coastal region that gives way to the golden Sahara; a mosaic of Arab, Berber, French and other cultures; Roman Empire ruins; good food and wine; some of the most hospitable people we’ve met.

We’ve been fantasizing about this time in life since we got married. For decades, time was a rare commodity, and we had to spend a lot of money to acquire it. We paid an absurd price for a house in San Francisco, partly to limit our commutes. We often hired others to do tasks I enjoyed, like fixing our cars or restoring the trim on our Victorian.

“We need more time” was our constant lament, at no time more than during travel. We would shoehorn several countries into two-week tours. We liked to travel abroad on a low budget—it got us closer to the reality of wherever we were—but that took time, and we often didn’t have the luxury.

We have it now. Earlier this year, we rode the Amtrak California Zephyr to Iowa, rather than flying, to see my parents. It was about 48 hours each way, but what was the hurry? We got beds, three meals a day and a rolling display of Western America. We extended our stay with Mom and Dad to a full week.

Back home, I fired up the metal lathe to fine-tune a bearing-cup press I had made earlier—a bike tool that worked fine but which I had great fun fussing with for hours to refine it. I’ll soon solicit bids for scaffolding, so I can start restoring trim.

It’s beginning to occur to us: By saving money assiduously during our 44 years of marriage, we weren’t putting away only funds. We were also accumulating time to spend in retirement.

Money, at long last, is time.

Karen

Karen Kreider Yoder

I’ve never been more aware of the finite nature of time. We’re rich with it now, but there’s no guarantee how long those riches will last. At best, thanks to the longevity that runs in our families, we may have 30 good years of life left. That feels like a long time—and no time at all.

So I’ve been thinking: Maybe we should be budgeting our time like we budget money.

Should I, for instance, spend some of my newfound wealth of time on things I’ve loved to do all my life but had to cut back on while I was working? During the busy years of my career, I continued to make quilts, but had to leave many undone. I baked my own granola and whipped up many meals for friends, but found myself ordering out or picking up prepared foods from the grocery store to save time.

Yet now that I have the luxury of time, the opportunities to fill it have also grown. And that means I still find myself weighing how to spend it—and when to keep spending money instead. I still love to create things, for instance, but would I rather sew an original outfit from scratch or shop for a less-original affair and bank the time? We have time to do housecleaning now; does that mean we should stop paying someone else to do it once a month?

These aren’t easy questions. As a result, we’re talking about looking at all the large time expenditures on our list—travel, house work, volunteering, organizing photos—and laying them out on an annual budget. That will help us use our time more wisely.

As we talked about in our last column, we also need to do a better job savoring—as opposed to just running through—the time we have. That hit home on our trip to the Algerian Sahara this year. We had blocked off a week to explore the desert, far longer than we would have during preretirement travel. We could finally take a leisurely pace, we told ourselves.

Yet we couldn’t shake the old urge to make each hour pay off. My question when we arrived the first night: “When should we be ready for breakfast in the morning?”

Our Tuareg guide, Habib, laughed. “You get up when you want,” he said. “In the desert, slowly, slowly.”

That became our mantra for the next days as we camped each night in a different swath of the wilderness. We sat around a low table for our morning coffee and baguette with fig jam. “Slowly, slowly,” Habib would say, and we would repeat it after him.

“Slowly, slowly,” he cautioned as we set off scrambling over rocks toward ancient pictographs. After lunch under a cool tree, we would chat and read and nap. “Slowly, slowly,” we would chant, and again in the evening as Habib stoked a small fire to heat tea, pouring it back and forth between two pots until it foamed into a thick, sweet brew. We brought that mantra home from Algeria. We’ve got time now, and if we budget it carefully, we can afford to spend it slowly, slowly.

The Yoders live in San Francisco and can be reached at reports@wsj.com.

To see more fantastic articles like this one, please see here.

Financial News for the Week of May 5th, 2023

Financial News Highlights

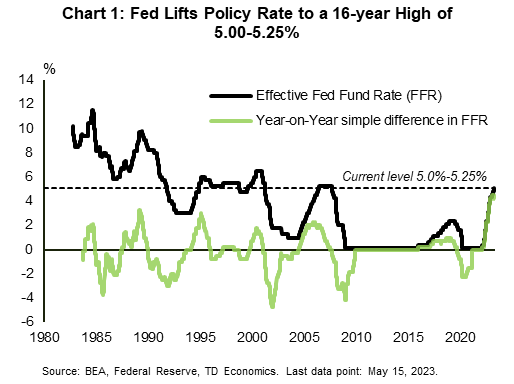

- The Federal Reserve hiked the policy rate 25 basis points this week, lifting it to a 16-year high of 5.00-5.25%. Changes in FOMC statement hinted at the potential for a pause, though Chair Powell stated that such a decision had not been made.

- The banking stress continues to fester, with this week marking the failure of another bank (First Republic).

- Though still slowing on a trend basis, hiring ticked up in April, with the economy adding 253k jobs. That was above market expectations for a gain of 180k, but downward revisions to the prior months tempered the optimism.

Fed Lifts Policy Rate to a 16-year High

The Fed followed through with its highly anticipated decision to hike the policy rate by 25 basis points (bps) this week in financial news. This lifted the fed funds rate to 5.00-5.25% – the highest level in 16 years – in what has been a historically aggressive hiking cycle (Chart 1). Changes in the FOMC statement hinted at the potential for a pause, so this could very well be the last hike of this cycle. But, stating this explicitly would not serve the Fed well at this point. In the press conference, Chair Powell tried to keep his options open, stating bluntly that a decision on a pause had not been made.

The Fed followed through with its highly anticipated decision to hike the policy rate by 25 basis points (bps) this week in financial news. This lifted the fed funds rate to 5.00-5.25% – the highest level in 16 years – in what has been a historically aggressive hiking cycle (Chart 1). Changes in the FOMC statement hinted at the potential for a pause, so this could very well be the last hike of this cycle. But, stating this explicitly would not serve the Fed well at this point. In the press conference, Chair Powell tried to keep his options open, stating bluntly that a decision on a pause had not been made.

The Fed’s communication is at odds with market expectations. Markets are dismissing the possibility of further rate hikes and are instead signaling that after a brief pause the Fed will begin cutting rates. Market odds as tracked by the CME Group point to 75 bps in cuts over the last few months of the year. Asked about this divergence, Powell pushed back against the notion of soon-to-come cuts in financial news. In his words, the reasoning is that the Fed sees inflation coming down “not so quickly”, and that if that outlook proves to be broadly correct then “it would not be appropriate to cut rates”.

Fed Chair Powell noted that upcoming policy rate decisions would ultimately be data-dependent, mentioning the usual suspects (i.e., inflation and labor market metrics), while also putting a focus on credit conditions. Tighter credit conditions ultimately serve a similar purpose to rate hikes when it comes to cooling economic growth and inflation. This is something that the Fed considers in setting monetary policy, especially in light of the recent banking stress, with this week marking the failure of another regional bank. Powell had access to the Senior Loan Officer Opinion Survey (SLOOS), due to be released publicly on Monday, and noted that it would show a tightening in credit conditions among small and medium sized banks.

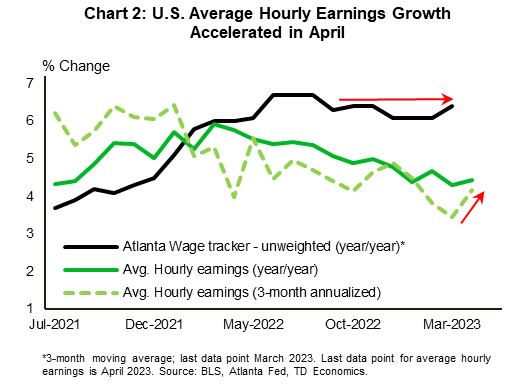

Factoring in the banking stress and tighter credit conditions suggests that the Fed has done enough, but labor market resilience continues. On the one hand, the pace of job creation continues to trend down on a three-month moving average basis. On the other hand, it’s hard to discount the strength in the April jobs report. The economy added 253k jobs last month – well above expectations for 180k. Gains were concentrated in service sectors (+197k). The labor force participation rate held flat at post-pandemic high of 62.6%, while the unemployment rate ticked down to 3.4%, matching January’s multi-decade low. Amidst the ongoing tightness in the labor market, growth in average hourly earnings accelerated both on a year-on-year and month-on-month basis, while other wage measures also point to some resilience (Chart 2).

Factoring in the banking stress and tighter credit conditions suggests that the Fed has done enough, but labor market resilience continues. On the one hand, the pace of job creation continues to trend down on a three-month moving average basis. On the other hand, it’s hard to discount the strength in the April jobs report. The economy added 253k jobs last month – well above expectations for 180k. Gains were concentrated in service sectors (+197k). The labor force participation rate held flat at post-pandemic high of 62.6%, while the unemployment rate ticked down to 3.4%, matching January’s multi-decade low. Amidst the ongoing tightness in the labor market, growth in average hourly earnings accelerated both on a year-on-year and month-on-month basis, while other wage measures also point to some resilience (Chart 2).

Should the strength seen in April extend in the months ahead, it could push the Fed to hike a bit more. However, other labor market indicators – such as job openings, which are trending down, and initial jobless claims, which continue to trend up – are not in tune with this view. All told, the upcoming data will continue to bear careful watching, with next week’s CPI report next under the magnifying glass.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of April 28th, 2023

Financial News Highlights

- U.S. real GDP growth slowed to 1.1% quarter-over-quarter (q/q) annualized in 2023 Q1, from 2.6% q/q in the previous quarter. A measure of underlying domestic demand accelerated to 2.9% q/q, supported by a strong gain in consumer spending, although the monthly pattern revealed that the spending gain was entirely concentrated in January.

- New home sales grew by 9.6% month-on-month in March. While this series is volatile, it has been trending up since the end of last year.

- Core PCE inflation remained elevated in March, easing modestly to 4.6% year-on-year from 4.7% in February.

Core Inflation Remains Elevated, Fed to Hike Next Week

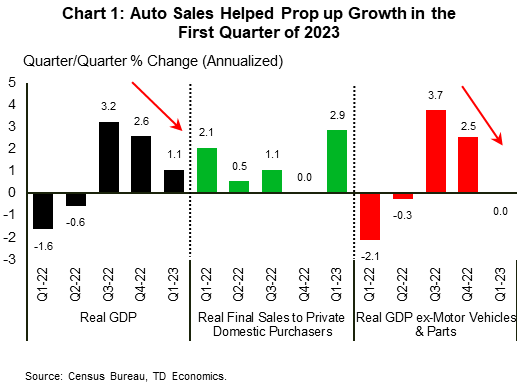

U.S. real GDP growth slowed to a 1.1% quarter-over-quarter (q/q) annualized pace in the first quarter of 2023, from 2.6% q/q at the end of 2022 in financial news. While consensus expectations were looking for a better print, a slowdown in growth was always in the cards as a reversal of the prior quarter’s inventory built-up was expected. That reversal materialized. Government spending, meanwhile, provided an offset, delivering a 0.8 percentage point (pp) contribution to growth. With the combined impact of inventories and government spending adding volatility to the data, we typically look past these items and focus on ‘final sales to private domestic purchasers’ to get a clearer reading of underlying domestic demand. After several quarters of slow growth, this measure accelerated to 2.9% q/q, supported by a strong gain in consumer spending (+3.7%).

U.S. real GDP growth slowed to a 1.1% quarter-over-quarter (q/q) annualized pace in the first quarter of 2023, from 2.6% q/q at the end of 2022 in financial news. While consensus expectations were looking for a better print, a slowdown in growth was always in the cards as a reversal of the prior quarter’s inventory built-up was expected. That reversal materialized. Government spending, meanwhile, provided an offset, delivering a 0.8 percentage point (pp) contribution to growth. With the combined impact of inventories and government spending adding volatility to the data, we typically look past these items and focus on ‘final sales to private domestic purchasers’ to get a clearer reading of underlying domestic demand. After several quarters of slow growth, this measure accelerated to 2.9% q/q, supported by a strong gain in consumer spending (+3.7%).

At face value, the acceleration in underlying domestic demand is good news. However, monthly spending data shows that the strength was concentrated in January, with growth flatlining over the next two months. Much of the quarter’s strength came from auto sales. Unit auto sales grew from 14.3 million (annualized) at the end of 2022, to 15.3 million in 2023 Q1, resulting in a 1.1 (pp) contribution to GDP. If we remove that impact, the rest of the economy recorded zero growth (Chart 1). While our forecast calls for motor vehicles sales to remain at a high level over the near-term, as pent-up demand is satiated by improved production (see here), this channel is unlikely to offer the same level of support in 2023 Q2.

Residential investment remained a growth detractor for the eight consecutive quarter, but its negative impact moderated noticeably as average declines of 26% q/q in the second half of 2022 eased to 4.2% q/q in 2023 Q1. We expect residential investment to be less of a drag this year, a message echoed by some moderate positive signals out of the housing market. New home sales, a volatile series, continue to trend up since the end of last year, rising 9.6% month-on-month in March. This is happening as tight supply conditions on the existing home market look to be driving some more action towards the new home market. That said, with housing affordability still exceptionally low, buyers are showing increased sensitivity to mortgage rates (though with the typical lag). An index tracking the number of contracts signed to purchase existing homes, a reliable indicator of closed sales, fell 5.2% in March amidst an uptrend in mortgage rates earlier in the month in financial news. The stress in regional banking is also likely to have contributed to the hesitation among buyers to sign housing contracts.

Residential investment remained a growth detractor for the eight consecutive quarter, but its negative impact moderated noticeably as average declines of 26% q/q in the second half of 2022 eased to 4.2% q/q in 2023 Q1. We expect residential investment to be less of a drag this year, a message echoed by some moderate positive signals out of the housing market. New home sales, a volatile series, continue to trend up since the end of last year, rising 9.6% month-on-month in March. This is happening as tight supply conditions on the existing home market look to be driving some more action towards the new home market. That said, with housing affordability still exceptionally low, buyers are showing increased sensitivity to mortgage rates (though with the typical lag). An index tracking the number of contracts signed to purchase existing homes, a reliable indicator of closed sales, fell 5.2% in March amidst an uptrend in mortgage rates earlier in the month in financial news. The stress in regional banking is also likely to have contributed to the hesitation among buyers to sign housing contracts.

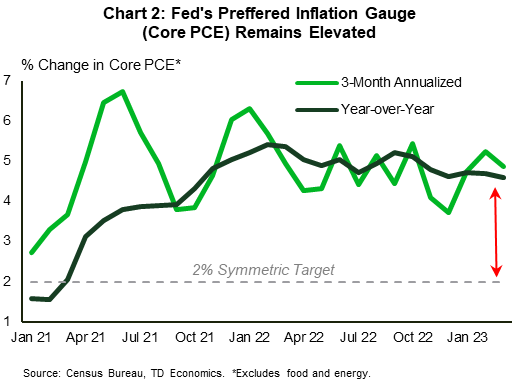

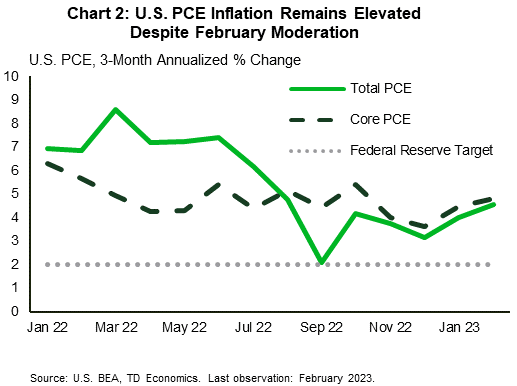

In weighing the Fed’s next interest rate decision, the latest PCE report showed that the Fed’s preferred inflation gauge remained elevated in March. While overall PCE slowed noticeably to 4.2% year-on-year (y/y), from 5.1% in the month prior, core PCE eased only modestly to 4.6% y/y (Chart 2). In our view, core PCE inflation has a long way to return to target (see here). As such, we expect the Fed to hike by 25 basis points next week and keep the policy rate at that high level through the end of the year.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of April 21st, 2023

Financial News Highlights

- China’s economy saw solid growth in the first quarter, with a strong rebound in consumption and exports after lockdowns were lifted at the end of last year.

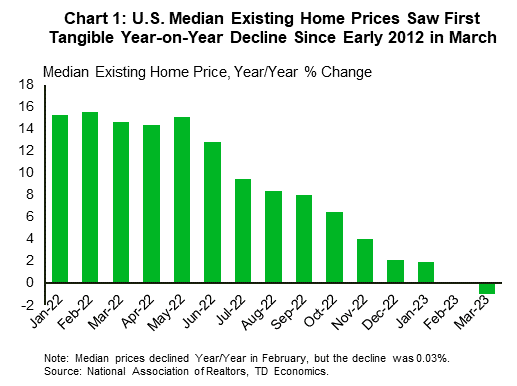

- U.S. existing home sales fell by 2.4% month-on-month (m/m) in March, falling from February’s revised 13.8% m/m uptick as past mortgage rate increases weighed on demand.

- FOMC members noted that they continue to monitor credit conditions, but many seem to be in favor of further policy tightening at the next meeting in May.

Housing Falls as the Fed Blackout Period Begins

As earnings season picked up pace this week, markets were closely attuned to the first quarter performance of U.S. companies in financial news. However, the net result on equity markets was muted, as results that were on aggregate moderately positive were partially overshadowed by the downbeat outlook for demand amid the expected economic slowdown later this year. As of the time of writing, the S&P 500 is down 0.5% on the week while the ten-year Treasury yield is up 5 basis-points (bps) to 3.57%.

As earnings season picked up pace this week, markets were closely attuned to the first quarter performance of U.S. companies in financial news. However, the net result on equity markets was muted, as results that were on aggregate moderately positive were partially overshadowed by the downbeat outlook for demand amid the expected economic slowdown later this year. As of the time of writing, the S&P 500 is down 0.5% on the week while the ten-year Treasury yield is up 5 basis-points (bps) to 3.57%.

On the global economic data front, we kicked off the week with first quarter Chinese GDP data, which grew by 4.5% from its year-ago level. The print was better than expected, as pent-up demand from consumers powered growth. China’s economic rebound is expected to be short-lived as consumer exuberance fades and structural headwinds continue to weigh on the economy in the back half of the year.

In the U.S. we had a housing-centric week for economic data, with updates on both existing home sales and residential construction. Data released on Thursday showed that existing home sales fell by 2.4% month-on-month (m/m) in March, pulling back from February’s revised 13.8% m/m increase. Month-to-month changes have been mirroring the volatility seen in mortgage rates (with a lag) as elevated prices have increased the reliance of buyers on financing conditions. While median home prices declined for a second consecutive month relative to year-ago levels (Chart 1), the seasonally adjusted change between February and March was slightly positive. Prices have been held up in part due to low inventory levels. However, new home construction is picking up, with single-family housing starts recovering for a second consecutive month in March, after eleven straight months of declines.

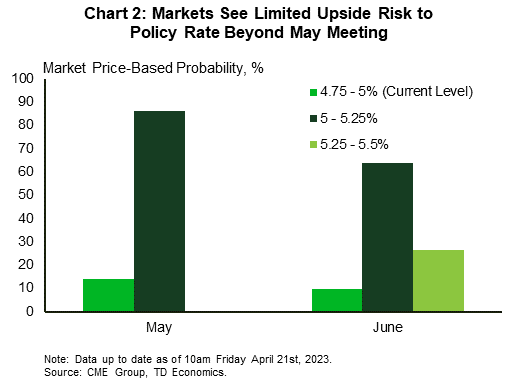

With the Federal Reserve’s pre-meeting blackout period starting on Saturday, we won’t hear from any FOMC members again until Chair Powell’s press conference on May 3rd. Luckily, we heard from ten Fed officials this week, six of whom are voting members. Most of the speakers noted that they were continuing to monitor credit conditions for signs of further stress. The Fed’s regional monitoring in April’s Beige Book stating that “several Districts noted that banks tightened lending standards amid increased uncertainty and concerns about liquidity” in financial news. Although this may aid the Fed in tightening credit conditions, as noted by Chicago Fed President Goolsbee this week, most members seemed to agree that further policy tightening would be required to sustainably return inflation to the Fed’s 2% target. As of the time of writing, markets are expecting the Fed to hike by 25bps in May, and then hold in June (Chart 2).

With the Federal Reserve’s pre-meeting blackout period starting on Saturday, we won’t hear from any FOMC members again until Chair Powell’s press conference on May 3rd. Luckily, we heard from ten Fed officials this week, six of whom are voting members. Most of the speakers noted that they were continuing to monitor credit conditions for signs of further stress. The Fed’s regional monitoring in April’s Beige Book stating that “several Districts noted that banks tightened lending standards amid increased uncertainty and concerns about liquidity” in financial news. Although this may aid the Fed in tightening credit conditions, as noted by Chicago Fed President Goolsbee this week, most members seemed to agree that further policy tightening would be required to sustainably return inflation to the Fed’s 2% target. As of the time of writing, markets are expecting the Fed to hike by 25bps in May, and then hold in June (Chart 2).

Next week we’ll get a first look at first quarter U.S. GDP and March PCE inflation, both of which are expected to show signs of cooling. Our forecast calls for activity to continue to slow through the remainder of 2023. This should help ease inflation pressures, enabling the Fed to keep the funds rate at 5.25% for the rest of the year.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of April 14th, 2023

Financial News Highlights

- Headline inflation rose 0.1% m/m in March, while core rose by a strong 0.4% m/m. The 12-month change on headline slipped to a near two-year low of 5%, while core ticked higher to a still uncomfortable 5.6%.

- Retail sales (-1.0% m/m) slipped again in March, falling for a second consecutive month after an unusually strong start to the year. Declines were seen across most categories, leaving a weak handoff heading into Q2.

- Though there are tentative signs the economy is cooling, the Federal Reserve likely has one more 25 basis-point rate hike to follow through on in May, before pausing to better assess the full impact of rate hikes.

Calm Prevails As Economy Shows Tentative Signs of Cooling

Rounding the corner into earnings season, a sense of calm seemed to descend across financial markets this week in financial news. But with earnings season not officially in full swing until Friday morning, investor focus fell squarely on the economic data. The two headliners this week were the March readings of CPI inflation and retail sales, though the release of the FOMC meeting minutes also garnered some attention.

Rounding the corner into earnings season, a sense of calm seemed to descend across financial markets this week in financial news. But with earnings season not officially in full swing until Friday morning, investor focus fell squarely on the economic data. The two headliners this week were the March readings of CPI inflation and retail sales, though the release of the FOMC meeting minutes also garnered some attention.

The latest move by the Federal Reserve occurred during the recent regional banking crisis, which ultimately forced the FOMC to rethink its trajectory for the federal funds rate. The uncertainty was on full display in the minutes, where several participants thought it was appropriate to hold the target range steady last month in light of recent events. This was an abrupt U-turn from what policymakers had communicated just a few weeks prior to the interest rate announcement, where the thought was rates needed to move both higher and faster relative to what had been assumed in the December’s Summary of Economic Projections. But perhaps the most noteworthy takeaway from the minutes was an explicit mention that considering the recent banking crisis “… the staff’s projection included a mild recession starting later this year, with a recovery over the subsequent two years”. Indeed, participants agreed that the actions taken by the Federal Reserve and other government agencies helped calm conditions in the banking sector but deemed that it was still too early to assess the confidence and magnitude of the effect of credit tightening on the real economy.

This morning’s retail sales gave a first glimpse into the impact that tighter credit conditions may already be having on households. Both nominal and real spending fell 1.0% m/m in March, marking the second consecutive month of declines. But even after accounting for the pullback, consumer spending is still tracking a robust 4.2% for Q1 in financial news. However, the weak handoff from March suggests last quarter may have been the “last hurrah” as the cumulative effect of higher interest rates alongside the recent tightening in lending standards appear to be bearing down on the consumer.

This morning’s retail sales gave a first glimpse into the impact that tighter credit conditions may already be having on households. Both nominal and real spending fell 1.0% m/m in March, marking the second consecutive month of declines. But even after accounting for the pullback, consumer spending is still tracking a robust 4.2% for Q1 in financial news. However, the weak handoff from March suggests last quarter may have been the “last hurrah” as the cumulative effect of higher interest rates alongside the recent tightening in lending standards appear to be bearing down on the consumer.

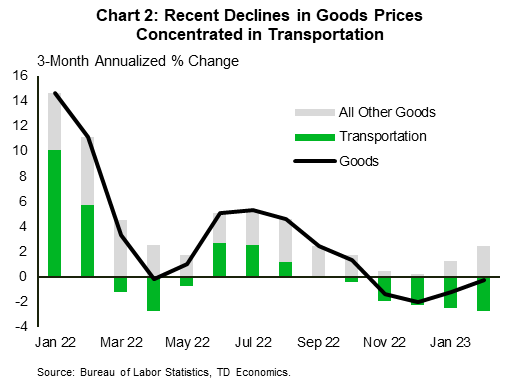

From an inflation standpoint, the softening in demand has yet to manifest in any significant easing in core consumer price pressures. Indeed, headline inflation slipped to 5% y/y – a near two-year low – thanks to lower food and energy prices (Chart 1). However, core CPI rose 0.4% m/m, leaving the 3-month (annualized) and 12-month rates of change at 5.1% and 5.6%, respectively. Underpinning the gains was an acceleration in goods prices alongside continued strength in shelter (0.6% m/m) and non-housing services (0.3% m/m).

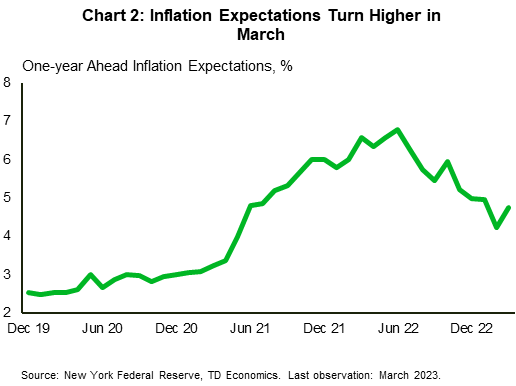

For a central bank who has become increasingly data dependent, the continued persistence in core inflation alongside the recent uptick in inflation expectations is unlikely to sit well (Chart 2). Provided there are no further flare-ups in financial markets, it is likely that the FOMC will need to raise the benchmark rate by another 25-bps in May, before pausing to better assess the full impact of the 500-bps of rate hikes.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Featured Article: 5 Best Places to Stay in U.S. National Parks

5 Best Places to Stay in U.S. National Parks

America’s national parks offer some of the best places to immerse yourself in nature, with stunning coastal and mountain landscapes that provide the ultimate spot for outdoor adventure. While most national parks offer campgrounds, a select few have hotels or lodges right within their boundaries. If roughing it isn’t something you relish, you’ll want to consider one of these properties, from the protected Alaska wilderness to the exotic shores of Hawaii.

Old Faithful Inn – Yellowstone National Park, Wyoming

A national historic landmark, the Old Faithful Inn opened in Yellowstone National Park in 1904, with the radiators and electricity fueled by a steam generator. It’s been the most popular place to stay in the park ever since, offering a warm, rustic feel, while still being spectacularly grand. The lobby is particularly impressive with its nearly 80-foot-high ceiling and huge stone fireplace. Rooms line the exterior of the seven-story log building, and each level has a balcony that overlooks the lobby. Some also boast breathtaking views of Old Faithful and the other geysers nearby. They don’t include TVs or Wi-Fi, so this is a perfect opportunity to forget about those electronic devices and just enjoy all that the inn and the park have to offer.

Open only from early May through early October, the inn is the most popular accommodation option in the park, so you’ll want to book your stay well in advance.

Glacier Bay Lodge – Glacier Bay National Park, Alaska

Glacier Bay Lodge is the only non-camping option for accommodation in Glacier Bay National Park. Open from around Memorial Day Weekend to Labor Day Weekend, it can only be reached by boat or plane. Most visitors take the 35-minute flight from Juneau followed by the lodge shuttle. The effort is worth the reward as you’ll be surrounded by snow-capped mountains, glistening turquoise water, and a wealth of wildlife. The highlight of a stay here is the catamaran tour operated by the lodge that will bring you to the park’s famous glaciers. Along the way, watch for the bald eagles and puffins that soar through the sky; mountain goats, coastal brown bears, and moose that roam the land; and sea lions, sea otters, porpoises, and whales that swim through the water.

The lodge guest rooms are tucked among the spruce trees at Bartlett Cove and include options for bay views. You won't have access to TVs or Wi-Fi in your room, but you can connect in the lobby, which features a stone fireplace, and a restaurant with floor-to-ceiling windows for dining or unwinding with a magnificent view of the bay.

Lake Quinault Lodge – Olympic National Park, Washington

Located at the edge of Lake Quinault in the western region of lush Olympic National Park, historic Lake Quinault Lodge provides the perfect base for exploring the rainforest and enjoying activities on the lake, with paddleboards, kayaks, and canoes available for rent. Plus, the coast is less than 30 miles away if you want to enjoy the park’s wild stretches of driftwood-strewn beach that’s thrashed by powerful waves. The lodge offers guided boat tours and tours through the rainforest where you’ll watch for black bears while learning about Quinault Indian Nation history.

A variety of lodge rooms are available year-round, including Fireplace Rooms with gas fireplaces and private lake and forest views. All come with TVs and Wi-Fi, while common amenities include an indoor pool, sauna, game rooms, and an outstanding restaurant.

The Ahwahnee – Yosemite National Park, California

Open every season, The Ahwahnee is an iconic property in one of the most breathtaking national parks in the country, Yosemite. Nestled among the park’s famous dramatic cliffs with sheer granite faces and enchanting waterfalls in Yosemite Valley, it’s hosted everyone from photographer Ansel Adams to Presidents Kennedy and Obama since opening its doors nearly a century ago. Guests are steps from scenic trails that lead to the park's famous peaks and cascades. Those who prefer to hang around the hotel will enjoy awe-inspiring views from the grounds and through the massive lodge windows of Yosemite Falls, Glacier Point, and Half Dome.

There are two dozen cottages and 97 rooms in the main lodge, ranging from standard to presidential, including the Mary Curry Tresidder Suite where Queen Elizabeth II once slept. While the interior elegantly blends Native American and art deco influences, you’ll have modern amenities, including a flat-screen TV and Wi-Fi.

Volcano House – Hawaii Volcanoes National Park, Hawaii

Those who are fascinated by volcanoes shouldn’t miss the opportunity to stay at Volcano House. Located inside Hawaii Volcanoes National Park, it offers one of the most stunning views you’ll find in any national park lodge. From the main floor, you’ll be able to watch the fiery glow through the massive windows. The park protects Kilauea volcano, one of the world’s most active, producing some 250,000 to 650,000 cubic yards of lava daily – that’s enough to resurface a two-lane, 20-mile stretch of roadway every day.

Guests who stay at Volcano House will be just a skip and a jump from hiking trails that wind around the edge of the caldera and there are daily guided walking tours available as well. Many of the guest rooms come with volcano views, some have lanais, and all come with Wi-Fi. Dining with a backdrop of the caldera and the crater can be enjoyed at The Rim at Volcano House, which offers an impressive menu of grass-fed beef and fresh-caught fish.

To see more fantastic articles like this one, please see here.

Financial News for the Week of March 31st, 2023

Financial News Highlights

- FOMC voting members noted the interest rate path will depend on incoming data and highlighted the uncertainty surrounding the effects of regional bank stress on credit availability.

- Inflation remained relatively elevated, despite moderating last month, as total and core PCE inflation both rose 0.3% month-on-month (m/m) in February.

- Pending home sales in February surpassed expectations by a notable margin as modest price declines and lower mortgage rates supported activity at the start of the year.

Quiet End to a Volatile Quarter

The last week of the first quarter was relatively quiet as markets continued to digest last week’s Federal Reserve decision and the potential implications of regional bank stress on credit conditions in financial news. In terms of economic data, we received updates on housing, consumption, and inflation. Equity markets drifted higher on the week, with the S&P 500 up 2.5%, while the 2-year Treasury yield rose by roughly 30 basis-points (bps) to sit at 4.1% as of the time of writing – still about 90bps below its cyclical peak of 5% at the start of the month.

The last week of the first quarter was relatively quiet as markets continued to digest last week’s Federal Reserve decision and the potential implications of regional bank stress on credit conditions in financial news. In terms of economic data, we received updates on housing, consumption, and inflation. Equity markets drifted higher on the week, with the S&P 500 up 2.5%, while the 2-year Treasury yield rose by roughly 30 basis-points (bps) to sit at 4.1% as of the time of writing – still about 90bps below its cyclical peak of 5% at the start of the month.

Starting off on Sunday, we heard from Minneapolis Fed President Neel Kashkari. Reiterating Chair Powell’s statements from last week, Kashkari noted that the banking system is resilient, but that uncertainty remained regarding the extent to which stress in the banking sector may lead to a credit crunch in financial news. For this reason, Kashkari assessed that “it’s too soon to make any forecasts about the next interest rate meeting [in May]”. This marks a notable deviation from his comments on March 1st that he was open to a 50bps hike in March. The uncertainty is also reflected in the market’s sentiment about the Fed’s May decision – now pricing the odds of a hike at basically a coin toss.

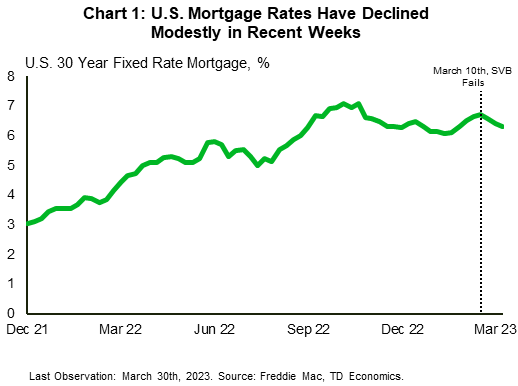

Housing data surprised to the upside this week, with pending home sales rising by 0.8% month-on-month (m/m) in February, down from the 1.8% rise seen in January, but well above the consensus expectation of a 3% m/m decline. This relative strength was likely front-loaded in the month, as mortgage rates rose by roughly 50bps in February. Pending home sales tend to lead final sales by 1-2 months, so this could be an indicator that the spring housing market may begin with some strength, particularly considering that mortgage rates have fallen by roughly 30bps since March 10th (Chart 1). However, stretched affordability and still relatively high financing costs are expected to remain notable headwinds moving forward.

The pulse check on the American consumer this week showed that personal income grew by 0.3% m/m in February, decelerating from January’s gain of 0.6%. This helped to push personal spending up by 0.2% m/m, with housing and health care services seeing the largest increases. Total and core PCE inflation both rose by 0.3% m/m, decelerating relative to January but remaining elevated (Chart 2). More recent data showed that consumer confidence rose in March on a modestly improved outlook for six months ahead, whereas the consumer assessment of the current economic situation deteriorated. The survey cut-off was 10 days after SVB failed, so it is likely that this reading only partially captures the consumer response to recent banking sector stress.

The pulse check on the American consumer this week showed that personal income grew by 0.3% m/m in February, decelerating from January’s gain of 0.6%. This helped to push personal spending up by 0.2% m/m, with housing and health care services seeing the largest increases. Total and core PCE inflation both rose by 0.3% m/m, decelerating relative to January but remaining elevated (Chart 2). More recent data showed that consumer confidence rose in March on a modestly improved outlook for six months ahead, whereas the consumer assessment of the current economic situation deteriorated. The survey cut-off was 10 days after SVB failed, so it is likely that this reading only partially captures the consumer response to recent banking sector stress.

Looking ahead to next week, markets will be closely watching the March employment data release on Friday, with consensus expectations for job growth to cool and the unemployment rate to remain unchanged. This will be one of the more important updates between now and the May Fed meeting, as policymakers continue to look for signs of labor market cooling and its subsequent easing effect on price growth.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of March 24th, 2023

Financial News Highlights

- The Federal Reserve delivered a modest 25-basis point hike this week amid banking stress, lifting the policy rate to a range of 4.75-5.00% – a level that’s just a hair below its previous peak back in 2007.

- Fed projections show the policy rate peaking at 5.1% in 2023, implying one more hike for the year, while next year a series of cuts are forecast to bring the rate down to 4.3%. Market expectations, however, are titled toward a lower rate environment in both years.

- Existing home sales rose 14.5% in February, recording the first increase after twelve consecutive months of declines.

Fed Delivers Small Hike Amid Banking Stress

Stuck between a rock and a hard place, the Fed appears to have taken a middle-of-the-road approach in setting monetary policy this week in financial news. Inflation, which remains well above target and has shown moderate signs of acceleration recently coupled with strong job growth, meant that the Fed could have opted for a more hawkish stance at Wednesday’s FOMC meeting. Fed Chair Powell nodded to this possibility in his testimony to Congress two weeks ago. However, the ongoing banking turmoil has upended this narrative. Instead of leaving the rate unchanged, – an option that was closely considered – Fed officials ultimately went with a 25-basis point hike, lifting the policy rate to 4.75-to-5.00%.

Stuck between a rock and a hard place, the Fed appears to have taken a middle-of-the-road approach in setting monetary policy this week in financial news. Inflation, which remains well above target and has shown moderate signs of acceleration recently coupled with strong job growth, meant that the Fed could have opted for a more hawkish stance at Wednesday’s FOMC meeting. Fed Chair Powell nodded to this possibility in his testimony to Congress two weeks ago. However, the ongoing banking turmoil has upended this narrative. Instead of leaving the rate unchanged, – an option that was closely considered – Fed officials ultimately went with a 25-basis point hike, lifting the policy rate to 4.75-to-5.00%.

In taking this decision, the Fed acknowledged the risks from the banking turmoil, including the potential negative impact on the real economy from tighter credit conditions for households and businesses in financial news. Tighter credit conditions could do some of the Fed’s work for it in reducing inflationary pressures, substituting for further hikes. However, as Chair Powell noted in the press conference, it’s not clear how significant and how sustained the credit tightening will be. The Fed is keeping the door open to some further monetary tightening for now, but changes in the language of the FOMC statement suggest that it is very close to wrapping up its hiking cycle.

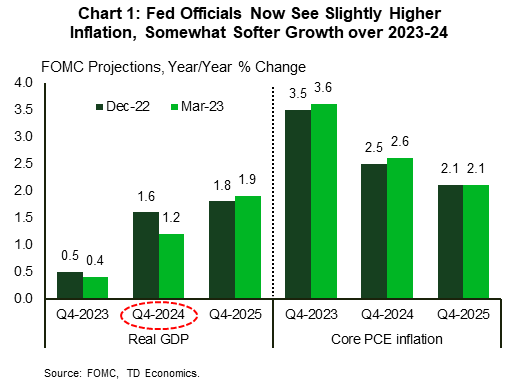

Along with the policy decision, the Fed also issued an update to its quarterly economic projections. Fed officials now expect inflation to remain slightly higher by the end of 2023 and 2024 compared to their view in December. Meanwhile, economic growth is expected to come in a bit softer over this same period, with a downgrade to the 2024 growth profile the most noticeable difference (Chart 1).

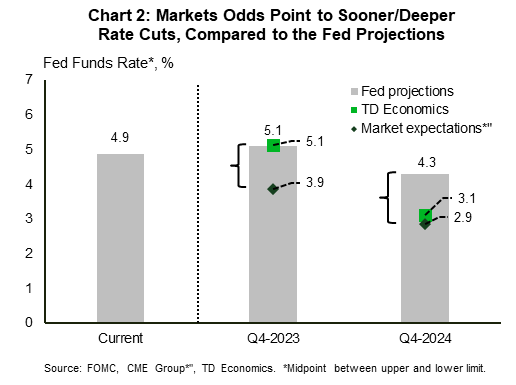

Policy rate expectations remained unchanged for 2023, with most Fed officials expecting the rate to peak to 5.1%, which implies one more hike this year. Market expectations, however, are not in tune with this view. The current pricing suggests that the Fed is done hiking rates, and that rate “cuts” will follow suit shortly this summer. Moving on to next year, while Fed officials have penciled in a series of rates cuts that will bring the policy rate down to 4.3%, market expectations remain more dovish, with the gap between the two forecasts widening (Chart 2). Our projection is aligned more closely with the Fed this year, but as growth slows into next year, we anticipate that in 2024 the Fed will loosen monetary policy more than it projects to steady the economic ship.

Policy rate expectations remained unchanged for 2023, with most Fed officials expecting the rate to peak to 5.1%, which implies one more hike this year. Market expectations, however, are not in tune with this view. The current pricing suggests that the Fed is done hiking rates, and that rate “cuts” will follow suit shortly this summer. Moving on to next year, while Fed officials have penciled in a series of rates cuts that will bring the policy rate down to 4.3%, market expectations remain more dovish, with the gap between the two forecasts widening (Chart 2). Our projection is aligned more closely with the Fed this year, but as growth slows into next year, we anticipate that in 2024 the Fed will loosen monetary policy more than it projects to steady the economic ship.

Reiterating Chair Powell’s view, the degree of credit tightening from the recent banking turmoil remains a major source of uncertainty for the outlook. On this front, it appears that authorities will need to stay alert in putting out more fires. Across the Atlantic, after finding a solution to the Credit Suisse troubles, the attention has now turned to another Global Systemically Important Bank (G-SIB), Deutsche Bank, after a surge this week in the cost of insuring the lender’s debt against default. With banking developments front and center, economic data played second fiddle, but a strong housing report (see here) did bring some cheer.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of March 17th, 2023

Financial News Highlights

- Following the collapse of SVB and Signature Bank, policymakers were quick to put together a rescue package over the weekend to allay depositor fears and reassure financial markets.

- Despite recent market jitters, economic data out this week including CPI, retail sales, and housing starts all suggest more tightening is still required to cool demand and return price stability.

- A classic run on banks rippled through the financial system, but the regional banks’ equity underperformance reflects the idiosyncratic nature of this episode.

- Risk sentiment tightens financial conditions and feeds through to the real economy if it remains unresolved for a period of time. At this early juncture, it may not deter the Fed from raising interest rates on March 22nd, but can certainly put the May meeting on ice if pressures persist.

Lifelines Extended, But Uncertainty Remains

In financial news, can policymaker’s walk while chewing gum? We’ll soon find out. The Federal Reserve’s attempt at reining in multidecade inflation without causing a recession was always thought to be a lofty goal. However, last week’s failure of both SVB and Signature Bank followed by the subsequent deposit run at First Republic has added a new layer of complexity.

In financial news, can policymaker’s walk while chewing gum? We’ll soon find out. The Federal Reserve’s attempt at reining in multidecade inflation without causing a recession was always thought to be a lofty goal. However, last week’s failure of both SVB and Signature Bank followed by the subsequent deposit run at First Republic has added a new layer of complexity.

In an effort to allay depositor fears and reassure financial markets, the FDIC, Federal Reserve, and U.S. Treasury implemented a rescue plan over the weekend. Deposit insurance for all deposits over $250k was extended, while a Bank Term Funding Program was also established, allowing all depository institutions to borrow at the Fed at a low rate using standard collateral. Moreover, the collateral could be valued at par rather than “marked to market” as is the case with other Fed liquidity facilities. Not only will this increase the amount of capital that troubled banks can access, but it will also prevent institutions from having to sell assets at significant losses, which should help to shore up confidence and stem the tide on further deposit outflows in financial news.

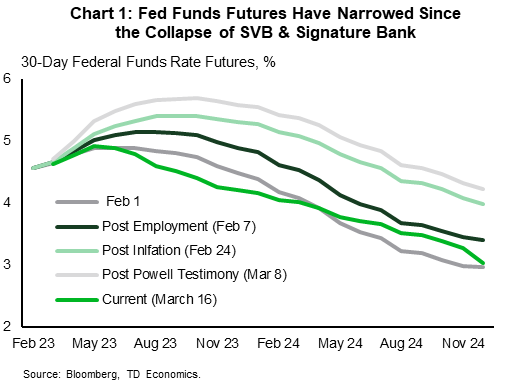

While sound in theory, investors remained skeptical that the risk remained contained to just a handful of regional banks. And this skepticism was only reinforced when news came that Credit Suisse may also be experiencing similar liquidity issues. Market sentiment soured mid-week but was quick to recover following news that First Republic had secured a rescue package and that the Swiss Central Bank would provide a liquidity backstop for Credit Suisse. After a volatile week, the S&P 500 finished 2% higher, while the 10-year yield fell 25bps landing at 3.45%. Investors also significantly recalibrated expectations on the future path of the fed funds rate, with a 25bps hike at next week’s announcement only 75% priced and rate cuts again priced for later this year (Chart 1).

Only time will tell if this sharp repricing is overdone, but at the moment, the Fed appears stuck between a rock and a hard place. It is clear that the rapid adjustment in interest rates over the past year has pinched a nerve within a sub-segment of the banking sector. But on the other hand, the recent flow of economic data suggests more tightening is still required to cool the economy and return price stability. This was evident in February’s reading of CPI, where core inflation accelerated on the month – rising by 0.5% m/m – pushing the 3-month annualized change to a four-month high of 5.2%. Considerable breadth was seen across the cyclical component of services, which is closely tied to discretionary spending. And while goods prices were flat on the month, that was largely due to another sizeable decline in used vehicle prices, offsetting an acceleration across most other goods categories (Chart 2). Outside of inflation, retail sales (-0.4% m/m) softened in February but that was only after an outsized gain in January, while housing starts ended a 5-month slide and surged 10% m/m to 1.45M. The data is definitely telling the FOMC to hike, but the financial stability concerns also cannot be ignored. Provided risks remain contained, we expect the Fed to push ahead with another 25bps hike next week.

Only time will tell if this sharp repricing is overdone, but at the moment, the Fed appears stuck between a rock and a hard place. It is clear that the rapid adjustment in interest rates over the past year has pinched a nerve within a sub-segment of the banking sector. But on the other hand, the recent flow of economic data suggests more tightening is still required to cool the economy and return price stability. This was evident in February’s reading of CPI, where core inflation accelerated on the month – rising by 0.5% m/m – pushing the 3-month annualized change to a four-month high of 5.2%. Considerable breadth was seen across the cyclical component of services, which is closely tied to discretionary spending. And while goods prices were flat on the month, that was largely due to another sizeable decline in used vehicle prices, offsetting an acceleration across most other goods categories (Chart 2). Outside of inflation, retail sales (-0.4% m/m) softened in February but that was only after an outsized gain in January, while housing starts ended a 5-month slide and surged 10% m/m to 1.45M. The data is definitely telling the FOMC to hike, but the financial stability concerns also cannot be ignored. Provided risks remain contained, we expect the Fed to push ahead with another 25bps hike next week.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

Financial – Some Banks Fail, but It's Not a Free Fall

The Federal Reserve was blind sighted by an evolving risk that was right under its nose. While it tightened monetary policy at an unprecedented pace, deposit growth within commercial banks plummeted at an historic pace (Chart 1) in further financial news. Some of this movement reflected the outcome of quantitative tightening and some reflected a shift in depositor preferences into higher yielding products. Predicting this shift was actually well within forecast models, offering little element of surprise. Predicting individual behaviors and market confidence, however, is another story.

The Federal Reserve was blind sighted by an evolving risk that was right under its nose. While it tightened monetary policy at an unprecedented pace, deposit growth within commercial banks plummeted at an historic pace (Chart 1) in further financial news. Some of this movement reflected the outcome of quantitative tightening and some reflected a shift in depositor preferences into higher yielding products. Predicting this shift was actually well within forecast models, offering little element of surprise. Predicting individual behaviors and market confidence, however, is another story.

Unless you've been completely cut off from every form of communication, by now it's well known that the sudden failure of Silicon Valley Bank was more than a classic "run on a bank". The aggressive rate hike cycle pressured the market value of the bank's financial assets, even though these were deemed high quality and liquid. Meanwhile, a concentration of a large amount of uninsured deposits from start-ups and cryptocurrency companies left the bank exposed to a sudden shift in confidence. Once the financial market participants witnessed a mass deposit exit and a swift bank failure, it opened the door to lurking risks within other institutions. The fear of the known unknown kicked in.

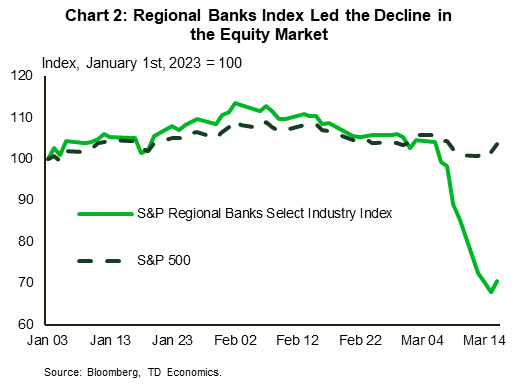

However, that fear has largely been contained, at least at this juncture. The pressure on equity markets was not economy wide. A concentration within the banking sector was further narrowed to the regional banks' sub-sector. In the period between March 8th and March 15th, the S&P's Regional Banks Sub-Industry Index lost more than 30% of its value while the S&P 500 index declined by 2.5%, half of which was due to the pressure on the banking sector (Chart 2). While large, the magnitude of change is not unprecedented. During the Global Financial Crisis – the poster child of the banking sector crisis – the index lost almost 80% of its value (albeit, in a period of six months), while its maximum daily loss was 1.5 times greater than the current episode.

However, that fear has largely been contained, at least at this juncture. The pressure on equity markets was not economy wide. A concentration within the banking sector was further narrowed to the regional banks' sub-sector. In the period between March 8th and March 15th, the S&P's Regional Banks Sub-Industry Index lost more than 30% of its value while the S&P 500 index declined by 2.5%, half of which was due to the pressure on the banking sector (Chart 2). While large, the magnitude of change is not unprecedented. During the Global Financial Crisis – the poster child of the banking sector crisis – the index lost almost 80% of its value (albeit, in a period of six months), while its maximum daily loss was 1.5 times greater than the current episode.

The relative containment of the crisis doesn’t negate the seriousness of the situation. Look no further than within expectations for the fed funds rate. In a matter of ten days, the futures market turned upside down, shifting its pricing from a 50-basis point hike in March and a 5.75% terminal rate, to 25-basis point hike and a terminal rate 85 basis points lower. On March 13th, the two-year yield collapsed by 57 basis points to 4.03% – the largest decline since the Black Monday market crash of 1987. This initially pushed the U.S. dollar down 2% relative to other currencies. But, the greenback reclaimed its strength as a safe-haven currency as soon as the confidence shock drifted over the Atlantic. As the biggest shareholder of Credit Suisse declared no interest in upping its funding commitment to the already-beleaguered institution, the greenback finished 1.5% below March 8th level.

In both cases, the respective regulators and the central bank stepped in to provide a liquidity backstop, having learned from the past that the first order of business is to stabilize financial market shocks that have the potential to seize up the system if left unchecked in financial news. The second order of business will be to ensure guard rails are in place to limit a future episode. This usually comes in the form of more oversight. Market chatter has already settled on one possible change for U.S. mid-and-small sized banks to lower the banks' asset threshold at which stricter capital and liquidity rules start to apply from $250 to $100 billion. Another proposal being bantered about is to put more rigor into the stress test that assesses valuation of banks capital during a hypothetical macroeconomic recession scenario.

From an economic perspective, any permanency in tighter financial conditions among mid- and smaller-sized banks that flows through to tighter credit standards will impact loan demand and the real economy. The irony is that this feedback loop might help the Fed tap down domestic demand and contain inflationary pressures, as long as pressure on financial conditions remain 'controlled'. Up until now, the U.S. economy was described as stronger-for-longer, with consumers and job demand completely defying the odds. Time will tell.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of March 10th, 2023

Financial News Highlights

- Chair Powell’s testimony threw the market in to risk-off mode with both the Treasury and equity market falling on the week.

- The economy added 311k jobs in February, well ahead of the consensus forecast of 225k, reinforcing the resilience of the job market.

- There’s still plenty of data to come in before the Fed’s rate decision, with next week’s inflation report the most important.

Jobs Market Stays Strong

Chair Powell’s bi-annual testimony to Congress pushed the market into risk-off mode as his explicit remarks put the half-point rate hike back on the table in major financial news. In his statement, Powell highlighted the strength of the latest economic data, “which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated”.

Chair Powell’s bi-annual testimony to Congress pushed the market into risk-off mode as his explicit remarks put the half-point rate hike back on the table in major financial news. In his statement, Powell highlighted the strength of the latest economic data, “which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated”.

Treasuries plunged to fresh lows, with the two-year yield moving briefly above 5% for the first time since July 2007, while keeping the ten-year yield hovering just below 4%. As a result, the spread between the two (one of the strongest market-based recession indicators) widened to the 100-basis point mark before narrowing back to 90 bps by the end of the week (Chart 1) in financial news. This is the deepest inversion since 1981. The equity market was as volatile, with the trouble at SVB Financial Group adding to shock. The S&P 500 Index moved below the 4,000-level finishing the week with a 3.4% loss (at the time of writing).

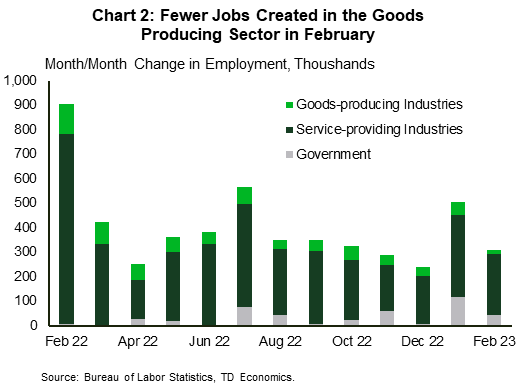

Today’s payrolls report didn’t help settle the markets. The employment number came in stronger than anticipated (at 311k v. 225k expected), suggesting that there is considerable strength in the jobs market. The unemployment rate returned to 3.6% as the labor force expanded, lifting the participation rate to 62.5%. Notably, the monthly increase in the goods producing sector was the smallest since May 2021, with job gains tilted towards the services sector (Chart 2). The trend pace of average hourly earnings growth over the past three months slipped to the slowest pace of growth in nearly two-years. However, hourly earnings don’t adjust for compositional effects across sectors, and have been running well below other metrics in recent months. February’s softness is likely in part due to job gains concentrated in lower-wage sectors and jobs losses in some higher-wage ones.

The tight labor market was also evidenced in January’s Job Openings and Labor Turnover Survey (JOLTS). While job vacancies declined to 10.8 from an upwardly revised 11.2 million in December, they remain high, suggesting that demand for workers exceeds supply – a condition that will continue to support wage growth.

The tight labor market was also evidenced in January’s Job Openings and Labor Turnover Survey (JOLTS). While job vacancies declined to 10.8 from an upwardly revised 11.2 million in December, they remain high, suggesting that demand for workers exceeds supply – a condition that will continue to support wage growth.

There’s still plenty of data to come before the Fed’s March 21-22 meeting, when the Fed decides on the rate hike and releases updated economic projections. Next week, we’ll have more details on CPI and retail sales for February. The former has more bearing on the rate decision, as it makes up the second half of the Fed’s dual mandate (besides maximum employment), while the latter may contribute to the Fed’s understanding of consumer spending momentum. To convince FOMC members to keep the same pace of rate hikes as in December, price changes would need to provide evidence of a decelerating trend. Today, the probability of a 50-basis points hike settled around 40% - higher than 28% last week but lower than more than 70% earlier this week.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.