Financial News for the Week of December 16th, 2022

Financial News Highlights

- The FOMC downshifted its tightening race in December, raising the policy rate by 50-bps, bringing the operating band to 4.25%-4.5%.

- The FOMC’s Summary of Economic Projections showed a less optimistic economic outlook, accompanied by higher inflation. The median consensus on the Fed Funds rate was lifted by 50-bps for 2023, implying a terminal rate of 5.25%.

- November inflation data showed a further softening in price pressures, with core CPI rising 0.2% m/m and the 12-month change falling to 6% y/y. Retail sales for November were weaker than expected (-0.6% m/m), recording its largest monthly decline in 11 months.

Slowing, But Not Stopping

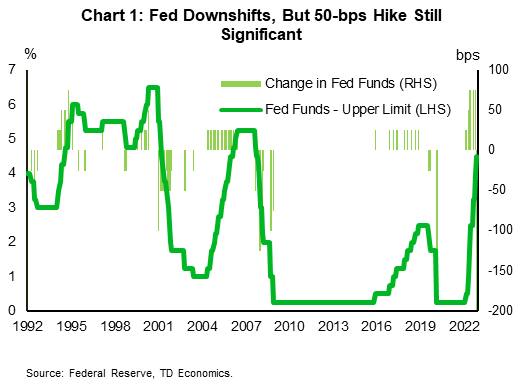

Phew, whatta week for financial news! The headlines included further evidence of softening inflation, wanning consumer momentum and the much-anticipated December FOMC interest rate announcement. The Fed met market expectations, increasing the policy rate by “only” 50 basis-points (bps), bringing the upper-bound to 4.5%. That marked a slowdown from the 75-bps pace undertaken at the four prior meetings, but still stands as a historically fast pace of policy adjustment (Chart 1).

Phew, whatta week for financial news! The headlines included further evidence of softening inflation, wanning consumer momentum and the much-anticipated December FOMC interest rate announcement. The Fed met market expectations, increasing the policy rate by “only” 50 basis-points (bps), bringing the upper-bound to 4.5%. That marked a slowdown from the 75-bps pace undertaken at the four prior meetings, but still stands as a historically fast pace of policy adjustment (Chart 1).

Beyond the interest rate announcement, the FOMC also released updated economic projections. Relative to the September assessment, Committee participants now expect growth to be considerably weaker in 2023 (0.5% vs 1.2%) and the unemployment rate slightly higher (4.6% vs. 4.4%). Despite the more downbeat outlook, policymakers view price pressures as having become more entrenched, and upgraded the inflation outlook through 2024. As a result, the FOMC signaled rates are likely to move at least 50-bps higher than previously expected next year – implying a terminal rate of 5.25% – with cuts not beginning until 2024.

In the press conference, Chair Powell struck a somewhat hawkish tone. When asked about the recent easing in financial market conditions, Powell stated that the Committee looks through near-term swings, but emphasized the importance of market conditions aligning to the Fed’s intentions. Moreover, Powell was quick to direct focus to the upward revision to the “dots”, reiterating that the Committee’s view on inflation remains skewed to the upside and thus future projections could still show an even higher terminal rate. Despite this deliberate signaling, market participants still believe that the Fed will begin cutting rates late next year.

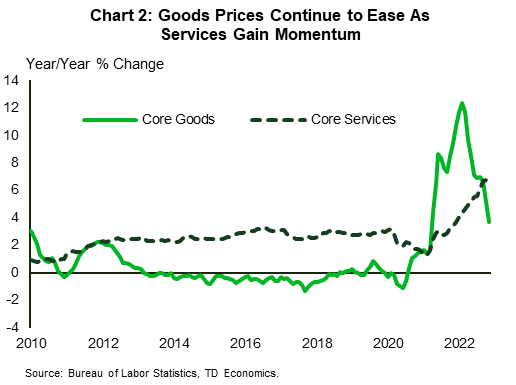

Investors current assessment might be somewhat biased by November’s CPI data, which showed a further cooling in inflationary pressures. Core inflation rose by 0.2% m/m – a tick below market expectations – bringing the 12-month change to 6.0%. Core goods prices declined for a second consecutive month, while price growth across services continued to be led by outsized gains in shelter. That said, even after removing its effects, most other service categories continue to show strength. This cuts to the heart of the issue. With goods prices appearing to have rolled over and the shelter component expected to slow in H2’2023, the move down towards 3% inflation by the end of next year is feasible. However, until we see a more meaningful slowdown in hiring activity, leading to a cooling in wage pressures, many labor-intensive service sectors will continue to run hot – preventing inflation from moving back to 2%.

Investors current assessment might be somewhat biased by November’s CPI data, which showed a further cooling in inflationary pressures. Core inflation rose by 0.2% m/m – a tick below market expectations – bringing the 12-month change to 6.0%. Core goods prices declined for a second consecutive month, while price growth across services continued to be led by outsized gains in shelter. That said, even after removing its effects, most other service categories continue to show strength. This cuts to the heart of the issue. With goods prices appearing to have rolled over and the shelter component expected to slow in H2’2023, the move down towards 3% inflation by the end of next year is feasible. However, until we see a more meaningful slowdown in hiring activity, leading to a cooling in wage pressures, many labor-intensive service sectors will continue to run hot – preventing inflation from moving back to 2%.

Though the cumulative impact from higher rates hasn’t yet hit hiring intentions, November retail sales showed consumer momentum may be wanning. Sales fell 0.6% m/m – its biggest monthly drop in nearly a year – with notable declines in holiday categories including, electronics, clothing, and sporting goods. As we noted in our Quarterly Economic Forecast, it was unrealistic to assume the recent strength in spending would continue indefinitely. A broader demand adjustment needs to occur over the coming quarters in order to restore price stability. It would appear we are nearing the precipice of that adjustment.

Thomas Feltmate, Director | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Featured Article: The 5 Best Places to See an Untouched Winter Wonderland

The 5 Best Places to See an Untouched Winter Wonderland

There’s something undeniably magical about a pristine, snowy winter landscape. Smoke rising from chimneys, the Northern Lights dancing above you, hot cocoa warming your hands while snowflakes fall outside your window. From soaking in hot springs to ice skating under mesmerizing mountain peaks, we’ve gathered up the best places to see an untouched winter wonderland around the world. Bundle up, grab a warm beverage and come with us to these snowy destinations.

Lapland, Finland

The far northern reaches of Finland, known collectively as Lapland, are a remote winter landscape utterly untouched. The scattered residents who call this region home carve out snowmobile trails as the polar night engulfs them for two solid months of darkness.

This might be one of the best places in the world to cross the northern lights off your bucket list. Polar nights allow a longer window of time to witness them while crisp winter air makes for perfect viewing conditions. As an added bonus, you can pay Santa Claus himself a visit in the village of Rovaniemi, and pet some of his reindeers.

When the cold starts to seep into your bones, hole up in a traditional Finnish sauna. The tradition of hitting fellow sauna goers with Birch branches is said to increase circulation, helping you thaw from the extreme cold that can reach -40 degrees.

Yellowstone National Park, Wyoming, USA

Winter is an ideal time for visiting Yellowstone National Park as crowds thin, geysers soar, and wildlife spotting becomes more likely. The contrast of bubbling hot springs and volcanic activity juxtaposed with the icy landscape creates an otherworldly effect that has to be seen to be believed.

There is no shortage of winter activities in America’s first national park including snowmobiling, snowshoeing, and cross-country skiing. If you’re feeling up for a splurge, organize a snowcoach for a frozen safari through the desolate landscape. These methods of transportation are some of your only options after the first week of November. Roads don’t open again until the end of April so be sure to plan around travel restrictions. At the end of your trip, head to Mammoth Hot Springs at the northern edge of Yellowstone to thaw out from your icy adventures.

Banff, Canada

Maybe one of the most picturesque places on our list, Banff is a stunning winter destination located in the heart of the Canadian Rockies. Visitors can enjoy ice skating with beautiful views of Lake Louise or a ride in the Banff gondola for sweeping panoramas of the wintery scenes below. If you’re lucky, Banff is another destination on this list where it’s possible to see the northern lights dance across the mountains. When conditions are right the best place to view them is at Lake Minnewanka, located about 10 minutes outside the city, with open sky views.

Chamonix, France

In the shadow of Mont Blanc, Chamonix is one of the premier destinations in Europe for winter sports. From extreme alpine skiing to dog sledding, there’s something for everyone in this frozen mecca.

If you’re feeling adventurous, take the Aiguille du Midi, to see the top of Mont Blanc. Here you can “Step Into the Void” by literally stepping out over a 1,000 foot drop covered by a glass atrium. Chamonix is also home to the largest glacier in France, Mer de Glace. The most scenic way to get there is aboard the Train du Montenvers with sweeping views of the Alps. After you’ve arrived, step inside the glacier itself in the Ice Cave or learn about global warming’s effect on the ice at the Glacorium. Afterwards Indulge in the local alpine cuisine raclette, melted cheese traditionally scraped over vegetables and meat, after a long day on the slopes.

Shirakawago, Japan

Japan is home to several cities with the highest snowfall records in the world. The island country’s unique geography causes ocean air to become trapped against the Japanese Alps resulting in huge snowfalls. Shirakawago sees 33 feet of snowfall on average in the winter months from December to March, making it one of Japan’s must-see winter wonderlands.

Shirakawago’s combination of extreme snowfall and unique cultural attributes caught the attention of UNESCO who designated it a World Heritage site. The idyllic Gassho-style houses that are nestled in the village of Ogimachi are built to withstand the extreme snowfall, giving them their unique look and architecture that allows snow to slide off the roof. Every year for six consecutive Sundays in January and February the village does an illumination ceremony, lighting up the iconic homes.

To see more fantastic articles like this one, please see here.

Financial News for the Week of December 9th, 2022

Highlights

- Somewhat unexpectedly, the ISM services index accelerated in November, with the business activity sub-index expanding to a level last seen in 2021.

- The services sector continues to struggle with elevated inflation as the prices paid component of the ISM services index and the services side of the producer price index showed no signs of price relief.

- Despite higher rates, consumers continued to borrow to support their spending. This underscores the degree of resilience of the U.S. consumer but increases prospects for a weaker economy next year as the Fed will have to move into more restrictive territory.

Waiting for the Fed

A slow week on the economic data front gave markets time to reflect and prepare for the FOMC meeting next week, which will include an update to the Fed’s economic projections in financial news. The consensus has solidified for a 50-basis points (bps) hike, but the Wall Street jury is out on how far the Fed will have to raise policy rates this cycle. Price volatility this week underscores increasing concerns that higher policy rates could tip the U.S. economy into recession.

A slow week on the economic data front gave markets time to reflect and prepare for the FOMC meeting next week, which will include an update to the Fed’s economic projections in financial news. The consensus has solidified for a 50-basis points (bps) hike, but the Wall Street jury is out on how far the Fed will have to raise policy rates this cycle. Price volatility this week underscores increasing concerns that higher policy rates could tip the U.S. economy into recession.

On Monday, the ISM Services index reported an acceleration in the services sector. Somewhat unexpectedly, the business activity sub-index expanded by whooping nine percentage points lifting it to a level last seen in 2021. This is in stark contrast with the manufacturing sector’s production index, which moved into contractionary territory. The pick-up in services activity was backed by remaining pent up demand, further boosted by the start to the holiday season as industries like Accommodation & Food Services and Retail Trade entered their busiest month of the year.

The prices sub-indexes reinforce the contrast between the two sectors. While the manufacturing sector has seen a significant deterioration in the prices paid component, which contracted in November with a reading of 43, it’s taking much longer for the services sector to see signs of price relief, with the sub-index remaining mired around 70 (Chart 1). Higher prices also appear to be broad-based with 16 out of 18 industries reporting higher prices. The Producer Price Index (PPI) for November provided another example of the sectoral divergence in price pressures. The PPI advanced by 0.3% month-on-month in November, driven by a 0.4% increase rise in services prices.

Tuesday’s trade data showed that goods exports declined in October, with a notable weakness in industrial supplies and materials (includes petroleum products), providing more evidence of dwindling demand from overseas. This contributed to a widening in the trade deficit to $78.2 billion in financial news. Imports also improved marginally supported by an increase in domestic demand for foreign goods, partially offset by weaker services imports from abroad.

Tuesday’s trade data showed that goods exports declined in October, with a notable weakness in industrial supplies and materials (includes petroleum products), providing more evidence of dwindling demand from overseas. This contributed to a widening in the trade deficit to $78.2 billion in financial news. Imports also improved marginally supported by an increase in domestic demand for foreign goods, partially offset by weaker services imports from abroad.

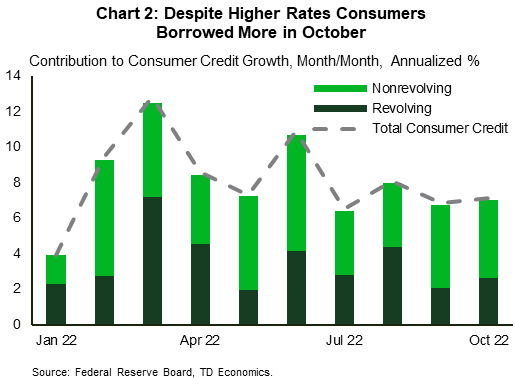

Consumer demand has proven a bit more resilient recently, and it looks to have been supported by consumer credit, which continued to expand in October despite higher interest rates. Consumer credit outstanding increased by $27.0 billion on the month (7.1% annualized), driven by nonrevolving credit, which gained $17.0 billion (Chart 2). Revolving credit added $10.1 billion, reflecting consumers stronger reliance on credit card debt as pandemic savings continue to dwindle. We think that consumers will add more leverage to support real spending growth of roughly 1.5% in 2023 – a step down from 2.8% expected in 2022.

That forecast underscores the degree of resilience coming from the U.S. consumer, but the cumulative effect of higher interest rates may create stronger headwinds than currently anticipated. Stronger domestic demand and higher inflation increases prospects that the Fed will have to move rates into more restrictive territory. Wednesday’s FOMC decision will feature the dot plot, so we won’t have to wait much longer to see the Fed’s latest thinking.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of December 2nd, 2022

Financial News Highlights

- Employment rose by 0.2% month-on-month (m/m) for the fourth consecutive month in November, surpassing expectations for a moderate slowdown in job growth.

- Core PCE inflation for October eased slightly to 5% year-on-year (y/y), but was supported by strong spending growth and a drop in the consumer savings rate to a 17-year low.

- FOMC Chair Powell noted in his speech on Wednesday that rate hikes may slow as early as December but reiterated that the Fed has a long way to go in restoring price stability.

U.S. - The Job Market Marches On

Markets had to hit the ground running after the Thanksgiving holiday, with a full slate of economic data and financial news. The November jobs report, personal income and spending data for October, and FOMC Chair Powell’s speech on Wednesday were just the headliners. Markets rallied to start the week, but gains were pared back after the release of the November jobs report on Friday. At the time of writing, the S&P 500 is up 0.3% on the week while the ten-year yield is down 10bps to 3.59%.

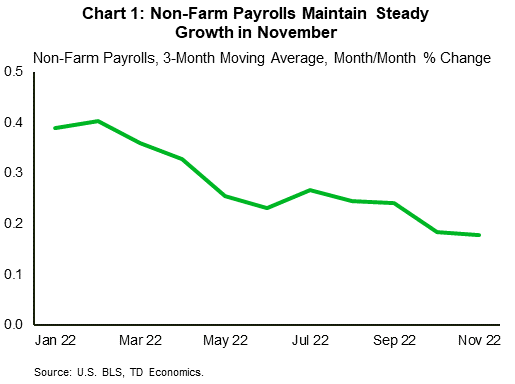

Markets had to hit the ground running after the Thanksgiving holiday, with a full slate of economic data and financial news. The November jobs report, personal income and spending data for October, and FOMC Chair Powell’s speech on Wednesday were just the headliners. Markets rallied to start the week, but gains were pared back after the release of the November jobs report on Friday. At the time of writing, the S&P 500 is up 0.3% on the week while the ten-year yield is down 10bps to 3.59%.In November, the seemingly indomitable U.S. labor market recorded another strong rise in employment. Non-farm payrolls rose by 263k jobs, rising at a pace of 0.2% month-on-month (m/m) for the fourth consecutive month (Chart 1). The unemployment rate remained unchanged at 3.7%, while the labor force declined slightly (-0.1% m/m). Average hourly earnings accelerated by 0.6% m/m, doubling market expectations.

Oil prices rose this week after Chinese officials eased up on their Zero-Covid messaging in the wake of wide-spread protests. With health protocols expected to be loosened heading into 2023, the prospect of renewed Chinese demand drove oil prices higher. Looking to next week, OPEC+ will have its bi-monthly meeting on Sunday after previously cutting production by 2 million barrels per day in October. The following day, the EU will implement its embargo on Russian oil. European officials also recently announced a $60 per barrel price cap on Russian oil, which they intend to implement in coordination with the G7 and Australia on the same day their embargo goes into effect. Overall, bullish sentiments linger in the oil market as we head into the final month of the year.

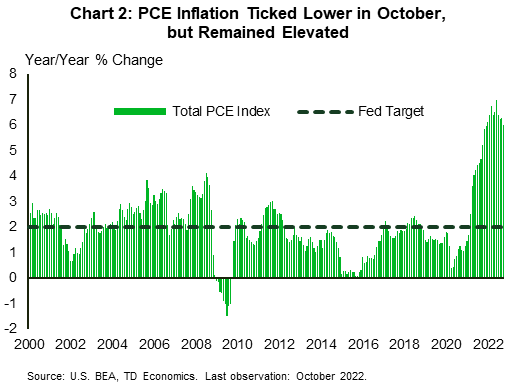

Personal income saw a healthy gain in October (+0.7% m/m), driven by strong growth in employee compensation (0.5% m/m) alongside one-time refundable tax credits issued by states. Consumers were keen to spend those gains, with spending rising even more (+0.8% m/m). That took the consumer savings rate to a 17-year low of 2.3%. It wasn’t all inflation either. Controlling for taxes and inflation, income rose 0.4% m/m. Real spending was up a healthy 0.5% m/m, which puts third quarter consumer spending on track for a healthy gain. Headline PCE inflation fell 0.2 percentage-points (ppts) to 6% y/y (Chart 2) while the Fed’s preferred core PCE measure fell 0.1ppts to 5% y/y.

Personal income saw a healthy gain in October (+0.7% m/m), driven by strong growth in employee compensation (0.5% m/m) alongside one-time refundable tax credits issued by states. Consumers were keen to spend those gains, with spending rising even more (+0.8% m/m). That took the consumer savings rate to a 17-year low of 2.3%. It wasn’t all inflation either. Controlling for taxes and inflation, income rose 0.4% m/m. Real spending was up a healthy 0.5% m/m, which puts third quarter consumer spending on track for a healthy gain. Headline PCE inflation fell 0.2 percentage-points (ppts) to 6% y/y (Chart 2) while the Fed’s preferred core PCE measure fell 0.1ppts to 5% y/y.Earlier in the week we heard from Chair Powell for the first time since the November FOMC meeting. His remarks were little changed overall, but markets reacted strongly to his statement that “the time for moderating the pace of rate increases may come as soon as the December meeting” in major financial news. This reaction, however, overlooked his reiteration that the FOMC has “a long way to go in restoring price stability” and that this will likely require “holding policy at a restrictive level for some time”. Coupled with his insistence that the FOMC will need to see “substantially more evidence to give comfort that inflation is actually declining” alongside the strong November jobs report, it is fair to say that their job is far from done.

Andrew Foran, Economist | 416-350-8927

Markets had to hit the ground running after the Thanksgiving holiday, with a full slate of economic data and financial news. The November jobs report, personal income and spending data for October, and FOMC Chair Powell’s speech on Wednesday were just the headliners. Markets rallied to start the week, but gains were pared back after the release of the November jobs report on Friday. At the time of writing, the S&P 500 is up 0.3% on the week while the ten-year yield is down 10bps to 3.59%.

Markets had to hit the ground running after the Thanksgiving holiday, with a full slate of economic data and financial news. The November jobs report, personal income and spending data for October, and FOMC Chair Powell’s speech on Wednesday were just the headliners. Markets rallied to start the week, but gains were pared back after the release of the November jobs report on Friday. At the time of writing, the S&P 500 is up 0.3% on the week while the ten-year yield is down 10bps to 3.59%. Personal income saw a healthy gain in October (+0.7% m/m), driven by strong growth in employee compensation (0.5% m/m) alongside one-time refundable tax credits issued by states. Consumers were keen to spend those gains, with spending rising even more (+0.8% m/m). That took the consumer savings rate to a 17-year low of 2.3%. It wasn’t all inflation either. Controlling for taxes and inflation, income rose 0.4% m/m. Real spending was up a healthy 0.5% m/m, which puts third quarter consumer spending on track for a healthy gain. Headline PCE inflation fell 0.2 percentage-points (ppts) to 6% y/y (Chart 2) while the Fed’s preferred core PCE measure fell 0.1ppts to 5% y/y.

Personal income saw a healthy gain in October (+0.7% m/m), driven by strong growth in employee compensation (0.5% m/m) alongside one-time refundable tax credits issued by states. Consumers were keen to spend those gains, with spending rising even more (+0.8% m/m). That took the consumer savings rate to a 17-year low of 2.3%. It wasn’t all inflation either. Controlling for taxes and inflation, income rose 0.4% m/m. Real spending was up a healthy 0.5% m/m, which puts third quarter consumer spending on track for a healthy gain. Headline PCE inflation fell 0.2 percentage-points (ppts) to 6% y/y (Chart 2) while the Fed’s preferred core PCE measure fell 0.1ppts to 5% y/y.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of November 25th, 2022

Financial News Highlights

- Minutes from the November FOMC meeting showed a sizeable majority of members were receptive to the idea of slowing the pace of rate hikes in the near-term.

- New home sales jumped 7.5% month-on-month (m/m), far outpacing expectations for a moderate decline, but remain down 5.8% year-on-year (y/y).

- Consumer sentiment declined in November for the first time since June, marking a return to the downward trend which started in the third quarter of 2021.

U.S. - FOMC Eyes Half-Point Hike

The holiday-shortened week was quiet overall, but did provide a healthy dose of Fed speak, new home sales data, and updated consumer sentiment readings in financial news. Due to lower trading volumes and shorter trading hours in the lead-up to the holiday, market movements this week were muted. The S&P 500 rose 1.5% on the week, while Treasury yields continued their gradual decline, with the 10-Year yield dropping 9 bps to 3.73% as of the time of writing.

The holiday-shortened week was quiet overall, but did provide a healthy dose of Fed speak, new home sales data, and updated consumer sentiment readings in financial news. Due to lower trading volumes and shorter trading hours in the lead-up to the holiday, market movements this week were muted. The S&P 500 rose 1.5% on the week, while Treasury yields continued their gradual decline, with the 10-Year yield dropping 9 bps to 3.73% as of the time of writing.

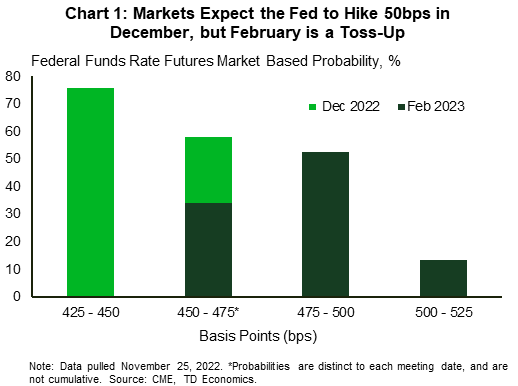

October’s CPI report has been the centerpiece of market thinking since its release two weeks ago. Fed speakers this week attempted to strike a balanced tone. San Francisco Fed President Daly started the week stating, “although one month of data does not a victory make, the latest inflation report had some encouraging numbers”. Cleveland Fed President Mester in a separate media appearance added that more work still needed to be done, but that “it makes sense that we can slow down a bit”.

The November FOMC minutes released on Wednesday echoed this sentiment, noting that “a substantial majority of [FOMC] participants judged that a slowing in the pace of increase would likely soon be appropriate”. As of the time of writing, markets are expecting the Fed to raise rates by 50bps in December (Chart 1) in financial news. Next week’s October PCE inflation and November jobs reports should provide further clarification on the Fed’s progress thus far and how much further it may have to go.

November new home sales surprised to the upside, rising 7.5% month-on-month (m/m) versus an expected decline. However, sales are still down on the year (-5.8% year-on-year, y/y). We don’t expect November’s uptick to be sustained. Mortgage rates remain elevated, homebuilder sentiment is at its lowest level since June 2012 (excluding the early pandemic low), and existing home sales have declined for nine consecutive months as of November.

November new home sales surprised to the upside, rising 7.5% month-on-month (m/m) versus an expected decline. However, sales are still down on the year (-5.8% year-on-year, y/y). We don’t expect November’s uptick to be sustained. Mortgage rates remain elevated, homebuilder sentiment is at its lowest level since June 2012 (excluding the early pandemic low), and existing home sales have declined for nine consecutive months as of November.

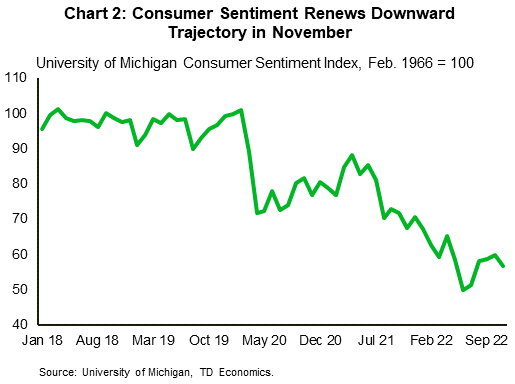

On the consumer front, we saw the University of Michigan consumer sentiment index reading for November drop 3.1 points to 56.8 (Chart 2). The index had previously notched four consecutive months of gains after a precipitous drop in the second quarter of this year, as the robustness of the labor market, combined with a build-up of savings had provided a cushion to consumers. However, with the unemployment rate ticking higher, job growth slowing, and excess savings winding down, the dual shock of higher rates and higher prices present a stronger headwind.

On a cheerier note, holiday air travel is expected to roughly return to its pre-pandemic level this week. Coupled with the expected spike in retail sales driven by Black Friday deals, the Thanksgiving holiday should provide partial short-term insulation from some aspects of the impending economic slowdown. Next week we’ll see whether job growth decelerated in November, or whether the Fed may have more to think about at its last meeting of the year.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of November 18th, 2022

Financial News Highlights

- Results from the midterm elections showed the Democrats maintained control of the Senate but lost their majority in the House of Representatives.

- U.S. housing data continue to slide in October, with housing starts down 4.1% m/m to 1.4 million units, while existing home sales fell 5.9% m/m to 4.3 million.

- Retail sales surprised to the upside in October, rising by 1.3% m/m. Gains were relatively broad based and suggest the U.S. consumer remains on a firm footing. Real consumer spending is set to accelerate to 3% in Q4.

Consumer Resilience on a Timer

After a week of ballot counting, results from the midterm elections showed that the Democrats maintained control of the Senate but lost their majority in the House of Representatives. With the Republican’s now having narrow control of the House, we have returned to a divided Congress, limiting prospects of new legislation over the next two years.

After a week of ballot counting, results from the midterm elections showed that the Democrats maintained control of the Senate but lost their majority in the House of Representatives. With the Republican’s now having narrow control of the House, we have returned to a divided Congress, limiting prospects of new legislation over the next two years.

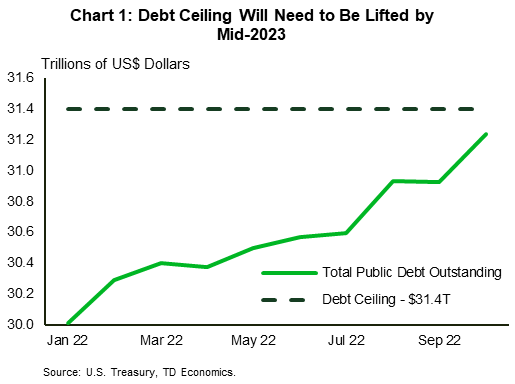

A partisan Congress raises the odds of another government shutdown or debt-ceiling showdown at some point next year (Chart 1) in financial news. We could get a firsthand glimpse of what’s to come as early as next month when the current ‘continuing resolution’ funding government spending expires on December 16th. At a minimum, Congress will need to negotiate another short-term patch to keep the federal government open. The other challenge that will come up in the coming months is the need to raise the debt-ceiling. Fortunately, the U.S. Treasury is estimated to have enough wiggle room in its existing cash holdings to fund the government through at least mid-2023.

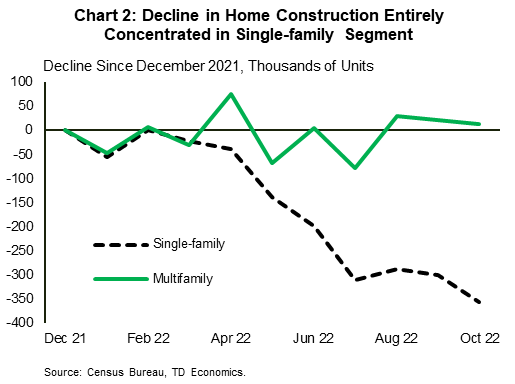

Looking to this week’s economic data, the impact of higher interest rates continued to tighten its grip on the housing sector. New home construction fell 4.2% m/m to 1.4 million units in October and is now down 19.4% since the beginning of the year. While the pullback continues to be concentrated across the single-family segment, the recent plateauing in multifamily permits suggests it too has peaked (Chart 2). Things look even more dire in the resale market. Mortgage rates reached 7.2% in October, and sales fell by another 5.9% m/m to 4.3 million and are now (outside of the pandemic lockdown period) at the lowest level since 2011. Inventory has remained tight so far and so the impact to prices has been small, with the median home price down just 3.5% from its peak. Because most homeowners hold mortgages originated at rates lower than today’s prevailing rate, listings are unlikely to spike like during the last housing crisis. As a result, the market will remain undersupplied for some time, limiting the downside pressure on prices.

In stark contrast to the housing sector, the U.S. consumer continued to show considerable staying power in October. Retail sales came in much better than expected, rising by 1.3% m/m. Indeed, some of the strength in October was already telegraphed earlier in the month when new vehicle sales jumped 10% m/m to 14.9 million units in financial news. However, even after stripping out autos, sales at gasoline stations, and building materials, the ‘control’ measure still rose by a healthy 0.8% m/m.

In stark contrast to the housing sector, the U.S. consumer continued to show considerable staying power in October. Retail sales came in much better than expected, rising by 1.3% m/m. Indeed, some of the strength in October was already telegraphed earlier in the month when new vehicle sales jumped 10% m/m to 14.9 million units in financial news. However, even after stripping out autos, sales at gasoline stations, and building materials, the ‘control’ measure still rose by a healthy 0.8% m/m.

After incorporating the October retail sales data, our current tracking for Q4 GDP sits at 2.2%, with consumer spending expected to expand by 3%. This is an acceleration from Q3 and underscores the degree of resilience we’re still seeing from the U.S. consumer. However, it would be a stretch to believe that the rapid adjustment in interest rates won’t eventually take a toll. Let’s not forget, the Fed still has ‘a ways to go’ before even reaching its terminal rate. Moreover, it can take anywhere from 12-18 months to feel the full effect of higher interest rates. By this logic, we expect a broader demand adjustment to begin early next year, with growth expected to fall to a stall-speed in 2023.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of November 11th, 2022

Financial News Highlights

- Republicans look to have won control of the House in this week’s midterm elections. The Senate race remains too close to call. With Washington more divided, major spending and tax changes are less likely, while some risks increase (i.e., the potential for a government shutdown).

- CPI inflation eased in October, with headline CPI decelerating to 7.7% y/y (from 8.2%) and core CPI cooling to 6.3% y/y (from 6.6%). Shelter costs remained a key contributor to inflation.

- Small business confidence pulled back a bit in October, but job openings remained unchanged near record highs.

Markets Cheer Inflation Easing a Touch

The midterm elections took center stage for much of the week, although markets were most encouraged by good news on the inflation front on Thursday in financial news. Republicans look to have won control of the House, capturing an estimated 208 seats thus far (vs. 185 for Democrats), while the Senate remains too close to call. We may need to wait until Georgia’s runoff election on December 6th, to know the final result, depending on races in Arizona and Nevada.

The midterm elections took center stage for much of the week, although markets were most encouraged by good news on the inflation front on Thursday in financial news. Republicans look to have won control of the House, capturing an estimated 208 seats thus far (vs. 185 for Democrats), while the Senate remains too close to call. We may need to wait until Georgia’s runoff election on December 6th, to know the final result, depending on races in Arizona and Nevada.

Either way, Washington is looking more divided than it was a week ago, and the chance that new major policy measures get the three required checkmarks – House, Senate and White House – have diminished. Indeed, large scale fiscal spending measures and major tax changes seem unlikely over the next two years. In this vein, the midterms should not have a major impact on economic growth in financial news. There are, however, risks that come with a divided Congress. One concerning aspect is the potential for a lack of agreement to fund government programs in the near-to-medium term, which could lead to a government shutdown, or debt-ceiling standoff, which raises the (unlikely) risk of a default on debt or leave other bills unpaid. These issues, which have the potential to significantly disrupt financial markets, as they’ve done in the past, are added risks for a slowing economy in the year ahead.

Inflation was likely top of mind for many voters as they headed to the polls, as it has been taking a sizable bite out of consumers’ wallets this year. The Consumer Price Index (CPI) showed that inflation eased in October, for both headline and core CPI, with the latter decelerating to 6.3% year-on-year (y/y) from 6.6% in the month prior (Chart 1). In month-over-month (m/m) terms, core CPI decelerated meaningfully to 0.3% in October from 0.6% previously. Core goods prices declined 0.4% (m/m) amidst a pullback in several categories such as appliances, apparel and used car prices. Price growth across core services (0.5%) also moderated from last month’s gain of 0.8%, driven by a notable pullback in health care services (-0.6%). However, shelter costs (0.8%) remained a meaningful contributor.

All in all, inflation has eased a bit, in part because of the pullback in core goods prices. However, it remains well above the Fed’s comfort zone, and (without wanting to sound like a broken record) we’re likely to see continued gains in the shelter component over the near term (see here). So, we’re not out of the woods just yet.

All in all, inflation has eased a bit, in part because of the pullback in core goods prices. However, it remains well above the Fed’s comfort zone, and (without wanting to sound like a broken record) we’re likely to see continued gains in the shelter component over the near term (see here). So, we’re not out of the woods just yet.

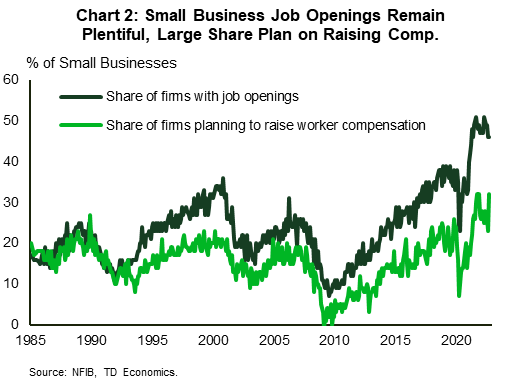

As Fed Chair Powell noted recently, the Fed has reached a point where it will dial back the pace of rate hikes, but there’s quite a bit more to be done in raising rates. Underpinning this hawkish tilt is the broad resilience in the labor market. Job openings for instance, have eased a bit, but remain plentiful – a message echoed by the NFIB small business survey (Chart 2). Still, cracks continue to form in some corners of the economy, case in point the tech sector. Layoffs at Meta and Redfin (online real estate broker) amounting to 13% of their workforces added to the string of cuts announced in the tech space this year. Meanwhile, the higher interest environment is expected to continue weighing on the housing market, with weak prints likely to follow in next week’s housing starts and existing home sales reports. Bringing inflation down comes at a cost.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of November 4th, 2022

Financial News Highlights

- The Fed increased the monetary policy rate by 75 basis points to a range of 3.75-4%, opened the door to a slower pace of tightening, while also setting expectations for a higher terminal rate.

- The ISM purchasing mangers’ indexes weakened in October, suggesting that demand is softening.

- The economy added 261k new jobs, while unemployment rate rose marginally to 3.7%. It will take much more of a slowdown for the Fed to be convinced that pressures from the labor market are moderating.

A Hawkish Pivot

On Wednesday, the Fed increased the monetary policy rate by 75 basis points to a range of 3.75-4% (Chart 1) in major financial news. The hike itself was expected, what captured headlines was the Fed’s pledge to “take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” In translation, the Fed plans to take a more measured approach to rate hikes going forward and opens the door to a slower pace of tightening. This sent bond and stock markets higher.

On Wednesday, the Fed increased the monetary policy rate by 75 basis points to a range of 3.75-4% (Chart 1) in major financial news. The hike itself was expected, what captured headlines was the Fed’s pledge to “take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” In translation, the Fed plans to take a more measured approach to rate hikes going forward and opens the door to a slower pace of tightening. This sent bond and stock markets higher.

Thirty minutes later, Chair Powell poured cold water on those animal spirits by clarifying that despite a potentially slower pace of hiking, the terminal policy rate is likely higher than what FOMC members expected in September. He pointed out that the labor market is very tight, and that consumers still have a mountain of excess savings to keep demand healthy. Therefore, further tightening is likely going to be required to rein in inflation. He further emphasized that it is “very premature” to consider pausing rate hikes, which soured market sentiment, pushing equity prices 3.5% lower relative to last week.

Despite Powell emphasizing strength in demand, leading business indicators – the ISM purchasing managers indexes – weakened in October. While the headline manufacturing index just managed to stay expansionary, the new orders and new export orders indexes continued contracting for the second and third straight month, respectively. Services activity also slowed, with demand factors expansion now clearly on the downward trend. This means that the cumulative impact of rate hikes might be catching up to consumers. However, more concerning to the Fed is that following five straight months of decline, the prices paid component of the services index suddenly accelerated. This suggests that the largest sector of the economy is still facing faster and more widespread price increases.

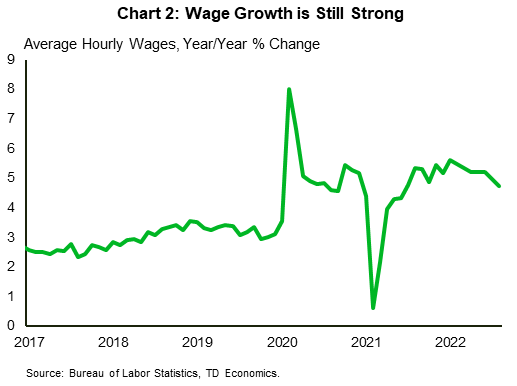

October’s jobs report provided little progress on the Fed’s mission to bring the labor market back into balance. The economy added 261k new jobs, above market expectations for a larger slow down. Meanwhile, the unemployment rate rose by two tenths of a percentage point to 3.7% in the household survey, which showed job losses of 328k in further financial news. While that is an increase, 3.7% is still a very low level historically. The tight labor market showed up in average hourly earnings growth, which eased only slightly to a still very healthy 4.7% year-on-year (Chart 2).

October’s jobs report provided little progress on the Fed’s mission to bring the labor market back into balance. The economy added 261k new jobs, above market expectations for a larger slow down. Meanwhile, the unemployment rate rose by two tenths of a percentage point to 3.7% in the household survey, which showed job losses of 328k in further financial news. While that is an increase, 3.7% is still a very low level historically. The tight labor market showed up in average hourly earnings growth, which eased only slightly to a still very healthy 4.7% year-on-year (Chart 2).

With the Fed laser focused on the bringing down inflation, it will take much more of a slowdown to be convinced that pressures from the labor market are moderating. For now, erring on the hawkish side remains the Fed’s best option. Looking ahead to next week, the CPI report on Thursday may provide some good news with consensus hoping for a slight moderation in price gains. Markets will also be watching the mid-term elections with recent polls pointing to a Republican majority in Congress, resulting in a divided government. While a divided government is historically positive for risk assets, it could result in more fiscal restraint, which would help the Fed at the margin in reigning in inflation.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of October 28th, 2022

Financial News Highlights

- The U.S. economy left behind the declines recorded in the first half of 2022, with GDP growth accelerating to 2.6% (ann.) in the third quarter. The headline was flattered by an outsized contribution from net exports, whereas private domestic drivers remained soft.

- The weakest area of the third quarter GDP report was residential investment, which fell 26% (ann.). Outside of the pandemic, this was the sharpest pullback since 2010.

- With mortgage rates currently topping 7%, there’s more weakness in the cards for housing. Pending home sales, a leading indicator of existing home sales, fell for the fourth consecutive month by a massive 10.2% m/m in September.

Fed’s Preferred Inflation Gauge Remains Hot

U.S. Treasury yields trended lower this week as investors digested mixed signals from the economy and earnings reports in financial news. The 10-year yield has fallen to around 4% as of writing after topping 4.3% late last week. Equities were trekked higher, with the S&P 500 looking to end the week up about 2.9% as at the time of writing.

U.S. Treasury yields trended lower this week as investors digested mixed signals from the economy and earnings reports in financial news. The 10-year yield has fallen to around 4% as of writing after topping 4.3% late last week. Equities were trekked higher, with the S&P 500 looking to end the week up about 2.9% as at the time of writing.

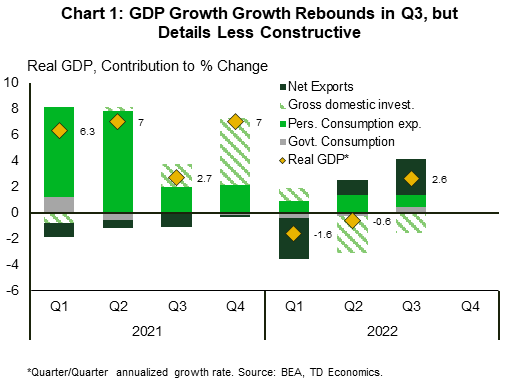

The U.S. economy left behind the negative prints recorded in the first half of the year, with growth accelerating to 2.6% annualized (ann.) in the third quarter – a touch higher than market expectations (2.3%). However, the headline number was flattered by an outsized gain in net exports (Chart 1). Meanwhile, private domestic drivers were largely unchanged, adding only 0.1 percentage points (pp) to headline growth – down from 0.5 pp in the second quarter. Consumer spending remained supportive, but its contribution to growth diminished in light of elevated inflation and a higher interest rate environment. Consumers continued to tap into the pent-up demand for services (up 2.8% ann.), while pulling back on goods – declined by 1.2%.

The weakest area weighing on domestic demand was residential investment, which fell 26% (ann.), marking the sixth consecutive quarterly decline. Outside of the pandemic, this was the largest quarterly decline since the start of 2010. The outsized pullback was the result of sharp declines in homes sales and residential construction through the third quarter, as higher interest rates have tighten the grip on the housing sector.

Housing is one of the most interest-sensitive areas of the economy and with rates elevated – with the 30-year fixed mortgage rate currently sitting at 7.1% – it is likely that there will be more weakness over the coming months. Several recent indicators support this view. Pending home sales, a leading indicator of existing home sales, fell by a massive 10.2% m/m in September. Meanwhile, mortgage applications to purchase a home dropped 2% last week from the week prior and were 42% lower than a year ago.

Housing is one of the most interest-sensitive areas of the economy and with rates elevated – with the 30-year fixed mortgage rate currently sitting at 7.1% – it is likely that there will be more weakness over the coming months. Several recent indicators support this view. Pending home sales, a leading indicator of existing home sales, fell by a massive 10.2% m/m in September. Meanwhile, mortgage applications to purchase a home dropped 2% last week from the week prior and were 42% lower than a year ago.

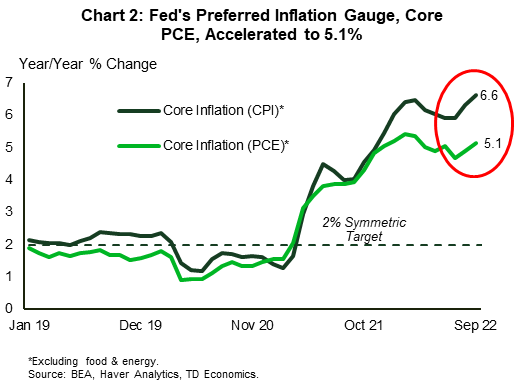

The housing market is also central to the Fed’s rate setting calculus. Market data tells us that rent growth is decelerating and that home prices are falling. However, as we explain in a recent note, market price changes take time to filter down to their corresponding inflation metrics, which means that shelter inflation is likely to continue to push up on core inflation over the next several months in financial news. This may be less of an issue for the Fed’s preferred inflation gauge, Core PCE – which accelerated to 5.1% Y/Y in September (Chart 2) – where shelter carries a lower weight than CPI (see here for differences). However, CPI gets released ahead of PCE, grabbing the market’s focus and adding to the Fed’s communication challenge.

The bottom line is that if the Fed does not pivot toward a more forward-looking stance, the result will be a more restrictive monetary policy than otherwise required, increasing the chances of a policy ‘error’. While the Fed will likely deliver on another 75-basis point hike next week, we expect the FOMC to soon start to pivot on its communication as the Fed will need to dial back on the pace of rate hikes.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of October 21st, 2022

Financial News Highlights

- UK policymakers abruptly U-turned on its recently proposed “mini” budget, forcing Prime Minister Liz Truss to resign.

- Existing home sales fell 1.5% m/m in September to 4.7 million units. Sales have now fallen for eight consecutive months and are down 23% year-to-date.

- Housing starts fell 8.1% m/m to 1.4 million units, with declines felt across both the single-family (-4.7% m/m) and multifamily (-13.2% m/m) segments. The number of units currently under construction continued to edge higher, rising to a historic high of 1.7 million units.

Hey Housing, How Low Can You Go?

This week brought some calming to global financial markets, helped along by UK policymakers abrupt U-turn on its proposed “mini” budget which had included £45 billion of unfunded tax cuts in financial news. UK Prime Minister Liz Truss resigned on Thursday, leaving the Conservative Party to elect a new leader sometime later next week. Yields on longer duration Gilts were down 50 basis points (bps) on the week, while the Sterling lost a modest 0.5% vis’-a-vis the dollar.

This week brought some calming to global financial markets, helped along by UK policymakers abrupt U-turn on its proposed “mini” budget which had included £45 billion of unfunded tax cuts in financial news. UK Prime Minister Liz Truss resigned on Thursday, leaving the Conservative Party to elect a new leader sometime later next week. Yields on longer duration Gilts were down 50 basis points (bps) on the week, while the Sterling lost a modest 0.5% vis’-a-vis the dollar.

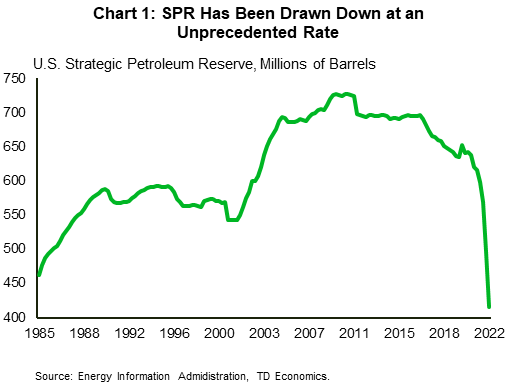

Investors also continued to digest last week’s CPI report, which led to further pressure on U.S. yields. At the time of writing, the 10-year has moved up an additional 30-bps this week to 4.3%, reaching both a new cyclical high and also the highest level since mid-2007. Top of mind on the inflation front, has been the recent turn higher in energy prices. Indeed, since peaking in July, gasoline prices had fallen by nearly 30% through mid-September. However, the recent announcement by OPEC+ members to pare back production quotas has led to renewed pressure on oil prices, which has also pulled gasoline prices higher. In an effort to provide some relief to consumers, the Biden Administration announced this week that they will be digging further into its Special Petroleum Reserve (SPR) and releasing an additional 15 million barrels in December. After including this week’s announcement, the cumulative release through December will total nearly 180 million barrels over the six-month preceding period in further financial news. And its impact on gas prices cannot be understated. The U.S. Treasury estimated that the release of reserves to date has lowered retail fuel prices by as much as 42 cents per-gallon. That has come at the expense of an unprecedented drawdown in the SPR, which will eventually need to be topped up (Chart 1). According to the Biden Administration, this will happen once oil prices fall below $70 per-barrel.

The renewed pressure on interest rates has brought the housing market squarely back into focus. With the 30-year fixed mortgage rate now at 7.25%, buyer affordability has eroded to levels beyond the lows pre-dating the mid-2000 housing crisis. Demand continues to soften, with existing home sales falling 1.5% m/m to 4.7 million units in September and are now down 23% year-to-date. No reprieve appears to in sight, as leading indicators such as pending home sales and mortgage applications both point to further weakness in the months ahead.

The renewed pressure on interest rates has brought the housing market squarely back into focus. With the 30-year fixed mortgage rate now at 7.25%, buyer affordability has eroded to levels beyond the lows pre-dating the mid-2000 housing crisis. Demand continues to soften, with existing home sales falling 1.5% m/m to 4.7 million units in September and are now down 23% year-to-date. No reprieve appears to in sight, as leading indicators such as pending home sales and mortgage applications both point to further weakness in the months ahead.

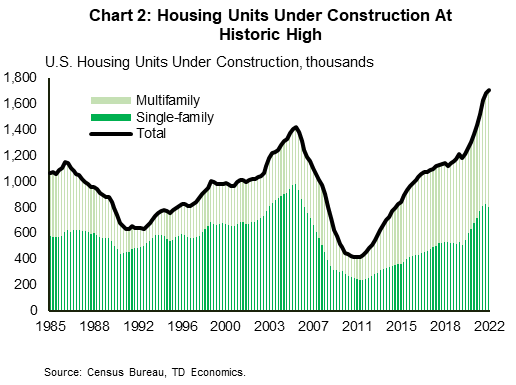

Beyond the sales side, the combination of rising rates and elevated material costs has also heavily weighed on builder sentiment, with September housing starts falling 8.1% m/m in September. Declines were seen across both the single-family (-4.7% m/m) and multifamily (-13.2% m/m) segments, though the former has disproportionately accounted for most of the pullback year-to-date. Interestingly, the number of homes currently under construction remains at a historical high, as labor and building material shortages have significantly lengthen the time it takes to build a home (Chart 2). Perhaps most worrying is the fact that the number of single-family homes under construction currently sits at a 16-year high. With demand in this segment quickly receding, builders have already started reducing prices and adding additional incentives in an effort to attract buyers. However, with record amounts of new supply still in the pipeline, further declines in home prices are all but certain.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.