Financial News for the Week of October 14th, 2022

Financial News Highlights

- This week’s Consumer Price Index report was another disappointing print, as inflation continues to be stubbornly high.

- Not all of it was bad news as core goods price inflation continued to moderate in September.

- Tighter financial conditions, improving supply chains, and eroding disposable incomes should work to weigh on demand and help the Fed in its fight against inflation.

U.S. - Looking for Silver Linings

Equity markets are in positive territory on the week despite the disappointment in the September inflation data in financial news. The Fed is struggling to contain inflation, and September’s reading was hotter than expected once again. The Fed still has its work cut out for it in bringing inflation back down. However, there were a few silver linings in inflation’s gray cloud that give some reasons to believe that the fight against inflation may be turning.

Equity markets are in positive territory on the week despite the disappointment in the September inflation data in financial news. The Fed is struggling to contain inflation, and September’s reading was hotter than expected once again. The Fed still has its work cut out for it in bringing inflation back down. However, there were a few silver linings in inflation’s gray cloud that give some reasons to believe that the fight against inflation may be turning.

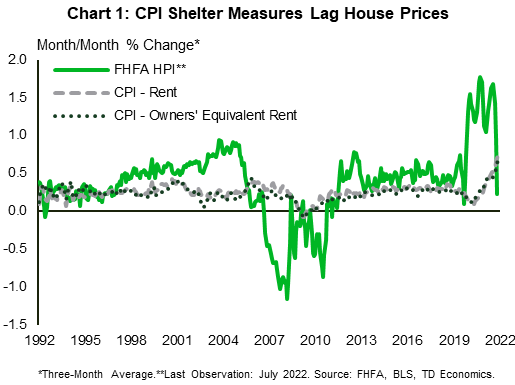

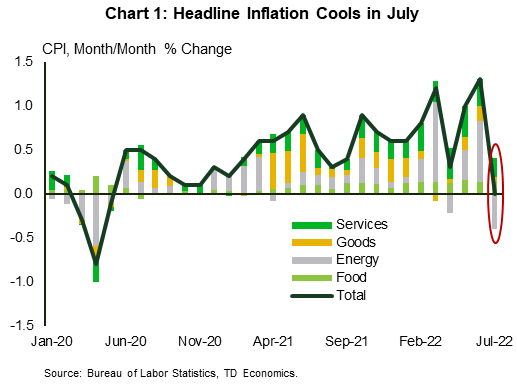

First up, the bad news. Consensus expectations for a +0.2% month-over-month (m/m) reading on headline inflation were shattered by the +0.4% increase, while expectations for core inflation of 0.4% were also handily beat by the 0.6% uptick. Underpinning the rise were strong price growth in core services (+0.8% m/m), and food (+0.8% m/m). The core services print is what’s of interest as these prices are notoriously sticky. Shelter costs (+0.7% m/m), medical care services (+1.0% m/m), and transportation services (+1.9% m/m) were all well above what the Fed would like to see. Of these, the shelter component is, by far, the largest contributor to the basket and will be crucial to tempering inflation. To this end, the rate hikes are working, as evidenced by the plateau in home prices. That said, this will take time to translate into the CPI’s measure of homeowner’s equivalent rent (Chart 1), but things are moving in the right direction.

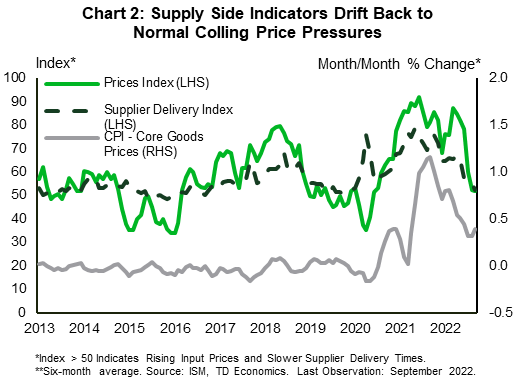

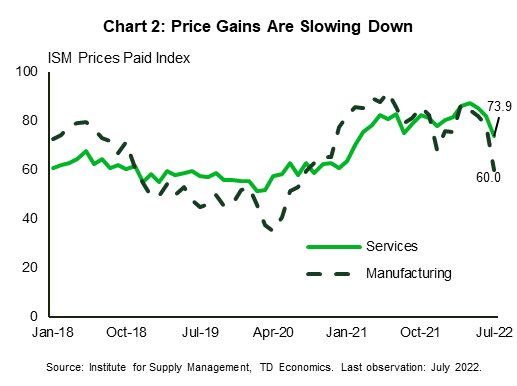

Indeed, core goods price inflation continued to moderate in September (+0.0% m/m), after having risen 0.5% in August. Helping keep a lid on things were a 1.1% m/m pull-back in used vehicles prices and a 0.3% decline in apparel prices. After the run-up over the past year, supply chain improvements are helping ease price pressures (Chart 2). These developments are important as they were always going to be among the first signs that inflation was moderating. Layer in this week’s NFIB report that showed a slightly smaller share of firms anticipating further wage gains and price increases, and the evidence for moderating inflation builds.

The Fed will welcome the signs of improvement, but if this week’s retail sales report shows anything it’s that even though things may be trending in the right direction there is still ample demand out there. The flat monthly reading registered below expectations for a modest 0.2% m/m gain but was weighed down by falling gasoline prices. The core control group (that goes into the GDP calculation) rose a solid 0.4% m/m, showing consumers are still very active.

The Fed will welcome the signs of improvement, but if this week’s retail sales report shows anything it’s that even though things may be trending in the right direction there is still ample demand out there. The flat monthly reading registered below expectations for a modest 0.2% m/m gain but was weighed down by falling gasoline prices. The core control group (that goes into the GDP calculation) rose a solid 0.4% m/m, showing consumers are still very active.Given that things are approaching a turning point, the Fed will be considering any weakness in the data. Indeed, FOMC member Lael Brainard highlighted that “output has decelerated more than anticipated” and emphasized the importance of “moving forward deliberately and in a data-dependent manner” amid “elevated global economic and financial uncertainty”. It would seem she is laying the groundwork for an eventual slowing in the pace of rate hikes. After 300 basis points of tightening this year, a slowing will be warranted soon in financial news. Looking forward, higher prices and diminished excess savings will help cool demand for goods and services. Coupled with improving supply-side conditions this will work to temper inflation. With other factors now starting to help the Fed in its mission, we anticipate this rate hiking cycle will top out at 4.5%.

Andrew Hencic, Senior Economist

Equity markets are in positive territory on the week despite the disappointment in the September inflation data in financial news. The Fed is struggling to contain inflation, and September’s reading was hotter than expected once again. The Fed still has its work cut out for it in bringing inflation back down. However, there were a few silver linings in inflation’s gray cloud that give some reasons to believe that the fight against inflation may be turning.

Equity markets are in positive territory on the week despite the disappointment in the September inflation data in financial news. The Fed is struggling to contain inflation, and September’s reading was hotter than expected once again. The Fed still has its work cut out for it in bringing inflation back down. However, there were a few silver linings in inflation’s gray cloud that give some reasons to believe that the fight against inflation may be turning.

The Fed will welcome the signs of improvement, but if this week’s retail sales report shows anything it’s that even though things may be trending in the right direction there is still ample demand out there. The flat monthly reading registered below expectations for a modest 0.2% m/m gain but was weighed down by falling gasoline prices. The core control group (that goes into the GDP calculation) rose a solid 0.4% m/m, showing consumers are still very active.

The Fed will welcome the signs of improvement, but if this week’s retail sales report shows anything it’s that even though things may be trending in the right direction there is still ample demand out there. The flat monthly reading registered below expectations for a modest 0.2% m/m gain but was weighed down by falling gasoline prices. The core control group (that goes into the GDP calculation) rose a solid 0.4% m/m, showing consumers are still very active.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of October 7th, 2022

Financial News Highlights

- The last jobs report before the Federal Reserve’s November meeting showed that 263k jobs were added in September, bringing the unemployment rate back down to 3.5%.

- ISM Manufacturing and Services PMIs indicate that demand for goods is slowing swiftly, while demand for services is slowing more gradually and has yet to yield substantial ground.

- Oil supply reductions signaled by OPEC+ this week will raise energy prices (see commentary), creating another headache for the Federal Reserve.

More Jobs, Less Oil, No Pivot

The first week of the third quarter was largely centered around labor market conditions and their potential impact on the policy stance of the Federal Reserve at their November meeting in four weeks’ time in financial news. Lower job openings, higher jobless claims, and slowing job growth all provided some evidence of a softening labor market, but a lower unemployment rate and solid wage growth clouded the aggregate outlook. Equity markets rallied to start the week with hopes of a ‘Fed pivot’ before retreating on Friday as the jobs report drove yields higher and dampened the prospect of a less aggressive Fed. As of the time of writing, the S&P 500 is still up 2.5% for the week, while the ten-year treasury yield sits at 3.9% - 10bps higher than it was to start the day.

The first week of the third quarter was largely centered around labor market conditions and their potential impact on the policy stance of the Federal Reserve at their November meeting in four weeks’ time in financial news. Lower job openings, higher jobless claims, and slowing job growth all provided some evidence of a softening labor market, but a lower unemployment rate and solid wage growth clouded the aggregate outlook. Equity markets rallied to start the week with hopes of a ‘Fed pivot’ before retreating on Friday as the jobs report drove yields higher and dampened the prospect of a less aggressive Fed. As of the time of writing, the S&P 500 is still up 2.5% for the week, while the ten-year treasury yield sits at 3.9% - 10bps higher than it was to start the day.

Non-farm payrolls capped the week, coming in slightly above market expectations with 263k jobs added in September. The unemployment rate ticked down by 0.2 percentage points, back to its July low of 3.5% as the labor force was virtually unchanged from its August level. Combined with steady growth in average hourly earnings of 0.3% month-over-month (m/m), it is clear that the labor market remains strong – a sentiment that is not lost on financial markets which are now pricing in a fourth 75bps hike by the Fed in November with 80% probability.

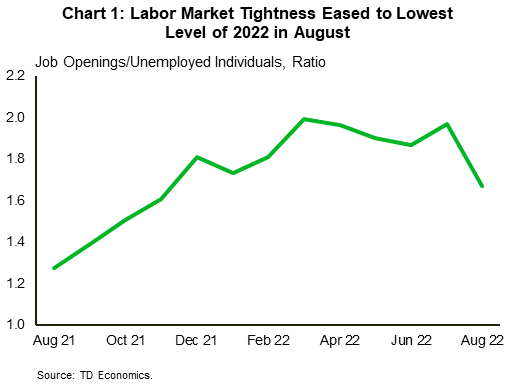

Earlier in the week, we saw job openings for August decline by 10% to reach their lowest level since June 2021. This brought the ratio of job openings to unemployed individuals down to 1.67 - its lowest level since November 2021 (Chart 1). This will be welcomed by Jerome Powell who noted that this ratio was exceptionally high in his September press conference. Jobless claims also displayed signs of softening with a 15.3% increase last week, although this only brings the level of claims back to where it was a month ago. On aggregate, the labor market will need to soften further in order for inflation to sustainably return to the Fed’s target range.

Earlier in the week, we saw job openings for August decline by 10% to reach their lowest level since June 2021. This brought the ratio of job openings to unemployed individuals down to 1.67 - its lowest level since November 2021 (Chart 1). This will be welcomed by Jerome Powell who noted that this ratio was exceptionally high in his September press conference. Jobless claims also displayed signs of softening with a 15.3% increase last week, although this only brings the level of claims back to where it was a month ago. On aggregate, the labor market will need to soften further in order for inflation to sustainably return to the Fed’s target range.

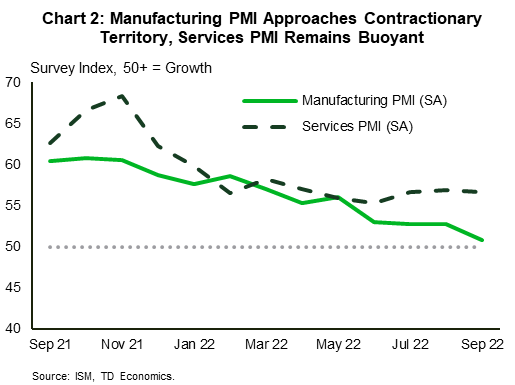

One sector which is showing clear signs of slowing is manufacturing, with the ISM Manufacturing PMI quickly approaching contractionary territory (Chart 2) in financial news. The index dropped by 1.9 percentage points to 50.9 in September, reaching its lowest level since May 2020. Slowing demand was a leading contributor to the lower reading, with both new orders and new export orders contracting. Some of this demand has shifted into the service sectors, with the ISM Services PMI remaining well in expansionary territory, though it too is showing some signs of slowing. While the reading for September was slightly above expectations at 56.7, a slowdown in the backlog of orders as well as new orders could be indicative of the early signs of peak demand for services.

International events this week will serve to further complicate the Fed’s already difficult position, with OPEC+ signaling that it will curtail oil production by 2 million barrels-per-day (bpd). National gas prices, which have been rising for the past few weeks, will likely rise further and return to making positive contributions to headline inflation. Next week’s CPI data for September will provide a better picture of recent developments on the prices front, but as it stands now the Fed will likely remain resolute in its current hawkish stance.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of September 23rd, 2022

Financial News Highlights

- The Federal Reserve raised interest rates by 75bps for the third consecutive meeting, bringing the federal funds rate to its highest level in 14 years.

- FOMC Chair Powell reiterated his Jackson Hole speech, stating that the Fed is willing to tolerate slower growth and higher unemployment to bring inflation back to its 2% target.

- Interest rate sensitive sectors continue to feel the effects of past rate hikes, with existing home sales down 0.4% (m/m) in August, marking the seventh consecutive month of declines.

The FOMC Aims High

The last days of summer 2022 were centered around the FOMC meeting which ended Wednesday with another 75bps hike, bringing the federal funds rate to its highest level in 14 years in financial news. The announcement was largely expected by markets after last week’s CPI print came in hotter than expected, with core CPI rising to 0.6% month-over-month (m/m). However, the Fed’s updated projections underlined a narrative that was more hawkish than what markets had been expecting, resulting in a volatile reaction from equity and bond markets. The S&P 500 ended the day down by 1.7% and the two-year treasury yield, which briefly rose above 4.1%, closed back at its pre-meeting level of 4%. Further digestion of the decision has seen the two-year yield rise to 4.2% and the S&P 500 retreat further, ending the week down 4.1% as of the time of writing.

The last days of summer 2022 were centered around the FOMC meeting which ended Wednesday with another 75bps hike, bringing the federal funds rate to its highest level in 14 years in financial news. The announcement was largely expected by markets after last week’s CPI print came in hotter than expected, with core CPI rising to 0.6% month-over-month (m/m). However, the Fed’s updated projections underlined a narrative that was more hawkish than what markets had been expecting, resulting in a volatile reaction from equity and bond markets. The S&P 500 ended the day down by 1.7% and the two-year treasury yield, which briefly rose above 4.1%, closed back at its pre-meeting level of 4%. Further digestion of the decision has seen the two-year yield rise to 4.2% and the S&P 500 retreat further, ending the week down 4.1% as of the time of writing.

Chair Powell used his press conference to reiterate his Jackson Hole speech, emphasizing that the Fed would not shy away from its fight to bring inflation back to its 2% target. Powell noted that a restrictive policy stance would likely be required for some time and that this would likely result in a sustained period of below trend growth and softer labor market conditions. Progress on the inflation front has been mixed so far with headline inflation showing early signs of peaking (largely due to falling gas prices), but core inflation has remained stubbornly high which has prompted the Fed to hold the line on its aggressive policy stance.

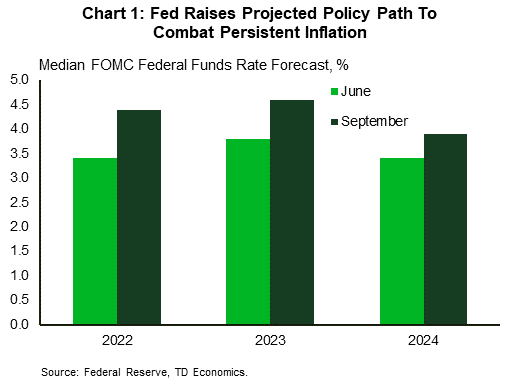

According to the updated Fed projections, the median estimate for the federal funds rate (FFR) is now expected to reach 4.4% by year-end, a full percentage point above their previous estimate in June (Chart 1). FOMC members expect that further rate increases will be required in 2023, with the median projection for the terminal rate reaching 4.6%. This represents roughly 150bps of further rate increases from the current level of 3 – 3.25.

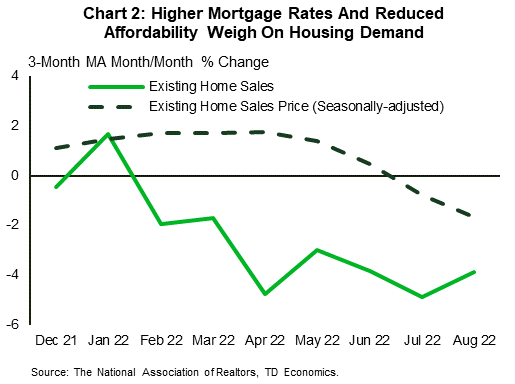

Elsewhere this week, the interest rate sensitive housing sector continued to show further signs of softening. Existing home sales declined by 0.4% m/m in August, marking its seventh consecutive month of declines. Seasonally adjusted median home prices also dipped deeper into negative territory, falling for the three straight months (Chart 2). Reduced affordability continues to act a headwind on consumer demand for housing, and with mortgage rates now well above 6%, that headwind is turning into a gale. Higher rates are not only affecting sales, but also residential construction. While housing starts rebounded in August (rising 12% m/m to 1.58M units), the 3-month moving average of year-over-year changes is still down 5.4%. Moreover, a pullback in August housing permits suggests more weakness in the months ahead. This lines up with recent readings of builder sentiment, which has now fallen for nine consecutive months and currently sits at a 28-month low.

Elsewhere this week, the interest rate sensitive housing sector continued to show further signs of softening. Existing home sales declined by 0.4% m/m in August, marking its seventh consecutive month of declines. Seasonally adjusted median home prices also dipped deeper into negative territory, falling for the three straight months (Chart 2). Reduced affordability continues to act a headwind on consumer demand for housing, and with mortgage rates now well above 6%, that headwind is turning into a gale. Higher rates are not only affecting sales, but also residential construction. While housing starts rebounded in August (rising 12% m/m to 1.58M units), the 3-month moving average of year-over-year changes is still down 5.4%. Moreover, a pullback in August housing permits suggests more weakness in the months ahead. This lines up with recent readings of builder sentiment, which has now fallen for nine consecutive months and currently sits at a 28-month low.

None of this will sway the Federal Reserve to lift its foot off the pedal as they continue to drive interest rates higher to bring down inflation. With the FOMC charting a course that nearly inverts the 2007/2008 run-down in the policy rate, the current and expected future path of monetary policy will continue to act as an increasing weight on the economy moving forward in financial news.

Andrew Foran, Economist | Andrew.Foran@td.com

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of September 16th, 2022

Financial News Highlights

- CPI inflation surprised to the upside in August, rising 0.1% m/m. The core measure also recorded a sizeable 0.6% m/m gain, as both goods and service categories accelerated on the month.

- Financial markets have now fully priced a 75-basis point hike from the Fed next week and are anticipating the Fed funds rate reaches 4% by year-end.

- A tentative agreement between U.S. rail companies and the unions representing rail workers was reached on Thursday, avoiding what could have been another crippling blow to U.S. supply chains.

Full Steam Ahead for the FOMC

Hopes that the Federal Reserve can still engineer a soft landing were tested again this week in financial news. Consumer Price Index (CPI) data for August showed inflation was far hotter than expected, leading to a sharp repricing of market expectations on the future path of rate hikes. Following the release, market participants were quick to fully price a 75-basis point move from the Federal Reserve next week, and now expect the Fed funds rate to reach 4% by year-end. The pull forward in rate hike expectations triggered a sharp sell-off in U.S. equities, with the S&P 500 suffering its worst day of the year – falling by over 4%. Equities dipped a bit further through the remainder of the week and are down 5.5% at the time of writing.

Hopes that the Federal Reserve can still engineer a soft landing were tested again this week in financial news. Consumer Price Index (CPI) data for August showed inflation was far hotter than expected, leading to a sharp repricing of market expectations on the future path of rate hikes. Following the release, market participants were quick to fully price a 75-basis point move from the Federal Reserve next week, and now expect the Fed funds rate to reach 4% by year-end. The pull forward in rate hike expectations triggered a sharp sell-off in U.S. equities, with the S&P 500 suffering its worst day of the year – falling by over 4%. Equities dipped a bit further through the remainder of the week and are down 5.5% at the time of writing.

In terms of the actual CPI figures, headline inflation rose 0.1% month-on-month (m/m), a few ticks above the consensus forecast. More worrying, was the 0.6% m/m increase in core inflation – a sharp acceleration from July’s 0.3% m/m gain. While some persistence in price growth across service categories such as shelter and healthcare was expected, the August data showed far more breadth and strength across nearly all goods and service categories.

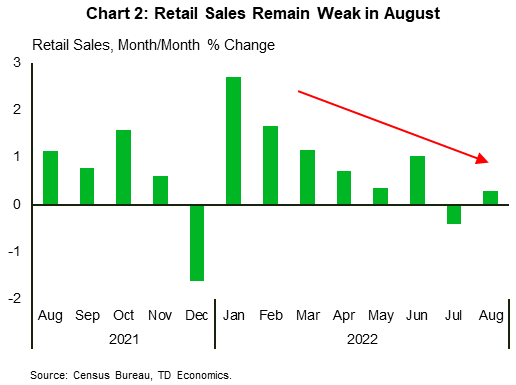

While we’re hesitant to put too much stock in one month of data, the re-acceleration in goods prices is somewhat concerning. Despite demand for consumer goods cooling more recently, goods inflation has shown considerable staying power. This was reaffirmed later in the week where August retail sales data showed only a modest gain of 0.3% m/m (Chart 1). The control group of sales was even weaker, recording a flat reading on the month.

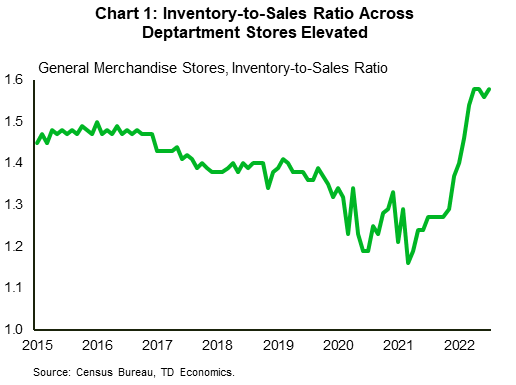

The continued gains in goods prices are even more perplexing when we consider the fact that not only is demand weakening, but inventory levels are also starting to look toppish. Inventory-to-sales ratios across department stores are now well above pre-pandemic levels – suggesting we should be seeing some disinflationary pressure (Chart 2). Other oddities are also starting to emerge across used vehicle prices. The Manheim Used Vehicle Price Index – a measure that captures dealer purchase prices – has fallen by over 10% this year, yet the CPI measure of used vehicle prices has declined by only 1.5%. This suggests that lower costs are not being passed onto consumers, and retailers are instead maintaining wider margins. Over the near-term, this is not necessarily problematic. But if left unchecked, it can start to sow the seeds of more engrained inflationary pressures. Fortunately, that hasn’t happened yet. According to data released by the New York Federal Reserve, both one-and-three-year inflation expectations have continued to move lower, with August readings falling to 5.8% (from 6.2%) and 2.8% (from 3.2%), respectively.

The continued gains in goods prices are even more perplexing when we consider the fact that not only is demand weakening, but inventory levels are also starting to look toppish. Inventory-to-sales ratios across department stores are now well above pre-pandemic levels – suggesting we should be seeing some disinflationary pressure (Chart 2). Other oddities are also starting to emerge across used vehicle prices. The Manheim Used Vehicle Price Index – a measure that captures dealer purchase prices – has fallen by over 10% this year, yet the CPI measure of used vehicle prices has declined by only 1.5%. This suggests that lower costs are not being passed onto consumers, and retailers are instead maintaining wider margins. Over the near-term, this is not necessarily problematic. But if left unchecked, it can start to sow the seeds of more engrained inflationary pressures. Fortunately, that hasn’t happened yet. According to data released by the New York Federal Reserve, both one-and-three-year inflation expectations have continued to move lower, with August readings falling to 5.8% (from 6.2%) and 2.8% (from 3.2%), respectively.

One piece of good news emerged this week, with a tentative agreement reached between U.S. rail companies and the unions representing the rail workers in further financial news. The labor deal averts what would have been another crippling blow to U.S. supply chains, and almost certainly lead to more near-term pressures on inflation. FOMC officials will likely breathe a sigh of relief, as the focus can remain squarely on what will still be a challenging task; threading the needle of lowering inflation while trying to avoid a recession.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of September 9th, 2022

Financial News Highlights

- The ISM Services index expanded at the fastest pace in four months with demand components rising and supply side challenges normalizing.

- The Fed’s Beige book pointed to a further softening in demand, while also suggesting that labor markets remained tight.

- A hot labor market is contributing to the Fed’s hard line on inflation emphasized in speeches this week. This solidified market expectations for a three-quarter hike in September.

U.S. - Fedspeak Solidifies Bets for Supersized Hike

The first post-Labor-Day week was scant on economic data, but markets had plenty of remarks from FOMC members to digest in financial news. Fed speakers’ hawkish message led Treasury yields higher, with the 2-Year yield up 12 basis points (bps) and the 10-Year yield up 10 bps on the week, at time of writing. The economic data was largely second tier sentiment surveys, which sent some conflicting signals.

The first post-Labor-Day week was scant on economic data, but markets had plenty of remarks from FOMC members to digest in financial news. Fed speakers’ hawkish message led Treasury yields higher, with the 2-Year yield up 12 basis points (bps) and the 10-Year yield up 10 bps on the week, at time of writing. The economic data was largely second tier sentiment surveys, which sent some conflicting signals.

The ISM Services index rose in August, expanding at the fastest pace in four months. The underlying measures remained on the right track. The demand components - such as business activity and new orders – reached above 60 for the first time since December and March, respectively. Meanwhile, supply-side challenges continue to normalize with employment subindex moving into the expansionary territory, supplier deliveries times returning to their pre-pandemic average, and prices paid component easing.

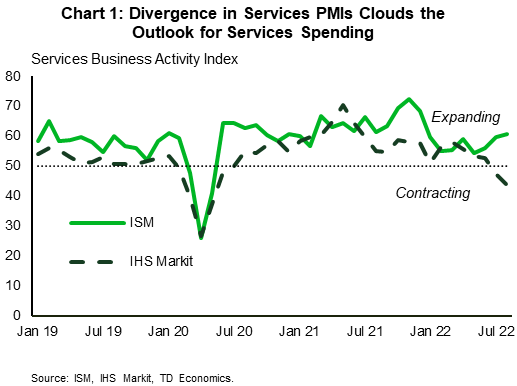

Yet, the reading came as a surprise as consensus was pricing a moderation, and the other services flash indicator – the IHS Markit PMI – contracted in August. Demand components were especially contrasting, as the ISM index suggested strengthening while the IHS Markit pointed to a looming demand destruction (Chart 1). The differences in methodology explain the divergence in the signals: the ISM index includes a broader range of industries (including construction and mining) and reflects business conditions of its members who tend to be larger and more established companies. The IHS measure therefore better reflects the sentiment of small- and medium-sized enterprises, but we find that the ISM index has stronger historical correlations with services spending.

While this divergence clouds the outlook, we expect the truth to lie somewhere in the middle, with current economic activity remaining unchanged. This sentiment was echoed in the Fed’s Beige book that gathers anecdotal information on current economic conditions through July and August across Federal Reserve Bank districts. The report characterizes consumer spending as “steady” and points to expectations for further softening of demand over the next six to twelve months in further financial news. On the other hand, respondents indicated that labor market conditions remained tight, but also pointed to a slower pace of wage increases and moderating salary expectations.

While this divergence clouds the outlook, we expect the truth to lie somewhere in the middle, with current economic activity remaining unchanged. This sentiment was echoed in the Fed’s Beige book that gathers anecdotal information on current economic conditions through July and August across Federal Reserve Bank districts. The report characterizes consumer spending as “steady” and points to expectations for further softening of demand over the next six to twelve months in further financial news. On the other hand, respondents indicated that labor market conditions remained tight, but also pointed to a slower pace of wage increases and moderating salary expectations.

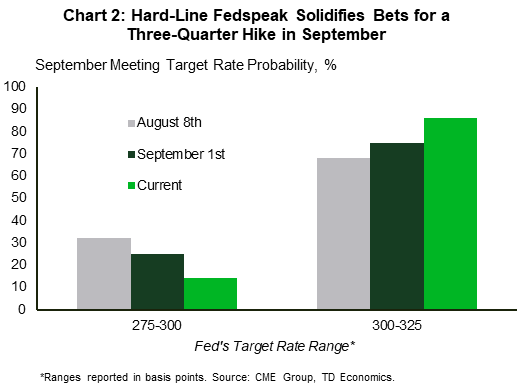

The tightness of labor market is a big part of why the Fed takes a hardline inflation fighting stance. FOMC speakers took every opportunity to reinforce their unanimity on this front ahead of the central bank’s black-out period prior to its September 21st rate decision. Chair Powell was very explicit by stating that the Committee wants to soften growth enough to “cause the labor market to get back into better balance, and then that will bring wages back down to levels that are more consistent with 2% inflation over time.” Investors heard it loud and clear with the federal funds futures markets now have greater conviction that the Fed will hike 75 basis to 3.25% (Chart 2). Moreover, the market appears less convinced that there will be rate cuts next year, buying into the Vice Chair Brainard’s “we are in this for as long as it takes to get inflation down” mantra.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of September 2nd, 2022

Financial News Highlights

- A strong week for economic data as the ISM manufacturing index and the payrolls report surprised to the upside.

- The details of both reports showed improvements on the supply-side of the economy as falling manufacturer input prices and a strong improvement in the labor force shined through.

- The Fed still has its hands full taming inflation, but supply-side improvements could make the job much easier.

U.S. -

Good News on Aggregate Supply

Markets continued to sell off this week as better than expected data dimmed the hopes of a 50-basis point hike by the Fed at its upcoming September meeting in financial news. However, there were some reassuring signals in the ISM manufacturing report and the household employment survey that the supply-side of the economy continues to improve and may help moderate inflation. The Fed will continue its hiking cycle, but the supply-side improvements might just make the job of taming inflation a bit easier.

Markets continued to sell off this week as better than expected data dimmed the hopes of a 50-basis point hike by the Fed at its upcoming September meeting in financial news. However, there were some reassuring signals in the ISM manufacturing report and the household employment survey that the supply-side of the economy continues to improve and may help moderate inflation. The Fed will continue its hiking cycle, but the supply-side improvements might just make the job of taming inflation a bit easier.

Tuesday’s solid job openings data from the JOLTS survey grabbed headlines. Private openings in July were north of 10 million. Though sky high job openings have become the norm, they are remarkable relative to history and represent the scale of the problem the Fed is looking to solve. To tame inflation, officials are hoping to lower the rate of job openings, without meaningfully raising the unemployment rate. There is little historical precedent for this, but there is also little modern historical precedent for what has transpired in the economy over the past two years. Nonetheless, with job openings still high, the labor market is signaling that employment demand remained robust in July despite rising interest rates.

The good economic news continued yesterday as the ISM manufacturing index surprised to the upside in August, registering a healthy 52.8 print. Growth and production were notably slower than earlier in the recovery, but this was to be expected as the economy continues to operate in excess demand territory. The details in the report were also strong. New orders flipped back to growth and employment was up for the month. For the Fed, there was good news on supply chains as the supplier delivery index was unchanged and input price growth eased to its lowest rate since the summer of 2020 [Chart 1].

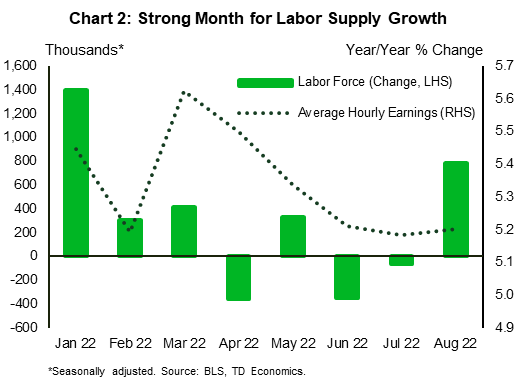

All of this was a buildup to today’s employment report. Consensus expectations were for nearly 300k new jobs, a print that would register as “good” during any expansion, let alone one that has featured so little bounce-back in the participation rate. Well, the data came in slightly better than expected, with payrolls adding 312k jobs, but it was the household report that had some positive elements. August showed that there was finally a large movement of people back into the labor force, 786k to be exact [Chart 2]. This helped lift the participation rate 0.3 percentage points, to 62.4% and brought some much-needed supply to the labor market. As the labor force expanded faster than employment, the unemployment rate rose to 3.7%. With just a bit more labor supply, average weekly wages moderated to 0.3% month-on-month, from 0.5% the month prior.

All of this was a buildup to today’s employment report. Consensus expectations were for nearly 300k new jobs, a print that would register as “good” during any expansion, let alone one that has featured so little bounce-back in the participation rate. Well, the data came in slightly better than expected, with payrolls adding 312k jobs, but it was the household report that had some positive elements. August showed that there was finally a large movement of people back into the labor force, 786k to be exact [Chart 2]. This helped lift the participation rate 0.3 percentage points, to 62.4% and brought some much-needed supply to the labor market. As the labor force expanded faster than employment, the unemployment rate rose to 3.7%. With just a bit more labor supply, average weekly wages moderated to 0.3% month-on-month, from 0.5% the month prior.

The Fed will see this report as good news. The drum-tight labor market is a key factor in setting wage expectations, and with more workers coming in off the sidelines, it means just a bit less wage pressure in further financial news. That said, labor markets remain tight as wage growth is still at 5.2% year-on-year, and inflation is still persistently high. The Fed will continue to raise rates to fight inflation, but this week’s data suggest that some of the supply-side factors behind current price growth are finally starting to abate.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of August 26th, 2022

Financial News Highlights

- Fed Chair Jay Powell’s hawkish remarks at the annual Jackson Hole conference did not sit well with equity markets.

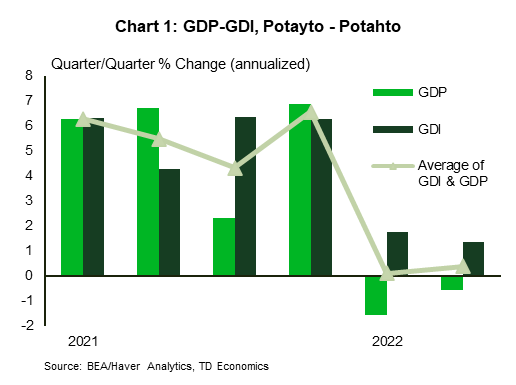

- The second estimate of Q2 GDP data showed that the economy contracted slightly less, and that GDI grew modestly. looking at an average of the two measures shows that the U.S. economy grew only slightly in the first half of the year.

- President Biden announced details on a much-anticipated student debt forgiveness plan that will forgive up to $20,000 in federal student debt per borrower.

- A reduction in student debt will be stimulative for people receiving the relief, and could add more fire to current inflationary pressures, making the Fed’s job that much more difficult.

U.S. - Powell Stands Firm on Higher Rates

It was a full week for economic data, but the most anticipated event for markets was the Fed Chair’s speech at the annual Jackson Hole conference on Friday in financial news. Equity markets didn’t like what they heard. Powell’s hawkish remarks that the Fed remains committed to fight inflation and is likely to keep rates high for an extended period did not sit well with investors, and stocks fell on the remarks. The yield on the 2-Year Treasury was up slightly after the speech, continuing a recent trend as markets expect a bit more monetary tightening over the next two years.

It was a full week for economic data, but the most anticipated event for markets was the Fed Chair’s speech at the annual Jackson Hole conference on Friday in financial news. Equity markets didn’t like what they heard. Powell’s hawkish remarks that the Fed remains committed to fight inflation and is likely to keep rates high for an extended period did not sit well with investors, and stocks fell on the remarks. The yield on the 2-Year Treasury was up slightly after the speech, continuing a recent trend as markets expect a bit more monetary tightening over the next two years.

Longer-term bond yields remain lower than the 2-Year as markets expect an economic slowing and future rate cuts by the Fed. It is understandable that investors are worried about a recession, when the second estimate for GDP growth in Q2, was revised up only slightly and still contracted by 0.6% annualized. This release was more highly anticipated than usual because it included another measure of national output – Gross Domestic Income (GDI). GDI measures output based on income in the economy – summing wages, profits, interest payments and investments. Whereas GDP is defined as the value of final goods and services on the production side. In theory they should be similar, but there usually is some deviation due to being measured from different data sources.

Some economists argue that GDI is the better measure – but it is released later by the BEA, and so usually gets less attention. Early estimates of GDI better captured the downturn in the 2007-09 recession. The compromise is that an average between the two measures likely captures momentum in the economy best. In the first half of 2022, GDP estimates suggested the economy contracted, while GDI showed the economy grew at 1.6% on average through Q1-Q2 (Chart 1). The average of the two measures shows the economy stalled in the first half of the year, so to some extent it feels like a potayto-potahto situation – either way you slice it, the U.S. economy is on a dramatically slower growth trajectory in 2022 in the face of high inflation, rising interest rates and less fiscal stimulus.

As for momentum in the second half of the year, consumer spending data for July showed that nominal spending continued to lose momentum. But, due to weaker inflation pressures, the real spending slowdown is somewhat less than we expected a few weeks ago. Real consumer spending is tracking around 1.5-2% annualized in the third quarter, which is roughly the same pace averaged over the first half of the year in financial news. This suggests the consumer is proving quite resilient to all the onslaughts against their purchasing power.

As for momentum in the second half of the year, consumer spending data for July showed that nominal spending continued to lose momentum. But, due to weaker inflation pressures, the real spending slowdown is somewhat less than we expected a few weeks ago. Real consumer spending is tracking around 1.5-2% annualized in the third quarter, which is roughly the same pace averaged over the first half of the year in financial news. This suggests the consumer is proving quite resilient to all the onslaughts against their purchasing power.

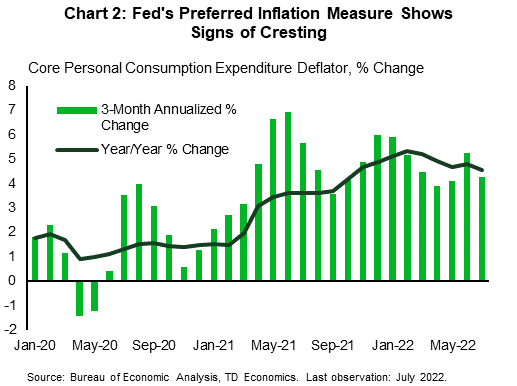

Inflation, as measured by the core PCE deflator, also cooled a bit in July. Looking at it on a year-on-year basis, core inflation has cooled to 4.6%, and ran at a 4.3% annualized pace over the past three months (Chart 2). We aren’t saying that inflation pressures have been vanquished, but it is encouraging they are moving in the right direction. Given the false dawn we had last year, where inflation pressures originally cooled, only to quickly heat up again, Chair Powell is right to point out that the Fed needs to see more convincing evidence before easing up on rate hikes.

Leslie Preston, Senior Economist | 416-983-7053

U.S. Students Get Up to $20,000 in Student Debt Erased

President Biden announced a much-anticipated executive action to reduce the burden of federal student debt in financial news. At the time of writing, the White House hasn't provided cost estimates, or all the details, but according to the Committee for a Responsible Federal Budget, the plan will cost roughly $500 billion dollars over the next 10 years.

President Biden announced a much-anticipated executive action to reduce the burden of federal student debt in financial news. At the time of writing, the White House hasn't provided cost estimates, or all the details, but according to the Committee for a Responsible Federal Budget, the plan will cost roughly $500 billion dollars over the next 10 years.

Under the plan, $10,000 in federal student loan debt will be forgiven for borrowers making under $125,000 (or $250,000 for couples). Approximately 40 million borrowers would be eligible for this amount. In addition, up to $20,000 will be forgiven for the 27 million recipients of Pell Grants – a specific program for students in financial need. It's estimated that more than a third of the total $1.6 trillion in student debt will be forgiven.

The plan also modifies existing income-driven repayments by reducing future monthly payments for lower-and middle-income borrowers. Payments will be reduced from 10% to 5% percent of discretionary income, and forgives loan balances of $12,000 or less after 10 years.

Furthermore, borrowers who are employed by non-profits, the military, or government may be eligible to have all their student loans forgiven through the Public Service Loan Forgiveness program. The pandemic moratorium on federal student loan payments will also be extended through December 31st, saving roughly $20 billion in debt payments.

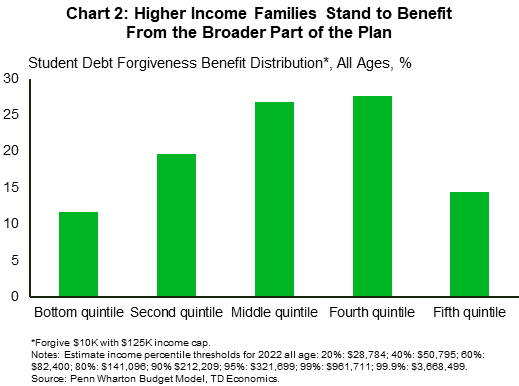

The announcement puts an end to a debate that has been around since at least the Occupy Wall Street protests a decade ago. The proponents of forgiveness argue it would stop the racial wealth gap from growing and help borrowers turn regular earnings into longer-lasting wealth. Indeed, African American college graduates hold disproportionally large student debt balances in comparison to peers (Chart 1). Those against forgiveness point out that student debt is disproportionately held by more affluent families, and that it will stimulate economic activity at the time when inflation is already running hot.

The debate is hot but ultimately the additional forgiveness of $20,000 for Pell grant recipients and modifications to income-driven repayment programs makes the plan more targeted towards lower-income Americans, helping the administration achieve progressive goals. According to White House's estimates, 87% of the relief will go to lower-income families earning less than $75,000. However, some portion of higher income families stand to benefit, given that the income threshold set at $125,000 is well above the median American income (Chart 2).

In terms of the economic impact, a reduction in student debt will be mildly stimulative, though the average borrower can expect to have their annual payment reduced by $1,000. While there’s still uncertainty over both the timing and implementation of the program, preliminary estimates suggest that the impact to economic growth will be relatively small compared to its cost – with only a tenth of the dollar amount forgiven expected to flow back into the economy. Still, more economic stimulus at time when inflation is already running at multidecade highs will make the Fed’s job that much harder to regain price stability over the coming years.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of August 19th, 2022

Financial News Highlights

- Total retail sales were flat in July, marking a deceleration from June’s pace. However, sales in the control group, which exclude several volatile categories and are used in calculating GDP, rose a sturdy 0.8% m/m.

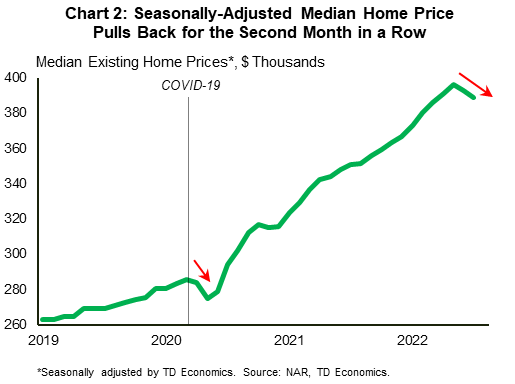

- Housing continued to cool in July. Existing home sales fell 5.9% and the median seasonally adjusted home price retreated for the second month in a row. Homebuilders also continued to ease off the accelerator, with starts down 9.6% in July.

- Minutes from last month’s FOMC meeting revealed that many participants acknowledged the risks that that the Committee could tighten the stance of policy by “more than necessary”.

How Quickly to Raise Rates? That Is the Question

The third week of August was a busy data week for the U.S., with updates on housing and the consumer for July in financial news. The consumer spent a little more than expected at retailers (omitting auto dealers and gas stations), thanks to a successful Amazon Prime Day event, but housing is continuing to recalibrate to the higher rate environment.

The third week of August was a busy data week for the U.S., with updates on housing and the consumer for July in financial news. The consumer spent a little more than expected at retailers (omitting auto dealers and gas stations), thanks to a successful Amazon Prime Day event, but housing is continuing to recalibrate to the higher rate environment.

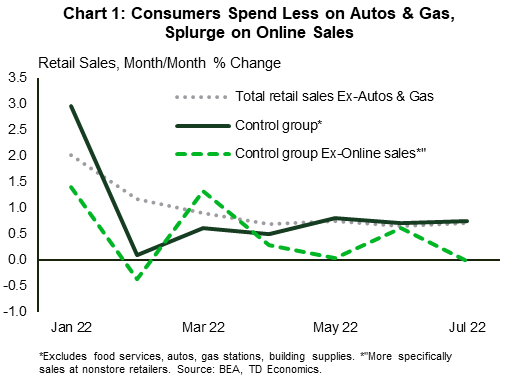

Headline retail sales were flat in July, marking a deceleration from June’s 0.8% month-over-month (m/m) gain. However, the headline measure was dragged down by sales auto & part dealers (-1.6%) and gasoline stations (-1.8%), the latter reflecting lower prices at the pump. Retail sales in all other categories rose a sturdy 0.7% m/m. Similarly, sales in the control group, which strip a couple of more categories from the total and are used in calculating personal consumption expenditures and GDP, were up 0.8% m/m thanks to a boost from sales at non-store retailers (Chart 1). Total CPI inflation was flat in July, so by these measures, real goods consumer spending appears to have had a decent start to the third quarter.

Consumers also spent handsomely at building material and supply dealers last month (+1.5% m/m), a move that went against the grain of the ongoing weakening in housing. Existing home sales fell by almost 6% in July, extending their downward slide from the start of the year to a staggering 26%. Home prices have also been feeling the impact of higher rates, with the median seasonally adjusted home price falling in each of the last two months (Chart 2). The fact that mortgage rates have eased a bit over the past several weeks could provide an opportunity for the housing rout to take a breather. However, the Fed is not done hiking rates, so affordability is likely to remain a meaningful constraint for the foreseeable future. As a result, we expect home sales to continue trending moderately lower through the first half of next year.

Consumers also spent handsomely at building material and supply dealers last month (+1.5% m/m), a move that went against the grain of the ongoing weakening in housing. Existing home sales fell by almost 6% in July, extending their downward slide from the start of the year to a staggering 26%. Home prices have also been feeling the impact of higher rates, with the median seasonally adjusted home price falling in each of the last two months (Chart 2). The fact that mortgage rates have eased a bit over the past several weeks could provide an opportunity for the housing rout to take a breather. However, the Fed is not done hiking rates, so affordability is likely to remain a meaningful constraint for the foreseeable future. As a result, we expect home sales to continue trending moderately lower through the first half of next year.

Homebuilders have continued to ease off the accelerator amidst this challenging market backdrop, with starts falling 9.6% in July. The weakness in homebuilding over the last several months has been concentrated in the single-family market. A recent sharp decline in homebuilder confidence in this sector suggests that the trend is poised to continue.

The fallout from the downturn in the housing market is only one factor the Fed must consider as it gears up to raise rates again next month in further financial news. Minutes from last month’s FOMC meeting revealed that many members acknowledged the risks that the Committee could tighten the stance of policy by “more than necessary”. In addition, participants judged that as the policy rate is tightened further “it would become appropriate at some point to slow the pace of policy rate increases” to assess the impacts. Markets interpreted this as a signal that the pace of rate hikes would slow soon, but a few Fed officials (i.e., Bullard, voting member, backs a 75-basis point (bp) hike next) appeared to push back against that notion. For now, markets are pricing in a 50-bp hike at the next meeting. Chair Powell’s Jackson Hole speech next Friday will be closely watched to gauge the Fed’s latest thinking as to where rate hikes are headed.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of August 12th, 2022

Financial News Highlights

-

- The U.S. Senate passed a climate, healthcare, and tax bill known as the Inflation Reduction Act of 2022 earlier this week. The legislation is now off to the House of Representatives for a final vote later today where it is expected to pass.

- July CPI came in weaker than expected, with the headline measure flat on the month and core “only” increasing by 0.3% month-over-month.

- While the deceleration in inflation comes as welcome news to policymakers, Fed officials have reiterated that more tightening will be required to achieve price growth stability of 2%.

U.S.-Inflation Was the Word of the Week

It was a week full of surprises, with inflation being the key theme in financial news. Chief among them was the U.S. Senate quickly moving to pass the Inflation Reduction Act of 2022 (IRA). It now heads to the House of Representatives later today for a final vote, where it’s expected to pass. The reconciliation bill is a significantly scaled back version of the far more ambitious Build Back Better Act, though it still incorporates many of the key climate related initiatives that were included in the previous bill.

In terms of broad strokes, the IRA aims to spend roughly $430B on climate and healthcare initiatives over the next decade and is estimated to more than offset those expenditures with $740B of proposed revenue. Over 85% of the appropriated expenditures will be directed towards climate related initiatives and will be dispersed mainly through grants and loans. Of those investments, perhaps most noteworthy is the $80B in new rebates allocated to eligible households for electric vehicles (EVs) and to help decarbonize residential buildings. The additional funding for EVs not only maintains the existing $7,500 rebate but also introduces a new tax credit of up $4,000 for both used and new EVs, with the latter applying only to those vehicles made in North America.

On the healthcare side, the IRA will put a cap of $2,000 on out-of-pocket prescription drug costs for individuals on Medicare. It also aims to bring down the cost of the most expensive drugs by allowing the government to negotiate the price of a subset of those drugs covered by Medicare, though this won’t start until 2026.

All of this will be paid for through a new 15% minimum corporate tax imposed on corporations earning more than $1B, enhancements to the IRS audit and review process, and taxing share buybacks. The fact that the deficit will be reduced over the next decade is what is being used to justify the “inflation reduction” element of the bill. However, the total deficit reduction is only estimated to be $400B (or 1.6% of GDP), and will be spread over the next decade – suggesting the impact to growth and inflation will likely be negligible.

All of this will be paid for through a new 15% minimum corporate tax imposed on corporations earning more than $1B, enhancements to the IRS audit and review process, and taxing share buybacks. The fact that the deficit will be reduced over the next decade is what is being used to justify the “inflation reduction” element of the bill. However, the total deficit reduction is only estimated to be $400B (or 1.6% of GDP), and will be spread over the next decade – suggesting the impact to growth and inflation will likely be negligible.

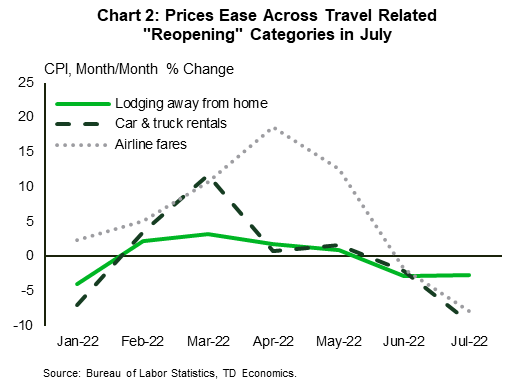

Turing to the other surprise this week, July CPI data (finally!) came in weaker than expected. The headline index was flat on the month, while core prices “only” rose by 0.3% m/m (Chart 1). Indeed, the recent pullback in energy prices subtracted from the headline measure, though accelerating food prices provided a partial offset in further financial news. Looking to the core measure, there were a few encouraging tidbits. Core services grew by 0.4% m/m – down from the 0.7% m/m reported in June. A lot of the pullback was the result of a softening in travel-related categories, such as airfares, car rentals, and lodging away from home (Chart 2). Other green shoots emerged on the goods side, as prices across most categories decelerated, while used vehicle prices, apparel, and education goods all declined.

This will be welcome news to FOMC officials, but as San Francisco Fed president Mary Daly said on Wednesday “it’s still too early to declare victory”. Daly reiterated her support to dial back on the pace of rate hikes in September but didn’t rule out another 75bps move should the turn in inflation prove to be fleeting.

Thomas Feltmate, Director | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of August 5th, 2022

Financial News Highlights

-

- The U.S. economy added a whopping 528k jobs in July, pushing employment above its pre-pandemic level. The unemployment rate also ticked lower, falling back to its pre-pandemic historical low of 3.5%.

- Sentiment indicators also surprised to the upside, with the manufacturing sector faring better than expected and the services sector pointing to plenty of pent-up demand.

- Data out this week support the narrative that the U.S. economy is not currently in a recession, and more monetary tightening will be required from the FOMC to slow inflation and restore balance in the labor market.

U.S. More Fuel to the Recession Debate

This week in financial news, the debate on whether the Fed will be able to achieve a soft landing intensified. Equities were trading up most of the week as investors bought into the positive economic news with an expectation that a slowdown in economic growth will avoid a severe downturn. In contrast, the bond market took a grimmer view of the future, by pushing the 10Y2Y yield inversion deeper into negative territory, suggesting a recession may be looming on the horizon.

This week in financial news, the debate on whether the Fed will be able to achieve a soft landing intensified. Equities were trading up most of the week as investors bought into the positive economic news with an expectation that a slowdown in economic growth will avoid a severe downturn. In contrast, the bond market took a grimmer view of the future, by pushing the 10Y2Y yield inversion deeper into negative territory, suggesting a recession may be looming on the horizon.

Investors weren’t the only ones arguing about the economic prospects. In academic circles, the debate on whether a soft landing can be achieved was out in the open. At its core is the argument that job vacancies can’t decline by a large amount without the economy falling into recession. This week’s release of June’s Job Openings and Labor Turnover Survey (JOLTS) showed that job openings dipped to 10.7 million while job vacancy rate continued to decline, indicating we have likely already surpassed peak tightness in the labor market. Still, demand for workers continued to outpace supply - a sign of a still strong labor market.

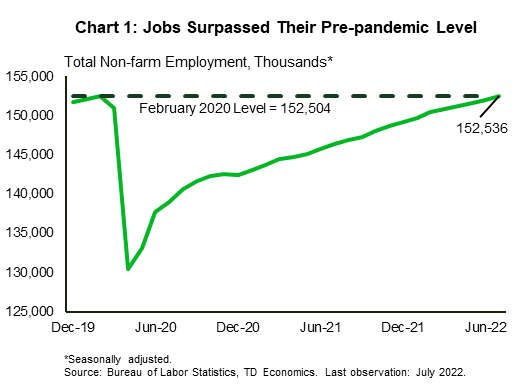

Indeed, anyone in search of more signs that the economy is in fact not in a recession need to look no further than today’s jobs report. July data shows that the economy added a whopping 528k jobs (well above the consensus forecast of 250k), while revisions resulted in additional 28k jobs – enough for the payroll figures to surpass their pre-pandemic level (Chart 1). The unemployment rate declined by a tenth of a percentage point to 3.5%, while the labor force participation rate fell slightly to 62.1%. Furthermore, average hourly earnings accelerated – not quite what the Fed was looking for as this increases the possibility of inflation becoming entrenched.

Meanwhile, sentiment indicators also surprised to the upside in financial news. The Institute for Supply Managements’ (ISM) readings for the manufacturing sector slipped modestly but came in above expectation. Demand is clearly slowing with new orders contracting for the second month in a row. Still, this comes with less pressure on suppliers, as supplier delivery times rose at their slowest pace since before the pandemic. Moreover, the inventories subindex continues to show improvement. This corresponds with rising auto inventories, where increased production helped improve market supply to roughly 28 days from February’s low of just 24 days.

Meanwhile, sentiment indicators also surprised to the upside in financial news. The Institute for Supply Managements’ (ISM) readings for the manufacturing sector slipped modestly but came in above expectation. Demand is clearly slowing with new orders contracting for the second month in a row. Still, this comes with less pressure on suppliers, as supplier delivery times rose at their slowest pace since before the pandemic. Moreover, the inventories subindex continues to show improvement. This corresponds with rising auto inventories, where increased production helped improve market supply to roughly 28 days from February’s low of just 24 days.

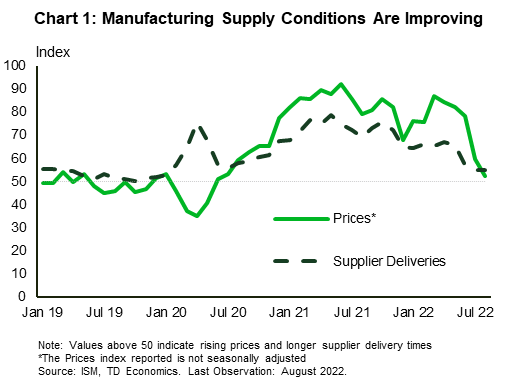

The ISM services index pointed to a broad pickup in services activity, proving again that there is still plenty of pent-up demand. The gap between the supplier deliveries time and the rest of the index’s drivers narrowed in July – a month after a similar improvement in the manufacturing sector. This seems to have contributed to a decline in the prices paid component in both sectors of the economy (Chart 2). The sizeable deceleration in the ISM price subindexes may very well be a harbinger of a slowing pace in broader price growth, which we’ll hopefully see in next week’s CPI report.

Still, at the 40-year high price growth is too overwhelming for the Fed to scale back on rate hikes. For now, robust employment growth adds further conviction that the economy remains on a solid footing and suggests the FOMC needs to remain aggressive in tightening rates to help cool inflation and re-anchor inflation expectations.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.