Financial News for the Week of March 3rd, 2023

Financial News Highlights

- Pending home sales rose 8.1% in January, however with mortgage rates now back up around 7% this is unlikely to be sustained moving forward.

- The ISM Manufacturing Index improved for the first time in six months but continued to indicate contraction in the sector.

- Fed speakers this week noted the upside risk to the policy rate path posed by recent economic data, pushing the 10-year Treasury yield above 4%.

Higher Rates Abound

Congratulations on successfully making it to the third month of 2023. We are now just two and a half weeks away from economists’ most anticipated day of 2023. No, not the first day of Spring, the next FOMC rate announcement on March 22nd. This week we got a peek into six different FOMC members thinking on the expected path of policy and got pulse checks on the housing, manufacturing, and service sectors. In financial markets, Treasury yields continued their upward march, with the ten-year Treasury yield rising above 4% while the S&P 500 has clawed back earlier losses and is up 1% on the week as of the time of writing.

Congratulations on successfully making it to the third month of 2023. We are now just two and a half weeks away from economists’ most anticipated day of 2023. No, not the first day of Spring, the next FOMC rate announcement on March 22nd. This week we got a peek into six different FOMC members thinking on the expected path of policy and got pulse checks on the housing, manufacturing, and service sectors. In financial markets, Treasury yields continued their upward march, with the ten-year Treasury yield rising above 4% while the S&P 500 has clawed back earlier losses and is up 1% on the week as of the time of writing.

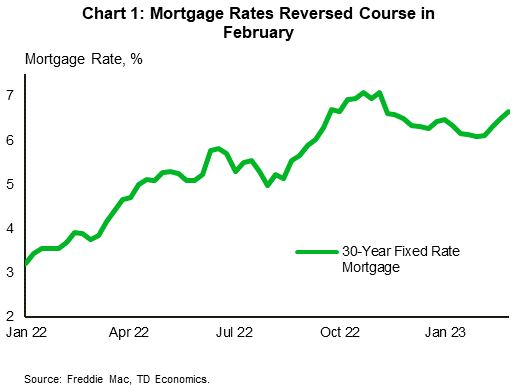

Pending home sales in January increased for the second consecutive month, rising by 8.1% month-on-month (m/m). Falling mortgage rates in late 2022 helped slow the year-long decline in sales activity, despite prices continuing to sink through the end of the year. Seasonally adjusted national home prices, as measured by the S&P CoreLogic Case-Shiller index, continued to decline in December (-0.3% m/m), matching the decline seen in November. With the 30-year mortgage rate rising to 7% in February this reprieve is likely to prove temporary (Chart 1).

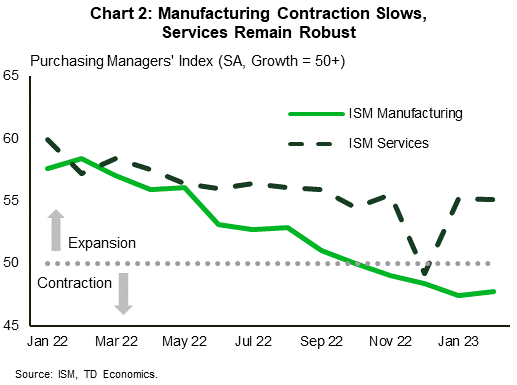

On Wednesday, the ISM Manufacturing Index improved for the first time since August, though the sector remained in contractionary territory for the fourth consecutive month (Chart 2). New orders and backlogged orders continued to contract, albeit at a slower pace. In contrast, the ISM Services Index reading on Friday showed that the industry is still expanding, with new orders growing at a faster pace.

Supplier delivery times continued to see improvement in both sectors with ocean freight costs declining for a sixth consecutive month. However, the manufacturing prices paid subindex increased for the first time since September, reflecting higher raw material prices. Although the subindex remained below the historical level associated with an uptick in the Producer’s Price Index, Treasury yields rose in response to the possible implications this could have on inflation and the Federal Reserve’s policy path.

Supplier delivery times continued to see improvement in both sectors with ocean freight costs declining for a sixth consecutive month. However, the manufacturing prices paid subindex increased for the first time since September, reflecting higher raw material prices. Although the subindex remained below the historical level associated with an uptick in the Producer’s Price Index, Treasury yields rose in response to the possible implications this could have on inflation and the Federal Reserve’s policy path.

Speaking of the Fed, we heard from seven different Federal Reserve officials this week, six of whom are current voting FOMC members. Their talking points covered a range of topics, from Governor Jefferson pushing back against calls for the Fed to raise its inflation target to Chicago Fed President Goolsbee saying it would be a mistake for the Fed to rely too heavily on financial market reactions. We also received policy specific comments, with Minneapolis Fed President Kashkari noting that he is open to a 50 basis point hike at the next meeting and Atlanta Fed President Bostic (a 2024 FOMC member) saying in an essay that he sees the policy rate going to 5.00 - 5.25% and staying there well into 2024.

Members made it clear that they are not yet convinced of the downward trajectory in inflation and upside risks to the policy rate path remain. All eyes will be on next week’s February employment data, which will show whether January’s blowout job growth was just a blip or something more concerning altogether for the Fed.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of February 24th, 2023

Financial News Highlights

- A second read on fourth-quarter GDP showed that the U.S. economy grew by 2.7% (q/q annualized) instead of 2.9%

as reported previously. A measure of underlying domestic demand was revised down from 0.2% to an even softer 0.1%. - Real consumer spending rose a solid 1.1% month-on-month (m/m) in January. Core PCE inflation came in hotter than

anticipated, rising to 4.7% year-on-year in January from an upwardly revised 4.6% in December. - Despite hopes for an improvement to the housing narrative at the start of 2023, existing home sales fell 0.7% (m/m) in

January, extending their losing streak to 12 consecutive months.

Sticky Inflation Means Higher Rates

Not all economic data was positive this week, but a strong rebound in consumption and evidence of sticky inflation continued to build the case that the Fed will take the policy rate higher in financial news. Rising Treasury yields took a toll on equity markets, with the S&P 500 down 3.3% from last week’s close (at time of writing).

Not all economic data was positive this week, but a strong rebound in consumption and evidence of sticky inflation continued to build the case that the Fed will take the policy rate higher in financial news. Rising Treasury yields took a toll on equity markets, with the S&P 500 down 3.3% from last week’s close (at time of writing).

A second reading on fourth-quarter GDP showed that the U.S. economy ended 2022 on softer footing than previously reported. The headline measure was revised down from 2.9% quarter-on-quarter (q/q) annualized to 2.7%. Net exports and inventory investment, two inherently volatile components, continued to make up the bulk of gain, while final sales to private domestic purchasers – a measure of underlying domestic demand – was downgraded from 0.2% to an even softer 0.1%. This as consumer spending was shaved down noticeably from 2.1% to 1.4%.

However, January’s personal income and outlays report showed that consumer spending rebounded strongly to start the year. Real consumer spending rose 1.1% month-on-month (m/m) in January, reflecting gains in both goods and services. Following in the footsteps of a strong retail sales report, real goods spending rose a sharp 2.2% (m/m), while services spending rose 0.6%. Overall, this is a very good start to first-quarter consumption, which we anticipate will expand in the 1.5-2.0% (q/q annualized) range in financial news. A tight labor market, which is helping support healthy growth in wages and salaries, will also help in this regard.

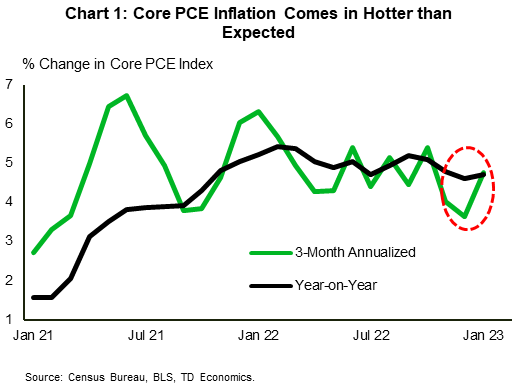

The above report also provided an update on inflation. Total PCE inflation accelerated to 5.4% year-on-year (y/y) from 5.0% in December. The Fed’s preferred inflation gauge, core PCE, accelerated modestly, rising to 4.7% y/y from an upwardly revised 4.6% in December. The key point to highlight here is that core PCE inflation looks to have picked up some steam recently (Chart 1).

The fact that inflation is showing signs of stickiness and that the labor market remains hot, raises the odds that the Fed will need to take the policy rate higher and perhaps keep it there for longer. Minutes from the latest FOMC meeting, which showed members’ resolve to keep fighting inflation through additional rate hikes based on incoming data, helps further cement this view. Marked odds still favor a rate hike of 25 basis points (bps) at the March meeting, but odds for a 50-bps hike crept higher following the PCE report and are hovering around 33% as of writing.

The fact that inflation is showing signs of stickiness and that the labor market remains hot, raises the odds that the Fed will need to take the policy rate higher and perhaps keep it there for longer. Minutes from the latest FOMC meeting, which showed members’ resolve to keep fighting inflation through additional rate hikes based on incoming data, helps further cement this view. Marked odds still favor a rate hike of 25 basis points (bps) at the March meeting, but odds for a 50-bps hike crept higher following the PCE report and are hovering around 33% as of writing.

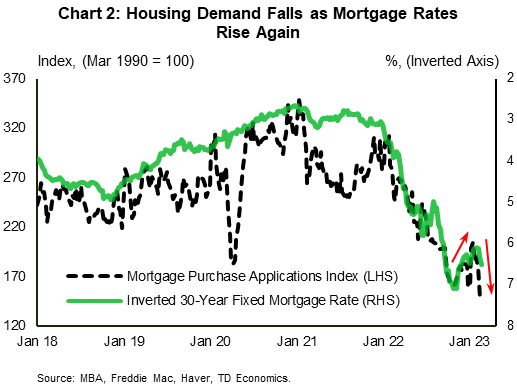

Among other things, a “higher for longer” policy rate, means that there could be additional fallout for interest-sensitive areas of the economy. On this front, existing home sales fell again in January (-0.7% m/m), extending the losing streak to 12 consecutive months. Since interest rate changes tend to influence sales activity with a lag, past declines in mortgage rates could drive some improvement in sales over the near-term. But given that mortgage rates turned higher again, housing activity will continue to be tested. High frequency data second this view, with mortgage purchase applications falling to a 28-year low last week (Chart 2). Indeed, it appears that the start of a new and improving trend in housing is still some time away.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of February 17th, 2023

Financial News Highlights

- The week’s data reminded markets that inflation is far away from the Fed’s target. Both headline and core CPI came in on par with expectations, but details suggest that disinflationary forces are softening.

- Retail sales rebounded from the year-end weakness. The biggest gains were picked up by auto dealers, but other categories were strong beyond expectations.

- More evidence of economic resilience means the Fed may need to fight harder to keep inflation under control. The probability of a 50-basis point hike in March rose from 9% to 21% on the week.

Higher for Longer

“Resilient” is the epithet that describes this week’s economic data the best in financial news. Retail sales came in a full percentage point stronger than expected, while inflation figures point to a slower descent than expected. The reaction of the equity market was mixed: stock prices dipped after the initial releases but then bounced back, losing less than 1% on the week. Bond markets, on the other hand, continued to price in higher rates, with 2-year and 10-year yields rising by 18 and 22 basis points on the week (at the time of writing).

“Resilient” is the epithet that describes this week’s economic data the best in financial news. Retail sales came in a full percentage point stronger than expected, while inflation figures point to a slower descent than expected. The reaction of the equity market was mixed: stock prices dipped after the initial releases but then bounced back, losing less than 1% on the week. Bond markets, on the other hand, continued to price in higher rates, with 2-year and 10-year yields rising by 18 and 22 basis points on the week (at the time of writing).

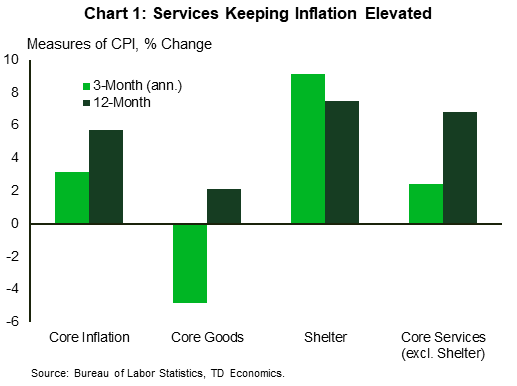

The source of this divergence is interpretation. The Consumer Prices Index (CPI) came in on par with expectations for both the headline and core (ex. food & energy) measures, which gained 0.4% and 0.5% on the month, respectively. Relative to last year, the pace of growth slowed to 6.4% for headline CPI and to 5.6% for core CPI in financial news. However, there were few convincing signs of weakness in core services inflation, even when excluding the shelter component – the most important metric for the monetary policy outlook, according to Chair Powell (Chart 1). This is at the time when the disinflationary contribution from core goods inflation appears to have taken a break, especially if the car prices turn higher next month (as signaled by the Manheim price index for used vehicles).

More inflationary pressure was also reported in the Producer Price Index (PPI), which surprised to the upside in January. The headline measure rose 0.7% month-on-month (m/m), while core inflation gained 0.5% m/m. A change in the PPI doesn’t always result in parallel changes in the CPI, but its volatile dynamic proves that the path to disinflation is not a straight line.

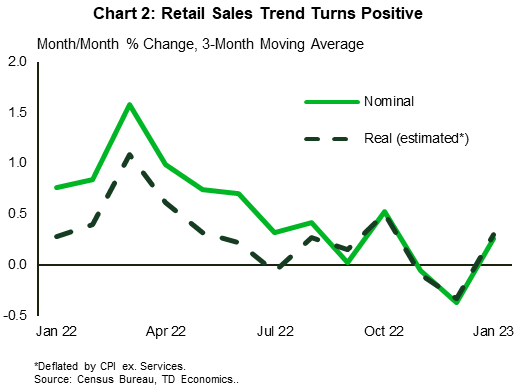

In the context this week’s retail sales report, however, persistent inflation seems less surprising. A warmer January helped heat up consumers’ aptitude to spend. The biggest gains were picked up by auto dealers, primed by the remaining pent-up demand and improved supply as production continues to recover. Predictably, nicer weather made dining out more pleasant, making restaurants the second largest contributor to growth last month. But other categories (department stores, e-commerce, and furniture & electronics stores to name a few) were also robust beyond expectations. This suggests that demand remains resilient: our estimate of real sales was up 2.8% on the month, turning the three-months trend positive (Chart 2).

In the context this week’s retail sales report, however, persistent inflation seems less surprising. A warmer January helped heat up consumers’ aptitude to spend. The biggest gains were picked up by auto dealers, primed by the remaining pent-up demand and improved supply as production continues to recover. Predictably, nicer weather made dining out more pleasant, making restaurants the second largest contributor to growth last month. But other categories (department stores, e-commerce, and furniture & electronics stores to name a few) were also robust beyond expectations. This suggests that demand remains resilient: our estimate of real sales was up 2.8% on the month, turning the three-months trend positive (Chart 2).

What didn’t respond to warm weather is housing starts, which fell by 4.5% m/m in January, coming in below the consensus forecast. Both single- and multi-family segments were softer, but while the former remains below its pre-pandemic average, the latter remains 27% stronger relative to 2018-19. Still, housing construction is the only measure that held a course towards disinflation this week. The rest of the economic data makes a “compelling economic case” to bring rates higher and keep them there for longer. As a result, the probability of a 50-basis point hike in March rose from 9% to 21% on the week, while bets on fewer rate cuts by the end of the year jumped higher. We now expect the Fed will raise the policy rate to 5.25% and keep it there until the fourth quarter of 2023 (see D&S).

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Featured Article: Dream Retirements Reconsidered

Dream Retirements Reconsidered

When deciding on the ideal place for retirement, a little homework can spare you a lot of headaches.

When it comes to retirement, people often get caught up in the illusion, rather than the reality of retirement living. Before making a commitment to move, understand this change is a fine mix of dreams, practicalities and your vision.

You can find your perfect mix when you consider all the factors, beyond the weather, amenities and proximity to friends.

With an ocean of options, how do you decide? Consider your vision and your wants and needs, because none of the "Best Places to Retire" lists can consider your personal likes and dislikes. Also, there are practical and financial considerations to recognize.

Here are three dreams that disappointed many newly minted retirees:

1. Live Near Your Children

You finally have time for family time in retirement. You want to be available to your children and more engaged in their lives. Best of all, if you are lucky enough to have grandchildren, you desire to get to know them better, even teaching them things your grandparents taught you.

There are some valuable conversations you need to have with your children before you put up that "For Sale" sign and look for a place nearby. As your children are working with full schedules, plan time for a serious chat. This important conversation is so you can understand their life a bit more and learn what works for them.

Ask yourself if you like the area enough that you would move there if your child was not there.

Some conversation starters are: How does your child and their family fit you into their life? Do they want you around more often? Are they worried about the time and energy of being with you? Or caring for you eventually? You may be healthy now, but such an issue may be on their mind.

Then, ask yourself if you like the area enough that you would move there if your child was not there. Is the community a good fit? The weather? The available activities?

If you do make the move, remember that your adult children had a routine and schedule before you got there. When you arrive, create a life without them as much as with them. Retirees who settle in and focus only on family often feel lost 10 years down the road when the toddler grandchildren who they saw everyday grow into teenagers who prefer to be with friends. If they end up moving away for college, you will see them even less.

Prepare for change, just in case. A job transfer, career change, corporate merger or any number of other life-disrupting events may lead your child's family to relocate in coming years. Would you feel you had no option but to follow them again? Or could you stay put because you had built a community that would let you confidently live on your own?

A couple bought a condominium in Arizona in anticipation of their retirement one year out and enjoyed the vacation time they spent with their children and grandchildren before they retired. Three months after they retired and moved, their son-in-law's company transferred him to California. The couple was left alone and reflecting on the possible need for another move.

2. Move to a Favorite Vacation Area

Vacations are freedom from everyday life. It's easy to dream of retiring in your favorite vacation spot. Before committing to a location, stay longer than usual. Rent a home for a month, a season or a year. Explore the area as a local.

Do not forget seasons. Spend a winter at the lake or a summer at the ski resort before committing to buy.

Just because you like to vacation somewhere does not mean it is the ideal retirement home location.

Just because you like to vacation somewhere does not mean it is the ideal retirement home location. Many people move twice because they thought they knew what they wanted. And moving is expensive. The average moving company bill for a 1,200-mile move is $4,000.

One couple made a quick decision to sell their home without thinking it through. As soon as the sale went through, they went to Florida and bought a condominium in an area where they spent their annual vacation.

They discovered they bought in a rental area, not a residential area, so making friends was difficult and some services limited. A year later, they moved to another area, incurring moving costs and Realtor fees again.

Emotional and personal reasons for moving are important, but so are costs such as taxes. If you change residency to a new state, consider the cost of new car registrations and legal fees for an updated estate plan. Explore the true costs of the area you want to move to, so you avoid surprises.

3. Head for the Border and Skip the Country in Retirement

The grass always looks greener when thinking of where to retire... and that applies whether you are considering Canada, Mexico, Europe or beyond. In the excitement to retire, many people only consider the big picture of what looks good rather than practicalities of an international move.

If you are moving for cultural immersion, understand many of the places that attract you also draw other Americans. The good news: you can associate with people who share your experience. But by sticking together, you are less likely to be treated as a local than foreigners who assimilate.

There is the legal side of residency. Understanding how you can live in a country long-term is essential, so check out the visa process. A country may or may not make it easy for U.S. citizens to immigrate. For example, Canada recently forbid foreign nationals to buy property for two years.

"The tax situation may be higher than anticipated, offsetting the lower cost of living."

The cost of living is one reasonable draw to live outside the United States, yet there are other financial considerations. "Retirement income will be 100% taxable by the U.S. and perhaps additionally in the country you move to," says Malissa Marshall, a Certified Financial Planner in Bristol, Vermont.

"The tax situation may be higher than anticipated, offsetting the lower cost of living," she emphasizes.

You may want to hire a tax professional in the country you are considering and one in the U.S. before finalizing any plans. An international expert can explain the reality in a short time.

Consider Health Care Abroad

Then, there is the issue of health care and insurance, especially if you do not pay for the Medicare premiums while you live abroad. If you ever return to the U.S., your Medicare insurance premiums will be permanently higher. Medicare charges a premium penalty for the months you did not pay but were qualified, even if you were covered overseas.

To see more fantastic articles like this one, please see here.

Financial News for the Week of February 9th, 2023

Financial News Highlights

- Since last Friday’s blockbuster employment report, market pricing on the peak fed funds rate has firmed to 5.25%. This aligns to the FOMC’s December projections, though markets still foresee the Fed cutting rates later this year.

- At an event on Tuesday, Fed Chair Powell did not pushback against investors’ diverging view, nor was his tone any more hawkish, despite last week’s strong reading on employment.

- With the FOMC now in the “fine turning” stage of the tightening cycle, policymakers have become increasingly data dependent. This means next week’s inflation report will be under the microscope.

Holding the Line… For Now

It was a very quiet week on the economic data calendar, giving investors a bit more time to digest last week’s blockbuster employment numbers in financial news. Since the jobs report, market pricing on the future path of the fed funds rate has firmed, with investors now anticipating two more 25 basis-point hikes by May, bringing the terminal rate to 5.25%. This aligns to FOMC’s last forecast outlined in the December Summary of Economic Projections. In contrast, markets differ from the Fed on the timing of rate cuts, with interest rate cuts priced in by financial markets for later this year, whereas the Fed doesn’t foresee that happening until 2024.

It was a very quiet week on the economic data calendar, giving investors a bit more time to digest last week’s blockbuster employment numbers in financial news. Since the jobs report, market pricing on the future path of the fed funds rate has firmed, with investors now anticipating two more 25 basis-point hikes by May, bringing the terminal rate to 5.25%. This aligns to FOMC’s last forecast outlined in the December Summary of Economic Projections. In contrast, markets differ from the Fed on the timing of rate cuts, with interest rate cuts priced in by financial markets for later this year, whereas the Fed doesn’t foresee that happening until 2024.

At an event on Tuesday, Fed Chair Powell did not pushback against the markets’ diverging view. Instead, he reiterated many of the same themes that he had emphasized in the press conference following last week’s interest rate announcement. The key message being that while the disinflationary process has begun, it remains very much in the early stages, and it will take “considerable time” before inflation returns to 2%. While financial markets initially rallied on the remarks, they later sold-off through the back-half of the week. At the time of writing, the S&P 500 is down 2%, while the 10-year Treasury edged higher by 15bps to 3.7% for the week.

When asked specifically about last week’s employment numbers, Powell said that it, “simply reaffirmed that the central bank has some way to go on raising rates” and that the strong numbers highlight that the adjustment process is unlikely to be linear. While there’s certainly validity to that argument, there’s also reason to believe that the January payrolls may be overstating the degree of strength in the labor market.

For starters, January was unseasonably warm across most of the U.S., which likely means there was a pull forward of economic activity. From that perspective, some of January’s gains may have been robbed from subsequent months – suggesting much weaker employment growth in the months ahead. Second, seasonal adjustment factors may have also played some role in biasing last month’s numbers higher. January is historically a month where non-seasonally adjusted payrolls record a massive decline in absolute terms (Chart 1). While this remained true last month, it did so by the smallest amount since 1995. This likely translated to an outsized gain in the seasonally adjusted figures.

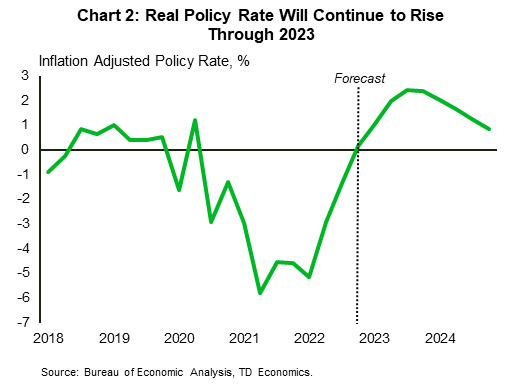

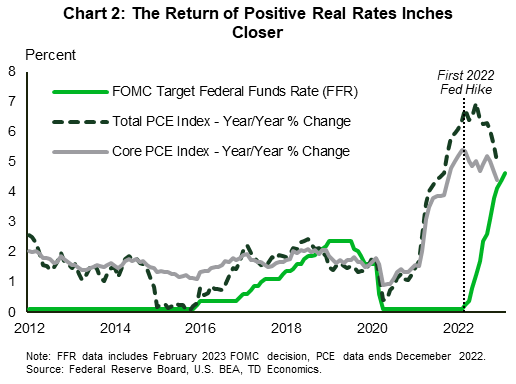

So, where does that leave us? It’s up for debate how much the January numbers are overstating the degree of underlying strength. But, at the end of the day, there is little doubt that the labor market remains incredibly tight. For now, Chair Powell seems content to not rattle expectations and watch how the data evolves in further financial news. You can’t argue the logic. Monetary policy acts with considerable lag, and the cumulative effect of all the tightening done over the past 11 months is not yet being felt. Even once rate hikes are finished, the real effective policy rate will continue to rise through this year as inflation continues to decline (Chart 2). With the FOMC now in the “fine tuning” stage of the tightening cycle, data dependence will be the name of the game. With that, the focus now shifts to next week’s inflation report. Stay tuned!

So, where does that leave us? It’s up for debate how much the January numbers are overstating the degree of underlying strength. But, at the end of the day, there is little doubt that the labor market remains incredibly tight. For now, Chair Powell seems content to not rattle expectations and watch how the data evolves in further financial news. You can’t argue the logic. Monetary policy acts with considerable lag, and the cumulative effect of all the tightening done over the past 11 months is not yet being felt. Even once rate hikes are finished, the real effective policy rate will continue to rise through this year as inflation continues to decline (Chart 2). With the FOMC now in the “fine tuning” stage of the tightening cycle, data dependence will be the name of the game. With that, the focus now shifts to next week’s inflation report. Stay tuned!

Thomas Feltmate, Director | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of February 3rd, 2023

Financial News Highlights

- The Federal Reserve hiked the fed funds rate 25 basis-points, a step down from six consecutive hikes of 50 or 75 bps.

- Non-farm payrolls accelerated in January for the first time in five months, adding 517k jobs and nearly tripling market expectations.

- The ISM Manufacturing Index dropped to its lowest level since May 2020, with new orders declining at an accelerating rate, while the ISM Services Index returned to strong growth after contracting in December.

Until the Job Is Done

With the first month of 2023 in the books, the start of February was marked by the much anticipated (but widely expected) rate decision delivered by the Federal Reserve on Wednesday in major financial news. Coupled with a sizeable upside surprise in the January employment data on Friday, markets certainly had a lot to think about this week. The S&P 500 rose 2.6% for the week, while the ten-year Treasury yield was little changed at 3.5% as of the time of writing.

With the first month of 2023 in the books, the start of February was marked by the much anticipated (but widely expected) rate decision delivered by the Federal Reserve on Wednesday in major financial news. Coupled with a sizeable upside surprise in the January employment data on Friday, markets certainly had a lot to think about this week. The S&P 500 rose 2.6% for the week, while the ten-year Treasury yield was little changed at 3.5% as of the time of writing.

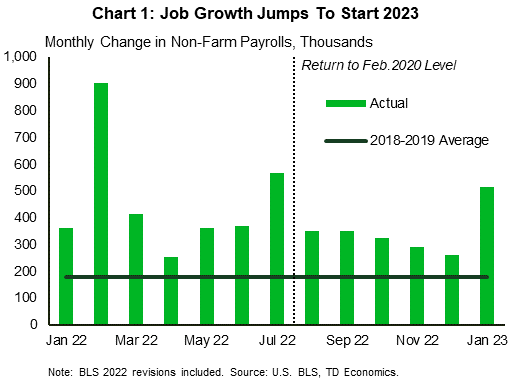

Labor markets began 2023 with a bang, breaking a five-month deceleration trend and adding 517k jobs (Chart 1). This brought the unemployment rate down by 0.1 percentage points (ppts) to a 53-year low of 3.4%. In addition, revisions to 2022 data added 311k jobs to last year’s tally. The labor force participation rate in January ticked up by 0.1 ppts to 62.4%. Average hourly earnings rose by 0.3% month-on-month (m/m) and hours worked increased by 0.9% m/m. On aggregate, this was an exceptionally strong jobs report, which when combined with the sustained downward trend in initial jobless claims and the increase in December job openings, will give the Federal Reserve plenty to contemplate over the coming weeks.

In contrast to the strong labor market data, the ISM Manufacturing Purchasing Managers’ Index (PMI) slipped further into contractionary territory in January, dropping 1 percentage point to 47.4 – its lowest level since May 2020. Economic activity in the sector contracted for the third consecutive month, as new orders continued to decline at an accelerating rate. This contrasts with the ISM Services PMI which showed the industry return to strong growth in January after briefly contracting in December, with new orders jumping up by 15.2 percentage points. While there have been positive developments in the manufacturing sector, such as reduced delivery times and lower price pressures, the robustness of the strength in the services sector will be a concern for the Federal Reserve as it seeks to put a lid on services price growth.

February began with a partial return to conventional monetary policy in the U.S., with the Federal Reserve raising rates by a more usual 25bps for the first time since last March (Chart 2). FOMC Chair Powell noted that it was gratifying to see progress on disinflation, but that further policy tightening would be required to ensure price growth sustainably returns to the Fed’s 2% target in financial news. During the press conference, Powell also pushed back against the idea of assuming the Fed could mitigate the risk of a binding debt limit in June, stating that the only way forward was for Congress to raise the debt ceiling.

February began with a partial return to conventional monetary policy in the U.S., with the Federal Reserve raising rates by a more usual 25bps for the first time since last March (Chart 2). FOMC Chair Powell noted that it was gratifying to see progress on disinflation, but that further policy tightening would be required to ensure price growth sustainably returns to the Fed’s 2% target in financial news. During the press conference, Powell also pushed back against the idea of assuming the Fed could mitigate the risk of a binding debt limit in June, stating that the only way forward was for Congress to raise the debt ceiling.

Markets expect another 25bps hike at the Fed’s next meeting in six weeks, at which time we will also receive an update on the Committee’s Summary of Economic Projections. The January employment report introduced fresh uncertainty to market expectations for the terminal rate, with May meeting expectations now evenly split between no change and a 25bps hike. Powell is in the hot seat in a Q&A next Tuesday, where he is likely to be pressed on his reading of the January jobs blowout. He is likely to confirm the hawkish bias of the press conference, and markets will be listening carefully for any hints of how high the Fed expects to raise rates now.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of January 20th, 2023

Financial News Highlights

- Markets finished the week lower on weaker economic data and rising political risks.

- December retail sales registered the biggest monthly decline in 2022, finishing the fourth quarter flat. Housing starts were down less than expected, driven by the volatile multifamily component. Existing home sales continued to soften.

- This week’s Fed speakers demonstrated a varying degree of hawkishness on the pace of upcoming rate hikes. Yet, markets are all but priced-in a 25-basis point increase.

Bad News is Bad News

The week started with a holiday, but that didn’t stop markets from feeling the blues of the most depressing period in the Northern Hemisphere in financial news. At the time of writing, equities are down almost 2% on the week. On the political front, concerns about the government’s ability to pay its debts resurfaced as the Treasury Department was forced to begin taking ‘extraordinary measures’ in order to keep paying the government’s bills. By suspending certain additional investments, the Treasury buys Congress more time – likely until June - to negotiate a resolution on how to increase the debt ceiling. With the deadline still several months out, investors’ focus was squarely on the economic data. Unfortunately, there was little to cheer about.

The week started with a holiday, but that didn’t stop markets from feeling the blues of the most depressing period in the Northern Hemisphere in financial news. At the time of writing, equities are down almost 2% on the week. On the political front, concerns about the government’s ability to pay its debts resurfaced as the Treasury Department was forced to begin taking ‘extraordinary measures’ in order to keep paying the government’s bills. By suspending certain additional investments, the Treasury buys Congress more time – likely until June - to negotiate a resolution on how to increase the debt ceiling. With the deadline still several months out, investors’ focus was squarely on the economic data. Unfortunately, there was little to cheer about.

Retail sales came in weaker than expected – falling 1.1% m/m - and marking the second consecutive month of declines. Most major categories were weak in both nominal and inflation adjusted terms. The only group that showed stronger demand was sales at gas stations, where real sales rose five percentage points on a sizeable drop in gas prices (Chart 1). The message is clear: consumers are becoming increasingly more cautious in allocating their income and pandemic savings. Moreover, judging by sales at restaurant and bars, demand for services might also be nearing an inflection point. The soft reading on retail sales led us to adjust our expectations for Q4 consumer spending down to a still robust 2.7% (previously 3.3%).

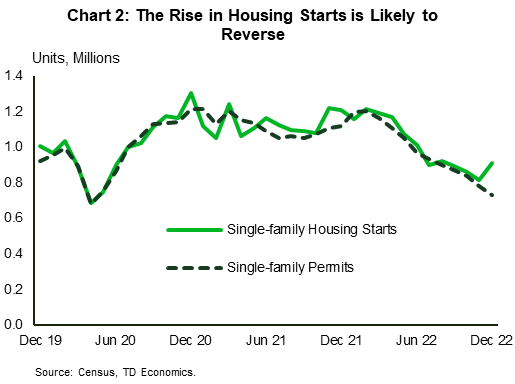

Housing activity also ended 2022 on a soft note. Residential construction declined for the fourth consecutive month, but by less than expected in December. The decline was attributed to a 19% drop in the multi-family segment. In contrast, starts in the single-family, rose for the first time in four months, but are likely to decelerate further in the months ahead as permits continue to trend lower (Chart 2).

On that note, existing home sales also continued to soften, falling 1.5% m/m December and 17.8% for the year. Despite the sharp decline in sales, prices have only fallen by 1.5%. However, the sharp increase in inventory since August suggests more meaningful downward pressure lies ahead.

On that note, existing home sales also continued to soften, falling 1.5% m/m December and 17.8% for the year. Despite the sharp decline in sales, prices have only fallen by 1.5%. However, the sharp increase in inventory since August suggests more meaningful downward pressure lies ahead.

Increasingly bold signs of cooling economic activity are welcome news for the Fed on its mission to bring down inflation. That said, this week’s Fed speakers had varying degrees of hawkishness on the pace of upcoming rate hikes. Of those who have the voting rights on the Federal Open Market Committee, James Bullard sounded most hawkish by expressing his preference to “err on the tighter side to get the disinflationary process to take hold”.

In contrast, Fed’s Lorie Logan and Patrick Harker voiced their support for a 25-basis point hike, while Vice Chair Lael Brainard, without explicitly backing a softer pace, emphasized the possibility of a soft lending - easing in the labor market and reduction in inflation without a significant loss of employment in further financial news. Markets side with this view, having priced-in a quarter-of-a percent hike on February 1st with a 97% probability. Compare it to exactly one month ago, when only 70% of market participants (including yours truly) expected a downshift. Seemingly, investors express more certainty about an economic slowdown ahead.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Featured Article: 401k and Retirement Changes

The 401(k) and IRA Changes to Consider After Congress Revised Many Retirement Laws

New policies for retirement saving would go into effect immediately or in the New Year

Americans will need to rethink how they save after Congress passed a series of laws that stand to overhaul parts of the country’s retirement saving system.

The retirement overhaul is part of a larger bill passed by Congress just before the holidays. It includes dozens of retirement policy changes that go into effect over the next decade. Many of these provisions kick in immediately after the bill passes, however, creating the need for Americans to examine their own financial planning now, financial advisers say.

The main changes that go into effect right away include incentives for more employers to offer retirement plans and to encourage workers to contribute, and new rules on taking money out and getting lifetime payouts.

Here’s a rundown of the key changes and what you might need to do:

New Rules for Taking Money Out

Required Minimum Distributions. The new legislation raises the age taxpayers generally have to start taking required minimum distributions, known as RMDs, from their retirement accounts to 73 from 72, starting in 2023. That means if you turned 72 in 2022, you have until April 1, 2023, to take your first RMD, the one for 2022, and you’ll have to take another for 2023 by Dec. 31, 2023. If you turn 72 in 2023, your first RMD will be for 2024, the year you turn 73, due on April 1, 2025.

The legislation doesn’t do anything to address the confusion surrounding the new 10-year payout rule for IRAs inherited after 2019.

Missed RMD penalty relief. Congress is reducing the 50% penalty for missed RMDs to 25% of the amount that should have been withdrawn. The penalty drops to 10% if it is corrected in a timely manner.

New exceptions to the 10% early withdrawal penalty. Typically, there’s a 10% penalty if you withdraw money from 401(k)s or other pretax retirement accounts before age 59 ½. The new legislation enhances several existing exceptions, including covering certain private-sector firefighters and public safety officers. It also adds new categories, allowing individuals who are terminally ill to make limited penalty-free withdrawals.

A catchall exception allowing anyone with a personal or family emergency to withdraw up to $1,000 a year penalty-free kicks in for 2024. A penalty exception for those affected by federally declared disasters is retroactive to Jan. 26, 2021. There are also exceptions for victims of domestic abuse and payment of long-term-care premiums.

New Rules to Encourage Savings

Small-employer retirement plan startup tax credit. If you work for a small employer with up to 50 employees that doesn’t offer a retirement plan, your company is eligible for an enhanced tax credit to start up a plan as of Jan. 1. The new credit covers 100% of initial costs up to $5,000 for three years, depending on the number of eligible employees. Employers with 51 to 100 employees get a lesser credit. There’s an additional credit if an employer also matches employee contributions, available for five years.

Solo 401(k)s. Under current law, self-employed individuals who want to establish an individual or solo 401(k) retirement plan have to set it up by Dec. 31 to make contributions for that year. Under the new provision, they have until they file their tax return the next year to open and fund the account, starting with the 2023 tax year.

$2,500 rainy day emergency savings accounts. The legislation allows employers to automatically enroll non-highly compensated employees, those who make up to $150,000 for 2023, in emergency savings accounts linked to a 401(k) plan. Employees could save up to $2,500, and withdrawals would be tax and penalty-free.

Gift cards. The legislation authorizes employers to hand out a small cash payment or gift card to encourage workers to sign up for and contribute to a 401(k)-type retirement plan. The idea is that some employees might respond to even a couple hundred dollars as a sign-up bonus, says Mark Iwry, a former Treasury Department official.

Roth employer matching. The new legislation permits employers to offer Roth matching contributions into an employee’s 401(k) account. Currently, employer match money goes into employee accounts on a pretax basis. Under the new rules, employees can now choose to take the Roth match, which means they are able to pay taxes up front and then later take out the contributions, and potentially the earnings, tax-free.

Lifetime Income Provisions

IRA Charitable Rollover. The legislation includes a provision that lets IRA owners who are 70 ½ or older take a one-time withdrawal of up to $50,000 to fund a charitable gift annuity or charitable remainder trust. That’s a tax win for IRA owners because the withdrawal doesn’t count as income, and it can count toward any required minimum distribution amount for the year.

They generally work like this: The IRA owner gets a minimum payout of 5% annually, taxed as ordinary income, and the charity gets what’s left when the donor dies. The only beneficiaries can be the owner alone or the owner and his or her spouse.

“Charities are going to be telling all their donors about this,” says Conrad Teitell, a tax lawyer in Stamford, Conn., who publishes Taxwise Giving. Effective date: Jan. 1, 2023.

Deferred annuities. For retirees looking for guaranteed income in their old age, the retirement legislation enables more people to take advantage of qualified longevity annuity contracts, known as QLACs, says Mr. Iwry, who spearheaded Treasury’s development of QLACs in 2014.

A QLAC is a deferred annuity that you can buy, say in your 60s, with guaranteed payouts for life starting at age 80 or 85, for example. Under the new rules, 401(k) participants or IRA owners could use up to $200,000 from their account to buy the annuity that would make guaranteed payments for life. Current rules limit the QLAC amount to $145,000 or 25% of the retirement account balance, if less.

“QLACs cover the tail risk of outliving your retirement savings,” Mr. Iwry says. Effective date: when the act is signed into law.

Write to Ashlea Ebeling at ashlea.ebeling@wsj.com

To see more fantastic articles like this one, please see here.

Financial News for the Week of January 13th, 2023

Financial News Highlights

- After fifteen rounds of votes, Kevin McCarthy was elected the new House Speaker. However, it didn’t come without making major concessions, setting the stage for more political brinksmanship over the coming months.

- Headline inflation came in below expectations – falling 0.1% m/m. The core measure rose by 0.3% m/m, bring the 12-month change to 5.7% - the slowest pace of price growth in a year.

- Data out this week showed that labor market remains incredibly tight. The number of small businesses with unfilled job openings remains historically elevated while jobless claims have steadily trended lower over the last month.

Inflation Turning, But Victory Still Nowhere Insight

This week ushered in a new House Speaker and a fresh reading on CPI in major financial news. The former came after fifteen rounds of votes and several concessions made by Speaker McCarthy. Of those, arguably the biggest was a commitment to pairing an increase in the debt ceiling with cuts in government spending. U.S Treasury Security Janet Yellen informed Congress that the debt limit could be reached as early as next week, and Treasury will start to employ extraordinary measures which are expected to last until June. With Democrats unwilling to tie debt ceiling negotiations to cuts in spending, we are headed for more fiscal brinkmanship over the coming months.

This week ushered in a new House Speaker and a fresh reading on CPI in major financial news. The former came after fifteen rounds of votes and several concessions made by Speaker McCarthy. Of those, arguably the biggest was a commitment to pairing an increase in the debt ceiling with cuts in government spending. U.S Treasury Security Janet Yellen informed Congress that the debt limit could be reached as early as next week, and Treasury will start to employ extraordinary measures which are expected to last until June. With Democrats unwilling to tie debt ceiling negotiations to cuts in spending, we are headed for more fiscal brinkmanship over the coming months.

After last week’s payrolls report, investors were eager to see the December reading on U.S. CPI to better gauge the future path of the policy rate. Going into the week, most market participants expected a further downshift in the pace of rate hikes when the FOMC next meets in early-February. Inflation is (finally) moving in the right direction, solidifying market pricing for a 25-bps hike in financial news. Equities were up 2% on the week, while the U.S. 10Y fell by roughly 10-bps and currently sits at 3.45%

Headline inflation fell 0.1% m/m – a tick below expectations – with the pullback largely attributed to weaker gasoline prices (-9.4%). The core measure rose by 0.3% which brought the twelve-month change to “just” 5.7% – the slowest pace of growth in over a year. Even more encouraging was the steady downward trend in the three-month annualized change, which now sits at 3.1% (Chart 1).

Distortions from the pandemic continued to show further evidence of easing, with core goods prices (-0.3%) falling for the third consecutive month. Declines were primarily concentrated in transportation, while most other categories were higher on the month. That said, retail inventories have been piling up more recently, suggesting we are likely to see further price declines in things like apparel, furniture, and electronics in the months ahead. While encouraging, a softening in goods prices alone can only go so far in bringing down inflation. Core services will also need to slow, and herein lies the problem. Shelter continues to make outsized gains and is not expected to rollover until mid-year. Meanwhile, services (excluding shelter), whose price growth is more closely tied to wages, is unlikely to slow until we see some softening in underlying labor market conditions. And that doesn’t appear to be on the immediate horizon.

Distortions from the pandemic continued to show further evidence of easing, with core goods prices (-0.3%) falling for the third consecutive month. Declines were primarily concentrated in transportation, while most other categories were higher on the month. That said, retail inventories have been piling up more recently, suggesting we are likely to see further price declines in things like apparel, furniture, and electronics in the months ahead. While encouraging, a softening in goods prices alone can only go so far in bringing down inflation. Core services will also need to slow, and herein lies the problem. Shelter continues to make outsized gains and is not expected to rollover until mid-year. Meanwhile, services (excluding shelter), whose price growth is more closely tied to wages, is unlikely to slow until we see some softening in underlying labor market conditions. And that doesn’t appear to be on the immediate horizon.

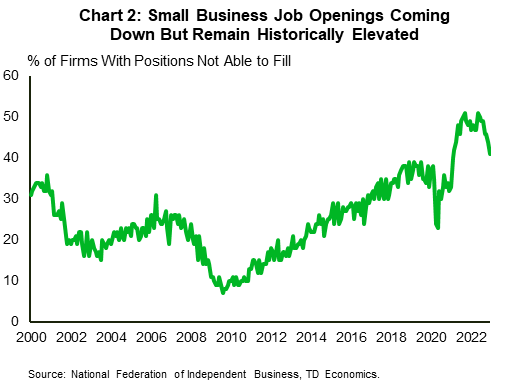

Data out this week showed that while the number of small businesses reporting job openings are declining, they remain historically elevated (Chart 2). As a result, nearly half of small businesses surveyed reported having increased compensation in recent months, while more than a quarter are planning to boost wages over the next three months. Elsewhere, jobless claims continued to edge lower through the first week of January – falling to 205k – with the four-week moving average having steadily declined since late-November. Putting all this together suggests the labor market remains incredibly tight and has not yet reached an inflection point. So while inflation may be easing, the Fed is nowhere near declaring victory. We expect more tightening to come over the coming months – likely in the form of two 25-bps hikes – before pausing to assess the cumulative impact of all 475-bps of tightening.

Thomas Feltmate, Director | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of January 6th, 2023

Financial News Highlights

- The labor market cooled modestly in December, with 223k new jobs added and the unemployment rate ticking back

down to 3.5%. - The House of Representatives failed to elect a Speaker of the House on the first ballot for the first time in 100 years,

delaying the start of the new legislative session in the lower chamber of Congress. - FOMC minutes from the December meeting underlined the hawkish stance of the committee and warned of the

dangers of a pre-mature easing of financial conditions.

Plenty of Jobs, Except in Congress

The start of the new year kicked off with several important December data releases, including an update on the labor market and FOMC meeting minutes in financial news. In addition, the new Congressional session got off to a rocky start, with the House of Representatives unable to elect a Speaker of the House. Equity markets fluctuated on the week with the S&P 500 down 0.4% while yields declined sharply, with the 10 Year Treasury at 3.58% as of the time of writing.

The start of the new year kicked off with several important December data releases, including an update on the labor market and FOMC meeting minutes in financial news. In addition, the new Congressional session got off to a rocky start, with the House of Representatives unable to elect a Speaker of the House. Equity markets fluctuated on the week with the S&P 500 down 0.4% while yields declined sharply, with the 10 Year Treasury at 3.58% as of the time of writing.

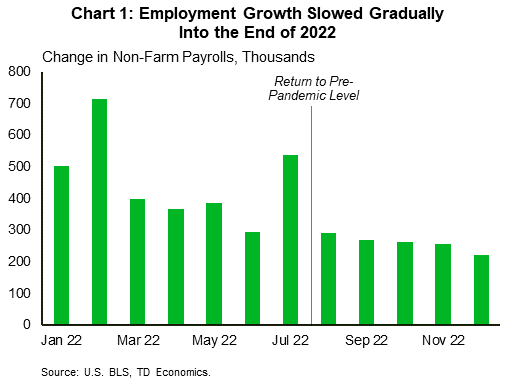

The exceptional strength seen in the jobs market over the past two years slowed into the end of 2022, with December adding 223k new jobs and bringing the annual total to 4.5 million (Chart 1). The labor market remained tight with the unemployment rate declining back to 3.5% as the labor force rose by 0.3% and the participation rate ticked up by 0.1 percentage-points. Average hourly earnings growth decelerated to 0.3% month-on-month, inciting an initial rally in equity markets as participants looked for evidence which might lead to a reprieve from the current aggressive round of rate hikes. The report also showed a notable uptick in the number of multiple job holders reflecting the weight of inflation and rate hikes on households as they seek additional support through secondary incomes.

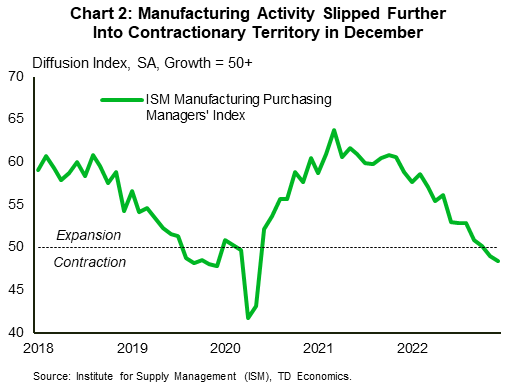

Earlier in the week, manufacturing data showed signs of further slowing, with the ISM manufacturing purchasing managers’ index (PMI) slipping further into contractionary territory in December (Chart 2). After two years of growth the industry has begun to give back some of its gains, in large part due to the direct and indirect effects of higher rates. We also saw this play a part in the ISM Services PMI which declined sharply and showed the sector contracting in December for the first time in 30 months. Within the services index, declines were led by new orders which dropped sharply by over 10.8 percentage-points relative to November. On a more positive note, the manufacturing report showed a continued decline in supply price pressures and improving delivery times, which will be welcome news for the Federal Reserve.

FOMC meeting minutes released on Wednesday unsurprisingly echoed earlier sentiments expressed by Chair Powell at his December 14th press conference. Members pushed back against the loosening of financial conditions seen in recent months on the back of softer inflation reports, noting that “an unwarranted easing in financial conditions…would complicate the committee’s effort to restore price stability” in financial news. The minutes reiterated that “it would take substantially more evidence of progress to be confident that inflation was on a sustained downward path”, and this was further emphasized by the fact that no committee members foresee cutting rates this year.

FOMC meeting minutes released on Wednesday unsurprisingly echoed earlier sentiments expressed by Chair Powell at his December 14th press conference. Members pushed back against the loosening of financial conditions seen in recent months on the back of softer inflation reports, noting that “an unwarranted easing in financial conditions…would complicate the committee’s effort to restore price stability” in financial news. The minutes reiterated that “it would take substantially more evidence of progress to be confident that inflation was on a sustained downward path”, and this was further emphasized by the fact that no committee members foresee cutting rates this year.

Minneapolis Fed President (and 2023 FOMC member) Neel Kashkari also released an essay on Wednesday in which he noted the need to raise rates by another 100bps this year, which helped to briefly push the odds of a 50bps hike in February close to 50%, though they have since declined back to roughly 25%. Next week we will get December CPI data which will help clarify whether the recent downturn in inflation persisted into the end of the year.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.