Financial News for the Week of July 29th, 2022

Financial News Highlights

-

Highlights

- Real GDP declined for the second consecutive quarter in Q2, meeting one (narrow) criteria of a recession.

- The Federal Reserve delivered another supersized rate hike of 75bps this week, bringing the upper bound of the policy rate to 2.5%. Chair Powell emphasized the need to take rates higher but neglected to give any forward guidance.

- The energy shock due to Russia’s war in Ukraine that is fueling much of the region’s inflation is also increasingly likely to profoundly restrict growth.

- For the European Central Bank, this represents the worst-case scenario, as it could soon be faced with the prospect of raising rates to preserve longer-term stability despite an output contraction.

U.S. Technically Not There (Yet)

The dreaded “R” word (recession) isn’t one economist’s use lightly. This is why so much focus was placed on this week’s advance estimate of Q2 GDP and the FOMC meeting in financial news.

The dreaded “R” word (recession) isn’t one economist’s use lightly. This is why so much focus was placed on this week’s advance estimate of Q2 GDP and the FOMC meeting in financial news.

According to Bureau of Economic Analysis, real GDP declined 0.9% q/q (annualized) in Q2 – well below the consensus forecast of a modest 0.4% gain (Chart 1). More significant than the headline print was that activity has now declined in each of the last two consecutive quarters – meeting one (narrow) criteria of a “technical” recession. At this point, most economists would agree that the US economy isn’t (yet) in recession. The National Bureau of Economic Research (NBER), who is tasked with dating business cycles, would also agree. Outside of just economic growth, the NBER considers a host of other indicators including measures of production, employment, and income. At present, most of these measures continue to point to an economy that remains in expansionary territory.

That said, domestic demand has shown a clear sign of slowing. Consumer spending decelerated to just 1% in the second quarter, while fixed investment declined by 3.9%. At this point, it doesn’t appear that growth prospects will be improving anytime soon. Measures of both consumer and business sentiment have turned decisively lower in recent months, and this is showing in the monthly consumer spending data (Chart 2). After adjusting for inflation, real consumer spending was up just 0.1% m/m in June – a rebound from May’s 0.3% decline – but nonetheless a weak handoff into Q3.

The FOMC acknowledged the recent softening in economic data in the very first sentence of its July statement. But that didn’t stop them from raising rates by another 75bps. At 2.5%, the policy rate is now in the vicinity of the FOMC’s assessment of neutral – the interest rate that’s neither accommodative nor restrictive. However, Chair Powell was explicit in the press conference that the Committee intends to raise the policy rate well into “restrictive” territory in order to return price stability. Powell was careful in his word choice, admitting that doing so will lead to some slowing in growth and a rise in the unemployment rate, but skirted any explicit reference to recession. Just how far above neutral the FOMC will have to go remains dependent on how the economy responds to past hikes between now and September.

The FOMC acknowledged the recent softening in economic data in the very first sentence of its July statement. But that didn’t stop them from raising rates by another 75bps. At 2.5%, the policy rate is now in the vicinity of the FOMC’s assessment of neutral – the interest rate that’s neither accommodative nor restrictive. However, Chair Powell was explicit in the press conference that the Committee intends to raise the policy rate well into “restrictive” territory in order to return price stability. Powell was careful in his word choice, admitting that doing so will lead to some slowing in growth and a rise in the unemployment rate, but skirted any explicit reference to recession. Just how far above neutral the FOMC will have to go remains dependent on how the economy responds to past hikes between now and September.Perhaps the most noteworthy takeaway from Powell’s entire press conference came from what he neglected to say. In contrast to more recent briefings, the Chair failed to give explicit forward guidance on the expected changes to the policy rate at its next meeting in major financial news. Instead, he emphasized the need to “just go to a meeting-by-meeting basis”, suggesting the size of future hikes will be entirely data dependent. From that perspective, the July/August CPI and employment reports will be under the microscope. However, the Q2 release of the employment cost index will also catch the FOMC’s eye. The index adjusts for the composition of jobs, providing the cleanest snapshot of overall employee earnings. It showed that growth in employment compensation remained elevated in Q2 – growing 5.4% (annualized). From a scoring perspective, this favors another big move in September. Let’s see what employment brings next Friday!

Thomas Feltmate, Director | 416-944-5730

The European Dilemma

The European Central Bank (ECB) is facing a daunting outlook. The energy shock due to Russia's war in Ukraine that is fueling much of the region's inflation is also increasingly likely to profoundly restrict growth in financial news. As near-term indicators are signaling that a recession may soon begin, the ECB has committed to a "meeting-to-meeting" basis for rate decisions that could force them to raise rates into a recession.

The European Central Bank (ECB) is facing a daunting outlook. The energy shock due to Russia's war in Ukraine that is fueling much of the region's inflation is also increasingly likely to profoundly restrict growth in financial news. As near-term indicators are signaling that a recession may soon begin, the ECB has committed to a "meeting-to-meeting" basis for rate decisions that could force them to raise rates into a recession.

Near-term tracking measures have started to show a steep deceleration, or outright contractions, in economic activity in the euro area. July's flash PMI readings for the euro area reflected a decline in output, with much of the pain being felt in its industrial engine – Germany. The EuroCOIN and Ita-COIN indicators are also showing growth having topped out and starting to fall.

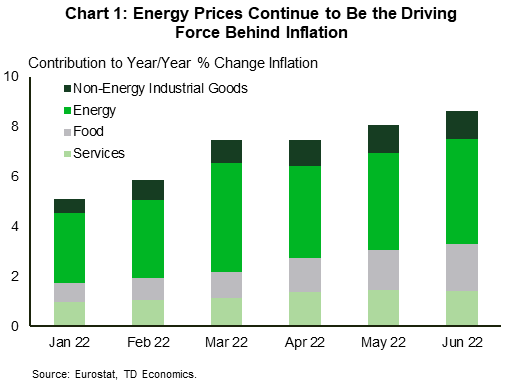

Looking forward, it is the ongoing lift to energy prices that is most concerning. Recession fears have helped crude oil prices off their highs, but supply concerns have supported a high floor under prices. Moreover, if Russia halts natural gas flows to Europe, it risks creating an outright shortage in the coming months, further raising inflation and reducing output. Thus far the energy shock is responsible for roughly half (Chart 1) of the inflationary impulse in the euro zone.

A full stoppage of gas flows would lead to substantial demand destruction and a host of literature on potential losses has emerged in the past months. IMF researchi suggests E.U. output losses could range between -2.7%, in the worst-case scenario and -0.4% if the E.U. were able to fully integrate into the global LNG market.

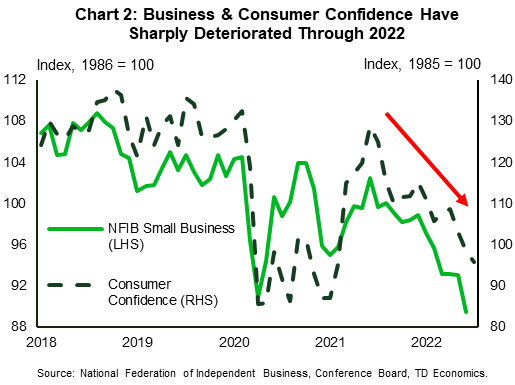

To counteract the risks, the European Commission has asked for a voluntary 15% reduction in natural gas usage across the EU (with some exceptions). These voluntary cutbacks could go a long way to limit the economic fallout from a gas shortage. IMF estimatesii for Germany suggest that by strategically rationing gas, the direct GDP loss in the first six months of the shock could be reduced from 0.9% to 0.2%.Beyond the direct effects, consumer confidence is tumbling (Chart 2). Falls this large typically drive up precautionary savings. Meanwhile, business confidence, having remained relatively resilient through June is starting to weaken notably.

The ECB supported its decision to raise interest rates by 50 basis points by emphasizing the need to temper inflation expectations and the introduction of a new bond-buying tool to help monetary policy transmission. However, higher energy prices are fueling an inflationary feedback loop, and it may soon be faced with the prospect of raising rates to preserve longer-term stability despite an output contraction.

Andrew Hencic, Senior Economist | 416-944-5307

The dreaded “R” word (recession) isn’t one economist’s use lightly. This is why so much focus was placed on this week’s advance estimate of Q2 GDP and the FOMC meeting in financial news.

The dreaded “R” word (recession) isn’t one economist’s use lightly. This is why so much focus was placed on this week’s advance estimate of Q2 GDP and the FOMC meeting in financial news.

The FOMC acknowledged the recent softening in economic data in the very first sentence of its July statement. But that didn’t stop them from raising rates by another 75bps. At 2.5%, the policy rate is now in the vicinity of the FOMC’s assessment of neutral – the interest rate that’s neither accommodative nor restrictive. However, Chair Powell was explicit in the press conference that the Committee intends to raise the policy rate well into “restrictive” territory in order to return price stability. Powell was careful in his word choice, admitting that doing so will lead to some slowing in growth and a rise in the unemployment rate, but skirted any explicit reference to recession. Just how far above neutral the FOMC will have to go remains dependent on how the economy responds to past hikes between now and September.

The FOMC acknowledged the recent softening in economic data in the very first sentence of its July statement. But that didn’t stop them from raising rates by another 75bps. At 2.5%, the policy rate is now in the vicinity of the FOMC’s assessment of neutral – the interest rate that’s neither accommodative nor restrictive. However, Chair Powell was explicit in the press conference that the Committee intends to raise the policy rate well into “restrictive” territory in order to return price stability. Powell was careful in his word choice, admitting that doing so will lead to some slowing in growth and a rise in the unemployment rate, but skirted any explicit reference to recession. Just how far above neutral the FOMC will have to go remains dependent on how the economy responds to past hikes between now and September. The European Central Bank (ECB) is facing a daunting outlook. The energy shock due to Russia's war in Ukraine that is fueling much of the region's inflation is also increasingly likely to profoundly restrict growth in financial news. As near-term indicators are signaling that a recession may soon begin, the ECB has committed to a "meeting-to-meeting" basis for rate decisions that could force them to raise rates into a recession.

The European Central Bank (ECB) is facing a daunting outlook. The energy shock due to Russia's war in Ukraine that is fueling much of the region's inflation is also increasingly likely to profoundly restrict growth in financial news. As near-term indicators are signaling that a recession may soon begin, the ECB has committed to a "meeting-to-meeting" basis for rate decisions that could force them to raise rates into a recession.

To counteract the risks, the European Commission has asked for a voluntary 15% reduction in natural gas usage across the EU (with some exceptions). These voluntary cutbacks could go a long way to limit the economic fallout from a gas shortage. IMF estimatesii for Germany suggest that by strategically rationing gas, the direct GDP loss in the first six months of the shock could be reduced from 0.9% to 0.2%.

To counteract the risks, the European Commission has asked for a voluntary 15% reduction in natural gas usage across the EU (with some exceptions). These voluntary cutbacks could go a long way to limit the economic fallout from a gas shortage. IMF estimatesii for Germany suggest that by strategically rationing gas, the direct GDP loss in the first six months of the shock could be reduced from 0.9% to 0.2%.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of July 22nd, 2022

Financial News Highlights

- June’s housing data showed another decline in activity as the effects of higher mortgage rates and stretched affordability impact the market.

- A strong labor market and tight inventories will support housing construction and limit the downside risks.

- Despite the slowdown in the housing market the Fed will keep up its fight against inflation with another 75-basis point hike next week.

U.S.-Softening Housing Market Won’t Deter Fed

This week’s housing data showed that the market continued to slow meaningfully through June in financial news. Yet, as inflation continues to linger at multi-decade highs the Fed will keep up the fight against rising prices by raising rates another 75-basis points (bps) next week. Fortunately for the housing market a strong labor market and tight inventories will support construction and limit the possibility of a rapid deterioration of conditions.

This week’s housing data showed that the market continued to slow meaningfully through June in financial news. Yet, as inflation continues to linger at multi-decade highs the Fed will keep up the fight against rising prices by raising rates another 75-basis points (bps) next week. Fortunately for the housing market a strong labor market and tight inventories will support construction and limit the possibility of a rapid deterioration of conditions.

On Tuesday the Census Bureau released June data on national housing starts. Overall, starts pulled back 32k units to 1,559k (annualized) in June, touching their lowest reading since last September. However, the entirety of the decline was attributable to weakness in the single-detached segment (-86k) as multifamily construction rose another 54k. The multifamily starts registered 577k units, and apart from April’s 632k and January 2020’s 601k, this is the strongest reading since the late 1980s. Permitting activity pulled back as well, falling 10k to 1,685k (annualized). Again, the multifamily segment showed ongoing strength, with permits rising 74k, while the single-family segment pulled back 84k.

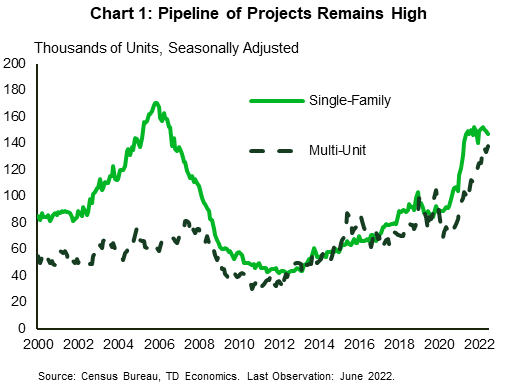

Looking forward, there still looks to be healthy support for construction in the coming months. The pipeline of projects (as measured by units authorized but not started), is at a multi-decade high with a near even split between multi-unit and single-family structures waiting to get shovels in the ground (Chart 1) in further financial news. As raw materials prices come down, and supply chain issues gradually fade, the opportunity for more projects to get underway increases.

Indeed, more construction will be needed as this week’s existing home sales data showed there was roughly 3.0 months’ worth of inventory in the market – still below what is a balanced market. That said, amid falling affordability sales are slowing markedly. June’s existing home sales data reflect just that as sales fell to 5.1 million units (annualized) – the lowest reading since June 2020 (Chart 2). The slowdown in sales activity helped push the seasonally adjusted median sales price down 0.2% on a month-over-month basis. However, affordability continues to be stretched, particularly for the single-family segment. Combined with elevated mortgage rates this should continue to cool housing sales in the coming months.

Indeed, more construction will be needed as this week’s existing home sales data showed there was roughly 3.0 months’ worth of inventory in the market – still below what is a balanced market. That said, amid falling affordability sales are slowing markedly. June’s existing home sales data reflect just that as sales fell to 5.1 million units (annualized) – the lowest reading since June 2020 (Chart 2). The slowdown in sales activity helped push the seasonally adjusted median sales price down 0.2% on a month-over-month basis. However, affordability continues to be stretched, particularly for the single-family segment. Combined with elevated mortgage rates this should continue to cool housing sales in the coming months.

Given the exuberance in the housing market over the past two years, the Fed’s mandate to fight inflation, and the strains on affordability, the slowdown in the housing market was expected. Indeed, residential investment is likely to contract well into 2023. That said, the moderation is simply helping bring the economy back to a pre-pandemic composition.

Despite the slowdown in the housing market the Fed will keep up its fight against inflation with another 75-basis point hike next week. The unemployment rate is still holding at 3.6%, while last week’s CPI print showed inflation hit 9% year-over-year in June. A strong labor market and inflation far from target means policymakers will continue working hard to keep inflation expectations anchored and bring down the pace of price gains.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of July 15th, 2022

Financial News Highlights

- Market sentiment soured this week on stronger than expected CPI data and a weak start to corporate earnings season.

- US CPI accelerated in June, rising 1.3% m/m, pushing the year-ago measure to a new multidecade high of 9.1%. Core inflation accelerated by 0.7% m/m, as hefty gains were seen across both goods (0.8% m/m) and service (0.7% m/m) categories.

- June retail sales surprised to upside, with both the headline (1% m/m) and control measure (0.8% m/m) recording decent nominal gains. However, sales were lower after adjusting for inflation.

U.S.-Gotta Bend Before You Can Break

Market sentiment decisively shifted to risk-off mode this week, as a stronger than expected print on CPI and a weak start to corporate earnings season helped cast further doubt on the economic outlook in financial news. At the time of writing, the S&P 500 is down 2% on the week and has now had one of the worst starts to a year in nearly a century. The deteriorating market sentiment led to a further widening in the yield curve inversion – highlighting the growing fear among market participants that a recession may be on the horizon. The 10Y-2Y spread now sits at -20 basis points (bps). The sour market sentiment also spilled over to commodity markets, with WTI down 8% to $98 per-barrel on the week.

Market sentiment decisively shifted to risk-off mode this week, as a stronger than expected print on CPI and a weak start to corporate earnings season helped cast further doubt on the economic outlook in financial news. At the time of writing, the S&P 500 is down 2% on the week and has now had one of the worst starts to a year in nearly a century. The deteriorating market sentiment led to a further widening in the yield curve inversion – highlighting the growing fear among market participants that a recession may be on the horizon. The 10Y-2Y spread now sits at -20 basis points (bps). The sour market sentiment also spilled over to commodity markets, with WTI down 8% to $98 per-barrel on the week.

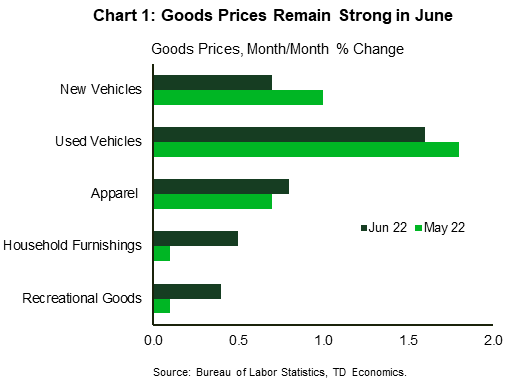

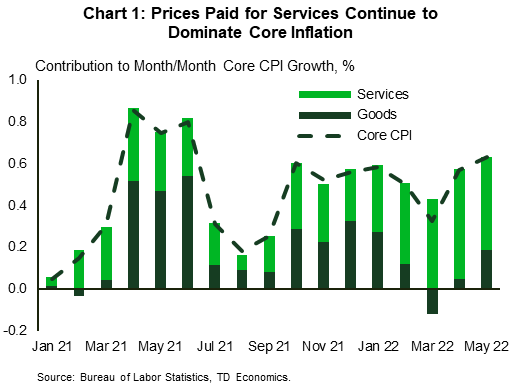

Any hopes of inflationary pressures easing in June were quickly dashed on Wednesday following the Bureau of Labor Statistics’ release of last month’s CPI data. Headline CPI accelerated by 1.3% month-on-month (m/m), pushing the year-ago measure to a new multidecade high of 9.1%. Indeed, with fuel prices having surged by 11% last month, and more recent gains in food prices showing incredible persistence, a further acceleration in the headline measure was inevitable. What was not anticipated, however, was the uptick in core inflation (0.7% m/m). Perhaps most disconcerting was the breadth in price gains across core, particularly among goods categories (Chart 1). Further gains in goods prices are at odds with more recent spending data, which has shown consumers pulling back on purchases of most discretionary goods in recent months. While inflation is notoriously a lagged indicator, it was thought that the combination of weakening demand and anecdotal reports of retailers carrying excess inventory would soon start to exert downward pressure on goods prices. That narrative has yet to come to fruition, and that detail will not be lost on policymakers when they meet later this month.

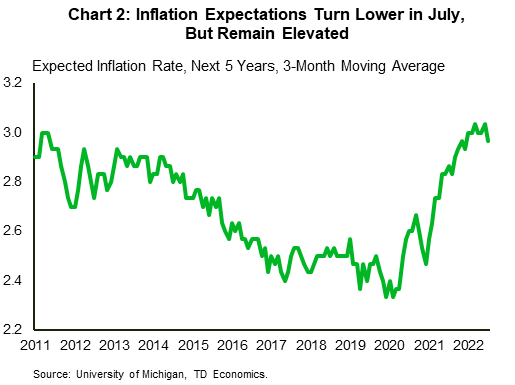

Perhaps one piece of encouraging news came from the July reading of the University of Michigan consumer confidence survey, which showed that expectations for inflation over the next five years now sit at 2.8% – down from last month’s reading of 3.1% (Chart 2). Chair Powell highlighted the recent upward drift in inflation expectations as being one of the key contributors in the FOMC’s decision to raise rates more forcefully in June. While the turn lower will provide some relief to policymakers, it won’t be enough to dissuade them from pushing ahead with another supersized hike later this month. This sentiment has been mirrored in market pricing, with odds a near coin toss on whether the Fed will raise by 75bps or 100bps.

Perhaps one piece of encouraging news came from the July reading of the University of Michigan consumer confidence survey, which showed that expectations for inflation over the next five years now sit at 2.8% – down from last month’s reading of 3.1% (Chart 2). Chair Powell highlighted the recent upward drift in inflation expectations as being one of the key contributors in the FOMC’s decision to raise rates more forcefully in June. While the turn lower will provide some relief to policymakers, it won’t be enough to dissuade them from pushing ahead with another supersized hike later this month. This sentiment has been mirrored in market pricing, with odds a near coin toss on whether the Fed will raise by 75bps or 100bps.

The big question now is to what extent higher interest rates will ultimately weigh on domestic demand in financial news. Retail sales data for June showed that consumers are remaining somewhat resilient, with both headline (1.0% m/m) and the control (0.8% m/m) up on the month. That said, consumer spending is only tracking around 1% q/q (annualized) for the second quarter, which is a marked slowdown from the 4.5% averaged through the second half of last year. With inflation continuing to erode purchasing power and rates expected to move decisively higher through year-end, the hope is that consumers will only bend under the weight of the dual-income shock and not completely break.

Thomas Feltmate, Director | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Featured Article: The Ingredients For A Happy Retirement

The Ingredients For A Happy Retirement

What are the ingredients for a happy retirement? (Photo by Bryn Colton)

What’s the difference between a happy retirement, and a not-so-happy retirement? Financial planners have the unique perspective of seeing many clients retire over time, and as such they can differentiate what creates a happy retirement for most people. While what makes someone happy is always subjective, there are some generalities that play out across many successful retirees.

Planning

While good planning doesn’t guarantee a happy retirement, it might help you to feel more prepared for retirement. Planning ahead, both financially and emotionally for a big change in your life can help you to deal with the stress of the upcoming change, leading to an easier transition.

Mindset

Retirees that seem the happiest are those retiring to something and not from something. If you’re retiring just to escape a work situation you don’t like, or because it feels like that is what you have to do, your retirement situation might be less than idea. If you’re retiring because you’re ready to put work aside and travel or spend more time with your family, you’re likely to have a better outcome in retirement and feel happier and more fulfilled. Having the right mindset and attitude is great first step in embracing retirement and ultimately, in feeling happier throughout your retirement years.

Surrounding Yourself With Loved Ones

Surrounding yourself with those that you love seems like an optimal way to have a happier retirement. Many retirees choose to spend more time with their families, but don’t discount the extra time that you might have to spend with your friends. You could also spend this time making new friends and broadening your social circle. Spending time with people you care about is one way to improve your mood, particularly during retirement when you have the extra time to devote to your social life.

Relaxation

Happy retirees balance out the fun things that they’re doing with additional rest and relaxation. After a long span of working, a bit of relaxation is natural, and finding out the rhythm that best fits your new lifestyle will result in your own happiness. Some retirees prefer to sleep in, or nap during the day, whereas another retiree may prefer to wake up early and use mindful meditate to relax. Whatever relaxation methods work best for you, incorporating additional rest and relaxation time into your retirement schedule may increase your happiness during these years.

Travel

Retirees and travel go hand in hand, and it can be a great way to spend your time during your retirement years. Seeing new places and experiencing new cultures can cause great happiness for some people, while others may prefer to stay home and travel within their own city or state. From weekend trips, to cruises, RV excursions or sailing, there’s plenty to experience in the world and exploring it with a renewed sense of adventure may bring you great happiness.

Prioritizing Health

Without prioritizing health, retirement may not last as long as you’d like. Putting your own health at the forefront, with exercise, healthy eating, and whatever stress reducing activities area meaningful to you, may not only improve your mood and happiness, but improve your life in general during retirement.

Giving Back

Giving back to others, either through volunteering, charity, or mentoring, can be an immensely positive experience that can bring great joy for retirees. Often, retirees may have wanted to spend time volunteering or mentoring during their career but haven’t had the time, and this time of life is an ideal time to get started. Helping others can certainly improve your own level of happiness.

Do More Of What You Love

Retirement is all about you, and doing what you love. So naturally, now is the time to do more of it. If fishing is your thing, and that is what brings you happiness, then spend more time fishing. If you’re a gardener, spend more time in the garden. Lean into what brings you happiness, especially during retirement.

To see more fantastic articles like this one, please see here.

Financial News for the Week of July 8th, 2022

Financial News Highlights

- Recession calls increased this week, but the job market begged to differ. The U.S. added 372k jobs in June, keeping the unemployment rate at its historic low of 3.6% and amplifying fears about inflation.

- In contrast, leading business indicators slipped modestly in June, while remaining above the 50 threshold, which suggests that both manufacturing and services sectors continue to expand.

- The FOMC minutes from the June meeting showed significant worries about the possibility that high inflation is becoming entrenched in consumer expectations. The Fed is positioned for another supersized rate hike at the end of the month.

U.S.-Job Gains Defy Recession Calls

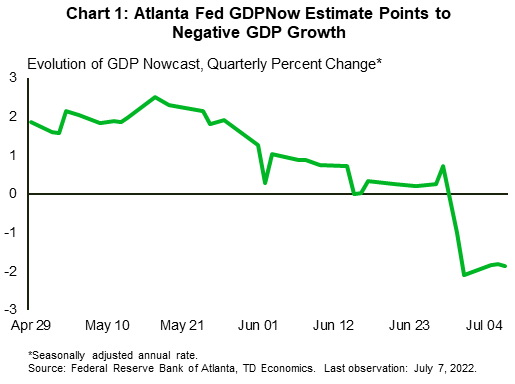

Recession became a much more popular word on the street this week in financial news. Revisions to first quarter GDP data and a weak spending report for May which came out at the end of last week revealed much softer consumer momentum in the first half of the year. This led many forecasters to downgrade their outlooks, with some calling for recession. TD Economics is not calling for a recession, but we acknowledge the downside risks have risen. As such, we have formulated an alternate economic profile on how a U.S. recession might unfold.

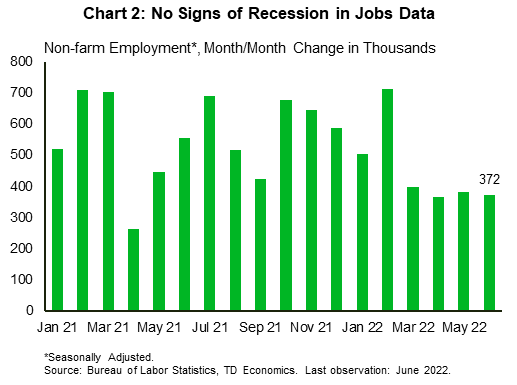

The Atlanta Fed’s GDP Nowcast is pointing to a second quarter of contraction in GDP in Q2 (Chart 1). However, two quarters of contraction in GDP is not enough to qualify as a recession according to NBER criteria – the economic body that defines recessions. In addition to economic output, it places a heavy importance on payrolls employment and real personal incomes less transfers. The income measure has certainly softened with high inflation in recent months but remains in expansionary territory. And the impressive June payrolls report confirmed that employment remained strong (Chart 2). The unemployment rate remained low at 3.6%, and average hourly wages were up a healthy 5.1% year-on-year, both pointing to tight labor market conditions.

Putting aside healthy hiring through June, sentiment indicators are showing some softness. The Institute for Supply Managements’ (ISM) readings for the manufacturing and services sectors both slipped modestly. However, both sectors remained above the 50 threshold, which suggests that both remained in expansionary territory. The underlying details paint a slightly more nuanced picture. Both sectors showed an increase in current business activity, but in the manufacturing sector, the new orders index slipped into contractionary territory, while in the services sector it eased but remained solidly expansionary.

Another important message of the ISM reports is that prices paid by businesses continue to ease – a trend that corresponds with a recent reduction in supply chain bottlenecks. Indeed, the supplier delivery times have improved since the beginning of the year, especially in the manufacturing sector. According to the San Francisco Fed’s research, the distribution of price gains as measured by core PCE inflation is equally split between supply and demand factors, suggesting that cooling on the supply side should help ease inflation going forward.

In the meantime, minutes from the FOMC meeting in June showed that members are worried about the level of stickiness in price gains, and the rising possibility that high inflation is becoming entrenched in consumers expectations. This fear clearly overshadowed any concern the members might have had about prospects for economic growth, resulting in a rare consensus when deciding to supersize the rate hike to 75 basis points. The Fed is positioned for another supersized rate hike at the end of the month, as it focuses on tempering demand.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of July 1st, 2022

Financial News Highlights

- Real personal consumption expenditures contracted in May, as consumers continue to tap excess savings.

- Indeed, in another sign that demand may be softening, core PCE inflation (that excludes food and energy) declined again to +4.7% year-over-year (y/y). Headline inflation (+6.4% y/y) continues to be supported by rising food and energy costs.

- The coming year will certainly pose economic challenges for emerging markets. However, there is still ample slack to be made up after the past two pandemic years that will provide a fillip to growth for many countries.

- Three shocks are the main drivers of the lower outlook for EMs: the spring lockdowns in China, the war in Ukraine, and the sanctions on the Russian economy.

U.S. -Consumers Cut Back As Prices at the Pump Surge

Cracks are starting to show in the U.S. economy in financial news. First quarter growth disappointed as the economy contracted for the three months to March. Despite the negative print, there was still reason to be optimistic given resilient consumer demand. Unfortunately, this fillip to growth is quickly fading.

The final release of the first quarter data this week showed that consumer spending was much weaker than realized at first blush. Personal consumption expenditures rose 1.8% (at a seasonally adjusted annual rate) in the first quarter, notably less than the 3.1% expansion reported in the prior release. Consumer services spending was notably weaker, having been marked down by 1.8 percentage points to 3.0%. Durables spending also registered a more tepid expansion of 5.9% relative to the 6.8% previously reported.

Most have expected that goods demand was set to lag as the economy reopened and people were able to travel, go out, and engage with the services sector. So, what is particularly worrisome about the report is the tepid growth in services demand. Indeed, May’s personal income and spending report looks like it reflects an extension of this trend. On a nominal basis spending registered + 0.2% month-over-month (m/m) but, with inflation at multi-decade highs, after price effects were stripped out the real consumption expenditures contracted 0.4% for the month. Worryingly, April’s growth was revised downward to 0.3% m/m from 0.7% prior.

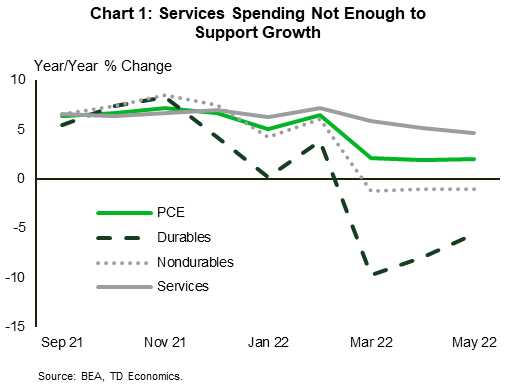

Ultimately this is coming about as the anticipated growth in services spending is not materializing to the extent required to offset the slowdown in goods spending (Chart 1). In May, real services expenditures grew by 0.3% (m/m) but were nowhere near enough to offset the 1.6% m/m contraction in goods purchases in financial news.

Indeed, in another sign that demand may be softening, core PCE inflation (that excludes food and energy) declined again to +4.7% year-over-year (y/y), after peaking at 5.3% in February. Unfortunately, headline inflation (6.4%) picked up and was underpinned by surging food prices and energy goods and services prices, which were up 11.0% and 35.8 % year-over-year respectively. The ongoing surge in the cost-of-living may already be forcing households to make tough choices on what to buy and what to forego, or at least rethink some discretionary purchases.

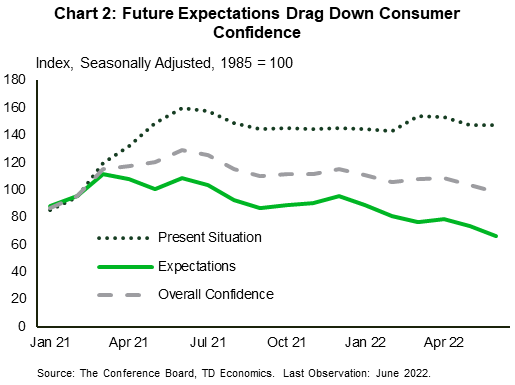

Going forward, the concern is that consumer sentiment continues to fall as inflation and rising interest rates dent disposable incomes and talk of recession raises anxieties. In June, the Conference Board’s measure of consumer confidence reached its lowest level since February 2021. The main culprit being the sustained decline in consumer expectations (Chart 2).

Households are facing a historic cost-of-living crunch. Moreover, given the broader context of high inflation, sagging consumer confidence, and a Fed that remains steadfast in tightening monetary conditions until inflation abates, consumer spending faces a slew of headwinds in the coming months.

Andrew Hencic, Senior Economist | 416-944-5307

Global- Emerging Market Outlook Dims

The skyrocketing food prices and interest rate hikes in advanced economies have raised bad memories of past stumbling blocks for emerging market (EM) economies. The coming year will certainly pose economic challenges, but there is still ample slack to be made up after the past two pandemic years that will provide a fillip to growth for many countries.

The skyrocketing food prices and interest rate hikes in advanced economies have raised bad memories of past stumbling blocks for emerging market (EM) economies. The coming year will certainly pose economic challenges, but there is still ample slack to be made up after the past two pandemic years that will provide a fillip to growth for many countries.

We have highlighted the risks to the outlook in our recent Quarterly Economic Forecast (link) and Question and Answer (link) publications. Broadly speaking, tighter financial conditions, slowing growth in advanced economies, the knock-on effects from the war in Ukraine, and China's commitment to Zero-COVID will all weigh on demand. Our outlook for emerging markets has been marked down to 3.2% in 2022 (from over 4% in our March outlook).

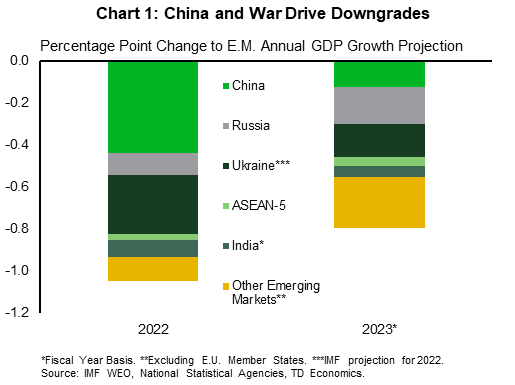

Three shocks are the main drivers of the lower outlook for EMs: the spring lockdowns in China, the war in Ukraine, and the sanctions on the Russian economy (Chart 1). Beyond that, the global economic landscape is shifting as growth in advanced economies slows – with anticipated knock-on effects for the rest of the world.

The war in Ukraine has kicked off another surge higher in energy prices. For most, higher energy prices act as a tax on households, eroding disposable incomes. Moreover, rising prices of key commodities (accompanied by the recent surge in the U.S. dollar) materially raise input costs for firms in import reliant markets.

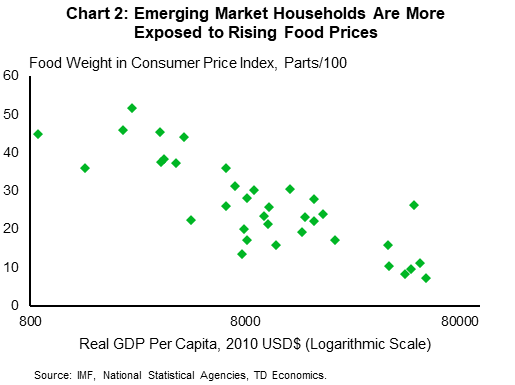

Food expenditures also make up a much larger share of the household expenditure basket in less developed nations than in advanced economies (Chart 2). Higher food prices will be reflected in more severe inflation, that indicates a rapid erosion in living standards and leaves less money available to purchase other goods and services.

Food expenditures also make up a much larger share of the household expenditure basket in less developed nations than in advanced economies (Chart 2). Higher food prices will be reflected in more severe inflation, that indicates a rapid erosion in living standards and leaves less money available to purchase other goods and services.

The increasingly downbeat outlook for China and the U.S. will bleed into total global demand. The two countries accounted for 13.9% and 8.5% of global merchandise imports, respectively, in 2019 and any slowdown in activity will trickle down through supply chains.

Financial conditions have also tightened as monetary authorities have been raising interest rates since 2021, in an effort to combat domestic inflation and stave off capital flight. As higher costs of capital feed through to the economy, the challenging conditions will leave vulnerable firms looking to secure liquidity.

Despite the landscape for emerging markets growing increasingly challenging in 2022 there is room for optimism as services spending resumes. Thailand, for example, saw tourist arrivals plummet from nearly four million in December 2019 to 520 thousand in May 2022. Moreover, if advanced economies execute a soft landing, the risks associated with a rapid tightening of financial conditions can be avoided.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Featured Article: To Find the Wines of Summer, Just Say Quaffable

Featured Article: To Find the Wines of Summer, Just Say Quaffable

Terms like ‘refreshing,’ ‘easy drinking,’ ‘crisp’ and ‘light’ have all been offered as synonyms. Our wine columnist dove deep into the category and came up with 5 categorically quaffable wines (also great values) to drink right now.

By

What does “quaffable” mean? When I went in search of a quaffable wine recently at Bogey’s Bottled Goods in Southold, N.Y., partner Zach Glassman met my request with a raised eyebrow. “ ‘Quaffing’ is such a fun word,” he said. “You don’t often hear such eloquence on Long Island!”

As a one-time resident of Long Island, I took the tiniest umbrage at Mr. Glassman’s response, but I understood what he meant. I love the words quaffing and quaffable. They are fun and capture the character of summer; to me, a quaffer is a wine that does the same. But while I’ve always found these to be useful descriptors, not everyone seems to agree. Often, retailers will translate “quaffable” to terms like “easy drinking” and “refreshing.”

Danny Roosevelt, head of purchasing at Parcelle Wine in New York City, told me he doesn’t consider “quaffer” a “customer-facing word.” In his view, it isn’t “universally meaningful.” Mr. Roosevelt might recommend a “light, refreshing red” or “crisp, salty white,” both of which he considers synonymous with quaffer.

He sent me his list of quaffing wines, red and white, from all over the world. One of his favorites is one of mine too: the 2020 Tiberio Trebbiano d’Abruzzo ($16). I already had a couple bottles at home, and I brought one to dinner at Divina Ristorante, my friend Mario Carlino’s (BYO) restaurant in Caldwell, N.J. “Quaffable?” Mario repeated when I described the wine. The native of Calabria, Italy, shook his head. I poured Mario a glass. He liked the wine but had his own words to describe it. “This is vinello leggero,” he said. Translation: light wine. It meant he considered the wine pleasantly drinkable, if somewhat cheap.

When I emailed Jason Jacobeit, co-proprietor of Somm Cellars in New York, to ask for his picks, he suggested a couple of village Chablis that “went down easy” and were “vividly fresh.” Two of his favorite producers, Charlène Pinson and Bernard Defaix, were priced a bit higher ($30 and $36, respectively) than my own favorite quaffing Chablis: the 2020 Gilbert Picq & ses Fils Chablis ($20), a fresh, lively and eminently drinkable wine from a producer who is also quite good, if somewhat underrated.

While Mr. Jacobeit’s fiscal sweet spot for quaffers was a bit higher than mine, Donna Garvey’s was more closely aligned. Ms. Garvey, a salesperson at Gary’s Wine & Marketplace in Wayne, N.J., does use the q-word when talking to customers, and she believes a quaffable wine shouldn’t cost more than $15. It should also be “universally likable” and taste good with or without food, in her view. I bought a couple of Ms. Garvey’s favorites and particularly liked her pick of the Gruet Brut Rosé ($15), a sparkling wine from New Mexico made mostly from Pinot Noir. A red berry-fruited Champagne-method wine, it’s a slightly frothy, just-dry-enough pink sparkler that is indeed suitable for drinking alone or pairing with food.

While the Gruet has broad distribution, some other $15 quaffers I tasted are a bit harder to find—but worth it. The 2021 Alkoomi Rosé ($12), from the Frankland River region in Western Australia, was dry yet wonderfully juicy. The 2020 Domaine de la Rosière Jongieux Blanc ($15), a white wine made in the Alpine Savoy region of France from the Jacquère grape, was pure mountain crispness.

While $15 is about as low as I typically go with a quaffer, Mr. Glassman at Bogey’s suggested an even cheaper wine: the 2021 Thresher Sauvignon Blanc ($10), from Chile. Marked by a pleasing sweet-tart flavor, it was mouthwateringly crisp and happily devoid of the herbaceous green notes that sometimes mar a cheap Sauvignon. It was so light-bodied it was better as an aperitif than as a food wine.

My friend Sue liked the Thresher Sauvignon Blanc for this very reason. “It’s a lot like water,” she said (something the Thresher winemaking team might not like to hear). She had her reservations about the word quaffer, however. “It sounds very King Henry the 8th,” said Sue, who is English herself and happened to be spot-on historically. An online etymology source I consulted said “quaff” dates back to the 16th century and originally meant “to drink or swallow in large draughts.”

Sue and I didn’t drink large draughts of any one quaffer, but we did try several, including reds from countries around the world. I don’t often think of red wines as quaffers—save, perhaps, for Lambrusco. The Lini 910 Labrusca Lambrusco Rosso ($18) from Emilia-Romagna is one of my summertime go-tos. Low in alcohol (11%), fruity but dry, it’s fizzy enough to be refreshing and substantial enough for food. I love it with barbecue.

A good quaffing wine isn’t the cheapest wine but rather a modest wine, well-made, from a good producer.

A couple of the reds recommended to me were a bit too much in terms of alcohol or tannins or oak to qualify as quaffable in my book. They just didn’t go down easily enough. A couple that did were produced from fairly obscure grapes. The soft and fruity 2020 Las Liebres Colonia Bonarda ($15) from Mendoza, Argentina, is made from the Bonarda grape (Mendoza’s other red grape besides Malbec). The 2020 Les Athlètes du Vin Grolleau ($20), a Loire Valley red made from the Grolleau grape, didn’t look much like a quaffer. The deep purple color suggested something tannic. But on the palate the wine was juicy and bright, and there was just a touch of earthiness behind the red-cherry fruit. And it was also low in alcohol (12.5%).

Another quaffing favorite came from the Rheinhessen region of Germany and the talented winemaker Florian Fauth. The 2020 Seehof Weissburgunder Trocken ($25), his most “basic” dry Pinot Blanc, is a wonderfully snappy white with an intense, even tangy mineral edge.

In the end, a fairly wide range of wines in our tasting qualified as what I’d define as quaffable. So how might you identify one when ordering in a restaurant? My friend Alan had an interesting answer. “They’re not at the bottom of the wine list,” he said. “They’re the next level up.”

That’s exactly it. A good quaffing wine isn’t the cheapest wine but rather a modest wine, well-made, from a good producer. Alan elaborated, and I couldn’t have said it better: “A quaffing wine is one you don’t really talk about, but you smile while you drink it.”

To see more fantastic articles like this one, please see here.

Financial News for the Week of June 24, 2022

Financial News Highlights

- Existing home sales fell 3.4% in May, extending the losing streak to four months. The months’ supply of inventory recorded an uptick, rising to 2.6. This was up from 2.2 months in April and 2.5 months in May of last year.

- New single-family home sales rose 10.7% in May but are still down 17% from the recent cyclical peak in December 2021.

- With little else on the data front, attention focused on Fed Chair Powell’s testimony in Congress. Powell characterized the Fed’s inflation fight as “unconditional”. Pressed on the likelihood of a recession, Powell reiterated that this was not the intended outcome, but that it was “certainly a possibility”.

U.S. -Changing Seasons

Fresh economic data was limited this short week, with financial markets closed on Monday for Juneteenth in financial news. Attention was focused on Powell’s testimony where he notably acknowledged the risk of recession, sending longer-term bond yields lower. So while summer may have officially kicked off this week, the economy may be a bit ahead of the curve, with the backdrop already featuring some falling leaves.

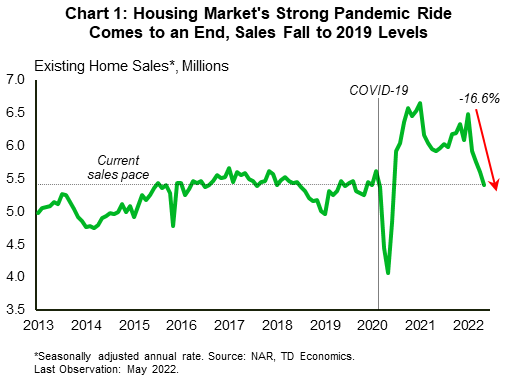

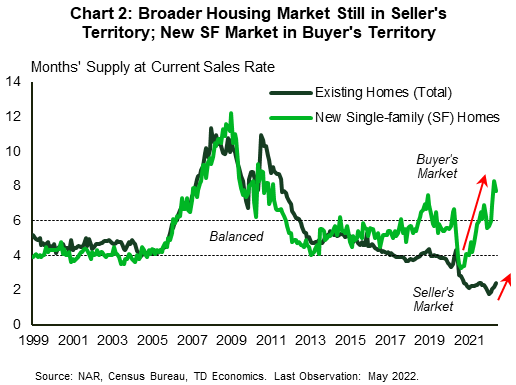

We did get an update on how the housing market was faring in the face of higher rates as of May. Existing home sales fell by 3.4%, stretching the string of declines to four months. After a solid ride during the pandemic, activity has fallen back to 2019 levels (Chart 1). With sales falling and inventories recording a small uptick, the months’ supply of inventory at the current sales rate has been edging higher. We’re not in balanced market territory yet, but the trend is slowly tilting toward it (Chart 2). Sales in the much smaller and more volatile new single-family home market regained some ground in May, but are still down 17% from their cyclical peak at the end of 2021. Led by gains in the South, new single-family housing inventory is piling up, rising to 444 thousand – the highest level outside of the 2005-06 housing boom period. This has brought this smaller segment of the housing market well into buyer’s territory (Chart 2).

The slump in housing demand is in large part a response to deteriorating affordability from the sharp increase in interest rates. Thirty-year mortgage rates are already near 6% – almost double their level at the start of the year, and a level not seen since 2008. The Fed is focused on bringing inflation down from its 40-year high with aggressive interest rate hikes. So it is unlikely that we’ll see any respite on the rates side anytime soon. As a result, we expect home sales to trend lower in the quarters ahead, while prices also likely to give back some of the recent gains starting later this year. A tight inventory backdrop will help limit some of the downside. Our latest home price forecast for East Coast States can be found here.

Fed Chair Powell testified before Congress this week and shared a similar view of the housing market: “Rate rises should impact house prices fairly quickly”. Powell’s testimony reconfirmed the Fed’s resolve to tackle inflation, calling the inflation fight “unconditional”. When pressed on the likelihood of a recession, Powell reiterated that this was not the intended outcome, but that it was “certainly a possibility”.

Recent Fed reports (see here and here) confirm that recession odds in the 1-2 years ahead have increased. What’s more, the Atlanta Fed’s GDP tracker (not an official forecast) points to 0% growth for a second quarter of this year, which would imply that that we may already be close to a technical recession. Our latest forecast also expects a sharp deceleration in economic activity and a modest increase in the unemployment rate in the year ahead, but it still points to decent growth of a little over 2% this year and 1.4% next. Still, there is indeed a very ‘Thin Margin for Error’. Whatever the outcome, autumn or a mild winter, one thing is for sure, the economy’s hot summer days have already passed.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Featured Article: 9 Under-the-Radar Vacation Spots in Europe

Where to beat inflation and crowds in Europe this summer? Here, 9 travel alternatives to the usual hot spots in Italy, France and Spain

So you missed your chance to travel too Venice, Paris and Barcelona without the crowds in the immediate aftermath of the pandemic’s early waves. Fret not. Here are nine alternative locales that promise to be relatively serene this summer even though tourism to Italy, France and Spain is expected to reach or exceed pre-Covid levels. And while inflation is also surging in Europe, the dollar is hovering near a five-year high against the euro, which means U.S. currency has more relative buying power in the Continent than in recent years. Steer off the Jet Set trail and toward one of these under-hyped spots and you’ll find serious bargains.

By

ITALY

The village of Comacchio in northern Italy’s Ferrara province.PHOTO: ALAMY

1. Ferrara: Renaissance art and ravioli

Three centuries of rule by the enlightened D’Este family left this city, tucked in the plains between Venice and Bologna, with an intriguing Renaissance legacy. To stroll through Ferrara is to step back in time. A good place to start is Trento e Trieste square, the city’s heart and home to Ferrara’s cathedral. From here it is a short walk to the city’s other highlights: the 14th-century Estense Castle, the Renaissance Palazzo dei Diamanti and the Via delle Volte, a winding, cobblestone alley that passes under vaults connecting buildings on each side. Don’t leave without trying Cappellacci di zucca (pumpkin-filled ravioli), a regional specialty. A 45-minute drive leads to Comacchio, a village with a network of canals much smaller but no less picturesque than Venice’s.

Italy’s Gran Sasso and Monti della Laga National Park in the Apennine Mountains, Abruzzo.The Canal du Midi in the Languedoc-Roussillon region of France, near the Spanish border.PHOTO: ALAMY

2. Gran Sasso and Monti della Laga National Park: Mountain pursuits

When “Italy” and “mountains” are used in the same sentence, the jagged Dolomites and the rest of the Alps tend to come to mind. But there are also the Apennines, which extend down the Italian peninsula for more than 700 miles, dividing the country in two. This national park just east of Rome is the ideal spot to explore Italy’s “other” mountains. A simple route to become one with nature here is to paddle a canoe down the Tirino River, reputedly Italy’s cleanest waterway. A cooperative called Il Bosso near the small town of Capestrano provides canoes and guides (reservations required). Travel to take your choice of nearby hikes: One leads to the top of the 9,550-foot Corno Grande, the highest peak in the continental Apennines.

On Marettimo, a small island off the coast of Sicily, one of the key pastimes is boating around grottoes.PHOTO: GETTY IMAGES

3. Marettimo: Secluded coves, translucent water

Hop on the hydrofoil in Trapani on Sicily and you’ll reach the island of Marettimo in just over an hour. At about 2 miles long and 3 miles wide, Marettimo offers salt-water-minded visitors limited options, most of which require a bathing suit. You’ll find no large beaches, but for a fee, locals will whisk you to one of the many secluded coves that can only be accessed by boat. Pastimes are simple: Snorkeling, scuba diving and boating around grottoes with translucent turquoise water. Or you can follow one of the many hiking trails in the island’s rocky, rugged interior.

FRANCE

Ile de Sein, among the most scenic of Brittany’s islands.PHOTO: ALAMY

1. The Brittany Coast: Elemental islands

The islands off Brittany’s shores in northwest France are hardly a secret, but they are plentiful and well spread out, which means that, even in July and August, visitors can avoid the summer crush (most of the time). Among the most scenic is petite Ile de Sein, travel only about 5 miles from the mainland. If you want to feel like you’ve reached Europe’s very edge, look no further. Another good choice is Saint-Malo, with its citadel and beaches that come and go with the tides. It’s considered a must-see, but the crowds can get intense (though not at the level of nearby Mont-Saint-Michel, farther up the coast in Normandy)

The Canal du Midi in the Languedoc-Roussillon region of France, near the Spanish border.PHOTO: ALAMY

2. Canal du Midi: Float around medieval villages

You can travel via barge down many canals in France, but this one in the southwest near the Spanish border is among the most picturesque. Along the way, you can stop to tour vineyards, bike along the path flanking the canal or visit medieval villages, prime among them the fortified town of Carcassonne. No license is required to pilot most of the barges. Or you can reserve a spot on a chartered barge with a captain, which removes some of the romance of floating freely down a 17th-century canal, but makes up for that with amenities.

Porte de Paris in the historic core of Lille. Ten miles from the border of northern Belgium, the city blends French and Flemish cultures.PHOTO: ALAMY

3. Lille: Beer and antiques

Blending French and Flemish cultures, this former industrial city, travel about 10 miles from the border of northern Belgium exudes a vibe you won’t find elsewhere in France. The colorful facades on many buildings in the city’s historic core will make you think you’ve crossed the border, as will one of Lille’s signature dishes—the distinctly Belgium classic moules-frites (steamed mussels and french fries). Beer and waffles also play a starring role, another reminder you could easily zip up to Belgium. The crowd-averse will want to ensure they leave Lille before the first weekend of September when the city is overwhelmed by the hordes arriving for the braderie,said to be the largest annual flea market in Europe. More social sorts will want to linger and be swept up in the pulsating energy surrounding the innumerable stalls, selling everything from vintage doorknobs to silverware dating back to the French Revolution.

SPAIN

Spain’s Cuenca, a 90-minute drive east of Madrid, seems to cling to the side of a steep rock face.PHOTO: ALAMY

1. Cuenca: Moorish relics, abstract art

This city, a 90-minute drive east of Madrid, offers a window onto Spain’s past that many foreigners miss, despite the vicinity to the capital. From a distance, Cuenca’s buildings, seemingly hanging precariously to the side of a steep rock face, recall Medieval towns in central and southern Italy. But as you get closer you see the added Spanish touches, including the Moorish architecture that mixes European and North African. A walk across the Saint Paul Bridge, which spans the gorge, will give you an appreciation for the prowess of the architects and engineers who built this town centuries ago. One of the best places to observe the bridge is from the nearby Spanish Museum of Abstract Art, which has works from the second half of the 20th Century. An excellent travel destination for the family!

Galicia’s Playa de las Catedrales (Beach of the Cathedrals).PHOTO: GETTY IMAGES

2. Galicia: Wild beaches, great gardens

This region in northwest Spain is famous for its capital city, Santiago de Compostela, the arrival point of the Camino de Santiago, an ancient pilgrim route that covers 500 miles between it and the French border. Lesser known is Galicia’s varied coastline, marked by rock formations that plunge into the sea and secluded beaches that lend themselves to long walks. Playa de las Catedrales is among the most popular spots on the coast thanks to the rock formations that inspired the name. Come at low tide to pass under the natural stone arches on the beach or high tide to watch from above as the waves crash against the rocks. A perfect travel location!

The fortified town of Girona, one of the filming locations for HBO’s ‘Game of Thrones.’PHOTO: ALAMY

3. Girona: Ancient architecture, seaside glamour

A 40-minute train ride from Barcelona, Girona is a walled medieval town covered in cobblestone streets and so eerily atmospheric that it was used as a set in the HBO series “Game of Thrones.” You’ll want to spend a day or two just wandering slowly by foot. Among the chief highlights is the Jewish quarter, one of the best-preserved in Europe, with restored buildings, narrow alleyways and arches dating to before 1492 when the Spanish monarchs expelled the Jews from the country. Girona also makes a good base for exploring the region since it’s just 45 minutes or less by car from beach resorts on the Costa Brava and less than an hour from the French border.

The Wall Street Journal is not compensated by retailers listed in its articles as outlets for products. Listed retailers frequently are not the sole retail outlets.

For more reading please click here.

Financial News for the Week of June 10, 2022

Financial News Highlights

- U.S. CPI came in above expectations, with the headline reading reaching a new 40-year high. Core inflation also surprised with a broad-based acceleration.

- The U.S. trade deficit narrowed in April with both lower U.S. imports and rising exports contributing. We expect further narrowing will add to GDP growth in the second quarter.

- Meanwhile, consumer credit made bad headlines this week, but as long as household income stays on the rise, credit growth should remain sustainable.

U.S. - The Good, the Bad and the Ugly

Market anticipation built through the week for Friday’s CPI data release. Inflation came in above expectations and markets reacted by ratcheting up their expectations for rate hikes. Financial markets have now priced in three consecutive 50 basis-point hikes, starting with next Wednesday’s FOMC decision. The 10-Year Treasury yield jumped seven basis points on the news, finishing the week 18 basis points higher at 3.11% (at the time of writing). Equity markets’ timid attempts to regain their footing early in the week came crashing down Friday, as Thursday’s sell-off intensified.

Indeed, “ugly” seems like an appropriate epithet for May’s CPI print. Energy prices pushed the headline print to a new 40-year high. Since May, the nationwide average retail gasoline price has continued to rise and is likely to reach $5 per gallon in the coming days. This will keep the headline reading elevated in June. Food prices also continued to accelerate, adding to the headline print.

Excluding energy and food, May’s month-on-month core inflation matched the April’s reading. What came as a surprise was an acceleration in core goods inflation. In turn, core services inflation, which tends to be stickier and less volatile, decelerated only slightly remaining above last year’s average (Chart 1). This suggest that core inflation – the main yardstick for monetary policy– is not coming down to a level the Fed would like it to be at any time soon. What’s needed is a further easing in demand, particularly for goods, to lower price pressures. Since some retailers are starting to discount their merchandise in the wake of excessive inventories, we expect pressures there to ease in the coming months.

Some good news came from trade data. The U.S. trade deficit narrowed in April to $87.1 from a record of $107.7 billion in March. Over the past two years demand for imported goods outweighed the value of American exports, contributing to a significant wedge in the trade balance, but this week’s report delivered a snapback, providing some evidence of declining demand for imported items. Meanwhile, exports of goods and services expanded. Trade data is quite volatile and it’s possible to see it zag after the current zig, but we think the recent report portends a reversal of the two-year trend, and we will see the gap narrowing further, adding to GDP growth in the second quarter.

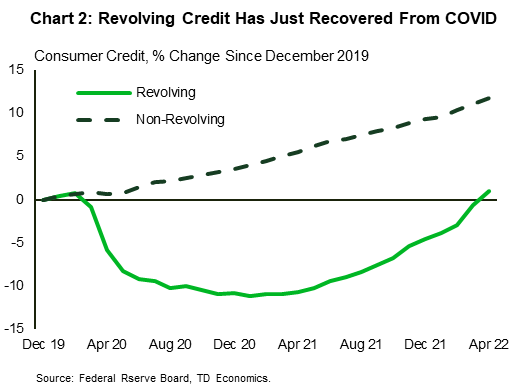

Meanwhile, consumer credit made bad headlines this week as it expanded by $38.1 billion in April after an already sizeable increase in March. This increase suggests that consumers are relying more on credit for their purchases, which could become a burden should they face trouble repaying this debt. Zooming in on details, however, much of this growth was due to an acceleration in revolving credit, which has only just recovered to its prepandemic level(Chart 2). This conincides with a normalization in spending on discretionary services, such as in-person entertainment and travel, which are usually financed by revolving credit, such as credit cards. As long as household income stays on the rise, credit growth should remain sustainable.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.