Financial News for the Week of September 22nd, 2023

Financial News Highlights

- The Federal Reserve held rates unchanged at its September meeting, but updated projections showed that the median FOMC member expects rates to remain above 5% through 2024, reinforcing the higher for longer message in financial news.

- The economy is likely to feel some drag from the UAW strike, which announced additional action at 38 parts and distribution facilities across 20 states, as contract negotiations continue to progress slowly.

- The theme of “higher-for-longer” had pushed mortgage rates higher, which weighed on both homebuilding activity and existing home sales in August.

Higher for Longer

Over the past eighteen months the Federal Reserve has raised interest rates eleven times, bringing the policy rate 5¼ percentage points (ppts) higher in today's financial news. On Wednesday, the FOMC opted to hold rates steady for the second time in the past three meetings, as it fine-tunes its approach to the level it deems sufficiently restrictive to return price stability to the economy. The Fed adopted the same policy decision it implemented in June - a hawkish pause if you will - indicating their expectation that one further rate hike is in the cards for 2023. In response, Treasury yields jumped to their highest level since 2007, with the ten-year yield rising by 12 basis points (bps) on the week to 4.4%, while equities fell with the S&P 500 down 2.3% as of the time of writing.

Over the past eighteen months the Federal Reserve has raised interest rates eleven times, bringing the policy rate 5¼ percentage points (ppts) higher in today's financial news. On Wednesday, the FOMC opted to hold rates steady for the second time in the past three meetings, as it fine-tunes its approach to the level it deems sufficiently restrictive to return price stability to the economy. The Fed adopted the same policy decision it implemented in June - a hawkish pause if you will - indicating their expectation that one further rate hike is in the cards for 2023. In response, Treasury yields jumped to their highest level since 2007, with the ten-year yield rising by 12 basis points (bps) on the week to 4.4%, while equities fell with the S&P 500 down 2.3% as of the time of writing.

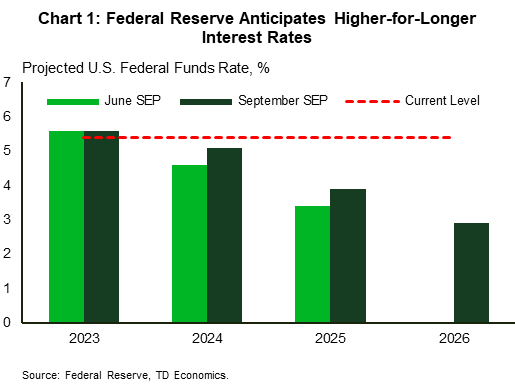

Accompanying the FOMC decision on Wednesday, the updated summary of economic projections (SEP) showed that the median FOMC member is projecting a de-facto soft landing for the U.S. economy. The median member expects the unemployment rate to rise only 0.3ppts by the end of next year. For reference, the U.S. unemployment rate just rose by 0.3ppts in August alone in financial news. The Fed’s expectation that inflation will be at 2.5% by the end of 2024 remained unchanged. However, the number of rate cuts for next year was pulled in, with the median FOMC member expecting the policy rate to be only 25bps below the current level at the end of 2024 - 50 basis points higher than in the June SEP (Chart 1). While these projections are decidedly hawkish, Chair Powell continued to emphasize that the Fed’s future decisions will depend on incoming data and its implications for the trajectory of inflation.

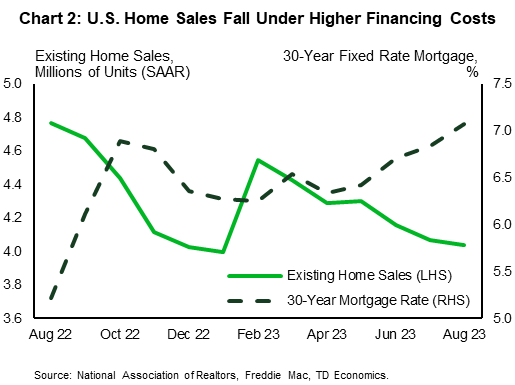

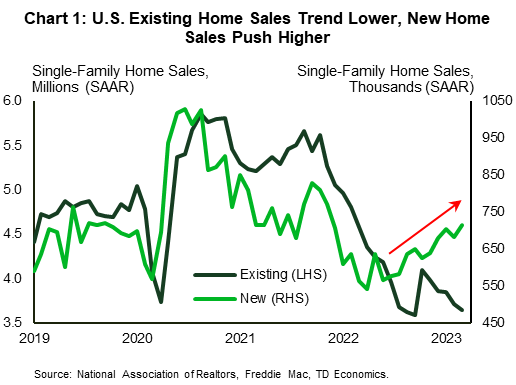

On that front, we saw in the housing data released this week that the interest rate sensitive sector continues to feel the strain of higher rates, as homebuilding activity faltered in August on slowing demand for new homes. With mortgage rates back above 7%, a similar curtailment of demand was seen in existing home sales in August, which declined for a third consecutive month (Chart 2). Price growth, however, has continued to push higher, as the highest mortgage rates in 22 years has left many would-be sellers locked-in to their lower rates, limiting resale supply. This dynamic is being monitored by the Fed but is unlikely to influence monetary policy discussions due to the lagged and proxied measurement of shelter costs in the CPI and PCE indexes.

On that front, we saw in the housing data released this week that the interest rate sensitive sector continues to feel the strain of higher rates, as homebuilding activity faltered in August on slowing demand for new homes. With mortgage rates back above 7%, a similar curtailment of demand was seen in existing home sales in August, which declined for a third consecutive month (Chart 2). Price growth, however, has continued to push higher, as the highest mortgage rates in 22 years has left many would-be sellers locked-in to their lower rates, limiting resale supply. This dynamic is being monitored by the Fed but is unlikely to influence monetary policy discussions due to the lagged and proxied measurement of shelter costs in the CPI and PCE indexes.

Looking ahead, there is no shortage of upcoming events that will be on the Federal Reserve’s radar. This includes the UAW strike, which was extended to an additional 38 parts and distribution facilities this morning as negotiations continue to progress slowly. In the most recent round of strike action, the UAW has targeted General Motors and Stellantis, citing negotiation progress with Ford as the reason for the company’s exclusion. This is expected to create additional disruptions on top of the roughly 7.5% hit to U.S. production stemming from the first round of strike action. Also on the horizon is a looming shutdown of the federal government, with only a few days left before the October 1st deadline. Adding to the impacts expected from the end of the moratorium on student debt repayment, it is clear that the Federal Reserve’s data-dependency approach is set to become more challenging over the near-term.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Featured Article: Changes Are Coming to Medicare Drug Costs. What It Means for You.

Please enjoy this educational article from Barron's

Medicare’s first round of drug price negotiations has begun, and while that should be a boon to enrollees, you will have to wait a couple of years to reap the benefits. In the meantime, there are other important changes to medication costs on the way—and steps to take right now to lower the amount you’re spending on prescription drugs.

Last month, the U.S. Department of Health and Human Services announced the first 10 drugs selected for price negotiation under the Inflation Reduction Act of 2022. The law gave Medicare the power to negotiate drug prices directly with pharmaceutical companies for the first time. Previously, the federal government was prohibited from leveraging its bargaining power to lower prices for beneficiaries.

“This is just a huge, historic change,” says Leigh Purvis, prescription drug policy principal in the AARP Public Policy Institute.

The 10 drugs in the first round were among those that Medicare Part D spends the most money on and include treatments for diabetes, heart failure, and blood cancer. In 2022, nine million Medicare Part D enrollees took the 10 drugs and paid a total of $3.4 billion in out-of-pocket costs on them, according to the Department of Health and Human Services.

New, negotiated prices for the first 10 drugs are set to take effect in 2026. Other medications are expected to follow: The Centers for Medicare and Medicaid Services will select up to 15 additional Part D drugs for negotiation in 2027, up to 15 more drugs for 2028 (including drugs covered under Parts B and D), and up to 20 more drugs for each year after that. The pharmaceutical industry has mounted a legal challenge to the plan.

All Medicare recipients stand to benefit from reduced prices on these drugs, Purvis says. That’s because Part D premiums reflect total costs borne by the plans, and to the extent that negotiations lower those costs, savings will trickle down to enrollees in the form of lower premiums, she says.

Price negotiations are one of several provisions in the Inflation Reduction Act designed to lower prescription drug costs for Medicare patients. Monthly out-of-pocket costs for insulin were capped at $35 this year. Starting next year, those with high drug spending will catch a break when their responsibility in the catastrophic coverage phase of Part D—which beneficiaries reach after spending roughly $3,000 out of pocket, Purvis says—will drop from 5% coinsurance to zero. Then, in 2025, out-of-pocket spending on medications will be capped at $2,000 annually, indexed for inflation going forward.

Beyond these measures, beneficiaries can take advantage of Medicare’s annual open enrollment period to re-evaluate their drug coverage and make sure it’s still the best option. From Oct. 15 through Dec. 7, beneficiaries can switch Part D plans, Medicare Advantage plans, or switch from Medicare Advantage to original Medicare or vice versa. Any changes made to coverage during this period will take effect Jan. 1, 2024.

Drug plans sometimes make changes to which drugs they cover, so if your plan no longer pays for your medication—or has moved it to a more expensive coverage tier—then it may make sense to find a different plan.

To see more fantastic articles like this one, please see here.

Financial News for the Week of September 15th, 2023

Financial News Highlights

- The third quarter is shaping up to be the strongest of the year for the U.S. economy, with GDP tracking 3.7% q/q (annualized).

- The August reading of CPI showed inflationary pressures accelerated last month, though the trend remains favorable, with the three-month annualized change on core inflation slipping to 2.4%.

- A 1-2-3 punch of risks lies on the horizon for the U.S. economy. The end of the student debt moratorium, a potential government shutdown, and the UAW strike could all leave a mark on Q4 growth.

Flying High in Q3, But Headwinds on the Horizon

There were a lot of new data reads on the U.S. economy this week in financial news, but on balance it is looking like the third quarter is shaping up to be the strongest of the year. Real GDP growth is on track for a nearly 4% q/q (annualized) pace! That performance is driven by defiant consumer spending, which is also close to 4% even though August retail sales weren’t much to write home about. The tradeoff, however, is that persistently higher demand undermines the Fed’s efforts to cool inflation. That was evident in the August CPI data, where both headline and core inflation accelerated relative to July.

There were a lot of new data reads on the U.S. economy this week in financial news, but on balance it is looking like the third quarter is shaping up to be the strongest of the year. Real GDP growth is on track for a nearly 4% q/q (annualized) pace! That performance is driven by defiant consumer spending, which is also close to 4% even though August retail sales weren’t much to write home about. The tradeoff, however, is that persistently higher demand undermines the Fed’s efforts to cool inflation. That was evident in the August CPI data, where both headline and core inflation accelerated relative to July.

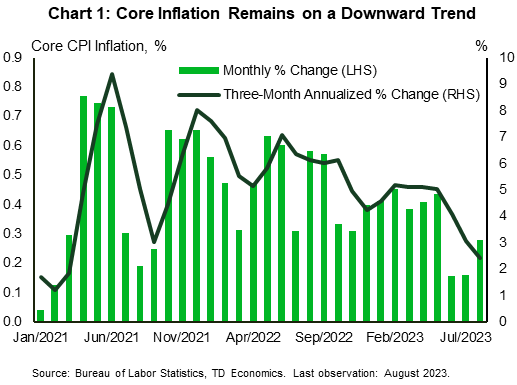

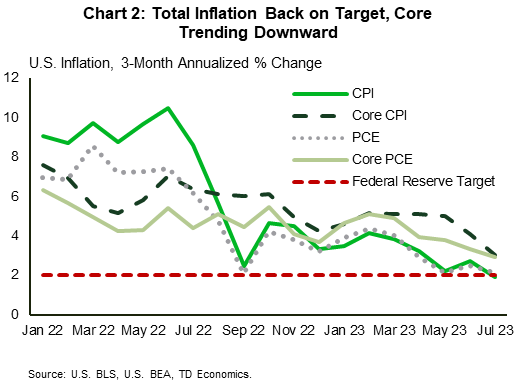

Over half of the gain in headline inflation was due to higher gasoline prices, which rose sharply alongside the recent uptick in oil prices. Meanwhile, the 0.3% m/m gain in core inflation came in a tick above expectations and bucked the trend from the ‘soft’ 0.2% gains seen in both June and July (Chart 1). However, putting these numbers in context, the monthly gain was still the third smallest in nearly two-years. Moreover, the trend on inflation remains favorable, with the three-month annualized pace cooling to 2.4% – the slowest pace of growth since March 2021.

Next week’s interest rate announcement hangs in the balance, where it is widely expected that the Federal Reserve will keep the policy rate unchanged. However, the devil will be in the details. The FOMC will also release revised economic projections, where at a minimum, they’re likely to lift the near-term growth forecast and lower the unemployment rate projection to account for the more persistent strength since the June update. The big question will be if policymakers see the near-term resilience as a source of more persistent inflationary pressures, and whether that alters the expected future path of the fed funds rate. While it is very unlikely that the FOMC would lift its terminal rate projection of 5.75% for 2023, a shallower rate cut trajectory could be signaled, reinforcing the need for rates to remain higher for longer.

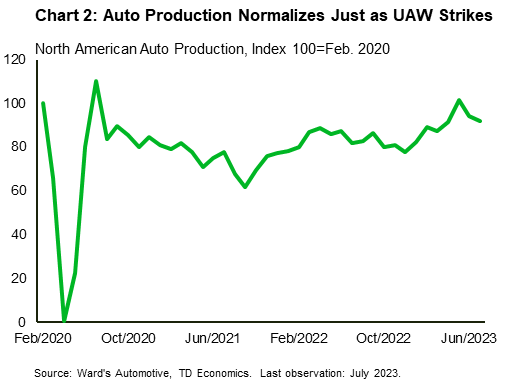

The Fed needs to thread a very small needle in its communication next week in major financial news. While policymakers will need to show a continued commitment to fight inflation, coming off too hawkish runs the risk of leading to an over tightening in financial conditions. This is particularly crucial now, as there is a trifecta of headwinds to fourth quarter growth on the horizon: the end of the student debt moratorium, a potential government shutdown, and the United Auto Workers (UAW) strike. The UAW strike, which began Thursday evening, comes just as auto production had normalized to pre-pandemic levels (Chart 2). As it currently stands, the UAW has announced work stoppages at three facilities, accounting for about 7.5% of overall U.S. production. Assuming no other stoppages, this alone would shave about 0.025 percentage points (pp) for each week the strike lasts. The hit from a government shutdown is a multiple of that, while the impact of the end of the student debt moratorium could have a cumulative Q4 hit of 0.3pp. So, while growth is flying high in the third quarter, there’s the potential it ends 2023 with a thud!

The Fed needs to thread a very small needle in its communication next week in major financial news. While policymakers will need to show a continued commitment to fight inflation, coming off too hawkish runs the risk of leading to an over tightening in financial conditions. This is particularly crucial now, as there is a trifecta of headwinds to fourth quarter growth on the horizon: the end of the student debt moratorium, a potential government shutdown, and the United Auto Workers (UAW) strike. The UAW strike, which began Thursday evening, comes just as auto production had normalized to pre-pandemic levels (Chart 2). As it currently stands, the UAW has announced work stoppages at three facilities, accounting for about 7.5% of overall U.S. production. Assuming no other stoppages, this alone would shave about 0.025 percentage points (pp) for each week the strike lasts. The hit from a government shutdown is a multiple of that, while the impact of the end of the student debt moratorium could have a cumulative Q4 hit of 0.3pp. So, while growth is flying high in the third quarter, there’s the potential it ends 2023 with a thud!

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 8th, 2023

Financial News Highlights

- Hard economic data was thin on the ground over the Labor Day shortened week, with survey indicators and Fed speakers grabbing attention.

- A slew of Federal Reserve speakers hint that the central bank may skip a rate hike at the next meeting, as the Beige Book (the Fed’s survey of economic conditions) suggests that the economy closed out the summer on a modest note.

- Oil markets were also on the move, after Saudi & Russian supply cuts were extended. Higher energy prices are a challenge to the needed cooling in inflation.

Higher for Longer Seems Surer

Hard economic data was thin on the ground over the Labor Day shortened week, with survey indicators and Fed speakers the main highlights on the calendar in financial news. Crude oil markets were also a bit livelier after Saudi Arabia and Russia both announced extensions to their supply cuts through to the end of the year.

Hard economic data was thin on the ground over the Labor Day shortened week, with survey indicators and Fed speakers the main highlights on the calendar in financial news. Crude oil markets were also a bit livelier after Saudi Arabia and Russia both announced extensions to their supply cuts through to the end of the year.

Since July, Saudi Arabia has voluntary removed 1 million barrels per day (b/d) of crude from global oil markets. While the measure was cited to be temporary, it was already extended to September, with this week’s announcement extending it once again. Russia added their own export reduction of 300,000 b/d. On the day of the announcement, Brent crude, the international benchmark, rose 1.2% to close at $90.04 – exceeding $90 a barrel for the first time this year (Chart 1). Prices have since given back some of the gain, but the general move higher in oil prices over the past few weeks is likely to threaten efforts to tame inflation.

On that front, this week featured a full roster of Fed speakers. Governor Waller was also in the news making more dovish than usual statements. He noted that data showing a cooling job market meant the Fed should “proceed carefully”, and does not necessitate an imminent rate hike. Bostic echoed these sentiments. Logan noted that it could be appropriate’ to skip an interest-rate increase in September. Williams left whether the Fed would hike again as an open question, while Goolsbee, hinting at a higher for longer stance, sees a “golden opportunity” for the Fed to tame inflation without triggering a recession. All speakers emphasized that the Fed will be paying close attention to the data.

The Fed’s latest survey of economic conditions, the Beige Book, noted that the U.S. economy grew at a modest pace during July and August, relative to slight growth in the previous report. This was bolstered by a final bout of pent-up demand for leisure activities. Outside of leisure travel and a rise in auto sales due to better inventory, nonessential retail sales slowed in financial news. Job growth was generally subdued nationwide with wage growth elevated but expected to moderate in the months ahead. Prices for consumer goods fell faster than in many other categories. Demand for manufactured goods waned while the supply constrained single-family housing market continued to be challenged by higher financing costs and rising insurance premiums.

The Fed’s latest survey of economic conditions, the Beige Book, noted that the U.S. economy grew at a modest pace during July and August, relative to slight growth in the previous report. This was bolstered by a final bout of pent-up demand for leisure activities. Outside of leisure travel and a rise in auto sales due to better inventory, nonessential retail sales slowed in financial news. Job growth was generally subdued nationwide with wage growth elevated but expected to moderate in the months ahead. Prices for consumer goods fell faster than in many other categories. Demand for manufactured goods waned while the supply constrained single-family housing market continued to be challenged by higher financing costs and rising insurance premiums.

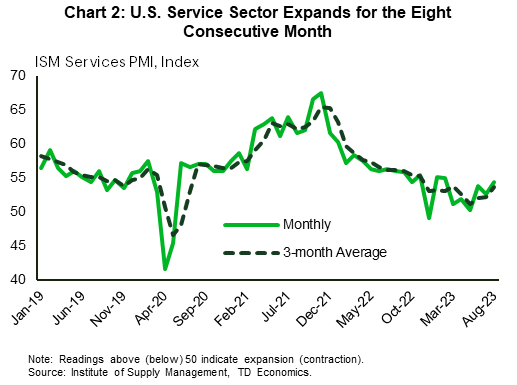

The ISM services index surprised to the upside this week, reaching a six-month high of 54.5 in August (Chart 2). The survey continued to highlight a service sector that is still in expansion mode, with survey respondents expressing positive sentiments about business and economic conditions. Beneath the headline, the positive details were an increase in business activity (+0.2 pts), new orders (+2.5 pts), and employment (+4.0 pts).

The tone of the economic news this week is likely to keep policymakers in a wait and see mode. Consumers are keeping the service sector humming along, even as the labor market cools. All good news for the Fed, but higher energy prices remain a wildcard that will require close monitoring so as not to undo the progress on inflation thus far.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 1st, 2023

Financial News Highlights

- The U.S. economy added 187k jobs in August, but revisions to the two prior months subtracted a notable 110k jobs from the previous reported tally.

- Both total and core PCE inflation rose by 0.2% month-on-month in July, equal to the monthly change seen in June for both measures.

- Hurricane Idalia, the first of the season to make landfall in the U.S., caused widespread flooding and wind damage through Florida’s Big Bend region and up through Georgia and the Carolinas.

The Labor Market Takes a Holiday

The U.S. almost managed to escape August without a major hurricane, but unfortunately those hopes were dashed when Hurricane Idalia made landfall as a category 3 hurricane on Wednesday in Florida in non financial news. Strong winds, rain, and storm surges caused widespread flooding and property damage, leaving hundreds of thousands of Americans without power across the Southeast. Although the extent of the damage is still being assessed, insurance and clean-up costs are expected to be well over a billion dollars.

Fortunately for the national economy, sunnier skies could be found in this week’s economic data, including the 187k new jobs added in August. While this reading, in addition to the downward revisions to the previous two months, marks a continued moderation in the pace of hiring, it indicates that supply and demand in the labor market are coming into a more sustainable alignment (Chart 1). This was further evidenced by the decline in job openings in July, with the job opening to unemployed ratio falling to 1.5 in financial news. While the unemployment rate did rise to 3.8%, this mostly resulted from a boost in labor force growth which could be considered a net positive if it helps to offset labor shortages. On aggregate, this progress will come as positive news for the Federal Reserve, however the most recent data on inflation was slightly more mixed.

On Thursday, we saw that PCE inflation rose by 3.3% year-on-year (y/y) in July, up from 3.0% in June. This was driven by a moderation in the negative base effects resulting from the spike in energy prices last year in addition to a moderate uptick in services inflation – driven entirely by Powell’s ‘supercore’ component. Looking at the 3-month annualized trend (Chart 2),  we can see that total inflation is pushing closer to the Fed’s 2% target, though this is likely to be short lived given the recent move up in energy prices. In addition, while core inflation is moving in the right direction, non-housing core services have barely budged from their cyclical highs and continue to run at an elevated annualized pace. Until we see a meaningful cooling here, core inflation will likely remain north of 3%.

we can see that total inflation is pushing closer to the Fed’s 2% target, though this is likely to be short lived given the recent move up in energy prices. In addition, while core inflation is moving in the right direction, non-housing core services have barely budged from their cyclical highs and continue to run at an elevated annualized pace. Until we see a meaningful cooling here, core inflation will likely remain north of 3%.

Some offset to inflationary pressures continues to be provided by the goods sector, with the ISM Manufacturing Purchasing Managers’ Index (PMI) showing manufacturing activity contracted for a tenth consecutive month in August. Ten out of sixteen industries reported lower input prices, which is likely factoring in downstream to the consumer. Price growth in the services sector has been more stubborn, so next week’s update on the ISM Services PMI will offer insight into how resilient the sector remains.

With the Labor Day holiday on Monday, next week will be short both in length and in the volume of economic data that we receive. However, the release of the Fed’s Beige Book will be one item to watch, as it will feed into the viewpoints that FOMC members bring to the upcoming meeting. We expect that the progress on inflation and job market cooling up to this point will be sufficient to warrant a hold in 2 weeks’ time, but the tone will likely remain hawkish to guard against the potential for pre-mature easing in financial conditions.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of August 25th, 2023

Financial News Highlights

- Speaking at the Jackson Hole Economic Symposium on Friday, Chair Powell noted that some progress had been made on the inflation front, but that inflation was still “too high”. He noted that the Fed would proceed carefully in either tightening the policy rate further or holding it constant as it watches the data.

- Existing home sales were one piece of data reacting strongly to higher rates, falling further in July. Inventories remained lean, at 42% below pre-pandemic levels.

- Lack of supply in the existing market continues to push buyers to the new market, with sales there up strongly in July.

Fed Chair Powell Sticks to Tough Talk

In a relatively quiet economic data week, markets took their cue from Chair Powell’s Jackson Hole Economic Symposium speech in financial news. The annual speech is always a highly anticipated event, but this year’s was particularly important with the Fed being at a monetary policy pivot point. The speech struck a balance between acknowledging that some progress had been made on inflation, but that it remained “too high” with substantial ground to cover to get back to price stability. Equity and bond markets didn’t like this reminder and were down on Friday (at time of writing).

The Chair noted the FOMC was prepared to “raise rates further if appropriate”, and that it intended to hold policy at a restrictive level until confident that inflation was moving sustainably down toward its objective (see commentary). However, given that they are navigating in a cloudy environment, they would proceed “carefully”. What appeared to be off the table was any indication of potentially lowering rates, thus giving the speech a more hawkish tilt in our view. We believe that the continuation of this tough talk is necessary to prevent an undesirable give back in bond yields and, ultimately, to help keep inflationary expectations in check as it continues to monitor the data closely (see here).

Powell provided a little more detail into the factors that will go into policymaking by breaking down inflation into three key categories. This included core goods inflation, along with housing and non-housing services. He noted progress on all three. On non-housing services – a category also known as “supercore”, which accounts for over half of the core PCE index – annual inflation has moved mostly sideways, but encouragingly it has started to decline on a three and six-month basis. Meanwhile, housing services inflation is expected to continue to ease given well-known lags (see here), but they will be watching market rent data closely.

Speaking of housing, existing home sales continued to head lower in July (see commentary). With mortgage rates some 40 basis points higher than in the two months prior it is no wonder that activity pulled back. The elevated rate environment also poses a hurdle on the supply side, as existing homeowners with much lower mortgage rates are reluctant to move and take on a higher rate. This theme is evident in inventories, which were 42% lower than pre-pandemic July levels (July 2019).

Speaking of housing, existing home sales continued to head lower in July (see commentary). With mortgage rates some 40 basis points higher than in the two months prior it is no wonder that activity pulled back. The elevated rate environment also poses a hurdle on the supply side, as existing homeowners with much lower mortgage rates are reluctant to move and take on a higher rate. This theme is evident in inventories, which were 42% lower than pre-pandemic July levels (July 2019).

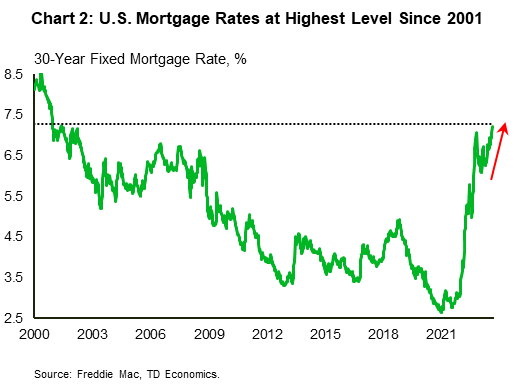

The tightness in resale market has kept a floor on home prices, while also pushing more would-be buyers to the “new” home market. New single-family home sales continue to buck the broader negative trend, making additional gains in July (Chart 1). This has been much to the delight of homebuilders, who have looked to boost supply in the single-family sector in financial news. While this trend may have some more room to run, mortgage rates have pushed even higher recently and are now hovering in the 7.2-7.5% range (Chart 2). This could test the strength of the positive single-family homebuilding trend sooner than anticipated, as evidenced by the recent pullback in homebuilder confidence and some flattening in single-family housing permits. Ultimately, it all ties back to interest rates, which, given the Fed’s continued tough talk, appear set to remain higher for longer.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of August 18th, 2023

Financial News Highlights

- The big news this week was U.S. Treasury yields reaching the highest point since 2007 thanks to a string of positive economic data releases. The 10-Year yield reached 4.30% on Thursday, surpassing last October’s high.

- July’s retail sales data was one of those positive releases, as a stronger-than expected monthly gain underscored the resilience of the consumer. And July housing starts was another: starts rose modestly despite high mortgage rates. Mortgage rates hit a 21-year high this week, in line with higher Treasury yields.

- The FOMC minutes also played a role taking yields higher, as they showed that Fed officials see upside risks to inflation, which may warrant further tightening in the policy rate.

Yields Drift Higher, As Macro Narrative Shifts

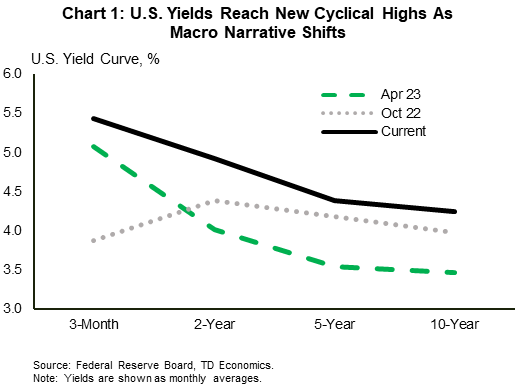

U.S. Treasury yields continued to climb higher this week, following a string of positive economic data releases in financial news. With the macroeconomic narrative shifting away from recessionary back towards soft landing, investor sentiment has also swung back in favor of rates needing to stay ‘higher for longer’. Current market pricing on the fed funds rate doesn’t fully price in the first rate cut until May of next year, with a relatively shallow trajectory on the policy rate through H2-2024. This is a sharp U-turn from just a few months ago when market participants had priced over 100 basis points of cuts through the second half of this year alone! As a result, yields across the curve are well off their April lows and have now even surpassed last October’s highs (Chart 1).

Nowhere has the theme of resilience been more on display than across the consumer segment, and that narrative has clearly carried over into the third quarter. Retail sales for July surprised even the most optimistic forecast, rising by an impressive 0.7% month-on-month (m/m) – its strongest monthly gain since January. Stripping out the most volatile items such as sales at gasoline stations, auto dealers and building supply stores showed even more strength – rising 1.0% m/m – with the largest gain coming from non-store retailers (+1.9% m/m). Indeed, some of the extra vigor was likely due to Amazon Prime Day – suggesting we could see some giveback in the months ahead. However, spending was fairly broad-based across most categories, with 9 of 13 retailers reporting gains. Even being conservative on our monthly assumptions for August/September, Q3 consumer spending is still tracking somewhere close to 3%, nearly doubling last quarter’s gain of 1.6%.

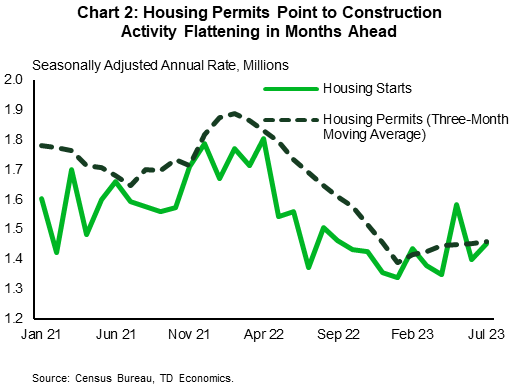

In contrast to the consumer, the housing sector has been one area of the economy that has certainly felt the impact of higher interest rates over the past year. But even here there are some early signs of stabilization. Home construction ticked modestly higher last month, rising by 3.9% m/m to 1.45 million units in financial news. Gains were entirely in the single-family segment, which are now up 22% from last November’s low. Flattening material costs alongside a shortage of lived-in homes for sale have been key factors underpinning construction activity across this segment in recent months. Still, further gains over the near-term seem limited. Permitting activity – a good leading indicator of future projects – has flattened in recent months, while builder confidence ticked down for the first time in 7 months in August alongside the recent surge in mortgage rates, which currently sit at a 21-year high of 7.1% (Chart 2).

Given the continued resilience in the economy, it’s no wonder the minutes from the FOMC’s July 25th-26th meeting showed that the majority of members think the inflation fight is far from over and could require additional tightening in the months ahead. Most forecasters are tracking +3% growth for the third quarter and the Atlanta Fed’s forecasting model is predicting 5.8%! While recent readings on inflation have been favorable, the economy will need to slow considerably to keep sustained downward pressure on inflation without requiring further rate hikes.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of August 11th, 2023

Financial News Highlights

- The U.S. economy had good news on the inflation front this week, as core inflation ticked down in July, even as unfavorable base-effects led to a marginal uptick in the headline measure.

- Some Fed speakers this week maintained a hawkish stance, suggesting September’s meeting is an open debate. Incoming inflation and labor market data will play a key role in the decision.

- Small businesses also showed signs that inflation is easing, with fewer of them raising or planning to raise prices.

Word of the Week is Inflation

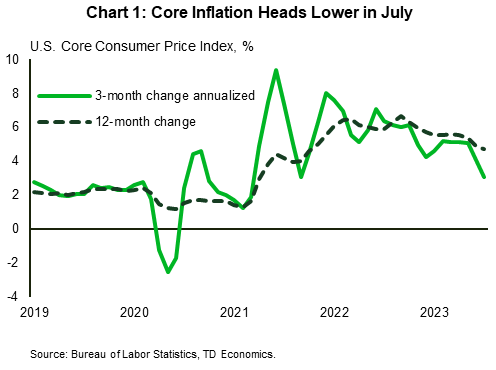

Since skyrocketing during the pandemic, inflation has been a key feature of the economic landscape in financial news. With both consumer and producer price data out this week there was much to add nuance to the scenery. Headline CPI inflation for July was 3.2% year-on-year (y/y), up 0.2 ppts from the previous month. The slight uptick was largely due to base-effects stemming from a notable decline in July 2022 energy prices. The monthly figure was more muted with a 0.2% increase, in line with expectations. Core prices also rose 0.2% month-on-month (m/m) contributing to a deceleration of annual core inflation from 4.8% in June to 4.7% (Chart 1).

Producer prices on the other hand rose slightly more than expected in July (0.3% m/m) due to a pickup in services inflation (0.5% m/m). The uptick in producer prices, which eventually feeds through to consumer prices, illustrates that it may still be too early for the Fed to let its guard down. Nonetheless, these inflation numbers combined with slowing labor market momentum do leave a cloud of doubt about whether the Fed will be raising rates again this year.

Comments from some voting members of the Federal Open Market Committee (FOMC) also suggest that a hike at the September meeting is not a foregone conclusion. NY Fed president Williams noted that both inflation and labor data are generally heading in the right direction, but both are still not quite there yet. He views the question of additional rate increases as still being “open”. Philadelphia Fed President Harker, contrary to his usual hawkish bent, noted that the Fed may be at the point where it can hold rates steady for a while. On the other hand, Fed Governor Bowman is of the view that additional hikes will likely be needed to tame inflation.

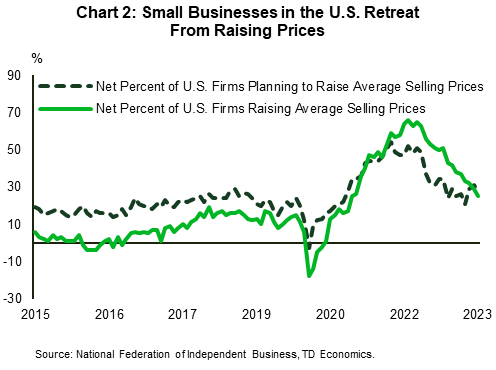

Data from the small business sector also supports the notion that price pressures are receding in financial news. The National Federation of Independent Business survey found that only about one-quarter of small business owners raised prices over the past three months, the lowest reading since January 2021 (Chart 2). Likewise, the share of owners planning to raise prices in the near-term retreated by 4 points following two consecutive monthly increases. Additionally, businesses reporting inflation as their single most important problem declined by 3 points to 21% in July. Overall, the survey suggests that price pressures are moderating, despite a still tight labor market.

One thing that could throw a kink in the downward trajectory of inflation, is rising energy prices in the face of crude oil production cuts by Saudi Arabia and Russia. While the Fed’s preferred measure excludes energy prices, rising oil prices will indirectly boost prices in most other categories.

Ultimately, core inflation should drift lower in the coming months. However, the battle is far from over given that the job market remains tight and the economy resilient. The risk that lower inflation could lift real wages and thus aggregate demand, thereby triggering another round of rising prices, means the Fed will be paying even closer attention to the evolution of jobs data.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial Advisor News for the Week of August 4th, 2023

Financial Advisor News Highlights

- Fitch became the second major credit rating agency to downgrade the U.S. from the top AAA rating, citing the growing fiscal debt burden and an erosion in governance.

- The U.S. economy added 187k new jobs in July, representing the slowest pace of hiring in over two years.

- The Federal Reserve’s Senior Loan Officer Opinion Survey showed credit standards tightened across the board in the second quarter, weighing on loan demand.

Tighter Credit Weighs on Resilience

In this weeks news from the world of a financial advisor, nearly twelve years to the day of the first U.S. credit rating downgrade in 2011, Fitch became the second major rating agency to lower its evaluation of the government’s creditworthiness. Fitch’s rationale was related to growing fiscal deficits in the near-term, medium-term fiscal challenges stemming from aging demographics, and a multi-decade erosion of governance. Since the decision was announced on Tuesday, Treasury yields rose and equities fell, with the ten-year Treasury up 11 basis-points (bps) and the S&P 500 down 1.8% as of the time of writing. Broader implications are expected to be muted as the U.S. economy continues to have strong fundamentals, however it comes at a time when credit standards are already tight.

Monday’s Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) showed that a significant share of banks had tightened business and consumer lending standards in the second quarter. Unsurprisingly, demand for most loan types fell over the period, with the only exception being credit card loans, which saw no change in demand. The economy is clearing feeling the effects of the rapid rise in interest rates over the past 17 months.

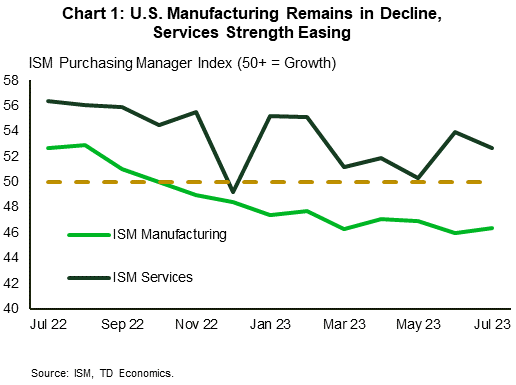

Despite tightening credit conditions, pockets of resilience remain. The ISM PMI data this week continued to show a notable divergence between the manufacturing and service sectors, with the former contracting for a ninth consecutive month and the latter expanding for a seventh straight month in July (Chart 1). Employment growth in both sectors slowed last month, but the services sector is still creating jobs as demand remains robust, whereas the manufacturing employment subindex hit its lowest level in three years.

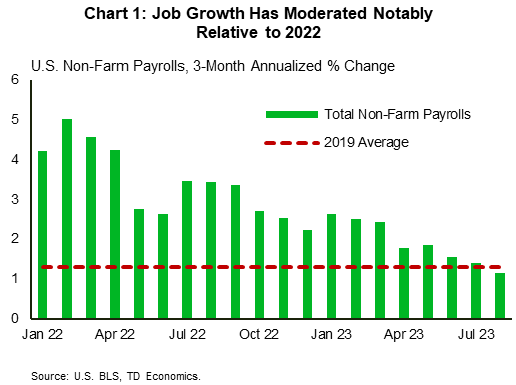

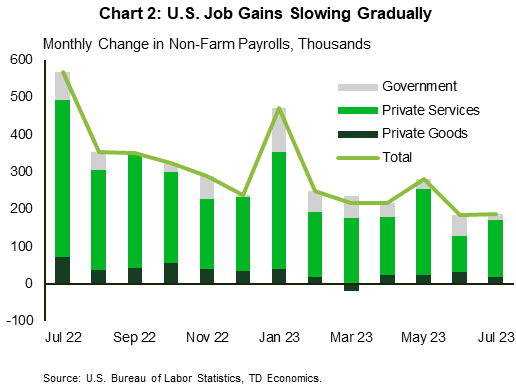

Looking more closely at the most recent labor market update, 187k jobs were created in July, which along with the revised reading for June, represent the slowest pace of job creation in over two years (Chart 2). While this puts job growth on a more sustainable footing, the labor market remains tight, as evidenced by the 4.4% year-on-year(y/y) growth in average weekly earnings in July. The moderation in hiring will be seen as a positive development by the Federal Reserve, but it is unlikely that they will take the prospect of further policy tightening off table until the sustainability of the trend is determined from a financial advisor perspective.

The Fed will get another important indicator next week in the form of the CPI inflation reading for July. June’s print showed core CPI fell below 5% y/y for the first time since December 2021 and the Federal Reserve will be looking to see further progress. With preliminary evidence that the cumulative effects of past rate hikes are working to cool inflationary pressures, we expect that the FOMC will leave the policy rate unchanged when they meet in September. However, they are likely to continue to emphasize the importance of incoming data on determining the future path of interest rates as the ultimate form of ‘landing’ for the economy becomes clearer.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.

Financial News for the Week of July 28th, 2023

Financial News Highlights

- Fed Chair Powell signaled a meeting-by-meeting approach on changes to the fed funds rate, opting to evaluate incoming data and fine-tune interest rates to help temper inflation.

- The second quarter’s GDP release showed an economy that continues to chug along at a solid pace – exceeding expectations for a steeper slowdown.

- The Fed will keep rates in restrictive territory into next year so, even if a recession is avoided, tepid economic growth is to be expected.

Preparing for Landing

Readers would be right to ask, what’s “moderate” about another upside surprise to economic growth in the second quarter for financial news? Fed Chair Powell signaled a meeting-by-meeting approach on changes to the fed funds rate, opting to evaluate incoming data and fine-tune interest rates to help temper inflation. Incoming data have shown that the economy remains resilient – buoyed by healthy consumer spending growth and business investment – as fears of a recession gradually fade. What remains to be seen is whether inflation will continue to moderate in the coming months or whether the Fed will have to push interest rates higher still – thereby raising the odds the economy contracts.

The second quarter’s GDP release showed an economy that continues to chug along at a solid pace – exceeding expectations for a steeper slowdown in financial news. However, the composition of growth was interesting. In line with our forecasts, consumer spending growth advanced 1.6% quarter-on-quarter (q/q) annualized – slowing from 4.2% in Q1. The Fed will be reassured that its rate hiking cycle is filtering through to consumer behavior as spending growth slows despite a drum-tight labor market. Moreover, with rates at multidecade highs, the housing market is feeling the force of tight financing conditions, with residential investment continuing to pull back in the second quarter – now contracting for the ninth quarter in a row. With demand growth slowing, imports pulled back again – now having contracted for the third time in the past year. The gradual slowdown is also not unique to the U.S., as plummeting export growth indicates the global economy is slowing under the weight of inflation and higher interest rates.

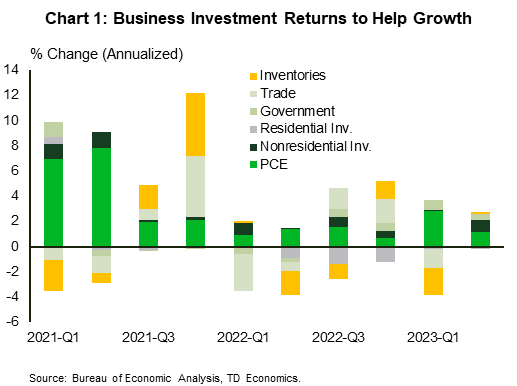

A pleasant surprise in the data was the healthy activity in the business sector that provided a meaningful lift to the economy (Chart 1). Nonresidential investment advanced 7.7% q/q – good for the strongest showing since the first quarter of 2022. The flow of federal funds to support climate friendly investments is helping fuel the ongoing strength in structures and equipment investment – the latter registering its best quarterly growth rate since 2011, outside of the post-2020 lockdown bounce.

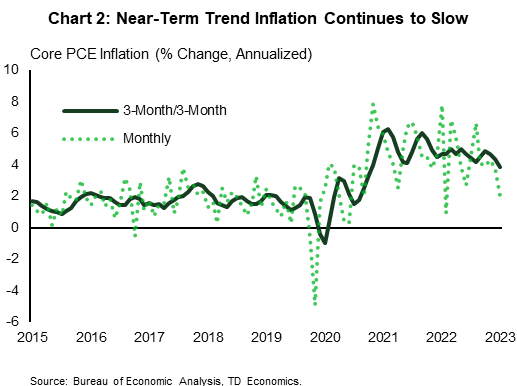

With full second quarter data showing a healthy consumer, all eyes were on June’s personal income and outlay report for signals of spending and price momentum heading into the summer months. Healthy spending held up in June and outstripped income growth, denting the personal savings rate. Between higher interest rates, strong inflation and depleting savings the pandemic era spending binge is slowing down. This is music to the Fed’s ears as it means softening inflationary pressures. Needless to say, the downside surprise on core PCE inflation (4.1% year-on-year vs. 4.2% expected) was a particularly welcome development. Even more encouraging, the near-term trend (Chart 2) has eased to its slowest pace since March 2021.

With inflation slowing and consumer spending remaining resilient the odds of a soft landing are ticking higher. However, the Fed will keep rates in restrictive territory into next year so, even if a recession is avoided, tepid economic growth is to be expected.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.