Financial News for the Week of March 21st, 2025

Financial News Highlights

- The FOMC held the policy rate steady at a target range of 4.25%-4.5% for the second consecutive meeting in financial news. But, committed to slowing the pace of balance sheet runoff of its U.S. Treasury holdings.

- Revised economic projections showed a small downgrade to the FOMC’s growth outlook, but a near-term upgrade to inflation. The median forecast still expects 50bps of rate cuts by year-end.

- February data out this week were mixed. Retail sales underwhelmed, while housing data rebounded from January’s weather induced slide.

Uncertainty Clouding the Outlook

With no new tariff announcements, trade tensions were temporarily moved to the backburner this week, allowing investors to shift the focus to the economic data calendar. February data readings out this week were mixed. Retail sales underwhelmed expectations, but both housing starts, and existing home sales largely recovered from January’s weather induced slide. Meanwhile, in financial news the Federal Reserve held the policy rate steady at a target range of 4.25%-4.5% but signaled an intention to slow the pace of balance sheet runoff for U.S. Treasury holdings starting in April. While investors were braced for a more downbeat messaging on the outlook, the Fed’s statement and Chair Powell’s press conference struck a more balanced tone. This helped to temporarily soothe unnerved financial markets, but growth fears reemerged by late-week, fueling a further sell-off. At time of writing, the S&P 500 was down 0.5%, while term yields traded lower by about 10bps, with the 10-year Treasury currently sitting at 4.22%.

With no new tariff announcements, trade tensions were temporarily moved to the backburner this week, allowing investors to shift the focus to the economic data calendar. February data readings out this week were mixed. Retail sales underwhelmed expectations, but both housing starts, and existing home sales largely recovered from January’s weather induced slide. Meanwhile, in financial news the Federal Reserve held the policy rate steady at a target range of 4.25%-4.5% but signaled an intention to slow the pace of balance sheet runoff for U.S. Treasury holdings starting in April. While investors were braced for a more downbeat messaging on the outlook, the Fed’s statement and Chair Powell’s press conference struck a more balanced tone. This helped to temporarily soothe unnerved financial markets, but growth fears reemerged by late-week, fueling a further sell-off. At time of writing, the S&P 500 was down 0.5%, while term yields traded lower by about 10bps, with the 10-year Treasury currently sitting at 4.22%.

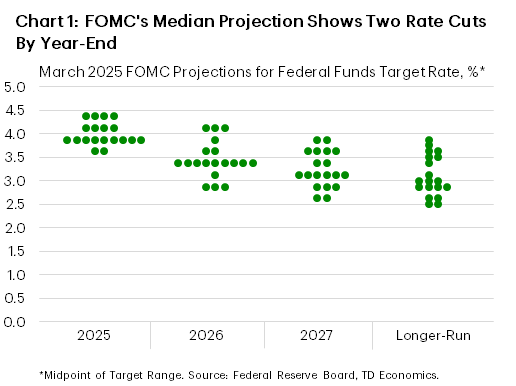

The Fed’s statement included updated economic projections from FOMC members. The median GDP forecast was revised lower over the forecast, with a below-trend pace of economic growth expected in 2025 (1.7% from 2.1%), before steadying at 1.8% in 2026 (previously 2.0%) and 2027 (previously 1.9%). The unemployment rate was nudged higher by a tick this year to 4.4% but remained unchanged at 4.3% in 2026 and 2027. Core PCE inflation was also revised higher for 2025 (2.8% from 2.5%), which Chair Powell largely attributed to tariff impacts. Importantly, the revised “dot plot” still showed two 25bps rate cuts for this year. But a closer inspection of the dots shows that committee members see the balance of risks skewed towards fewer cuts, as eight officials now expect one or no cuts this year (up from four in December) (Chart 1).

During the press conference, Chair Powell characterized the economy as “strong”, but emphasized that any point forecasts remain “highly uncertain” in light of recent policy changes under the new administration. When asked about the recent pullback in business and consumer sentiment measures, Powell reiterated that the “hard data” are still showing an economy that is “solid”. He also downplayed the recent jump in inflation expectations shown in the University of Michigan survey, characterizing it as an outlier relative to most other measures.

During the press conference, Chair Powell characterized the economy as “strong”, but emphasized that any point forecasts remain “highly uncertain” in light of recent policy changes under the new administration. When asked about the recent pullback in business and consumer sentiment measures, Powell reiterated that the “hard data” are still showing an economy that is “solid”. He also downplayed the recent jump in inflation expectations shown in the University of Michigan survey, characterizing it as an outlier relative to most other measures.

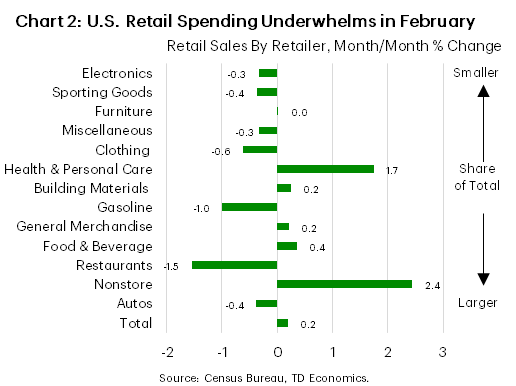

But this week’s retail sales data suggests otherwise. Retail sales rose by just 0.2% m/m in February, after declining 1.2% in January. Only 5 of the 13 major categories (Chart 2) saw gains last month while revisions to January showed an even weaker pace of retail spending than previously reported. Moreover, spending at bars & restaurants – the only services-based metric included in the retail report – plunged by 1.5% or the largest monthly pullback in two-years. This bears close watching, as discretionary services spending has been a key driver underpinning the strength of the consumer in past years.

For now, the Fed appears comfortable to sit tight and wait for more clarity on both the policy and data front. This will not come from any one policy announcement or data reading, suggesting policymakers will remain on the sidelines for at least another few months before making their next move.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of February 28th, 2025

Financial News Highlights

- The Fed’s preferred inflation metric, core PCE, rose 2.6% year-on-year in January, in-line with expectations and continuing to converge with the Fed’s 2% target in financial news.

- The Conference Board’s Consumer Confidence Index showed a material decline in February, as tariffs weighed on sentiment and boosted inflation expectations.

- The President announced an additional 10% tariff on China set to take effect on March 4th, in concert with the previously announced 25% tariffs against Canada and Mexico.

Angst Builds with Tariff Threats

The final week of February included an update on the health of the American consumer, and the Federal Reserve’s preferred inflation metric in financial news. Meanwhile, financial markets remained cautious as the prospect for broad-based tariffs to go into effect next week against the nation’s three largest trading partners kept sentiment subdued. As of the time of writing, the S&P 500 was down 2.3% on the week, while the 10-year Treasury yield fell nearly 20 basis-points to 4.24%.

The final week of February included an update on the health of the American consumer, and the Federal Reserve’s preferred inflation metric in financial news. Meanwhile, financial markets remained cautious as the prospect for broad-based tariffs to go into effect next week against the nation’s three largest trading partners kept sentiment subdued. As of the time of writing, the S&P 500 was down 2.3% on the week, while the 10-year Treasury yield fell nearly 20 basis-points to 4.24%.

The impact of tariff threats on consumer confidence has partially contributed to the negative sentiment in financial markets over the past week. Last Friday, the University of Michigan consumer sentiment index fell to its lowest level in 15 months, and this was followed by the Conference Board Consumer Confidence Index dropping sharply this week to an eight-month low. The Conference Board’s survey also noted that mentions of trade and tariffs had risen to a level last seen in 2019. While we saw real personal consumption expenditures fall 0.5% month-on-month in January in data released this week, severe weather undoubtedly played a role.

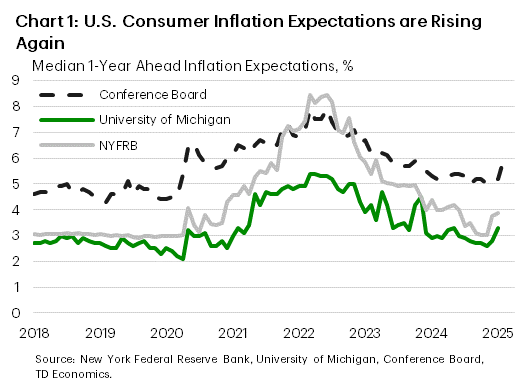

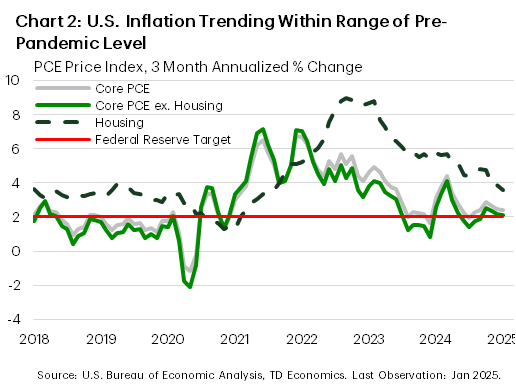

At the same time, consumer surveys have also begun to show signs of rising inflation expectations (Chart 1), which could present a risk for the Federal Reserve’s mission to return inflation to their 2% target. Core PCE inflation, the Fed’s preferred metric, rose 2.6% year-on-year in January. Looking at the three-month annualized percentage change, momentum has continued to trend favorably (Chart 2) with both the housing and excluding housing subcategories within range of pre-pandemic levels. However, these metrics remain slightly elevated on aggregate, which supports the Federal Reserve’s holding pattern. This, combined with rising inflation expectations, is also likely why several of the Federal Reserve officials we heard from this week favored a patient approach to future monetary policy adjustments, particularly amid elevated uncertainty. Market pricing has the Fed returning to rate cuts in June, with one additional rate cut before year end – in line with the median FOMC official projection from December.

At the same time, consumer surveys have also begun to show signs of rising inflation expectations (Chart 1), which could present a risk for the Federal Reserve’s mission to return inflation to their 2% target. Core PCE inflation, the Fed’s preferred metric, rose 2.6% year-on-year in January. Looking at the three-month annualized percentage change, momentum has continued to trend favorably (Chart 2) with both the housing and excluding housing subcategories within range of pre-pandemic levels. However, these metrics remain slightly elevated on aggregate, which supports the Federal Reserve’s holding pattern. This, combined with rising inflation expectations, is also likely why several of the Federal Reserve officials we heard from this week favored a patient approach to future monetary policy adjustments, particularly amid elevated uncertainty. Market pricing has the Fed returning to rate cuts in June, with one additional rate cut before year end – in line with the median FOMC official projection from December.

Looking ahead to next week, there will be plenty to keep markets on their toes. First up will be the potential for the 25% tariffs on Canada and Mexico, plus the new additional 10% tariff on China announced this week, to be implemented next Tuesday. If an eleventh-hour resolution cannot be achieved again, then significant trade disruptions would likely follow. President Trump will also be delivering his State of the Union address on Tuesday, which may include new policy considerations. Lastly, we’ll round out the week with the employment report for February on Friday, which will be the last employment report released prior to the Fed’s next meeting in mid-March. Consensus expectations currently call for 158k new jobs to have been created this month, which would likely be viewed positively by the Federal Reserve. All-in-all, there will be plenty of information released next week to guide expectations in the months ahead.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of February 21st, 2025

Financial News Highlights

- Fed Speakers this week emphasized the need for a data-dependent approach to policy decisions in financial news.

- As a result, next week’s inflation data in the Personal Income and Outlays Report for January will be closely watched.

- From our lens, the Fed is likely to remain on pause until the second quarter of this year, delivering two cuts by year end, as healthy economic activity supports the labor market and price growth.

Data Dependent Decisions

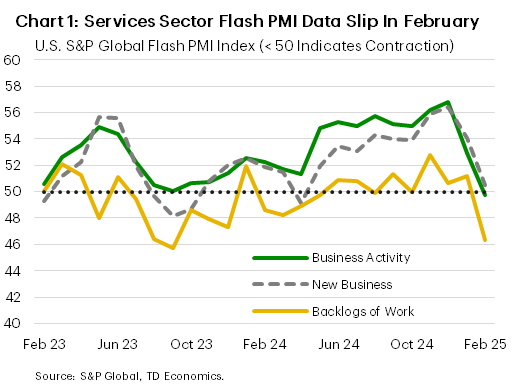

In the absence of major economic data, equities and Treasury yields were a smidge below where they started the week after reacting to a flash PMI release on Friday that suggested shrinking activity in the services sector in February (Chart 1). That said, the focus is on next week, when the second update of fourth quarter GDP and January’s Personal Income and Outlays report will give a fresh look at economic momentum and the first look at the Fed’s preferred inflation metric for 2025. Fed speakers provided some insights this week on why the data-dependent approach is key when looking to understand how inflation will evolve in a still-healthy economy.

In the absence of major economic data, equities and Treasury yields were a smidge below where they started the week after reacting to a flash PMI release on Friday that suggested shrinking activity in the services sector in February (Chart 1). That said, the focus is on next week, when the second update of fourth quarter GDP and January’s Personal Income and Outlays report will give a fresh look at economic momentum and the first look at the Fed’s preferred inflation metric for 2025. Fed speakers provided some insights this week on why the data-dependent approach is key when looking to understand how inflation will evolve in a still-healthy economy.

At the start of the week Board member Christopher Waller gave a speech in Sydney with a title that left very little ambiguity, “Disinflation Progress Uneven but Still on Track. Rate Cuts on Track as Well.” The speech clearly outlined his views, including that monetary policy is restrictive and “putting downward pressure on inflation”, while economic momentum is holding up. Vice Chair Jefferson spoke later in the week, reaffirming the view that the economy and labor market are on solid footing, and the need to maintain a data dependent approach. Dr. Jefferson focused on the strength of household balance sheets and how they are supporting consumer spending. The key was that while they are generally in good position, households with lower- and middle-incomes “have less of a buffer of liquid assets than they did before the pandemic” and keeping an eye on balance sheet developments will help “inform forecasts of overall economic activity”.

One interesting concept to monitor was Dr. Waller’s acknowledgement that progress on cooling inflation in the early part of the year has been notably slow in past years. This could be attributable to “residual seasonality”– the idea that the price adjustments that usually come in the early part of the year are now bigger than they were typically and are showing up in the seasonally adjusted data that should have accounted for them. This is an interesting wrinkle, and Dr. Waller cited research that price pressures have tended to be greater in the first half of the year relative to the second in 16 of the past 22 years. The expectation then would be that even with stronger-than-expected inflation in the early part of the year, this effect should fade into the latter part of 2025, as it did in 2024.

One interesting concept to monitor was Dr. Waller’s acknowledgement that progress on cooling inflation in the early part of the year has been notably slow in past years. This could be attributable to “residual seasonality”– the idea that the price adjustments that usually come in the early part of the year are now bigger than they were typically and are showing up in the seasonally adjusted data that should have accounted for them. This is an interesting wrinkle, and Dr. Waller cited research that price pressures have tended to be greater in the first half of the year relative to the second in 16 of the past 22 years. The expectation then would be that even with stronger-than-expected inflation in the early part of the year, this effect should fade into the latter part of 2025, as it did in 2024.

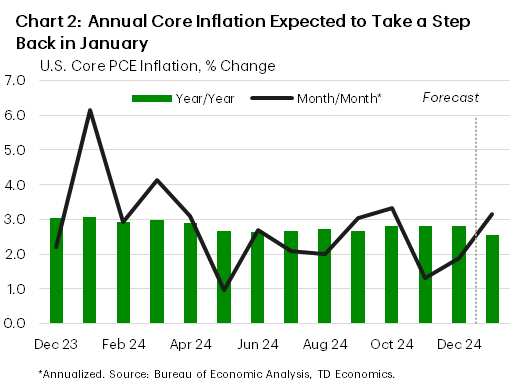

With speakers emphasizing the data-dependent approach, the focus will then be on the Personal Income and Outlays report on next Friday in financial news. The spending figures could be noisy, as cold weather and large fires in Los Angeles likely disrupted economic activity, so the focus will be on what happens with inflation. Current expectations are for the core PCE price index (the Fed’s preferred inflation gauge) to clock in at around 0.2%-0.3% month-on-month in January (2.6% year-on-year, Chart 2), but as Dr. Waller suggested even an upside surprise could be due to some residual seasonality. From our lens, the Fed is likely to remain on pause until the second quarter of this year, delivering two cuts by year-end, as healthy economic activity supports the labor market and price growth.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of February 14th, 2025

Financial News Highlights

- President Trump announced a universal 25% tariff on all steel and aluminum imports, effective March 12th in financial news.

- January CPI came in hotter than expected, with core inflation rising at its fastest monthly pace since March 2024.

- Speaking at a semiannual congressional hearing, Chair Powell emphasized that policymakers were in no rush to cut rates.

Hot CPI + Trade Uncertainties = Extended Fed Pause

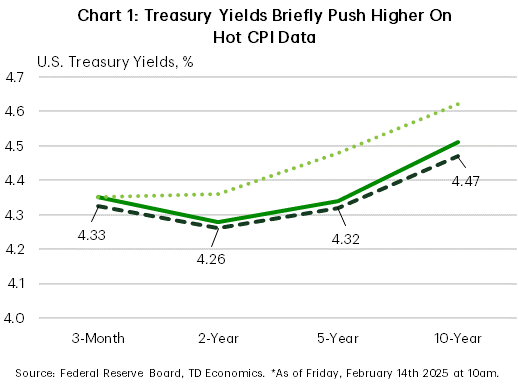

Tariffs remained the policy focus of the new administration this week, with President Trump announcing a universal 25% tariff on all steel and aluminum imports into the U.S., effective March 12th. Financial markets were largely unperturbed by the announcement, perhaps because the more targeted measures hinted towards a broader pivot on how the administration planned to implement its tariff agenda. But a hotter-than-expected CPI reading for January and a firm commitment from Chair Powell that policymakers were in no hurry to cut rates, helped to temporarily sour the mood by mid-week. Treasury yields across the curve briefly pushed higher only to completely retrace on Thursday, as President Trump’s threat of announcing further reciprocal tariffs showed no immediate action. The S&P 500 ended the week 1.6% higher, while Treasury yields were largely unchanged, with the 10-year currently sitting at 4.47% (Chart 1).

Tariffs remained the policy focus of the new administration this week, with President Trump announcing a universal 25% tariff on all steel and aluminum imports into the U.S., effective March 12th. Financial markets were largely unperturbed by the announcement, perhaps because the more targeted measures hinted towards a broader pivot on how the administration planned to implement its tariff agenda. But a hotter-than-expected CPI reading for January and a firm commitment from Chair Powell that policymakers were in no hurry to cut rates, helped to temporarily sour the mood by mid-week. Treasury yields across the curve briefly pushed higher only to completely retrace on Thursday, as President Trump’s threat of announcing further reciprocal tariffs showed no immediate action. The S&P 500 ended the week 1.6% higher, while Treasury yields were largely unchanged, with the 10-year currently sitting at 4.47% (Chart 1).

The steel and aluminum tariffs announced on Monday come just a week after Canada and Mexico were able to get a 30-day delay on the blanket 25% tariffs that were supposed to go into effect on February 1st. But unlike those tariffs, the administration has some historical precedence for the steel and aluminum tariffs, with President Trump having enacted similar measures back in 2018/19. For most countries, the previous tariffs had been lifted. However, this week’s announcement would reinstate the 25% tariff on steel and ups the tariff on aluminum to 25% (previously 10%), with no country exemptions.

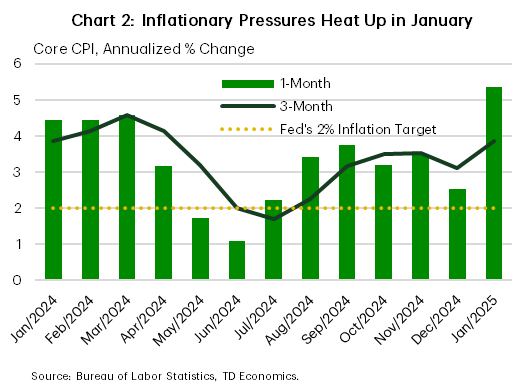

The ratcheting up of trade tensions has come at particularly challenging time for policymakers, as the Fed’s fight to return price stability has hit a wall. The January CPI reading showed headline inflation rising at its fastest monthly pace in nearly a year and a half, while core inflation’s gain was the largest since March 2024 (Chart 2). Residual seasonality looks to be at least partially responsible for January’s uptick – as it was in the early months of last year. This appears to be a legacy issue stemming from the pandemic.

The ratcheting up of trade tensions has come at particularly challenging time for policymakers, as the Fed’s fight to return price stability has hit a wall. The January CPI reading showed headline inflation rising at its fastest monthly pace in nearly a year and a half, while core inflation’s gain was the largest since March 2024 (Chart 2). Residual seasonality looks to be at least partially responsible for January’s uptick – as it was in the early months of last year. This appears to be a legacy issue stemming from the pandemic.

Historically, businesses tend to build in big price adjustments at the beginning of each year, which would normally be corrected for with appropriate seasonal factors. But during the COVID pandemic, firms were much faster to pass on price increases, distorting the seasonal patterns, and biasing the January inflation readings higher in recent years in financial news.

But it’s unlikely that residual seasonality is telling the whole story. Consumer spending remained incredibly strong through the second half of last year – averaging an impressive 3.6% annualized. Moreover, spending on both goods and services was very healthy in Q4, helping to explain the breadth of price pressures last month. While the January retail sales data point to a sharp slowing in spending, those figures were likely impacted by inclement weather and the California wildfires – suggesting some giveback in spending in February.

At this point, the Fed appears to have plenty of runway to maintain its current policy rate and wait for more clarity on the inflation front. This is unlikely to come with just the next few inflation readings, which means the Fed is on hold until at least the summer.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of February 7th, 2025

Financial News Highlights

- Tariffs on Canada and Mexico have been put on hold for one month, but a 10% tariff was imposed on imports from China in financial news.

- Companies have ramped up inventories ahead of tariffs, leading to a sharp increase in the trade deficit in December. Activity has eased off in the services sector, but continued to reaccelerate in manufacturing.

- Hiring has slowed in January, however, the labor market remains solid overall. Significant upward revisions to the fourth quarter figures suggest that job growth was stronger at the end of last year than previously thought.

Canada-Mexico Tariffs on Hold

This week was anything but boring for financial news. On Monday, an 11th-hour deal was reached to delay tariffs on Canada and Mexico for a month. However, while Canada and Mexico were spared, China was not, as an additional 10% tariff was imposed on all imports from the country.

This week was anything but boring for financial news. On Monday, an 11th-hour deal was reached to delay tariffs on Canada and Mexico for a month. However, while Canada and Mexico were spared, China was not, as an additional 10% tariff was imposed on all imports from the country.

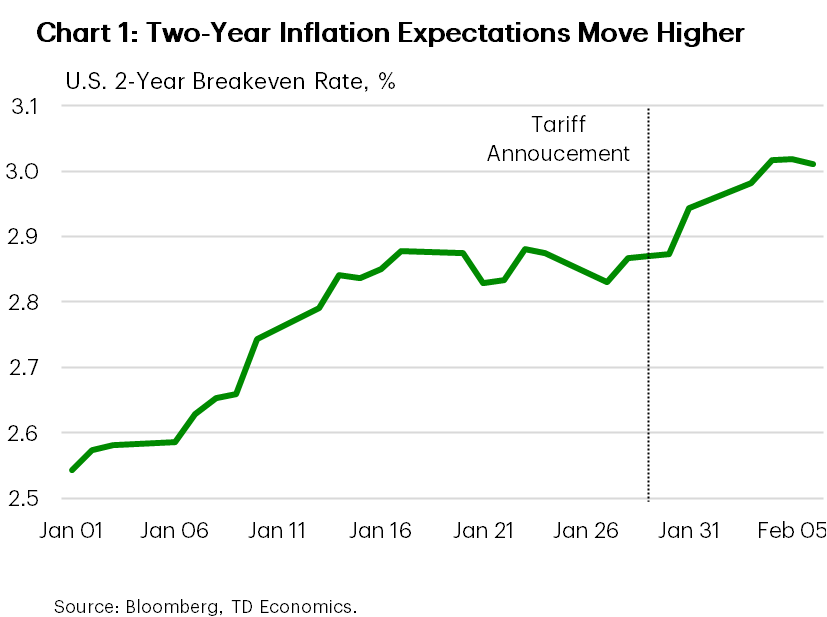

The prospect of tariffs being imposed on North America in a month, or in April when the review of current trade policies is completed, looms large. Financial markets have largely recovered from their initial knee-jerk reaction to the tariff announcement, with the S&P 500 paring back losses by the end of the week. However, inflation expectations over the next two years have risen (Chart 1) while bond yields have declined. This points to investors’ concerns that tariffs will accelerate inflation and slow economic growth.

Businesses’ uncertainty about the looming tariffs were reflected in the trade data. The U.S. trade deficit widened sharply in December – the largest one-month increase since the early 1990s. Imports surged as companies rushed to ramp up inventories ahead of potential tariffs. Last month’s sharp increase in the trade deficit is likely temporary, but trade policy uncertainty will continue to affect trade flows throughout the year. Uncertainty about tariffs also clouds the outlook in the manufacturing sector, particularly in industries such as auto manufacturing (report). Even though the ISM manufacturing index has continued to improve in January, rising for the third consecutive month and finally moving into expansionary territory, supply chain disruptions could dent the sector’s nascent progress.

Activity in the services sector continued to expand robustly in January, although it dialed back a notch. The services sector is less exposed to trade than manufacturing, but it is not immune. The prices paid subcomponent remains elevated, and any supply chain disruptions and higher input prices could reignite inflationary pressure.

Additional inflationary impetus could also come from the labor market. Today’s employment report showed that the U.S. economy added 143k jobs in January. This is considerably less than December’s tally (+305k), but still a solid outturn, particularly when combined with a slight decline in the unemployment rate and an uptick in wage growth. Moreover, wildfires in Los Angeles and a cold weather spell nationwide could have also weighed on employment, suggesting a bounce-back next month could be in the cards. Lastly, revisions through the fourth quarter were notably higher, adding an extra 101k jobs to the previously reported figures and suggesting that hiring momentum was even stronger at the end of last year than previously thought (Chart 2).

Additional inflationary impetus could also come from the labor market. Today’s employment report showed that the U.S. economy added 143k jobs in January. This is considerably less than December’s tally (+305k), but still a solid outturn, particularly when combined with a slight decline in the unemployment rate and an uptick in wage growth. Moreover, wildfires in Los Angeles and a cold weather spell nationwide could have also weighed on employment, suggesting a bounce-back next month could be in the cards. Lastly, revisions through the fourth quarter were notably higher, adding an extra 101k jobs to the previously reported figures and suggesting that hiring momentum was even stronger at the end of last year than previously thought (Chart 2).

With inflation progress having stalled in recent months, wage growth showing staying power and heightened uncertainties on how far the new administration will go on its policies, the Fed is likely to remain more cautious. Next week’s inflation report will likely show that the Fed’s patience is justified, as inflation remains persistently above the Fed’s 2% target.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of January 31st, 2025

Financial News Highlights

- The U.S. economy ended 2024 on solid footing, expanding at a 2.3% annualized pace. The consumer did the heavy lifting, with spending accelerating in the fourth quarter.

- The Fed’s preferred inflation gauge, the core PCE deflator, continued to hover somewhat above target in December, growing at 2.8% year-on-year. But trends over the past few months suggest further cooling ahead.

- Major action may come on the trade policy front as early as this weekend, with President Trump reiterating his intentions to impose tariffs on Canada and Mexico – America’s largest trading partners.

U.S. – Stock Market Rowdy, Economy Steady

The last week of January began on a soft note for stock markets in financial news. As it became apparent that a low-cost Chinese artificial intelligence start-up (DeepSeek) could threaten the dominance of American rivals, the valuations of several large tech firms took a hit, weighing on major indexes. Some recovery ensued later in the week, with the S&P 500 and tech-heavy NASDAQ nearly erasing the losses from last week’s close (at the time of writing). In contrast to the rowdiness of the stock market, signals out of the economy continued to point to steadiness.

The last week of January began on a soft note for stock markets in financial news. As it became apparent that a low-cost Chinese artificial intelligence start-up (DeepSeek) could threaten the dominance of American rivals, the valuations of several large tech firms took a hit, weighing on major indexes. Some recovery ensued later in the week, with the S&P 500 and tech-heavy NASDAQ nearly erasing the losses from last week’s close (at the time of writing). In contrast to the rowdiness of the stock market, signals out of the economy continued to point to steadiness.

The first read on fourth quarter GDP showed that the U.S. economy ended last year on a solid footing as it grew at 2.3% quarter-on-quarter annualized. The consumer did the heavy lifting, offsetting a notable drag from gross fixed private investment (Chart 1). Goods spending carried the torch once again, propelled forward by a double-digit increase in durable goods, but services also notched a mild acceleration. Meanwhile, within the softness of the broad private investment category, residential investment was a bright spot for a change, lifted by a double-digit gain in housing starts last quarter. Looking at the big picture, the fact that the economy essentially sustained 2023’s pace through 2024, despite the still elevated interest rate environment, is an impressive accomplishment.

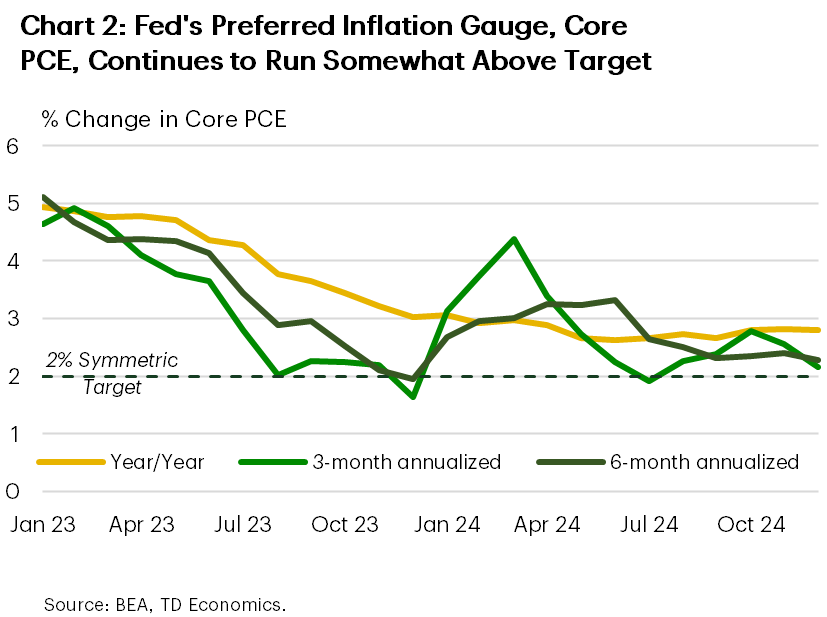

Friday morning’s monthly PCE report provided some more detail with respect to consumption and inflation trends at the turn of the year. The handoff to the start of 2025 is solid, as real spending growth remained robust in December, growing at nearly 5% annualized. This, as strength in services helped offset some cooldown in goods spending from the double-digit gain in the month prior. Additionally, the Fed’s preferred inflation gauge – core PCE – held at 2.8% in year-on-year terms. The fact that the 3-month and 6-month annualized rate of change in core PCE inflation gravitated lower toward the target, was a welcome development (Chart 2).

With inflation still somewhat elevated (though appearing to head in the right direction) and the economy remaining on solid footing, the Fed can afford to take a cautious approach to further loosening monetary policy. The FOMC left the policy rate unchanged at this week’s meeting – a move that was widely anticipated. Fed Chair Powell acknowledged that “we don’t need to be in a hurry to adjust our policy stance”, while nodding to the uncertainties and the risks related to major policy changes out of Washington, such as on trade policy. Powell reiterated a wait-and-see approach, stating that they’d need any new policy changes to be articulated first, before assessing their impacts on the economy in financial news.

With inflation still somewhat elevated (though appearing to head in the right direction) and the economy remaining on solid footing, the Fed can afford to take a cautious approach to further loosening monetary policy. The FOMC left the policy rate unchanged at this week’s meeting – a move that was widely anticipated. Fed Chair Powell acknowledged that “we don’t need to be in a hurry to adjust our policy stance”, while nodding to the uncertainties and the risks related to major policy changes out of Washington, such as on trade policy. Powell reiterated a wait-and-see approach, stating that they’d need any new policy changes to be articulated first, before assessing their impacts on the economy in financial news.

Major action on the trade front may come as early as this weekend, with President Trump reiterating his intention to impose 25% tariffs on Mexico and Canada on February 1st. There’s still a possibility that cooler heads will prevail, as President Trump’s top pick for commerce secretary suggested that tariffs could be avoided if swift action was taken on the border issues. Still, the deadline is fast approaching and any trade skirmishes with its neighbors will be problematic – the two countries are America’s largest trading partners and are deeply integrated in supply chains.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of January 3rd, 2025

Financial News Highlights

- The Federal Reserve cut its policy rate by 25 basis points to 4.25-4.5%, as expected in financial news. But, updated forecasts showed that FOMC members now expect inflation to be a bit hotter next year, and as a result expect to make only 50 basis points in cuts next year, down from 100 bps in September.

- Economic growth was revised upwards in the third quarter. Real GDP rose 3.1%, up from 2.8% previously.

- There was also good news on the Fed’s preferred inflation gauge. The Core PCE Deflator held steady at 2.8% in year-on-year terms in November, but cooled noticeably on a month-to-month basis.

Awaiting the Changing of the Guard

Turning the page on 2024, we eased into the new year this week with limited updates on the state of the economy in financial news. For that reason, the attention of financial markets was more attuned to developments in Washington as the 119th session of Congress kicked off. However, the holiday period continued to weigh on trading volumes overall, with the S&P falling 1.1% on the week, while U.S. Treasury yields declined modestly.

Turning the page on 2024, we eased into the new year this week with limited updates on the state of the economy in financial news. For that reason, the attention of financial markets was more attuned to developments in Washington as the 119th session of Congress kicked off. However, the holiday period continued to weigh on trading volumes overall, with the S&P falling 1.1% on the week, while U.S. Treasury yields declined modestly.

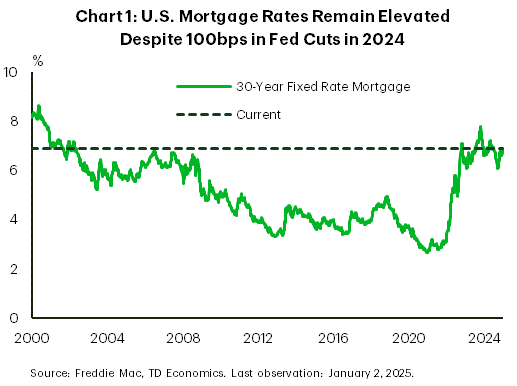

Economic data releases this week showed that housing market activity continued to gradually recover from its current subdued state. Pending home sales improved for a fourth consecutive month in November, although gains have moderated recently as rates ticked higher through the fourth quarter. With mortgage rates remaining near 7% (Chart 1) and the Federal Reserve shifting into a more cautionary stance in 2025, the housing market’s recovery is expected to remain gradual this year (see report). As of the time of writing, market pricing implies a nearly 90% probability of the Fed pausing at their next meeting at the end of the month, but the ultimate trajectory of monetary policy this year will likely depend on the fiscal policies implemented by the incoming administration and the impact they have on the economy.

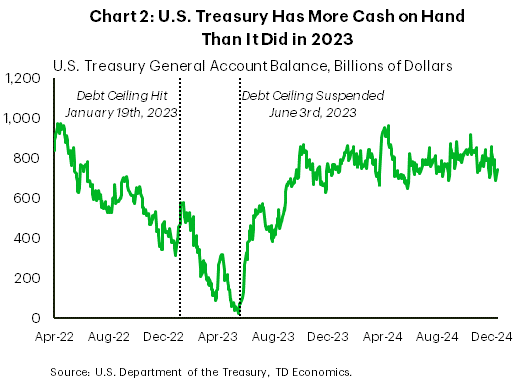

Shifting over to D.C., the federal government continues to be funded by the continuing resolution passed by Congress on December 20th, which will remain in effect until March 14th. This means the twelve appropriation bills for the current fiscal year will be one of the first priorities of the new session of Congress which commenced this week. In addition, the debt ceiling suspension that had been in place since June 2023 expired with the start of the new year. The U.S. Treasury put out a statement last week stating that they anticipated that the debt ceiling would become binding in the next 2-3 weeks, at which time they would begin taking extraordinary measures to avoid defaulting on their fiscal obligations. These measures would likely last until the summer (as they did when the debt ceiling was last hit in early 2023 – Chart 2), but the timely implementation of measures to suspend, raise, or eliminate the debt ceiling will be of paramount importance in the first half of 2025.

Shifting over to D.C., the federal government continues to be funded by the continuing resolution passed by Congress on December 20th, which will remain in effect until March 14th. This means the twelve appropriation bills for the current fiscal year will be one of the first priorities of the new session of Congress which commenced this week. In addition, the debt ceiling suspension that had been in place since June 2023 expired with the start of the new year. The U.S. Treasury put out a statement last week stating that they anticipated that the debt ceiling would become binding in the next 2-3 weeks, at which time they would begin taking extraordinary measures to avoid defaulting on their fiscal obligations. These measures would likely last until the summer (as they did when the debt ceiling was last hit in early 2023 – Chart 2), but the timely implementation of measures to suspend, raise, or eliminate the debt ceiling will be of paramount importance in the first half of 2025.

With a full legislative agenda already taking form, the first order of business for the new Congressional session this week was electing a new Speaker of the House, with a vote expected Friday afternoon. Looking ahead, Senate confirmation hearings for President-elect Trump’s cabinet nominees are likely to begin in the coming weeks, with the much-anticipated presidential inauguration day set for two weeks from Monday.

On the economic front, we’ll return to a more normal schedule of data releases next week, with the December employment report expected to show 153k new jobs added for the month – down from 227k in November. FOMC December meeting minutes will also be released next Wednesday, which will provide further insights on the Fed’s updated projections. All-in-all, 2025 already looks set to be an eventful year.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of December 20th, 2024

Financial News Highlights

- The Federal Reserve cut its policy rate by 25 basis points to 4.25-4.5%, as expected in financial news. But, updated forecasts showed that FOMC members now expect inflation to be a bit hotter next year, and as a result expect to make only 50 basis points in cuts next year, down from 100 bps in September.

- Economic growth was revised upwards in the third quarter. Real GDP rose 3.1%, up from 2.8% previously.

- There was also good news on the Fed’s preferred inflation gauge. The Core PCE Deflator held steady at 2.8% in year-on-year terms in November, but cooled noticeably on a month-to-month basis.

Fed Signals a More Cautionary Stance on Rate Cuts Next Year

The Federal Reserve delivered some sour candy to cap off 2024, cutting its policy rate by 25 basis points, but signaling a more moderate pace of cuts next year. This hawkish tilt sent Treasury yields higher, with the 10-year rising from just under 4.4% to briefly over 4.6%. Equity markets took the news hard, with the S&P 500 down roughly 3.5% from pre-meeting levels at time of writing. Part of the weak equity market performance may also have to do with a looming government shutdown. Washington has only a few hours to pass a funding bill into law. Failure to do so will lead to a partial government shutdown. Essential services would continue, but most federal workers wouldn’t receive a paycheck. In addition, some workers would be furloughed until Congress passes new funding. The Bipartisan Policy Center estimates that some 875 thousand federal workers would be furloughed.

The Federal Reserve delivered some sour candy to cap off 2024, cutting its policy rate by 25 basis points, but signaling a more moderate pace of cuts next year. This hawkish tilt sent Treasury yields higher, with the 10-year rising from just under 4.4% to briefly over 4.6%. Equity markets took the news hard, with the S&P 500 down roughly 3.5% from pre-meeting levels at time of writing. Part of the weak equity market performance may also have to do with a looming government shutdown. Washington has only a few hours to pass a funding bill into law. Failure to do so will lead to a partial government shutdown. Essential services would continue, but most federal workers wouldn’t receive a paycheck. In addition, some workers would be furloughed until Congress passes new funding. The Bipartisan Policy Center estimates that some 875 thousand federal workers would be furloughed.

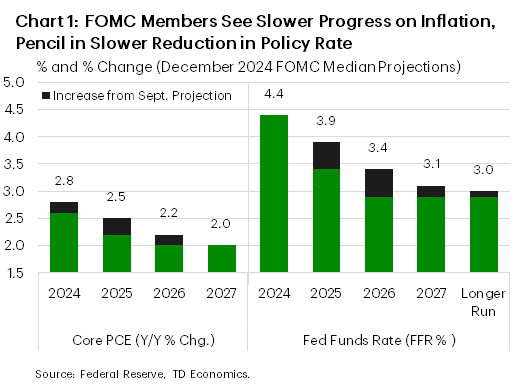

The Fed’s quarter point interest rate cut was as expected, but the accompanying Summary of Economic Projections (SEP) raised a few eyebrows. While the median forecasts for economic growth and the unemployment rate were little changed, the outlook for inflation and the policy rate were raised noticeably (Chart 1). Focusing on the year ahead, the median projection now has the Fed Funds Rate ending next year 50 basis points higher than expected in September. This is in tune with a firmer outlook for core inflation. Asked about the more cautious stance on rate cuts, Fed Chair Powell listed several reasons. These included the economy growing at a better pace and inflation coming in a bit hotter than expected recently. Powell also highlighted an elevated uncertainty around the inflation projections – a theme that was visible in the SEP document, with uncertainty and upside risks to core PCE inflation both up noticeably since September. Pressed on how much of the difference could be explained by the evolving data versus potential policy changes from the new Trump administration, the Fed Chair acknowledged that some policymakers did take preliminary steps to incorporate “highly conditional estimates of economic effects of policies into their forecast at this meeting”.

This week’s economic data buttressed several of Powell’s comments. The third estimate of Q3 GDP indicated that the economy grew at an improved pace of 3.1% annualized, up from 2.8% previously. At the same time, the November personal income and spending report indicated that consumer spending should end the year on solid footing. Consumer spending is on track for a solid 3% pace in the fourth quarter of 2024. That is only a small downshift from 3.5% pace in the third quarter. The November report also carried some better news on inflation, with the Fed’s preferred inflation gauge – core PCE – cooling noticeably in November, up a modest 0.1% month-over-month. While the annual pace remained at 2.8%, this latest cooldown helped reverse near-term trends lower (Chart 2).

This week’s economic data buttressed several of Powell’s comments. The third estimate of Q3 GDP indicated that the economy grew at an improved pace of 3.1% annualized, up from 2.8% previously. At the same time, the November personal income and spending report indicated that consumer spending should end the year on solid footing. Consumer spending is on track for a solid 3% pace in the fourth quarter of 2024. That is only a small downshift from 3.5% pace in the third quarter. The November report also carried some better news on inflation, with the Fed’s preferred inflation gauge – core PCE – cooling noticeably in November, up a modest 0.1% month-over-month. While the annual pace remained at 2.8%, this latest cooldown helped reverse near-term trends lower (Chart 2).

Overall, with the economy remaining on decent footing and inflation seemingly having resumed its downward path, there is room for further policy normalization next year. But, the potential for major policy changes from the new U.S. administration remains a wildcard.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of December 6th, 2024

Financial News Highlights

- The embattled ISM Manufacturing Index showed improvement in November, but continued to point to contraction in financial news. In contrast to manufacturing, the services sector continued to expand in November, although the pace of growth slowed.

- As was widely expected, hiring rebounded in November, with payrolls adding 227,000 new jobs, as impact of the Boeing strike and hurricanes reversed. However, an uptick in the unemployment rate increased market confidence that a Fed rate cut is in the offing.

- Vehicle sales also posted a sizeable gain in November, reaching the highest level in over three years. It is possible that some of this strength in sales came from replacement demand related to hurricane activity.

Data Clears the Path for the Rate Cut in December

It’s not just the Christmas holidays that are fast approaching. The next Federal Reserve meeting is also just around a corner, and this week featured several important updates for signals on the health of the U.S. economy. This week’s results were broadly positive: contraction eased in manufacturing, activity continued to expand in the services sector, job growth rebounded in November, as did vehicle sales. Vehicle sales registered their highest level in over three years, although it is possible that some of this strength came from replacement demand related to hurricane activity.

It’s not just the Christmas holidays that are fast approaching. The next Federal Reserve meeting is also just around a corner, and this week featured several important updates for signals on the health of the U.S. economy. This week’s results were broadly positive: contraction eased in manufacturing, activity continued to expand in the services sector, job growth rebounded in November, as did vehicle sales. Vehicle sales registered their highest level in over three years, although it is possible that some of this strength came from replacement demand related to hurricane activity.

The embattled ISM Manufacturing Index showed improvement in November, but still signaled that activity is contracting. Overall, the manufacturing sector has gained some momentum, with the new orders index rising for the third consecutive month, since the Fed began cutting interest rates. However, regulatory and trade policy cloud the outlook. In contrast to manufacturing, the services sector continued to expand in November, although the pace of growth slowed. Still, with 14 out of 18 industries reporting growth, the services sector appears to be in relatively good shape.

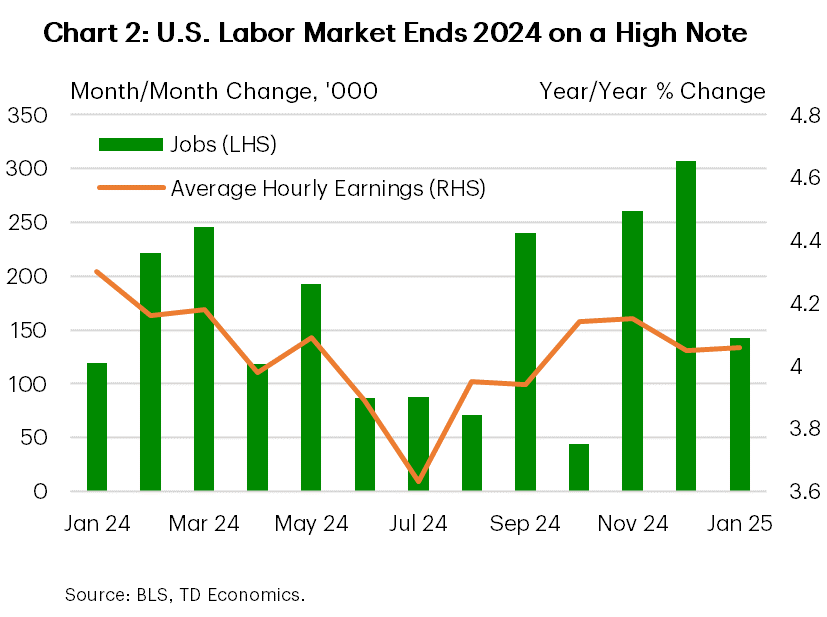

As expected, hiring rebounded in November, with payrolls adding 227k new jobs in financial news (Chart 1). Revisions also added 56k jobs to the gains seen in the prior two months. Smoothing through the recent volatility, job gains have averaged 173k over the past three-months, or only a modest step down from the 186K averaged over the prior twelve-month period. But this likely overstates the degree of “strength” in the job market. In the household survey, the unemployment rate backed up one tenth to 4.2%, after spending September and October at 4.1%.

Other indicators, such as the Job opening and labor turnover survey (JOLTS), similarly point to a labor market that has come into balance and is no longer a meaningful source of inflationary pressure. JOLTS data, released this week, showed that while job openings increased in October, the uptick was narrowly concentrated in professional and business services and leisure and hospitality. Meanwhile, both the quit rates and the hiring rate are below their pre-pandemic levels. This suggests that the employers are becoming more selective, while workers are less eager to leave job voluntarily. Indeed, with no significant premium for job switching (Chart 2) and given the low hiring rate, landing a new job may be challenging.

Other indicators, such as the Job opening and labor turnover survey (JOLTS), similarly point to a labor market that has come into balance and is no longer a meaningful source of inflationary pressure. JOLTS data, released this week, showed that while job openings increased in October, the uptick was narrowly concentrated in professional and business services and leisure and hospitality. Meanwhile, both the quit rates and the hiring rate are below their pre-pandemic levels. This suggests that the employers are becoming more selective, while workers are less eager to leave job voluntarily. Indeed, with no significant premium for job switching (Chart 2) and given the low hiring rate, landing a new job may be challenging.

Comments from the latest Fed’s Beige book also reflected this trend, stating that “hiring activity was subdued as worker turnover remained low” and that “wage growth softened to a modest pace”. The Beige book, along with the payrolls and especially the next week’s inflation report will help to solidify the Fed’s stance on their next rate move later this month. The cooling labor market should give the policy makers confidence for another quarter point cut. However, with inflation showing some stickiness lately, and in the words of Jerome Powell this week, the Fed could “afford to be a little more cautious”. The market is pricing nearly 90% odds of a December cut, but the path for rate cuts in 2025 is less clear (report).

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of November 22nd, 2024

Financial News Highlights

- A quiet week for data with the housing market showing healthy sales activity and Fed speakers recommitting to a data-dependent approach to policy in financial news.

- The focus will be on housing inflation in next week’s Personal Income and Outlays report for October.

- Productivity growth has allowed inflation to cool without sacrificing much growth. Whether that continues through the end of 2024 and into 2025 will be material for Fed policy.

Looking Ahead After a Quiet Week

A brief rally in Treasuries fizzled out this week and, at the time of writing, Treasury yields are roughly back to where they were at Monday’s open. Ultimately, a pair of housing reports coming in roughly in line with expectations and two Fed speakers emphasizing data dependence, leave us looking to next week’s Personal Income and Outlays report as the next sign-post to gauge where the Fed’s rate cutting campaign is headed.

A brief rally in Treasuries fizzled out this week and, at the time of writing, Treasury yields are roughly back to where they were at Monday’s open. Ultimately, a pair of housing reports coming in roughly in line with expectations and two Fed speakers emphasizing data dependence, leave us looking to next week’s Personal Income and Outlays report as the next sign-post to gauge where the Fed’s rate cutting campaign is headed.

Two Fed Board Members took the stage this week – Governor’s Bowman and Cook in financial news. Though they offered slightly different interpretations of the state of the economy both recommitted to a data-dependent approach to rate setting. Governor Cook presented her view of the outlook, with an emphasis that the disinflation process is well on its way “even if the path is occasionally bumpy”. Governor Bowman was more pessimistic noting that, “progress on inflation seems to have stalled”. Markets now expect the Fed’s preferred inflation gauge (the personal consumption expenditure index excluding food and energy) to show another strong advanced in October of 0.3% month-on-month (m/m, 3.7% annualized) – well ahead of the Fed’s 2.0% target. Whether it’s a bump or another sign of stalling will come down to the details of the report.

The good news is that the growth in most goods and services prices has moderated significantly (Chart 1). Goods price trends have been a key part of the recent cooling with prices in both durables and nondurables in deflation over the past several months. There is some worry this benefit could be coming to an end as there was a notable uptick in durable goods prices last month (+0.3% m/m). With retail sales demand still healthy, another price gain can’t be ruled out. Adding to the concern is the prospect that tariffs are around the corner. For policymakers, the end of the downdraft from durable goods prices would come at an inopportune time as it has provided a meaningful deflationary offset to a still-hot housing sector.

The good news is that the growth in most goods and services prices has moderated significantly (Chart 1). Goods price trends have been a key part of the recent cooling with prices in both durables and nondurables in deflation over the past several months. There is some worry this benefit could be coming to an end as there was a notable uptick in durable goods prices last month (+0.3% m/m). With retail sales demand still healthy, another price gain can’t be ruled out. Adding to the concern is the prospect that tariffs are around the corner. For policymakers, the end of the downdraft from durable goods prices would come at an inopportune time as it has provided a meaningful deflationary offset to a still-hot housing sector.

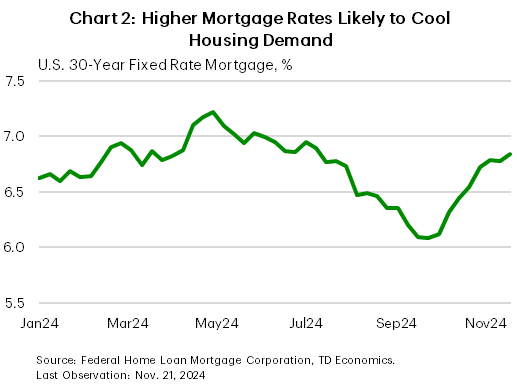

This puts more focus on what kind of print we can expect in the coming months from the housing market. Sales activity clocked in a healthy gain last month amid lower mortgage rates in late summer. However, this is likely to be a temporary burst as affordability is still stretched, and the recent backup in borrowing costs should dent demand (Chart 2). With inventory levels near balanced territory, this should help temper further price gains.

To date, U.S. consumers have benefited from a productivity boom that has allowed inflation to cool without sacrificing much growth. The key concern now is whether this pace of productivity growth can extend into next year. This means looking at the details in the data for signs that demand growth is yet again outpacing supply. Markets currently judge the odds of a Fed cut in December at a coin toss. An upside surprise next week could make it a long-shot.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.