How to Turn Your Nest Egg Into Income for a Confident Retirement

By Jason List, CFP®, CFA

You’ve spent years building a retirement portfolio you can be proud of. However, when it comes to retirement planning, saving is just half the battle. The next step is taking those savings and using them to create a steady income. When you have a well-designed strategy, it allows you to spend more time enjoying retirement.

Step 1: Understanding How Much Will Be Needed Each Year

The first step is getting a general idea of your retirement expenses and your desired lifestyle. Estimate how much you’ll need to spend on these common expenses (and any others you can think of):

- Healthcare

- Housing and home maintenance

- Travel

- Hobbies

- Taxes

- Transportation

In our experience with helping retirees develop a distribution strategy, we find that there are three stages to retirement. In the first stage, people often spend more than they expect to accomplish their bucket-list items. In the second stage of retirement, people tend to spend less. Lastly, in the third stage of retirement, people tend to spend more because of healthcare needs.

While you don’t need to have exact numbers, having a general sense of what you want your expenses to be and how you want to enjoy your retirement builds the foundation for a sustainable withdrawal strategy.

Step 2: Working Out a Sustainable Strategy for Withdrawals

When you create a retirement withdrawal strategy, you’re planning how much money to take from your savings each year. You want to make your savings last, but if you’re overly cautious, you might not be able to enjoy the lifestyle you’d hoped to have in retirement.

Some people choose to follow established rules when creating a withdrawal strategy. The best known of these rules is the 4% rule, which advises withdrawing 4% of your retirement savings in the first year and adjusting each year thereafter for inflation.

However, “rules” like this are more like starting points. We stress the importance of developing a customized withdrawal strategy for each client to account for their longevity, personal goals, and market fluctuations. We help clients build flexible withdrawal strategies that suit their needs.

People often find that they spend more in their 80s and 90s because of healthcare needs. As you are developing your distribution strategy, consider having enough funds to receive the level of care you anticipate.

Step 3: Align Investments for Steady Income

Each person’s portfolio and goals are different. However, we have found that constructing a diversified portfolio provides our clients with income they need while still investing for long-term growth.

We aim to balance stability and growth based on your timeline and risk tolerance. You don’t have to navigate market volatility alone. At Aventus, we continually monitor and adjust your portfolio to keep you on track.

Step 4: Plan for Taxes and Inflation

In retirement, you want to spend your time in meaningful ways, supported by a plan that gives you clarity and confidence about your financial future. It’s smart to make adjustments to your distribution strategy over time, especially when you account for taxes and inflation. We help our clients develop a distribution strategy that seeks to minimize taxes and maximize their after-tax returns.

Move Toward Retirement With Clarity and Confidence

Whether you already have a detailed retirement plan or you’re just getting started, Aventus Investment Advisors is here to help you align your finances with your future vision.

Planning for sustainable income in retirement can be daunting, but we’re here to offer you custom-tailored advice designed to help you achieve your goals.

To schedule a meeting, call (704) 237-4207 or email jason.list@aventusadvisors.com.

About Jason

Jason List, CFP®, CFA, is a Senior Client Advisor with Aventus Investment Advisors in Cornelius, North Carolina. With nearly two decades of industry experience, he helps clients organize, grow, and preserve their wealth through comprehensive planning, investment management, and tax-focused strategies. Clients value his approachable style and the confidence that comes from having a fiduciary partner to navigate life’s milestones, whether retiring, traveling, or buying a new home.

Jason earned his undergraduate degree in mathematics from the University of North Carolina at Charlotte, a master’s in finance from Shanghai University of Finance and Economics, the CERTIFIED FINANCIAL PLANNER® designation in 2012, and the Chartered Financial Analyst® designation in 2024. He joined Aventus in 2021 after working at large financial institutions, drawn to the firm’s focus on personalized, transparent advice.

A Charlotte-area resident for more than 30 years, Jason lives with his wife, Ashley, and their beagle, Mindy. He enjoys traveling, hiking, bowling, and watching sports, and also serves as treasurer for a nonprofit that supports disenfranchised children in Kenya. To learn more about Jason, connect with him on LinkedIn.

Financial News for the Week of October 3rd, 2025

Financial News Highlights

- The U.S. government has shut down all “non-essential” services this week as Congress failed to pass a bill to fund government spending.

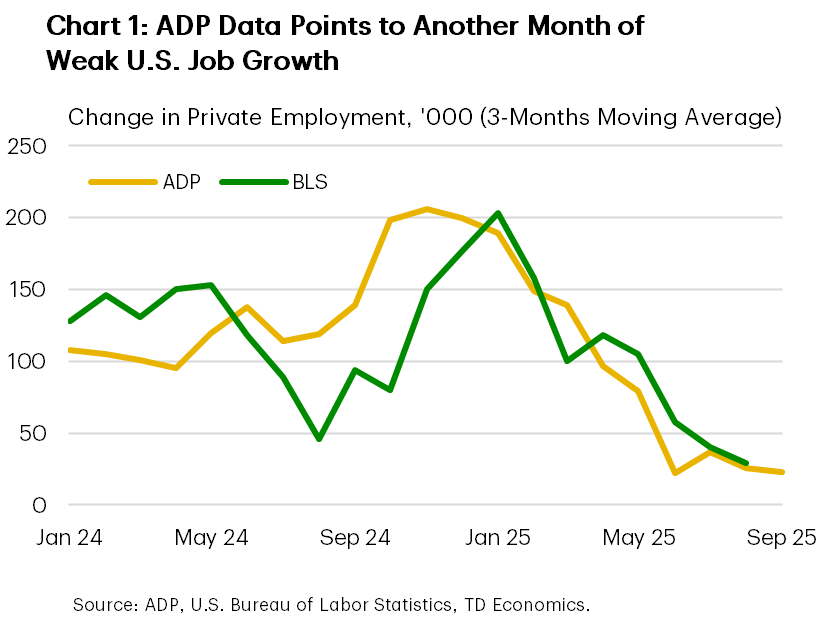

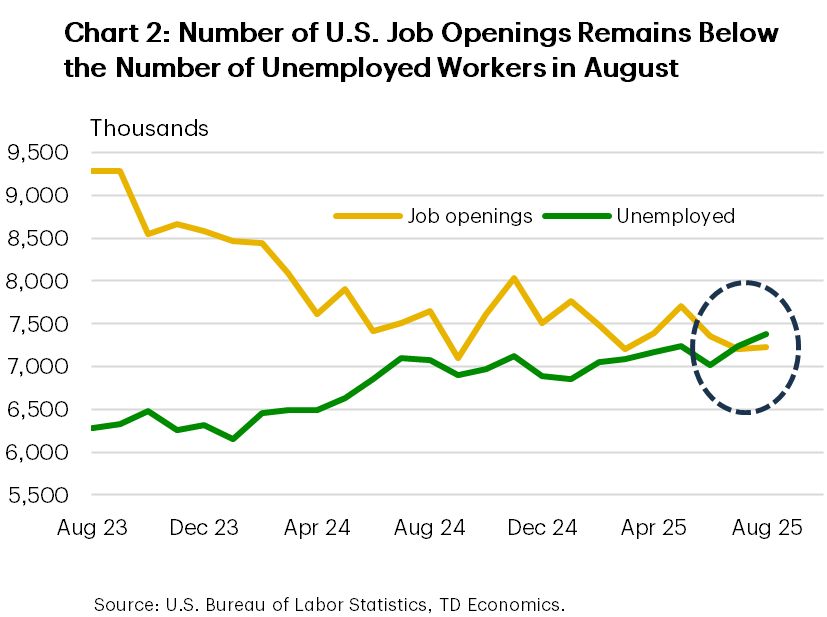

- In the absence of payrolls data, the ADP report took the center stage, and showed that private payrolls declined by 32,000 in September. August’s JOLTS report showed that businesses remained in low hire, low fire mode.

- The ISM manufacturing index rose slightly in September but remained in contractionary territory. Its services counterpart dropped sharply, narrowly avoiding slipping into contractionary territory.

Shutdown Throws a Curveball at the Fed

On October 1st, the U.S. government shut down all “non-essential” services, as Congress failed to pass a bill necessary to fund government in the current fiscal year. Financial markets have shrugged off the shutdown so far, with equities ending the week higher, bond yields declining, and the U.S. dollar weakening only slightly. In past shutdowns in 2013 and 2018, equities and the USD declined modestly and recovered quickly, so the reaction this time is even more muted.

If this shutdown is brief, the markets may be right to discount it. Most lost output in previous shutdowns was eventually recovered. Studies show shutdowns reduce annualized quarterly real GDP growth by up to 0.1 percentage points for each week. However, negative effects increase non-linearly the longer the shutdown lasts as disruptions accumulate (report).

The lack of updated official economic data is another casualty of the shutdown. September’s payrolls release has been postponed. A prolonged shutdown may delay other key indicators like the Consumer Price Index (CPI). A lack of official data complicates decision-making for the Fed. For now, the Fed will have to rely on private and internal data sources. Earlier this week, Chicago Fed President Goolsbee (who is a voting member of the FOMC) echoed that, but also acknowledged that it worries him “that we wouldn’t be getting official statistics at exactly a moment when we’re trying to figure out is the economy in transition.”

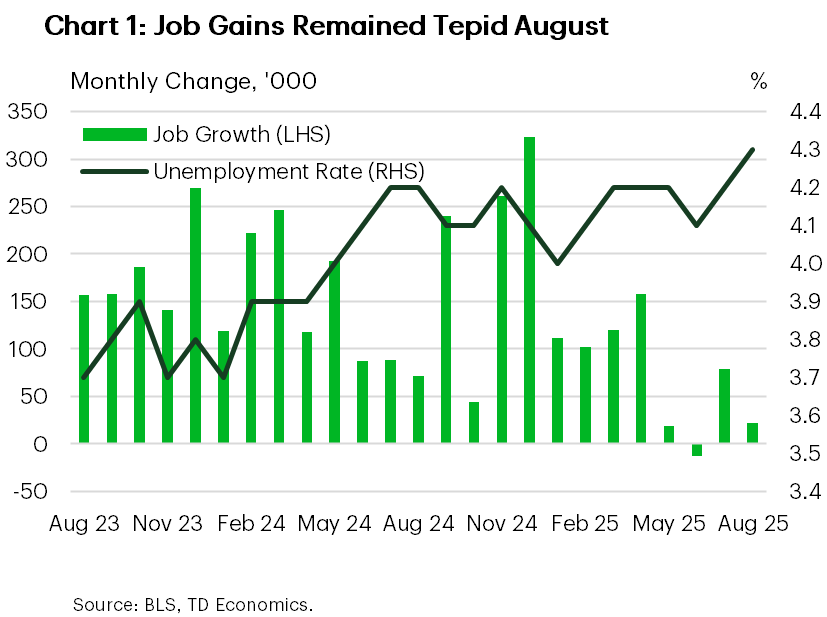

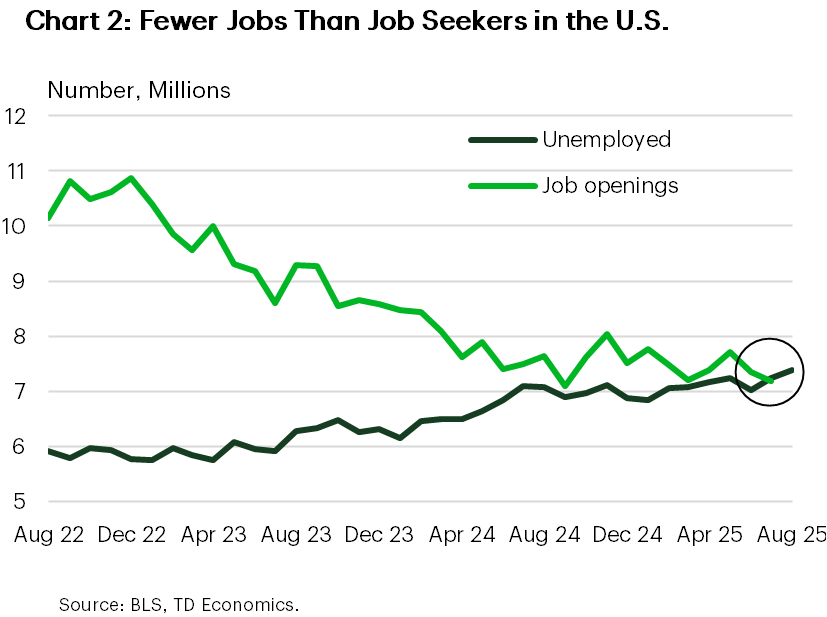

Without official payrolls data, employment surveys—such as ADP and JOLTS—filled the gap. The ADP report showed continued weakness in job growth in September, with private payrolls declining by 32,000. Though ADP data can be volatile, recent trends show greater alignment with payroll figures through 2025, especially on a three-month moving average (Chart 1). The August JOLTS report, released before the shutdown, also showed a hiring drought, with job openings below the number of unemployed for a second consecutive month (Chart 2). Although job opportunities were scarce, layoffs have remained subdued. Employers seem to be in “low hire, low fire” mode, supporting stability in the unemployment rate and helping to cushion consumer spending for now.

In terms of economic growth, ISM indexes pointed to slowing momentum in September, with businesses increasingly citing the growing impact of tariffs on their bottom lines. The ISM manufacturing index edged higher, but remained in contractionary territory, with only 5 out of 18 industries reporting growth. Activity moderated in the services sector, with the ISM non-manufacturing index declining to 50.0 from 52.0, narrowly avoiding slipping into contraction. Details were disappointing: new orders and business activity moderated, prices rose and the employment subcomponent remained in contractionary territory. While limited, this week’s data continues to support the case for additional monetary stimulus from the Fed, with another rate cut in October being nearly priced in by markets.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 26th, 2025

Financial News Highlights

- With the House and Senate unable to pass a continuing resolution and both chambers on recess until next week, a government shutdown looks increasingly likely on October 1st.

- President Trump announced new tariffs on pharmaceuticals, furniture and heavy trucks on Thursday, all effective October 1st. However, exemptions on pharmaceutical tariffs likely mean most drugs will remain duty free.

- Data out this week suggest the U.S. economy is faring considerably better than previously thought, but the softening labor market remains a concern for the Fed.

Waiting on Rates to Change

Numerous Fed speeches, a looming government shutdown, and a handful of new tariff announcements made for a busy week. Chair Powell’s remarks on Tuesday were parsed for any hints surrounding the Fed’s next move. However, Powell stuck to the script, reiterating the challenging environment faced by policymakers due to rising inflation and a weakening labor market. But fears of a softening economy were lessened this week, following an upward revision to Q2 GDP, a healthy read on August personal income & spending and a sharp drop in jobless claims. Meanwhile, President Trump’s announcement on Thursday evening to impose a 100% tariff on pharmaceuticals, 25% on heavy trucks, and 50% on furniture did little to jar markets. The S&P 500 is trading slightly higher on Friday morning but looks to end the week 0.6% lower.

In recent years, the threat of a government shutdown has become a regular occurrence marking the beginning of each new fiscal year. This year appears to be no different. House Republicans passed a ‘clean’ continuing resolution (CR) on September 19th that would have funded the government through November 21st. However, the bill failed to garner the 60-vote majority required to pass the Senate. Meanwhile, Senate Democrats put forward a separate CR, which came with several provisions, including a permanent extension to the expiring expansions of the Affordable Care Act subsidy. The bill had no chance of passing the Senate, but was meant to serve as a stake in the ground from which Democrats hoped to negotiate. However, this all backfired on Tuesday when President Trump cancelled his meeting with top Democratic leaders. With both the House and Senate on recess until next week, odds now heavily favor a government shutdown come October 1st (see report).

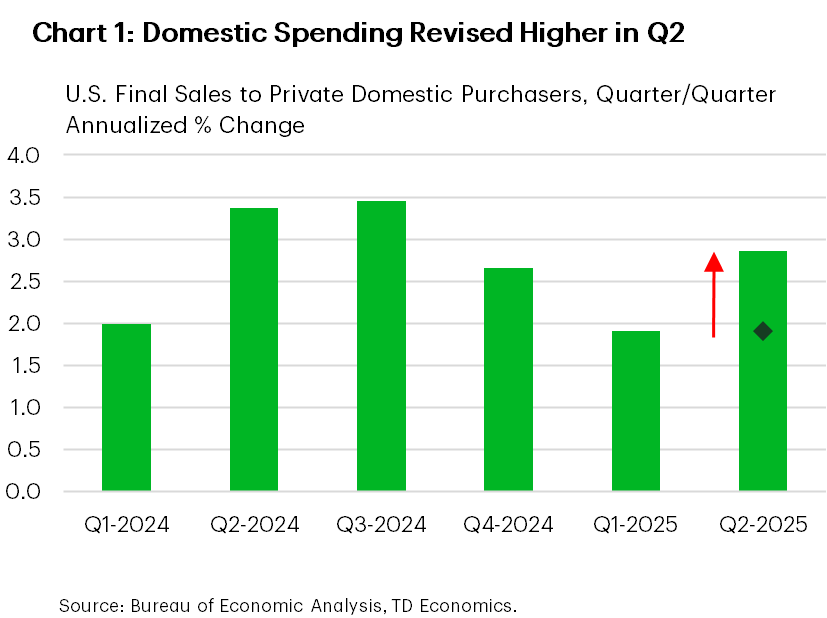

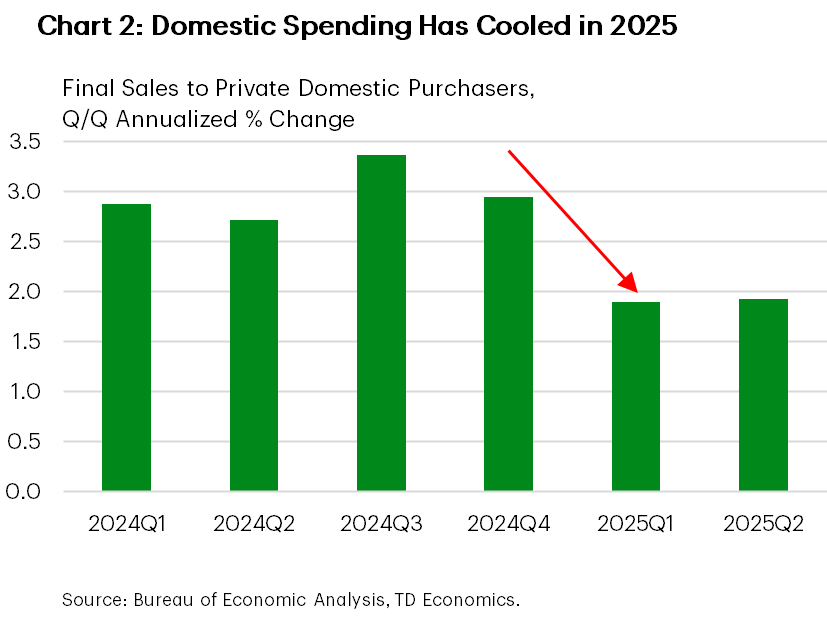

Turning to the economic data, the third revision to Q2 GDP showed a notable upgrade to growth (3.8% from 3.3%). Nearly all the additional strength came from consumer spending on services (2.6% from 1.2%) and business investment (7.3% from 5.7%). As a result, final sales to private domestic purchasers – our best gauge of underlying demand – was revised to 2.9% (from 1.9%), suggesting a more resilient economy (Chart 1).

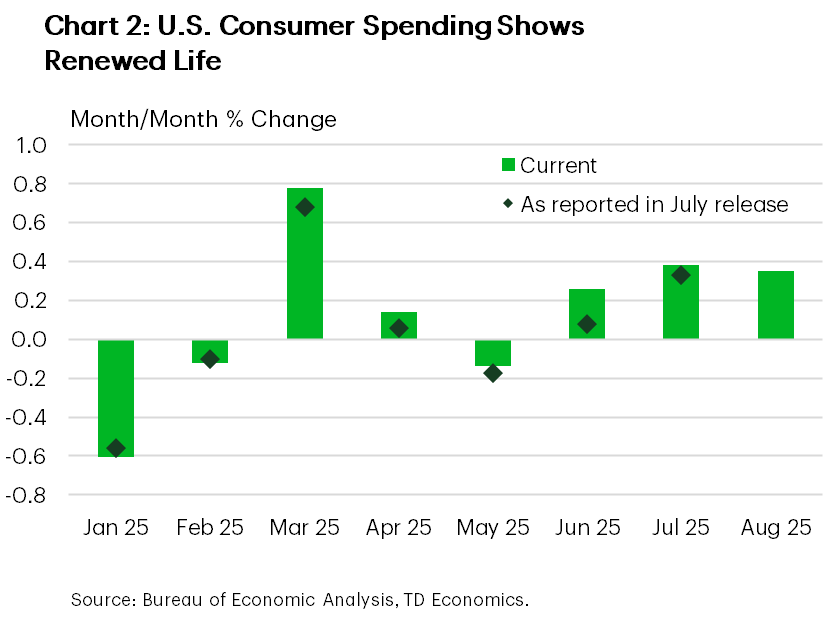

Encouragingly, the new-found momentum looks to have carried into Q3. Personal spending for August advanced 0.35% m/m (Chart 2), while income growth also remained healthy. Elsewhere, durable goods orders – a leading indicator of CAPEX – also came in on the hotter side. After incorporating this week’s data, our Q3 GDP tracking is now north of 3%.

But even with the renewed strength, the labor market remains an ongoing concern for the Fed. Higher frequency data on jobless claims and job openings suggest conditions have stabilized in the ‘low hire, low fire’ environment, but next week’s payrolls report will be key in shaping the Fed’s next move. However, a government shutdown would delay its release, leaving both policymakers and market participants in the dark.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 19th, 2025

Financial News Highlights

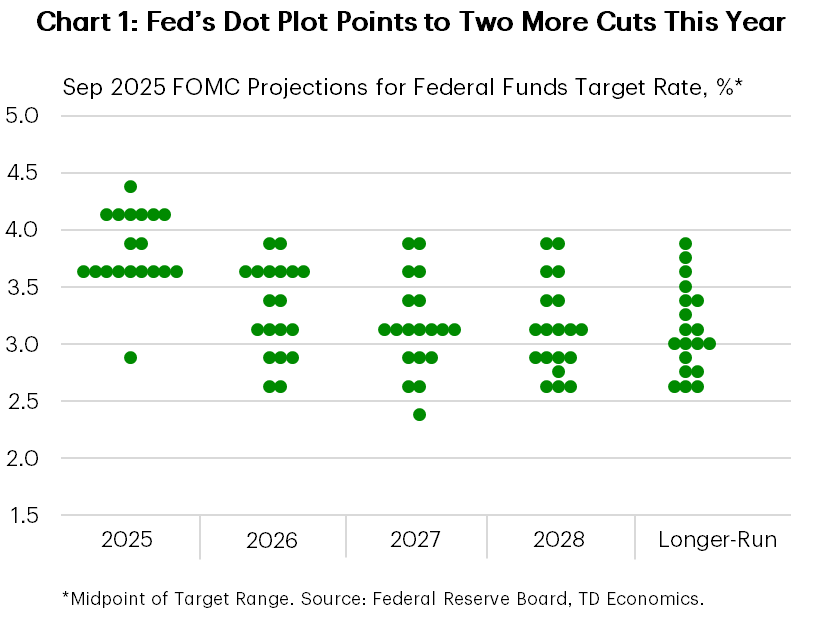

- The Fed resumed rate cuts at this week’s FOMC meeting, lowering the policy rate by 25 basis points to 4.00%-4.25%.

- The Fed’s “dot” plot pointed to two more cuts by the end of this year, but it also showed one member who expects a lot more easing.

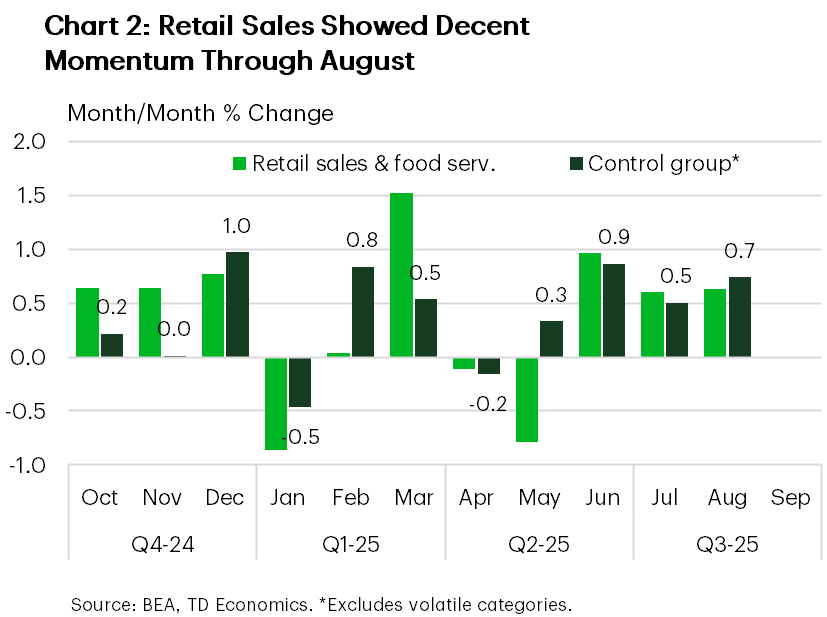

- Retail sales came in better than expected in August, rising 0.6% on the month. Sales in the control group, which strip out volatile categories, rose an even better 0.7%.

Powell’s ‘Risk Management’ Cut

The Federal Reserve resumed its easing cycle after a nine-month pause, cutting the policy rate by 25 basis points at this week’s FOMC meeting. The move was widely anticipated, and while bond yields initially dipped, they ultimately rose as markets digested the broader implications. Equities, however, rallied, with the S&P 500 climbing another 1% on the week at time of writing.

The FOMC statement signaled a shift in emphasis from the ‘price stability’ mandate toward ‘full employment’, noting that “downside risks to employment have risen”. This echoed Fed Chair Powell’s remarks at Jackson Hole last month and set the tone for what he later described as a “risk management cut”. In essence, while inflation remains elevated, the Fed deemed it prudent to begin easing the policy rate to help guard against further labor market deterioration.

The decision was accompanied by the latest Summary of Economic Projections (SEP), which offered a mixed picture. Unemployment rate forecasts were largely unchanged, while growth projections for 2025 and 2026 were nudged up 20 basis points (bps) to 1.6% and 1.8%, respectively. Core inflation expectations for next year were also bumped up by 20 bps to 2.6%, with this measure now projected to return to target only by 2028 – which would mark seven consecutive years above the Fed’s 2% goal. The median forecast now calls for three cuts by year-end (including this week’s) up from two, and is in tune with our expectations. But one member projected the equivalent of three jumbo 50 bps cuts total (Chart 1). Stephen Miran, President Trump’s newly appointed Fed governor, is likely the one projecting more aggressive cuts as he was the lone dissent at this week’s meeting, favoring a larger 50 bps cut.

Economic data released this week did little to bolster the case for continued easing. Initial jobless claims fell back last week, following a surge in the week prior. And while housing remained a soft spot, with homebuilding pulling back in August, consumption-related data came in better than anticipated. August retail sales and food services rose 0.6% on the month, matching July’s gain. Sales in the ‘control group’ – which strip out volatile components – rose a solid 0.7%, building on gains in the prior two months (Chart 2). While tariffs are still expected to chip away at spending power and weigh on consumption, this recent data suggests consumers may still have some gas in the tank.

The bottom line is that while the Fed has resumed rate cuts to guard against further labor market weakness, its “risk management” approach means future moves will remain highly data dependent. The Fed will continue to have a hard time balancing the risks with respect to its dual mandate. But ultimately, we believe that the tariff impact on inflation will be temporary, and we expect the central bank to continue to cuts rates to support the economy (see our latest Quarterly Economic Forecast here).

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 12th, 2025

Financial News Highlights

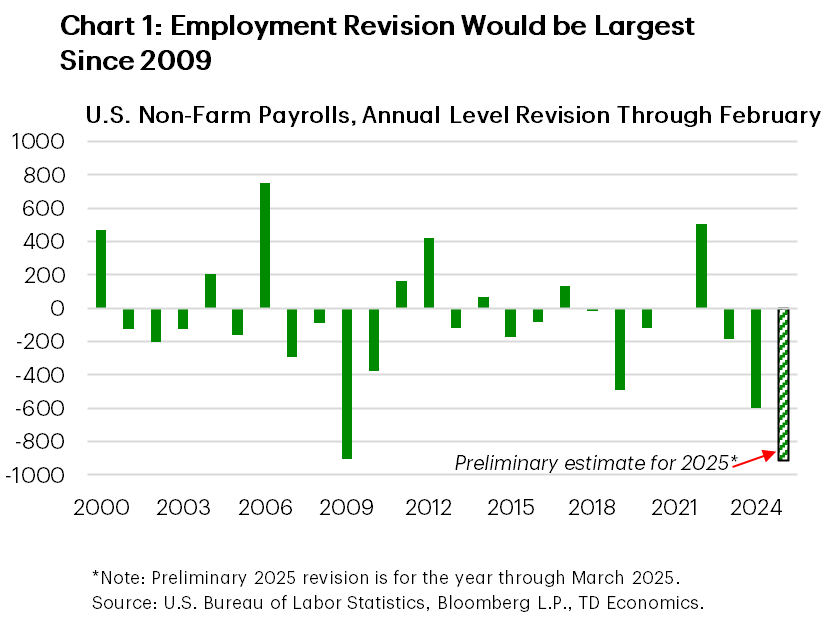

- The preliminary benchmark revisions to the payrolls data through March 2025 suggest that job growth slowed earlier than previously believed, with 911k fewer jobs added in the year through March 2025.

- August’s consumer inflation report showed continued price pressures from tariffs.

- All eyes will now turn to the Federal Reserve meeting next week, with the FOMC expected to implement its first 25 basis-point cut of the year.

Waiting on Rates to Change

Despite there only being a handful of economic data releases this week, each was influential to the economic outlook. This included the preliminary benchmark revision for employment, as well as the consumer and producer inflation reports for August. While the data was somewhat concerning, financial markets largely took it in-stride as expectations for next week’s Federal Reserve decision remained in-tact. The S&P 500 rose 1.6% on the week, with U.S. Treasury yields seeing little change as of the time of writing.

The preliminary revision to non-farm payrolls released on Tuesday will not be incorporated into the official data until the January 2026 release, but the snapshot it provided was concerning. Estimates of employment for the year through to March 2025 were revised lower by 911k jobs, which would be the largest revision since 2009 (Chart 1). This comes on the heels of last week’s employment report for August, which showed only 22k jobs added during the month and the unemployment rate rising to 4.3%. The emerging shift away from full employment in the economy is likely to be a top priority during Federal Reserve deliberations at next week’s meeting.

However, they will also have to assess the emerging risks to the other side of their dual mandate related to price stability, with the data we received this week on inflation also raising concerns. Those with dovish predispositions may point to the surprise decline in the producer price index (PPI) in August as evidence that price pressures are under control. However, the rolling 12-month volatility of the PPI final demand index excluding food & energy has hit its highest level since mid-2022, likely reflecting the impact that constant trade policy changes have had on firm pricing decisions. Single-month changes in the PPI therefore need to be taken with a grain of salt and illustrate the challenges the Fed faces in assessing price developments in 2025.

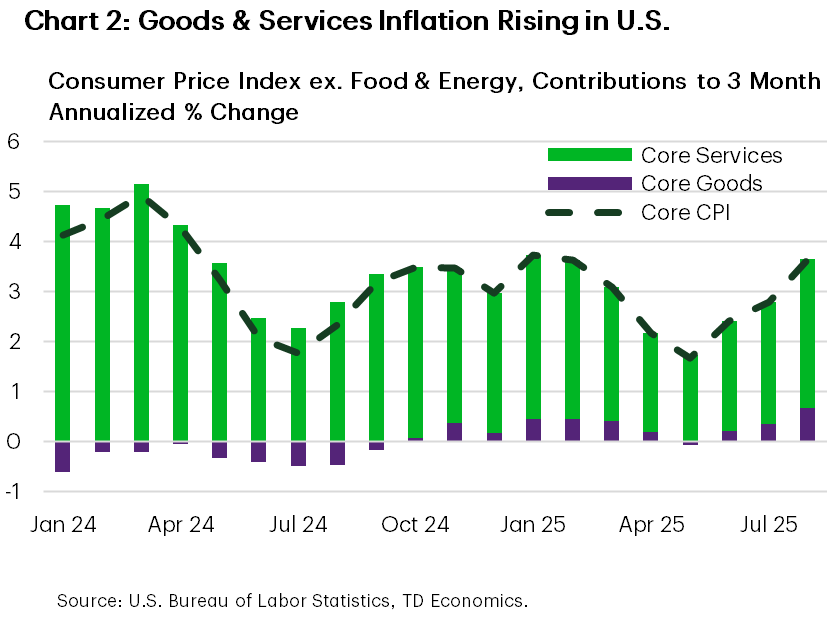

On the consumer inflation front, we saw further upward pressure on goods prices in August, while services inflation also remained elevated. With the three-month annualized percent change in core CPI accelerating to 3.6% in August (Chart 2), the Federal Reserve’s response function would typically be to consider raising interest rates in such an environment, all else equal. However, given the temporary nature of tariff-induced inflation and the flagging labor market, the full balance of risks will need to be taken into consideration. Amid this backdrop, in conjunction with the sustained stability in consumer inflation expectations, we expect the Fed to implement its first 25 basis point cut of the year next week.

Further interest rate reductions are expected to be implemented gradually through the end of the year, to provide support to the economy without fanning the flames of inflation anew. This is expected to be a delicate maneuver by the Federal Reserve, and one that will be sensitive to the balance of incoming economic data.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 5th, 2025

Financial News Highlights

- Financial markets were volatile this week. Bonds and equities sold off at the start of the week only to reverse course later as soft labor market data started to trickle in.

- ISM manufacturing and non-manufacturing indexes moved higher on month, driven by gains in new orders, however, employment subcomponents remained in contractionary territory.

- The job market continued to lose momentum in August, with payrolls gains disappointing and downward revisions to prior months. The unemployment rate also rose to a new cycle high.

Low Hiring, Low Firing… Lower Fed Funds Rate

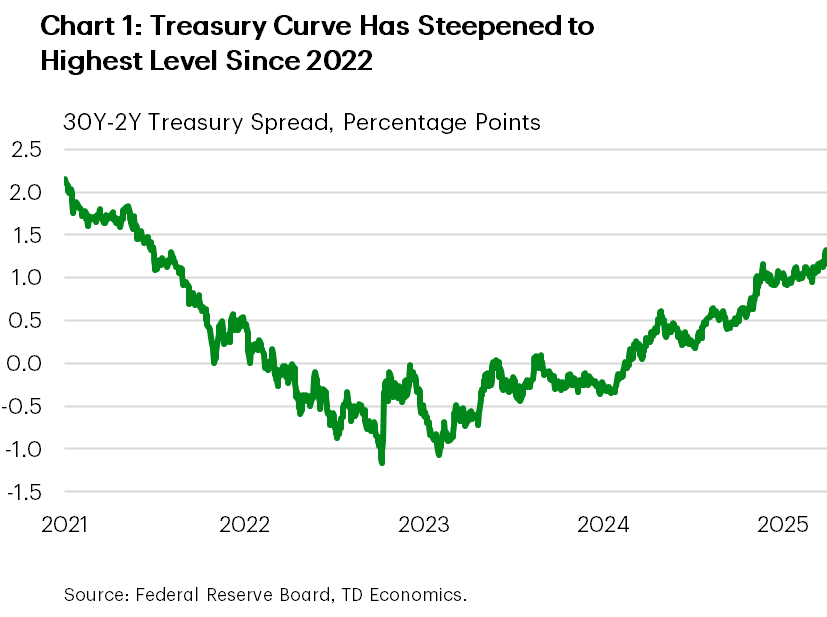

This was a short but volatile week in financial markets. Earlier in the week, equities and bonds sold off amid growing concerns about the long-term sustainability of government debt in the U.S. and other developed nations. These concerns stemmed from increased borrowing needs and reduced demand for government bonds, particularly from central banks. Long-dated bonds were particularly under pressure, with the gap between 30-year and 10-year Treasuries rising to 0.7 percentage points—the highest since 2021.

In the U.S., fears were amplified by questions around the Federal Reserve’s independence and inflation risks linked to tariffs. Adding to the fiscal alarm was a court ruling that IEEPA tariffs were imposed illegally. The case now heads to the Supreme Court, and if the decision stands, it could jeopardize this revenue stream and leave the government liable for billions in refunds.

However, sentiment reversed on Wednesday, with bond yields falling and equities rising. It was a classic case of “bad news is good news,” as softer-than-expected economic data – namely the lower job openings in the JOLTS report – boosted expectations of more aggressive rate cuts from the Fed. Given last month’s downward payroll revisions and modest job gains, investors were already on alert for signs of ongoing labor market weakness ahead of Friday’s payroll report. They didn’t have to look too hard.

August’s payroll report confirmed that the labor market is softening quite quickly (Chart 1). Job growth was well below expectations in August, with just 22k new jobs added, and has averaged only 29k over the past three months (see commentary). Goods-producing industries, especially those exposed to tariffs, continued to shed jobs for a fourth straight month. Government employment also declined. The services sector added 63k jobs, but gains were not broad-based. Education & health added 46k jobs and 28k were in leisure & hospitality. While employers are not rushing to hire, they aren’t cutting jobs en masse either. Still, the jobless rate edged up to 4.3% from 4.2% the prior month, reaching a new post-pandemic cyclical high.

Playing second fiddle to the payrolls number, the July JOLTS data also surprised with weaker-than-expected job openings, which declined to 7.18 million from 7.36 million. Openings also fell below the number of unemployed for the first time since 2021—though the margin has been narrow since mid-2024 (Chart 2). Quits and layoffs were little changed, suggesting the economy remains in a “low hiring, low firing” state.

Fed officials have recently become more concerned about the downside risks to the labor market, and the August payrolls report shows these concerns are valid. As such, we maintain our view that the Federal Reserve would need to deliver 75 basis points in rate-relief this year, with the first one coming in less than two weeks.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of August 29th, 2025

Financial News Highlights

- President Trump is attempting to remove FOMC member Lisa Cook, sparking further concerns of Fed independence.

- Real GDP growth for the second quarter was revised higher to 3.3%, with most of the upward revision stemming from stronger business investment.

- Real consumer spending rose 0.3% m/m in July, thanks to a strong gain in motor vehicle sales & parts. Meanwhile, annual core PCE inflation hit a five-month high of 2.9%.

President Trumps Applies Further Pressure on Fed

President Trump continued to pressure Federal Reserve officials this week, this time attempting to fire Governor Lisa Cook for alleged mortgage fraud. The situation remains influx, as Cook is contesting the President’s actions in court. But the mere threat of her removal has sparked further concerns of central bank independence, sending shorter-term yields lower. The yield curve steepened on the week, with the 30-to-2-year spread widening to its highest level since early-2022 (Chart 1). Meanwhile, equity markets largely shook off the news, as investors’ attention remained squarely focused on this week’s earnings reports, including Nvidia and several large retailers. The S&P 500 briefly hit another all-time on Thursday, but retraced on Friday and looks to end the week slightly in the red.

Turning to the economic data calendar, the Bureau of Economic Analysis released its second estimate of Q2 real GDP. Relative to the first release, economic growth was revised higher by 0.3 percentage points to 3.3%. While net trade remained a major source of growth, a good chunk of the upward revision came from stronger business investment, specifically in categories that are likely tied to AI investments. In fact, spending on ‘computers & other peripheral equipment’ and ‘software’ accounted for all the growth in business investment through the first half of 2025.

Final sales to private domestic purchasers – the best gauge of underlying domestic demand – was raised from 1.2% to 1.9% and is now on-par with Q1’s rate of expansion. While this marks a deceleration from H2-2024 (Chart 2), it suggests the narrative of ongoing economic resilience hasn’t completely fizzled out amid ongoing trade uncertainty.

This point was further underscored in the Gross Domestic Income (GDI) figures, which accompany the second estimate of GDP and serve as an alternative measure of economic output. Real GDI rose a healthy 4.8% in Q2 – up from a flat reading in Q1. Corporate profits rose 7% annualized, despite elevated cost pressures from tariffs, while household income also continued to expand at a +5% clip.

Despite the healthy gains in income, households have become increasingly selective in their spending. Real PCE rose 0.3% month/month in July, with most of the gains coming from an increase in durable goods. Vehicle sales had a heavy hand in the uptick, as consumers appear to be pulling forward purchases to get ahead of tariff price increases which will likely materialize later this year once OEMs roll over to 2026 models. But it’s the discretionary services spending that remains weak, a theme that has played out through most of this year and something that’s unlikely to change until households have more certainty about the economic outlook.

With inflationary pressures heating up, this is unlikely to come anytime soon. Core PCE inflation rose 0.3% m/m, pushing the year-ago measures to 2.9% – a five-month high. Hotter services inflation was the major driver in last month’s uptick, something that is likely to further embolden Fed hawks. This puts next week’s employment report sharply in focus. Consensus currently expects payrolls to add 75k jobs in August. A stronger reading could push back on the odds for a September rate cut, which is currently 90% priced in.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of August 15th, 2025

Financial News Highlights

- Inflation pressures rose in July, with core CPI rising above 3% for the first time since February. Meanwhile the uptick in PPI suggests a shift to higher tariff passthrough by companies.

- Retail sales recorded healthy growth in July despite growing price pressures.

- The S&P 500 hit a double-digit year-to-date return after rising 1% on the week, which would mark the third consecutive annual double digit return if unconceded by year-end.

Price Pressure Firms in July, Equity Markets Undeterred

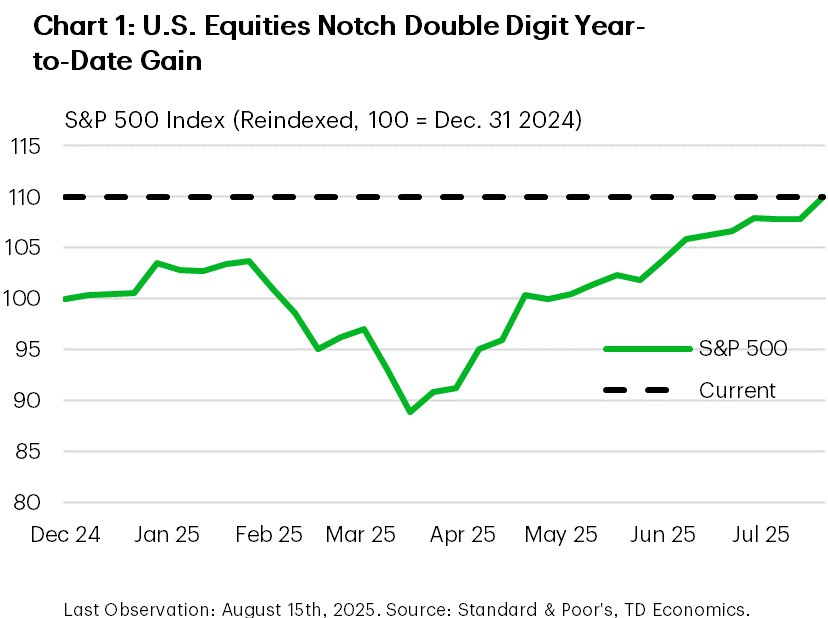

It has been one week since the full complement of reciprocal tariff policies went into effect. Those tariffs will not have an influence on the economic data for a few months, but the tariffs that prevailed through the first half of the year continued to show up in the July inflation readings released this week. This included the CPI and PPI, both of which showed signs of rising price pressures that are expected to trend higher over the coming months with the new tranche of tariffs now in effect. Largely undeterred, equity markets continued to probe record highs, with the S&P 500 rising 1.0% on the week and notching a double digit return year-to-date (Chart 1).

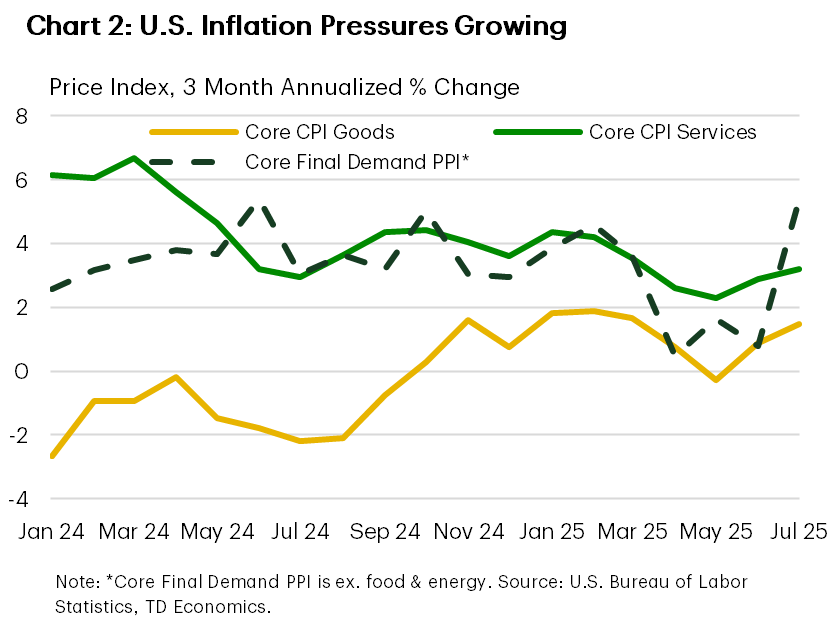

The first inflation report we received on Tuesday showed consumer price growth accelerating in July, with the annual percentage change in core CPI rising above 3% for the first time since February. This was driven by stronger core goods prices, largely related to higher tariff passthrough, while core services inflation also trended higher (Chart 2). Producer prices, which we received on Thursday and measure the prices charged by U.S. businesses, also began to trend notably higher in July with the monthly change hitting a 3-year high. This likely suggests that businesses are shifting to pass on more of the higher costs associated with tariffs to consumers after largely absorbing the costs in the first half of the year. Moving forward, with the effective U.S. tariff rate nearly 10 percentage-points higher after last week’s reciprocal tariffs came into force, inflationary pressures are expected to remain elevated through the second half of the year.

The Federal Reserve has been acutely attuned to these developments, with the central bank remaining on hold since the start of the year. Although a few Federal Reserve officials have advocated for rate reductions, the balance of the FOMC continues to voice caution regarding the uncertainty surrounding the outlook for inflation and the economy. The officials we heard from this week, including regional Fed presidents Schmid (Kansas City) and Goolsbee (Chicago) who are voting members of the FOMC this year, noted that caution was still warranted. Market pricing fluctuated this week, but currently has 90% odds for a rate cut in September. The annual Jackson Hole Symposium next week will be watched closely after this week’s inflation reports for any signs on the leanings of officials in the run-up to the next Federal Reserve decision in one month.

On a more positive note, retail spending appeared to remain healthy in July, growing 0.5% month-on-month. However, July also had Amazon’s multi-day Prime day event which tends to boost sales activity. A non-outsized reading could suggest that consumption is beginning to slow in line with the downward revisions to the labor market recorded in the second quarter. This is part of the reason why Federal Reserve officials have continued to advocate for caution, noting that it will take time to properly assess the state of the U.S. economy amid the fog of various shifts in trade policy.

Next week, we’ll receive the FOMC meeting minutes for July as well as the July reading for PCE inflation which should help formulate expectations for September’s Fed meeting. With trade policy uncertainty waning gradually, the attention of markets will shift back towards the Fed.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of August 8th, 2025

Financial News Highlights

- As of August 7th, dozens of U.S. trading partners face significantly higher tariff rates, pushing the U.S. effective rate to roughly 19%.

- July’s reading of ISM services provided further evidence that the U.S. economy is stagnating, with employment, new-orders and business activity all turning lower.

- Following last week’s employment report, Fed officials appear to be pivoting their communication. A September cut is more likely than not.

U.S. Economy Stagnating Just as Tariff Rates Reset

It was a quiet week on the economic data calendar, but with earnings season in full swing, further trade announcements, and several Fed officials out speaking, there were no shortage of developments for investors to sift through. To say this earnings season has gone better than expected would be an understatement. At this point, over 80% of companies included in the S&P 500 have reported second-quarter earnings. According to Reuters, after factoring in analysts’ forecasts for the remaining 20%, profit growth is tracking close to 12% annualized. That’s more than double what was expected just one month ago, and has without question been a driving force sustaining the recent strength in equities. At the time of writing, the S&P 500 is up 2% on the week and 8.5% on the year. Meanwhile, term-yields climbed a bit higher on the week, even after President Trump appointed Stephen Miran to complete Adriana Kugler’s brief remaining term on the FOMC, and more dovish leaning Governor Waller was reported to be the frontrunner for Fed Chair.

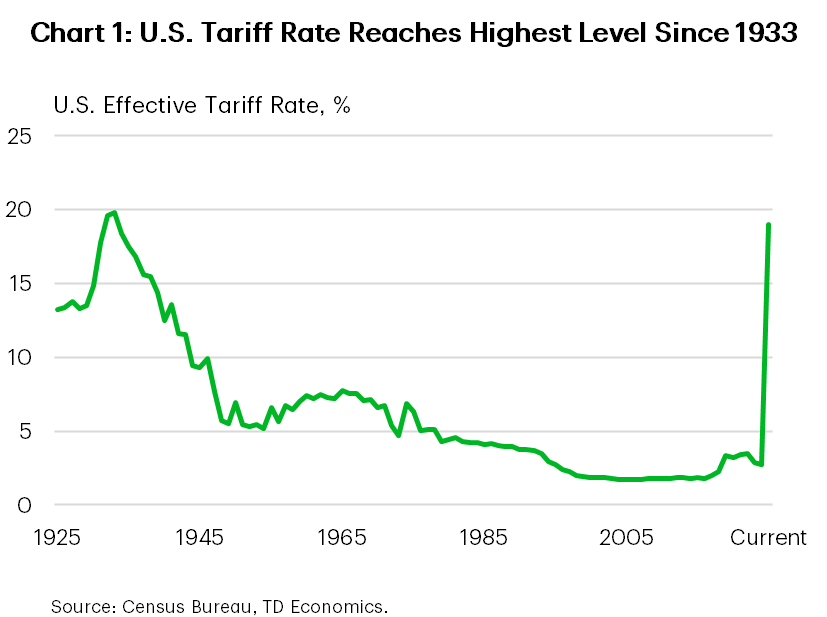

But we would argue that the run in equity markets this year is built on a shaky foundation. Inventory stockpiling and a haphazard rollout of the administration’s tariff policies meant that many businesses were able to circumvent or significantly limit tariff exposure last quarter. But that’s not going to continue. As of August 7th, dozens of trading partners now face significantly higher tariffs as per the Executive Order released by the White House on July 31st. By our estimates, the current effective tariff rate in the U.S. is around 19%, or the highest level since 1933 (Chart 1).

Over the near-term, it’s very likely that the U.S. tariff rate pushes even higher. The Trump administration singled out India this week, threatening an additional 25% tariff on August 27th and hinted at further tariffs on semiconductors – potentially as a 100% – and pharmaceuticals over the coming weeks.

While the economy had demonstrated unwavering resilience earlier in the year, more recent data has shown that ground is starting to shift. This week’s ISM services report provided further evidence that the economy is slowing, with the services index slipping to 50.1 or just barely remaining in expansionary territory. Details of the report came with plenty of ‘stagflationary undertones’, with new-orders, business activity and employment all turning lower, while the prices paid sub-component remained near its cyclical high.

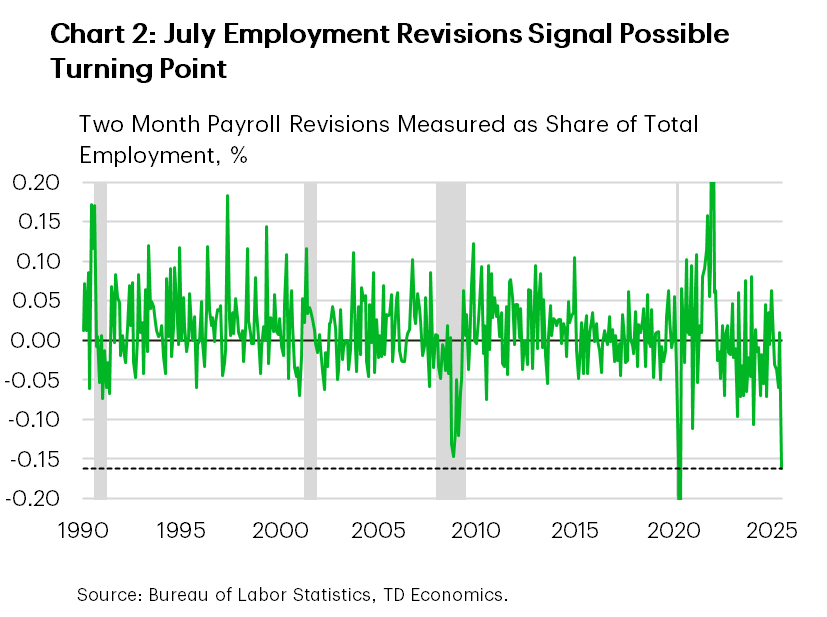

The shift in economic data has led Fed officials to pivot on their communication, with regional Fed President’s including Neel Kashkari and Mary Daly – neither of whom are voting members – to suggest that rate cuts are coming in the months ahead. Meanwhile, Governor Cook characterized last week’s tepid jobs report as ‘concerning’ and noted that the significant downward revisions to the May/June figures, which were some of the largest on record, are ‘typical of turning points in the economy’ (Chart 2). Next week’s CPI inflation data will shed more light on the extent of tariff passthrough, but even that is feeling somewhat backward looking given this week’s reset on tariff rates. Ultimately, the weakness in the labor market cannot be ignored and (in our view) solidifies the case for a September rate cut.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of July 11th, 2025

Financial News Highlights

- Trade tensions heated up this week, as President Trump announced higher tariffs on 23 trading partners as well as a 50% tariff on copper imports as of August 1st in financial news.

- If implemented, the combined announcements would add over 2 percentage points to the U.S. effective tariff rate, bringing it to a near century high of 17%.

- Minutes from the June 17th-18th FOMC meeting showed a growing divide among policymakers on when to resume rate cuts. A September rate cut is currently 63% priced in by Fed futures markets.

Trade Fireworks in July

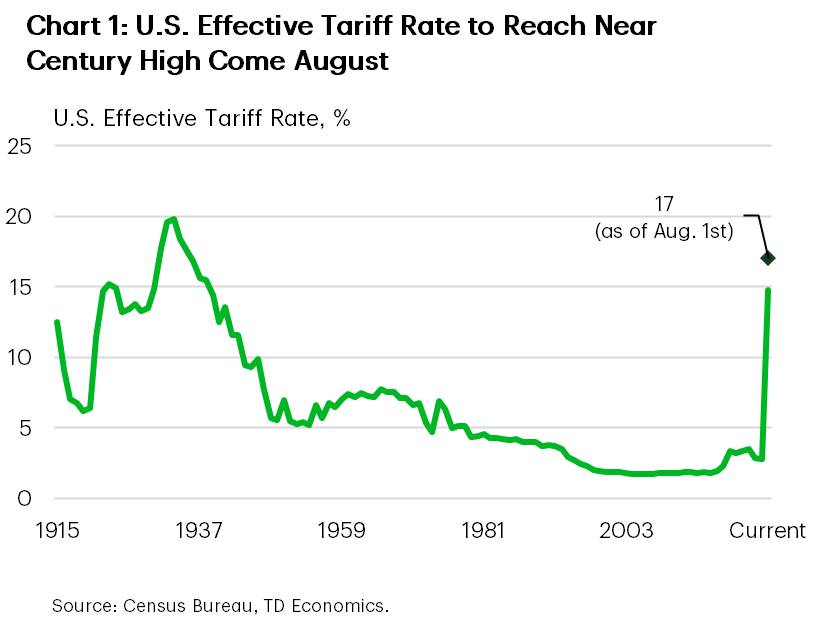

Financial markets were jittery to start the week, with the 90-day delay on the April 2nd “reciprocal tariffs” set to expire on Wednesday in financial news. While President Trump ultimately extended the deadline for another few weeks, he simultaneously ratcheted up trade threats on various fronts. He announced a 50% tariff on all copper imports, raised the tariff rate on Brazil to 50% and Canada to 35%, all effective August 1st. For Canada, the details remain sparse, but it’s assumed that all exports that are USMCA complaint – which is just under 60% of goods – would remain exempt from these tariffs. In addition, the administration sent letters to 21 other countries, including larger trading partners like Japan and South Korea, also threatening significantly higher tariffs come August. In total, the 23 countries put on notice account for $827B (or 25%) of annual U.S. imports – after accounting for USMCA compliance. Combined, these additional tariffs would raise the effective tariff rate by 2.2 percentage points if they come into effect August 1st, bringing it to 17%, or the highest level in nearly a century (Chart 1).

Financial markets were jittery to start the week, with the 90-day delay on the April 2nd “reciprocal tariffs” set to expire on Wednesday in financial news. While President Trump ultimately extended the deadline for another few weeks, he simultaneously ratcheted up trade threats on various fronts. He announced a 50% tariff on all copper imports, raised the tariff rate on Brazil to 50% and Canada to 35%, all effective August 1st. For Canada, the details remain sparse, but it’s assumed that all exports that are USMCA complaint – which is just under 60% of goods – would remain exempt from these tariffs. In addition, the administration sent letters to 21 other countries, including larger trading partners like Japan and South Korea, also threatening significantly higher tariffs come August. In total, the 23 countries put on notice account for $827B (or 25%) of annual U.S. imports – after accounting for USMCA compliance. Combined, these additional tariffs would raise the effective tariff rate by 2.2 percentage points if they come into effect August 1st, bringing it to 17%, or the highest level in nearly a century (Chart 1).

Investors appear to be taking the latest trade escalation in stride. U.S. equity markets briefly hit a new record high on Thursday, but then retraced on Friday in response to President Trump’s tariff threats on Canada. The S&P 500 looks to end the week 0.4% lower but is still up 6% on the year. Meanwhile, longer-term Treasury yields were a touch higher on the week, despite another healthy 10-year Treasury auction on Wednesday. As of the time of writing, the 10-year sits at 4.41%.

But the recent calm that has descended over global financial markets feels eerily tenuous, particularly amidst the ongoing shifts in trade policy and Q2 earnings season set to kickoff next week. Last quarter, much of the guidance companies were providing was purely speculative, as tariff policies were only in the early stages of being rolled out and were also changing on an almost daily basis. However, now that the tariffs have been in place for some time, companies are likely in a better position to gauge their impact and provide updates to earnings guidance for the second half of the year.

But the recent calm that has descended over global financial markets feels eerily tenuous, particularly amidst the ongoing shifts in trade policy and Q2 earnings season set to kickoff next week. Last quarter, much of the guidance companies were providing was purely speculative, as tariff policies were only in the early stages of being rolled out and were also changing on an almost daily basis. However, now that the tariffs have been in place for some time, companies are likely in a better position to gauge their impact and provide updates to earnings guidance for the second half of the year.

With the inflation impact so far proving more subdued than previously expected, there’s been a growing divide among FOMC members on when to resume rate cuts. Minutes from the June 17-18 meeting released on Wednesday showed that while most committee members favor delaying cuts until there’s more certainty on the inflation and labor market impacts, recent speeches suggest that two board members – Governor Waller and Bowman – support cutting rates as early as July.

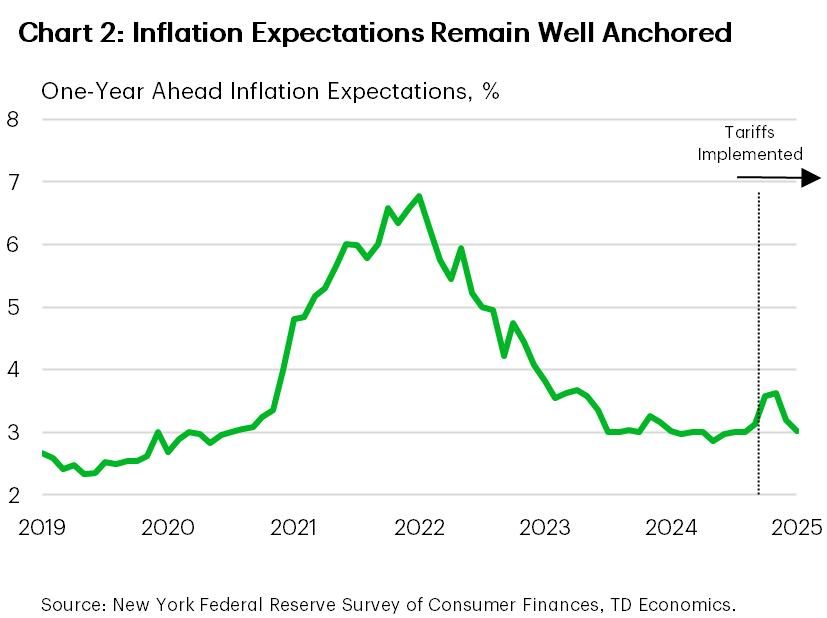

This puts next week’s CPI inflation release under the spotlight. We expect the June CPI report to show inflation having strengthened, with both goods and services price pressures having heated up relative to May. But at this juncture, the uptick is unlikely to unnerve policymakers, particularly with inflation expectations remaining well anchored. According to the New York Fed’s Survey of Consumer Expectations, one-year ahead inflation expectations fell to 3.0% in June – returning to its pre-tariff levels (Chart 2). In our view, this supports the Fed remaining on the sidelines until at least September.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.