Financial News for the Week of March 13th, 2026

Financial News Highlights

- The intensifying conflict in the Middle East continued to push global energy prices higher, as elevated uncertainty regarding the conflict’s duration weighed on financial markets.

- Inflation data for February, which pre-dated the uptick in energy prices, registered an annual reading of 2.4% ahead of next week’s Federal Reserve meeting.

- The U.S. announced new Section 301 tariff investigations covering dozens of countries, confirming that the administration will continue to levy tariffs in the wake of the Supreme Court ruling striking down the IEEPA tariffs.

Geopolitical Risks Keep Market on Edge

Financial markets faced another week of volatility as the conflict in the Middle East intensified. Iranian attacks against vessels passing through the Strait of Hormuz and energy infrastructure in the region has kept energy prices elevated, with oil prices remaining in the $90-100 per barrel range through the end of the week. The announcement that International Energy Agency member countries would release strategic oil reserves provided some relief to the tumult in financial markets, but on aggregate, the near-term risk outlook for the global economy remains elevated. As of the time of writing, the S&P 500 is down 1.2% and the U.S. 10-Year yield is up 14 basis points on the week to 4.27%.

The U.S. remains partially insulated from the spike in global energy prices as a net energy exporter, but the conflict is still expected to create a light headwind for growth this year. The duration of the conflict and its impact on energy prices remains highly uncertain, but the recovery time for energy markets is expected to be measured in months not weeks. This will likely weigh on U.S. consumers and businesses over the near-term.

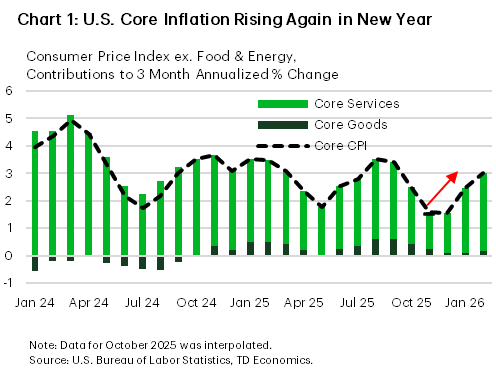

Inflation data for February, which pre-dated the rise in global energy prices, showed that inflationary pressures were still somewhat elevated to start the new year. The 3-month annualized percentage change in core CPI was back at 3% in February after briefly falling in the post-shutdown period (Chart 1). With energy prices rising sharply and tariff cost passthrough still occurring in the background, elevated inflation pressures are likely to keep the Federal Reserve cautious moving forward. As of the time of writing, financial markets have priced in a one-third chance of the Federal Reserve remaining on hold through this year.

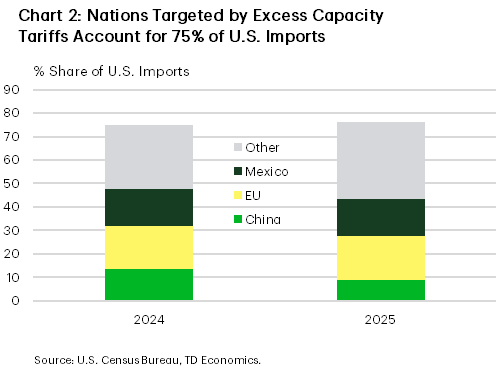

On the tariff front, U.S. Trade Representative Greer announced several new Section 301 tariff investigations covering dozens of countries this week. Section 301 tariffs are imposed against nations engaging in unfair/anti-competitive trading practices which disadvantage U.S. commerce. The first investigation announced on Wednesday relates to “structural excess capacity and production in manufacturing” which will target 15 countries and the E.U. The targeted countries account for roughly 75% of U.S. imports, with the E.U., Mexico, and China accounting for 40-50 percentage-points of that share (Chart 2). The other Section 301 tariff investigations relate to the failure of foreign nations to effectively prohibit the importation of goods produced using forced labor and targets the 60 largest U.S. trading partners. With the global 10% Section 122 tariff imposed last month set to expire at the end of July, the administration is likely to expedite these investigations to create a new tariff regime roughly equivalent to what was in place before the IEEPA tariffs were stuck down.

Looking ahead to next week, the Federal Reserve is widely expected to hold rates steady. However, investors will be keenly watching for their views on the balance of risks amid the spike in oil prices and elevated uncertainty. The labor market has weakened in recent months, but inflation pressures appear likely to keep inflation well above 2% through the year. Chairman Powell is likely to reiterate the data dependency of the FOMC and the need for patience to monitor the sustainability of emerging trends.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of March 6th, 2026

Financial News Highlights

- Global equity markets sold off this week, while energy prices pushed meaningfully higher following the United States and Israel’s strikes on Iran.

- Despite this week’s sharp move in oil prices, the impact to the U.S. economy remains relatively small, but that assumes the conflict is short-lived.

- The February employment report came in on the softer side, with hiring declining and the unemployment rate ticking higher.

Epic Fury Sends Shockwaves Through Financial Markets

The United States and Israel launched coordinated strikes on Iran over the weekend, prompting retaliatory counterattacks across other countries in the Middle East. On Monday, Iran announced that it would attack tanker ships passing through the Strait of Hormuz – a crucial choke point for 20% of global oil supply. Based on satellite imagery, shipping through the passage has effectively come to a halt. Energy prices pushed meaningfully higher this week, with WTI up roughly 33% (or $18per-barrel) and currently sits just north of $88 – its highest level since September 2023. U.S. equities were under pressure for most of the week, with February’s softer employment report adding further insult to injury on Friday. The S&P 500 looks to end the week down over 2%. Meanwhile, Treasury yields across the curve were about 20 basis points higher, as market participants pushed out the timing of expected rate cuts amid fears that higher oil prices will add further upward pressure to inflation.

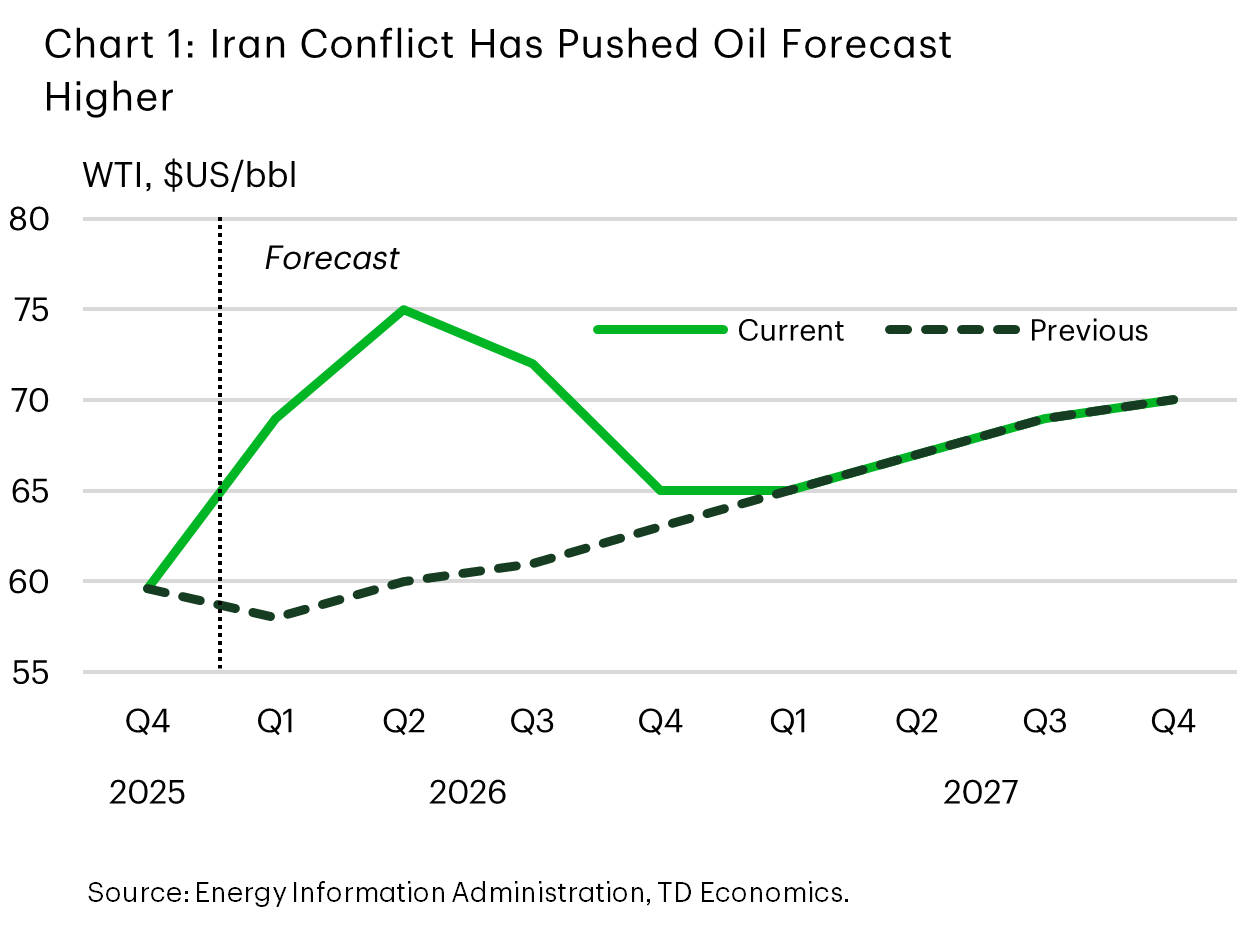

Despite the sharp move in oil prices, the impact to U.S. economy (so far) remains relatively small. In large part, that’s because the U.S. is now a small net exporter of oil, so energy shocks don’t pack the same punch that they used to. Case in point: we’ve marked-to-market our oil forecast, and the upgrade (shown in Chart 1) only shaves about a tenth of a percentage point from 2026 GDP growth – barely moving the needle considering our forecast of 2.7%.

But to say that uncertainty is elevated at the moment would be an understatement. President Trump and other administration senior officials have said this week that the conflict could drag on for at least another several weeks. This suggests further upside to oil prices over the near term, particularly if oil supplies were to remain choked off indefinitely.

From the Federal Reserve’s perspective, economic theory would tell us that policymakers should “look through” the energy shock given its supply driven nature. But because the jump in oil prices is coming atop already elevated inflationary pressures, Fed officials are likely to keep a close eye on inflation expectations. So far, market-based measures have remained well anchored, but there is a risk that they could start to drift higher, particularly if the conflict were to drag on.

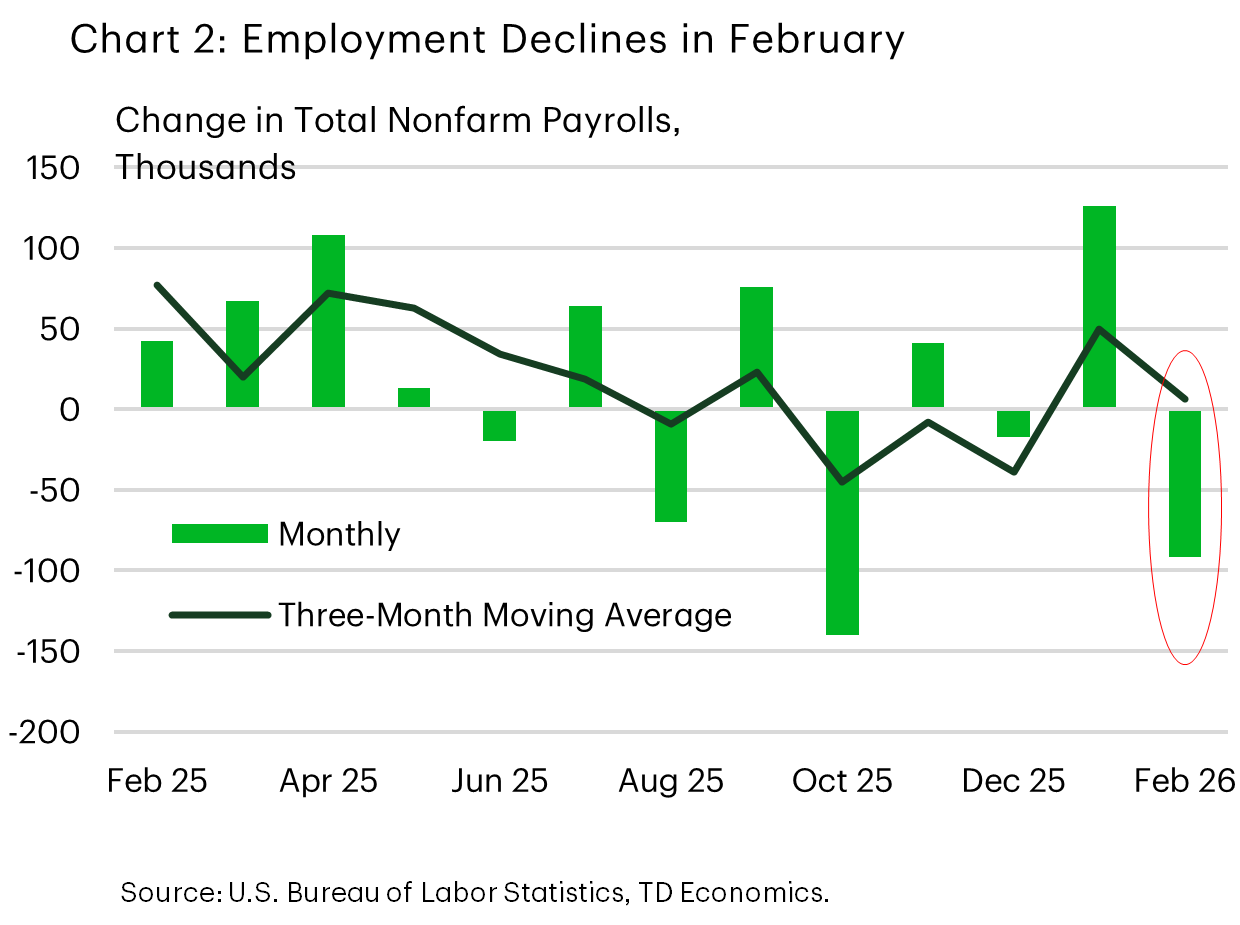

The further upside risk to the inflation outlook comes at a time when market participants have started to question the labor market narrative. Nonfarm employment unexpectedly declined in February (Chart 2), while the unemployment rate ticked up to 4.4%. On the surface, the employment report looked very weak, but there were a few factors including a strike and potential weather-related impacts that contributed to at least some of last month’s pullback. We feel it’s still too early to upend our prior thinking of the labor market – but it certainly underscores that current conditions are far from perfect. At the moment, the greater threat to the Fed’s dual mandate is price stability. That is reflected in market participants having pushed out the timing of next rate cut until September and are only 80% priced for a second cut.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of February 20th, 2026

Financial News Highlights

- A Supreme Court decision on Friday struck down a large chunk of President Trump’s second-term tariffs.

- January FOMC minutes reinforced a shift in the balance of risks toward inflation, with policymakers signaling little urgency to resume rate cuts.

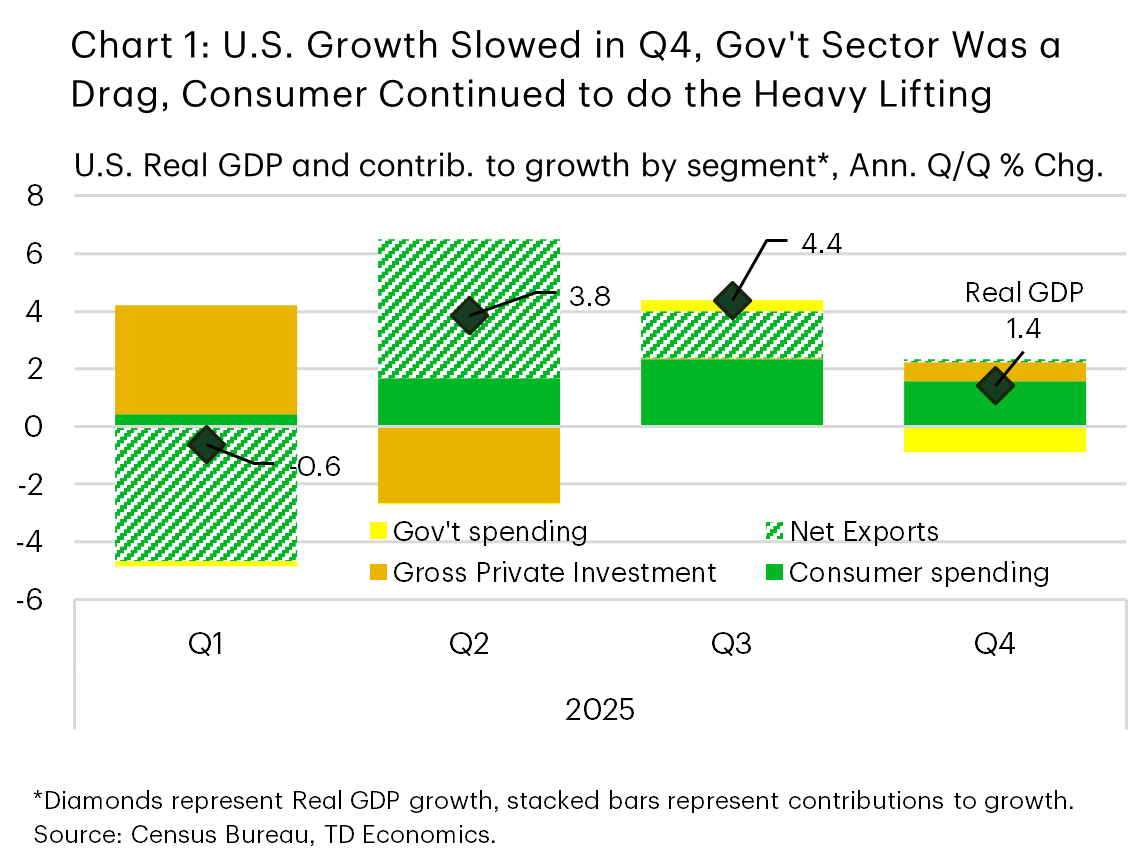

- GDP growth cooled to 1.4% at the end of 2025, reflecting a sharp contraction in federal outlays. Core PCE inflation rose to 3.0% y/y in December, remaining well above target.

Markets Blink, Jobs Hold Firm

Financial markets were largely rangebound for much of this week as investors digested the January FOMC minutes and an important run of macro data. Early market reaction to the Supreme Court’s decision to strike down a large chunk of President Trump’s second term tariffs appears broadly positive, with the S&P 500 is up 0.9% from last week’s close at time of writing.

The Supreme Court ruling found that the law that underpins many of Trump’s global tariffs – the International Emergency Economic Powers Act (IEEPA) – “does not authorize the President to impose tariffs”. The decision did not rule on how or if tariffs that have already been paid should be refunded – a potentially messy process. We expect the U.S. administration will act quickly to recreate its tariff regime using justification from other statutes. For more on this, see our commentary here.

Prior to the tariff decision, the January FOMC minutes dominated the financial market limelight. Two key takeaways stood out from the minutes. First, the balance of risks has shifted away from labor market weakness and toward inflation staying uncomfortably high. Driving home this point was the fact that most committee members judged that “downside risks to employment had moderated, while the risk of more persistent inflation remained”. Importantly, this assessment occurred before the release of last week’s delayed payrolls report, which showed a firmer labor market than many feared. Second, most participants judged that the current policy rate is closer to neutral rather than restrictive. That assessment diminishes the urgency to resume rate cuts.

his week’s macro data broadly echoed the tone of the minutes, even as growth was weaker than expected at the end of 2025. Fourth-quarter GDP growth came in at 1.4% annualized in the first estimate, a notable slowdown from 4.4% in the third quarter (Chart 1). The disappointment was driven largely by a steep pullback in federal outlays, reflecting the 43-day government shutdown. Importantly, final sales to private domestic purchasers rose 2.4%, underscoring the resilience of underlying private sector demand despite the headline slowdown.

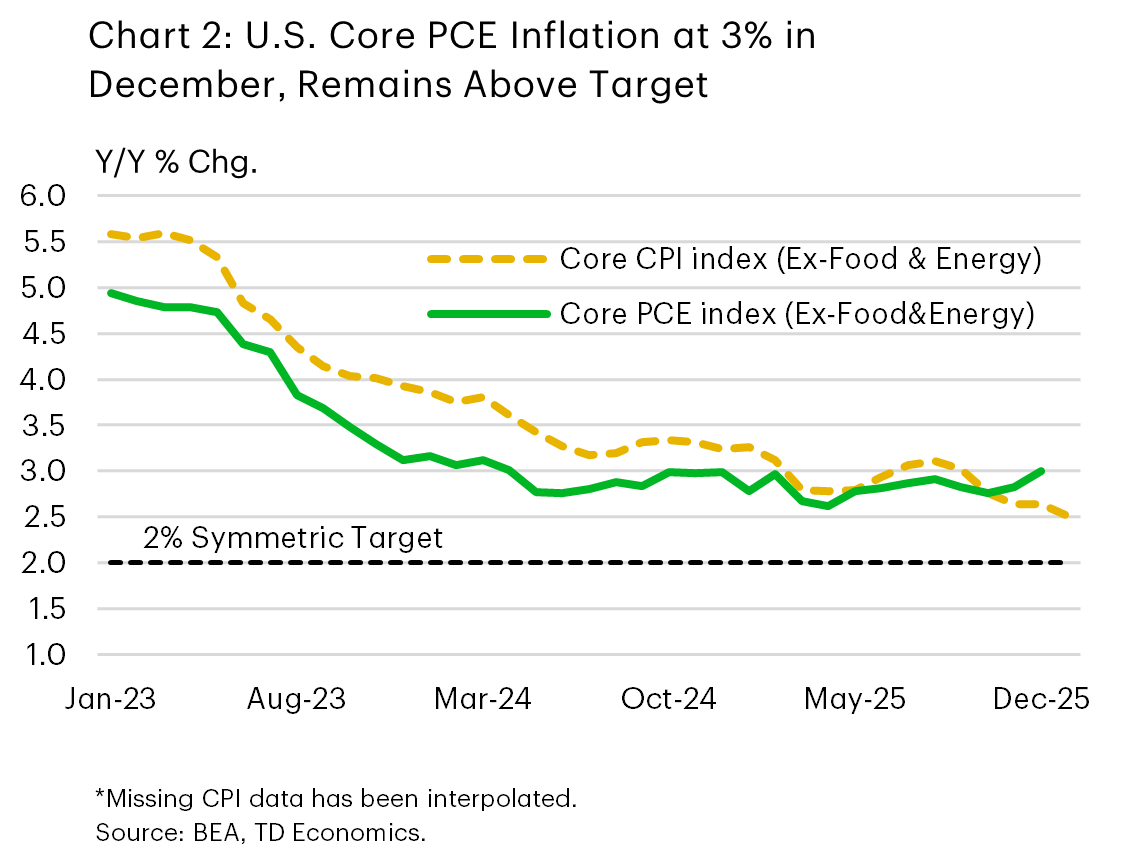

The December personal income and outlays report added further color to the economic backdrop at year‑end. Real consumer spending was up just 0.1% m/m in December, reflecting a pullback in goods spending. Inflation pressures, meanwhile, re‑accelerated at the margin. Core PCE inflation rose to 3.0% y/y, remaining well above target (Chart 2).

All told, even after accounting for this morning’s miss on Q4 growth, we still feel that the U.S. economy has entered 2026 with considerable momentum. That said, it appears that 2026 may start off in similar fashion to 2025 after all – with elevated tariff uncertainty. This reinforces the notion that the Fed will remain on hold for the time being, as it waits for the policy fog to clear.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of February 13th, 2026

Financial News Highlights

- Financial markets sold off this week as developments in AI and tech raised doubts about future earnings.

- January’s employment report delivered a clear upside surprise, easing concerns that the labor market was rolling over after last year’s slowdown.

- In other important data releases, there were softer signals from consumer spending and housing. Inflation had a softer-than-expected headline number, but some cautionary signs of inflation pressures in the core.

Markets Blink, Jobs Hold Firm

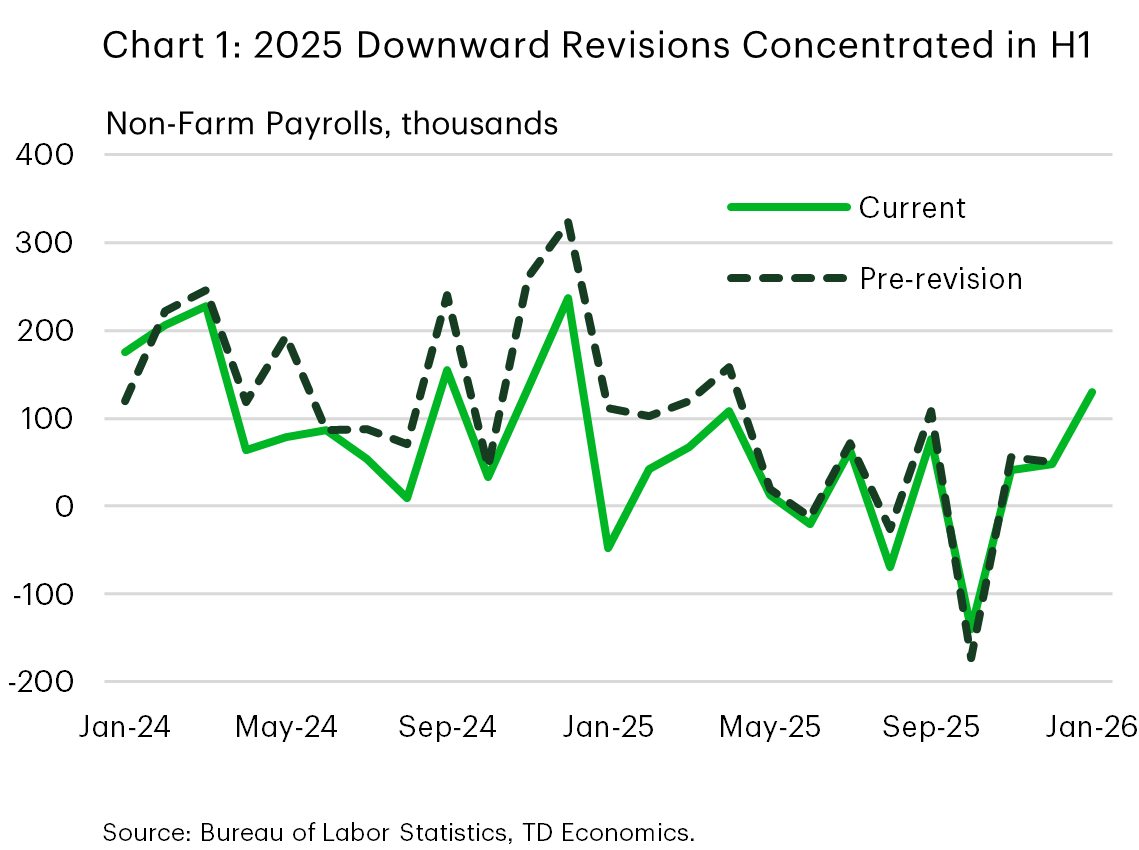

Financial markets endured a rough patch this week, with a broad sell off across equities reflecting anxiety about the threat AI could pose to earnings and employment, the path of interest rates, and the durability of the ongoing expansion. That market reaction stood in contrast to the message from the January employment report. Payrolls growth came in well ahead of expectations, accompanied by a further dip in the unemployment rate. While revisions did reveal that job growth over much of 2025 was weaker than previously thought, the January rebound suggests that labor demand remains intact (Chart 1).

The rest of the data flow painted a more mixed picture of the economy. Headline CPI inflation came in softer than expected this morning, but core CPI picked up the most since August. Services inflation heated up while core goods inflation (excluding used vehicles) rose at its fastest monthly pace in nearly a year. The inflation report comes at a pivotal moment, as reports that the Trump administration may scale back its steel and aluminum tariffs suggest the administration is conscious of inflation risks.

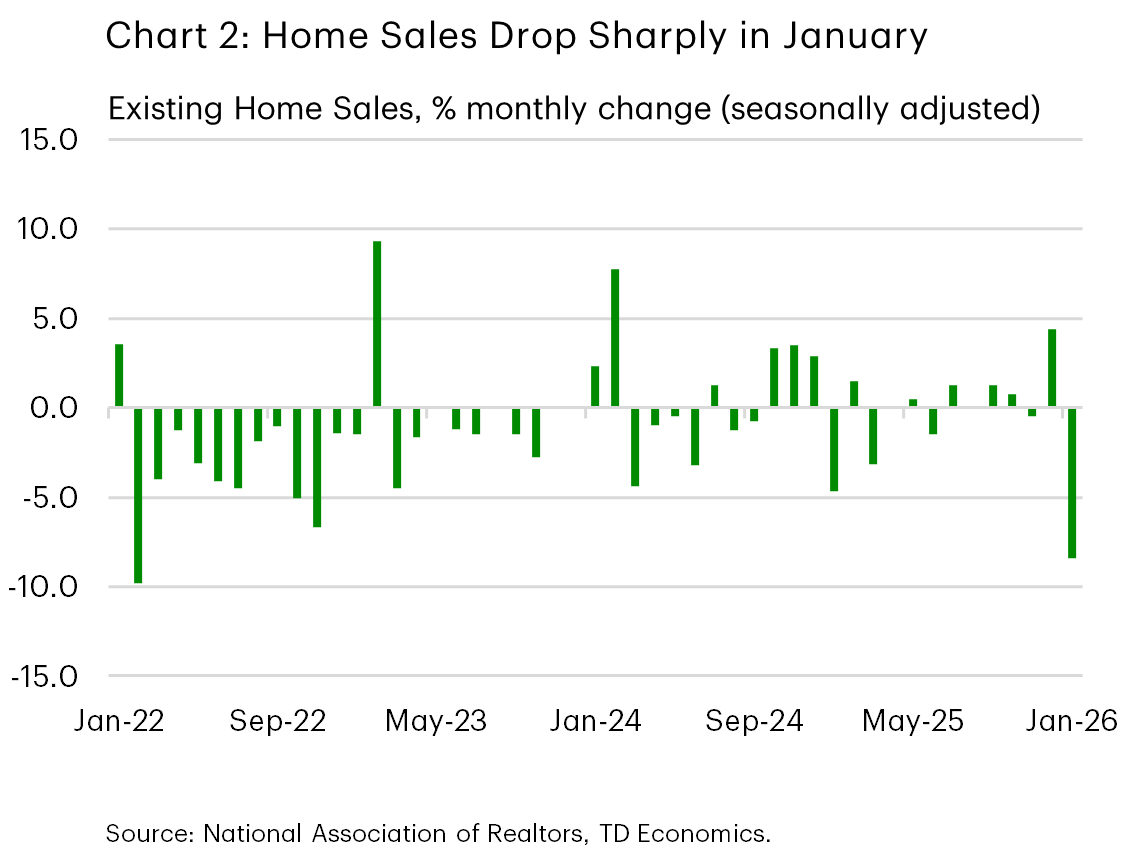

Retail sales ended 2025 on a soft note. December sales were flat after a solid November, and downward revisions tempered the momentum implied by earlier releases. Housing data were also notably weak. Existing home sales posted their largest monthly decline in nearly four years in January, reflecting a combination of affordability constraints and bad weather (Chart 2).

Markets, meanwhile, struggled to reconcile the week’s macro data with a less accommodating policy backdrop. The equity sell off reflected concerns about growth-sensitive sectors and fear that advancements in AI may dislodge large incumbents across a wide swath of the economy, and a reassessment of the path for interest rates following a string of Fed communications. Market pricing for the Federal Reserve to reduce rates in its June meeting have fallen from 60% to around 50% over the course of this week. Speeches this week from Federal Reserve officials revealed a balance of opinion. More hawkish voices stressed that inflation remains above target and warned against premature easing, while others acknowledged that, even with a strong jobs report, there is still an argument for rate cuts later this year if disinflation continues. On balance, we read the prevailing sentiment from Fed officials as one of patience rather than urgency, but still hold on to our call for a rate cut in June. This morning’s softer CPI release may help move the Fed’s perceived balance of risks slightly towards easing, particularly if the disinflationary pressure were to persist over the coming months.

Looking ahead, our eyes will be on next week’s release of the FOMC meeting minutes, which should provide additional insight into how policymakers have been weighing inflation risks against signs of labor market stabilization. And next Friday’s PCE inflation and consumer spending data will be helpful in assessing the durability of consumer spending and the extent of momentum in recent inflation data.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of February 6th, 2026

Financial News Highlights

- Congress passed legislation to fund most of the government through September, with a 2-week continuing resolution used for the Department of Homeland Security.

- The ISM Purchasing Managers Index reports showed solid growth in manufacturing and services activity in January, suggesting the economy entered 2026 on a solid footing.

- January data releases for employment and inflation next week will be closely monitored for potential risks related to the Fed’s dual mandate.

U.S. – Shutdown Ended, Labor Market Concerns Linger

The first week of February was eventful on several fronts. The partial government shutdown, which began over the weekend, ended on Tuesday as the House managed to pass the requisite spending bills. Funding for the Department of Homeland Security was provided by a 2-week continuing resolution - which expires on February 13th - as both parties continue to negotiate the details of the department’s funding. Despite the positive news, financial markets had a tough week, with the S&P 500 down 0.7% as of the time of writing, owing in part to investor concerns regarding the impact of AI on existing business models.

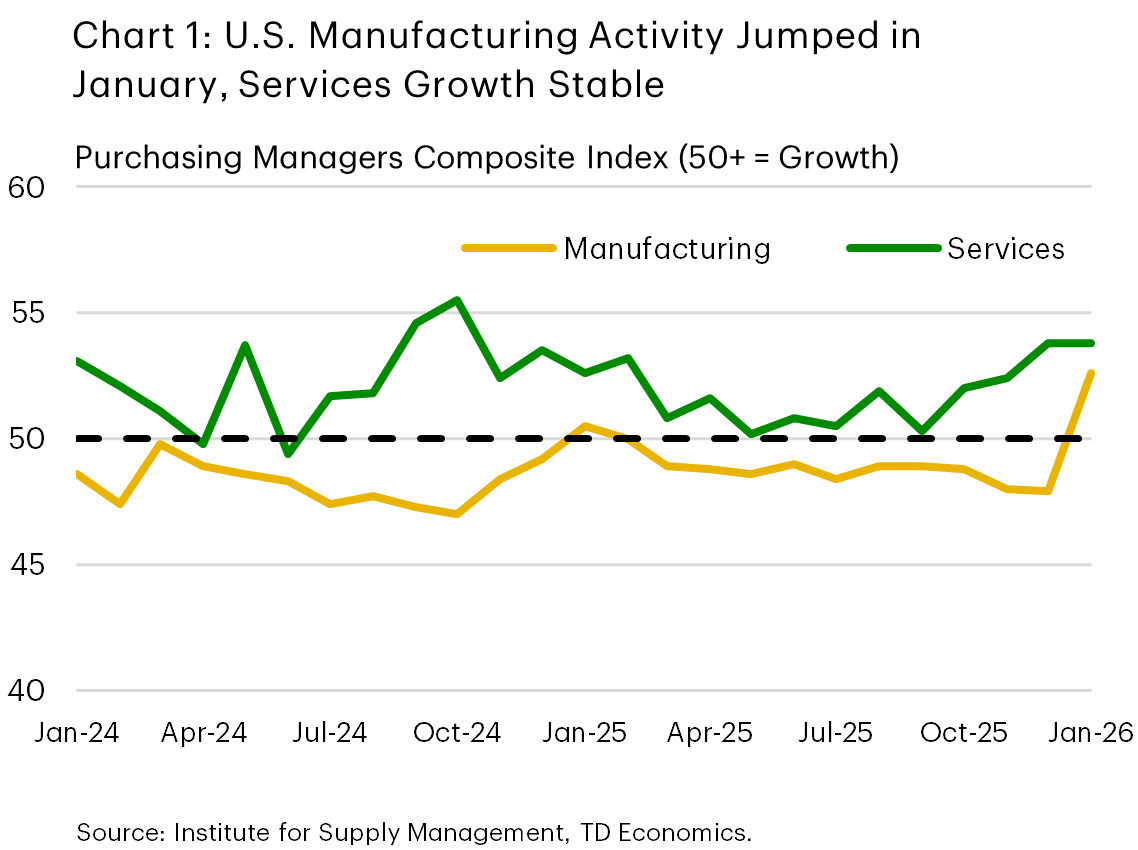

On the economic data front, the ISM Purchasing Manager Index (PMI) reports showed a substantial uptick in manufacturing activity in January (Chart 1). However, survey respondents noted that this was at least partly owing to post-holiday inventory replenishment and front-loading activity ahead of potential new tariffs on Europe and other nations. The services PMI also pointed to growth in activity in January, although the acceleration recorded in recent months eased. On aggregate, these reports suggest economic activity remained on a solid footing to start the new year.

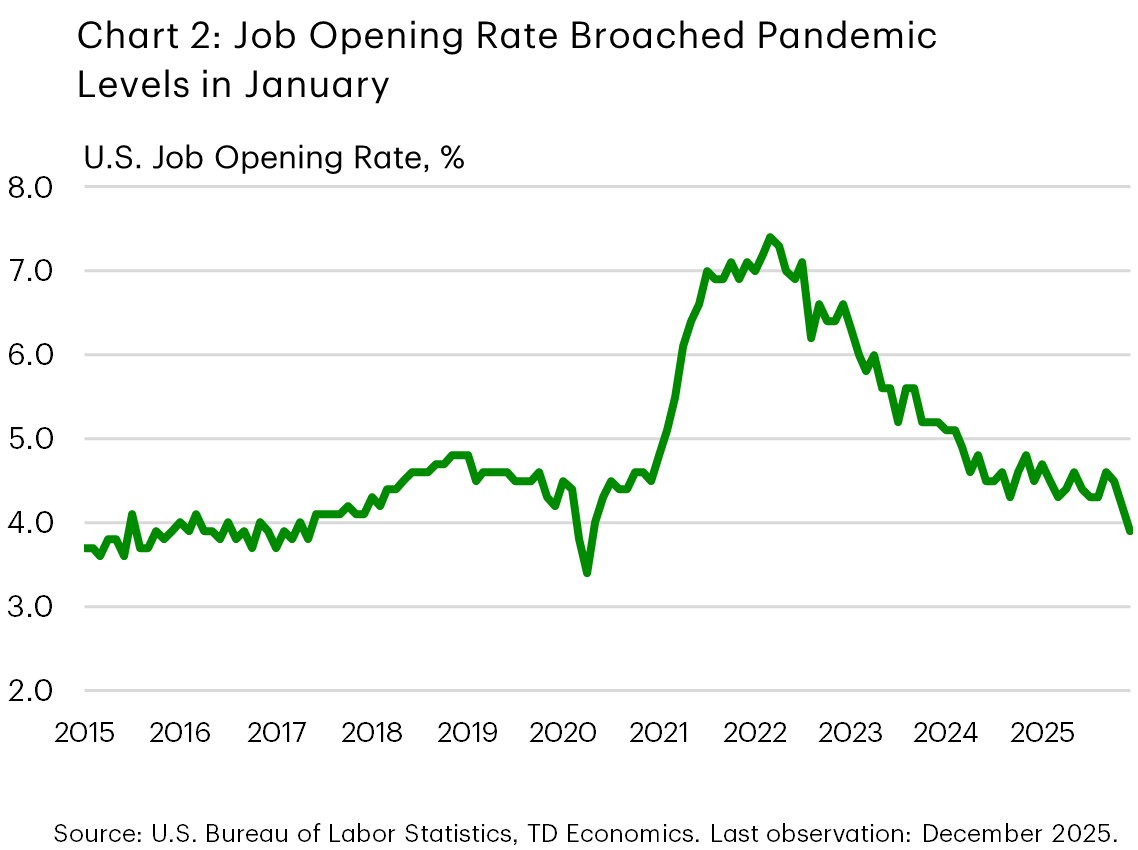

Our ability to see if this translated to the labor market in January was delayed by a week owing to the shutdown, with the Bureau of Labor Statistics pushing the release of the employment report to next Wednesday (originally scheduled for February 6th). However, we did receive the Job Opening & Labor Turnover report on Thursday, which showed a sharp drop in the job opening rate in December (Chart 2), particularly among white-collar sectors. The slowdown in the labor market has been a key concern for the Federal Reserve and provided the main rationale for the three “risk management” rate cuts implemented by the FOMC last year. Next week’s employment report will be watched closely, with a healthy addition of 70k jobs currently expected by consensus forecasters.

Although the next Fed meeting is still six weeks away, the Fed officials we heard from this week - including Atlanta Fed President Bostic, Richmond Fed President Barkin, and Fed Governor Lisa Cook - were broadly consistent in their view of the balance of risks between the Fed’s dual mandate. Most believed that risks to the labor market have eased, and that the persistent deviation of inflation from the 2% target is currently the greater risk. All speakers this week stated that patience was warranted to ensure that recent disinflation progress was sustained, but Governor Cook also noted that the FOMC was cognizant of the lingering risks to the labor market and would respond accordingly to the evolving risk environment.

Core CPI inflation sat at 2.6% in December, but price growth momentum dropped materially in the aftermath of the October government shutdown disruption. Further information will be available with next week’s CPI report for January, which is expected to show a modest drop in core CPI to 2.5%.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

6 Smart Tax Strategies to Help You Keep More of Your Income

By Jason List, CFP®, CFA

Many top earners are doing well financially, yet still ask a practical question: “How can I hold on to more of what I earn?” Tax strategies to keep more income are most effective when they’re part of a coordinated financial plan, not a standalone exercise or a once-a-year conversation.

When approached with clarity and purpose, tax planning supports the goals people are already building toward, whether it’s a confident retirement, flexibility to travel, or the ability to be generous with family and causes they care about.

The six tax strategies below outline practical principles designed to help you keep more of your income supporting the life you want to enjoy.

1. Start With the Big Picture, Not Just the Tax Bill

Taxes rarely exist in isolation. They are closely connected to how and when you retire, how income is generated over time, and what you want your legacy to look like.

Looking only at a single year’s tax bill can miss opportunities that become clearer when decisions are viewed over years instead of months. For example, the timing of retirement, the transition from earning income to drawing income, and long-term family priorities all influence how taxes affect overall wealth.

By stepping back and viewing taxes through a broader financial lens, many clients gain a clearer understanding of how today’s decisions support tomorrow’s outcomes. Coordinated planning helps bring structure and reassurance to what might otherwise feel fragmented.

2. Focus on Income Over Time, Not Just Annual Earnings

High earners often focus on what they make this year, but income rarely stays the same across life stages. Career peaks, retirement transitions, and business changes all shape how income flows over time.

Tax awareness becomes especially valuable when income is viewed across these phases rather than as a single snapshot. Understanding how income sources may change can support flexibility and choice later on.

Clients often appreciate how this approach contributes to smoother retirement transitions, greater freedom to travel, or confidence when navigating a career shift or business exit. In this way, tax strategies to keep more income are designed to support lifestyle goals, not limit them.

3. Use Timing Thoughtfully to Create Flexibility

Timing is one of the most powerful principles in financial planning. Aligning income, expenses, and major life events can create opportunities for efficiency and adaptability without adding complexity.

Life doesn’t move in straight lines. Retirement dates shift, businesses are sold, and priorities evolve. Planning with timing in mind allows your financial structure to adjust as circumstances change.

Rather than locking decisions into a rigid framework, thoughtful timing helps preserve flexibility, so your plan can evolve alongside your life.

4. Align Investment Decisions With Tax Awareness

Investment decisions and tax outcomes are deeply connected, even though they are often treated as separate conversations. When these areas align, clients often gain confidence that their financial plan is working cohesively.

To support this alignment, we invest alongside our clients and prioritize transparency and education. Our philosophy centers on helping clients understand how their investment decisions fit within their overall financial picture, including tax considerations.

This alliance supports long-term confidence and understanding, rather than focusing on short-term results or market headlines.

5. Plan With Purpose: Family, Legacy, and Generosity

For many individuals and families, financial prosperity goes beyond account balances. It reflects priorities such as supporting family, giving generously, and shaping a meaningful legacy.

Thoughtful planning allows financial decisions to reflect these priorities in an intentional way. Whether supporting children and grandchildren, contributing to charitable causes, or planning how assets are passed on, purposeful planning brings structure and meaning to long-term decisions.

Over time, this approach often enhances both confidence and fulfillment, reinforcing that wealth is a tool to support what matters most.

6. Why Thoughtful Guidance Makes Tax Planning Feel Manageable

Tax planning doesn’t have to be navigated alone. With the right guidance, it becomes an organized, understandable part of a broader financial strategy.

The team at Aventus Investment Advisors follows a disciplined, fiduciary process centered on education, simplification, and long-term relationships. With extensive experience working with retirees and those preparing for retirement, we help clients put tax strategies into action in ways that support long-term income and wealth preservation.

Thoughtful Tax Strategies to Keep More Income

Tax strategies to keep more income are most effective when they support the life you want to live. When financial decisions are aligned with your priorities, they can create room for flexibility, generosity, and meaningful experiences, today and into the future.

Aventus Investment Advisors partners with clients to help them stay focused on what matters most, keeping financial progress steady as goals and seasons of life evolve.

To schedule a meeting with us, call (704) 237-4207 or email jason.list@aventusadvisors.com.

Frequently Asked Questions

How can tax strategies help me keep more of my income over time?

Tax strategies to keep more income work best when they’re coordinated with your broader financial plan, not handled in isolation. By looking at income across different life stages—peak earning years, retirement transitions, or business changes—you can make decisions that support flexibility and long-term goals rather than reacting to a single tax year. This approach helps your income continue working for you as priorities evolve.

Do tax strategies change as I get closer to retirement or experience career transitions?

Yes. As income sources shift from earned income to investment income, retirement accounts, or business proceeds, the tax considerations change as well. Timing withdrawals, aligning investments with tax awareness, and planning for future income variability can all influence how much of your income you ultimately keep. Working with a fiduciary advisor can help these decisions remain aligned as your career or lifestyle changes.

How does Aventus Investment Advisors support clients with tax-aware financial planning?

Aventus Investment Advisors integrates tax awareness into a disciplined, fiduciary planning process rather than treating taxes as a once-a-year issue. By investing alongside clients and focusing on education and transparency, the team helps clients understand how income, investments, and long-term goals fit together. This coordinated approach helps tax strategies support income stability, legacy goals, and the life clients want to enjoy.

About Jason

Aventus Investment Advisors

Senior Client Advisor

Jason List, CFP®, CFA, is a Senior Client Advisor with Aventus Investment Advisors in Cornelius, North Carolina. With nearly two decades of industry experience, he helps clients organize, grow, and preserve their wealth through comprehensive planning, investment management, and tax-focused strategies. Clients value his approachable style and the confidence that comes from having a fiduciary partner to navigate life’s milestones, whether retiring, traveling, or buying a new home.

Jason earned his undergraduate degree in mathematics from the University of North Carolina at Charlotte, a master’s in finance from Shanghai University of Finance and Economics, the CERTIFIED FINANCIAL PLANNER® designation in 2012, and the Chartered Financial Analyst® designation in 2024. He joined Aventus in 2021 after working at large financial institutions, drawn to the firm’s focus on personalized, transparent advice.

A Charlotte-area resident for more than 30 years, Jason lives with his wife, Ashley, and their beagle, Mindy. He enjoys traveling, hiking, bowling, and watching sports, and also serves as treasurer for a nonprofit that supports disenfranchised children in Kenya. To learn more about Jason, connect with him on LinkedIn.

Financial News for the Week of January 23rd, 2026

Financial News Highlights

- Financial markets declined sharply on rising trade and geopolitical tensions but clawed earlier losses as cooler heads prevailed at the World Economic Forum in Davos.

- Consumer resilience carried into the fourth quarter, despite around 650,000 federal workers being furloughed without pay throughout the six-week long government shutdown.

- Core PCE inflation rose to 2.8% year-over-year in November, a light acceleration form 2.7% in October.

Canada – Transatlantic Tensions Unsettle Markets

For financial markets this week, an appropriate statement may have been “what a year this week was”. The TSX, for instance, plunged early in the week on tensions between Europe and the U.S. over Greenland. It then staged a relief rally, more-than-fully recouping those losses after President Trump eased fears of military action in the region and a renewed trade war with Europe. Canadian bond yields were also volatile, flaring higher alongside the spike in Japanese bond yields and geopolitical tensions, before pulling back a touch, as cooler heads prevailed on the Greenland issue.

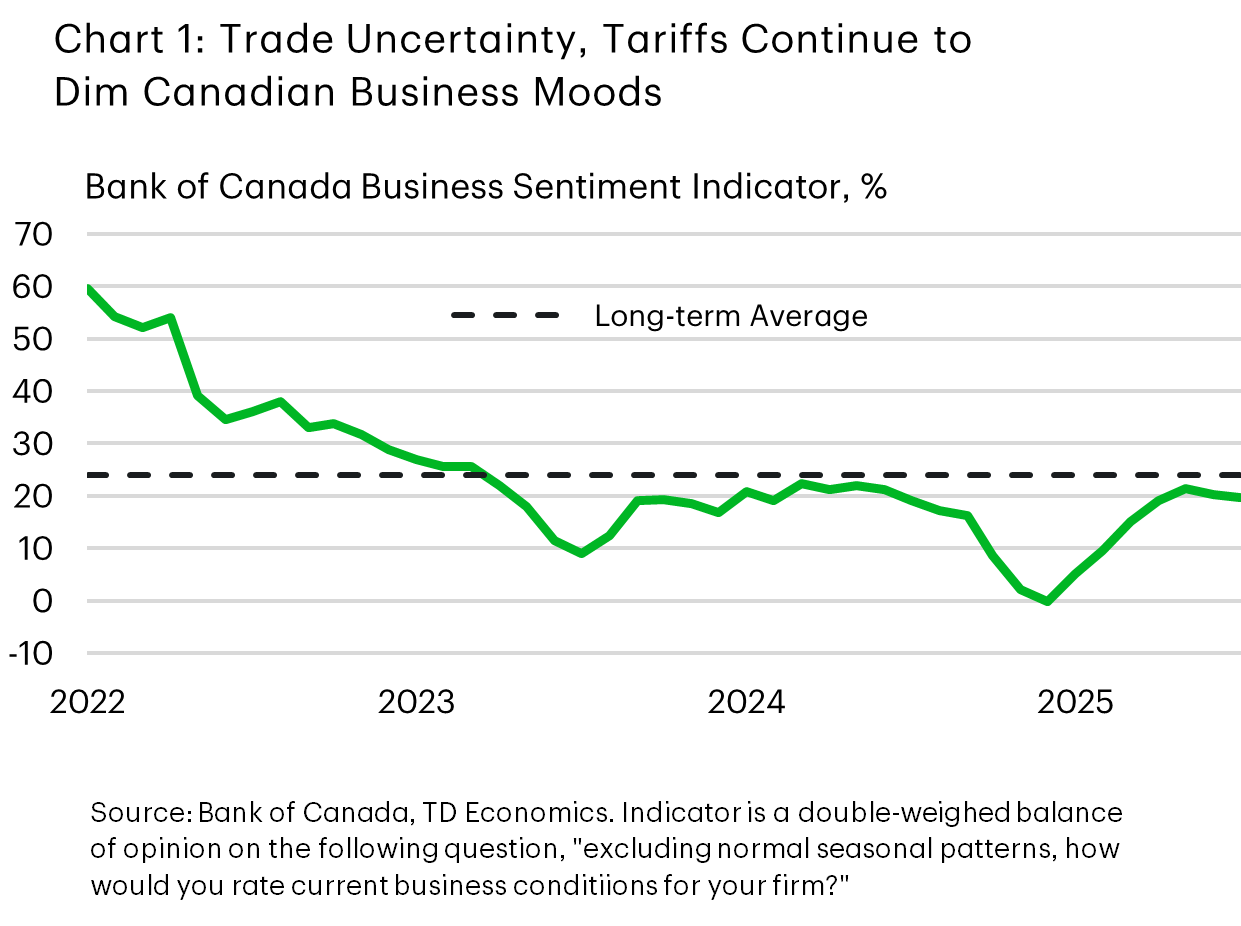

These events reinforced that Canada continues to deal in an uncertain economic backdrop, and this will likely be a factor restraining economic activity in 2026. This uneasiness has certainly been weighing on consumer and business moods, and we received fresh evidence of this impact this week with the latest Bank of Canada surveys on business and consumer confidence. Although showing some improvement relative to early 2025, business sentiment continues to be “subdued” (Chart 1). The uncertainty caused by the trade war continues to weigh on investment intentions, consistent with the pullback that we are seeing in the hard data. Consumers are also concerned about trade uncertainty, though actual spending remains decent. This week’s retail spending report showed a healthy 1% monthly gain in volumes. And, although retail sales are tracking flat for Q4 overall, we see some upside risk to our fourth quarter consumption forecast, on the back of stronger services spending.

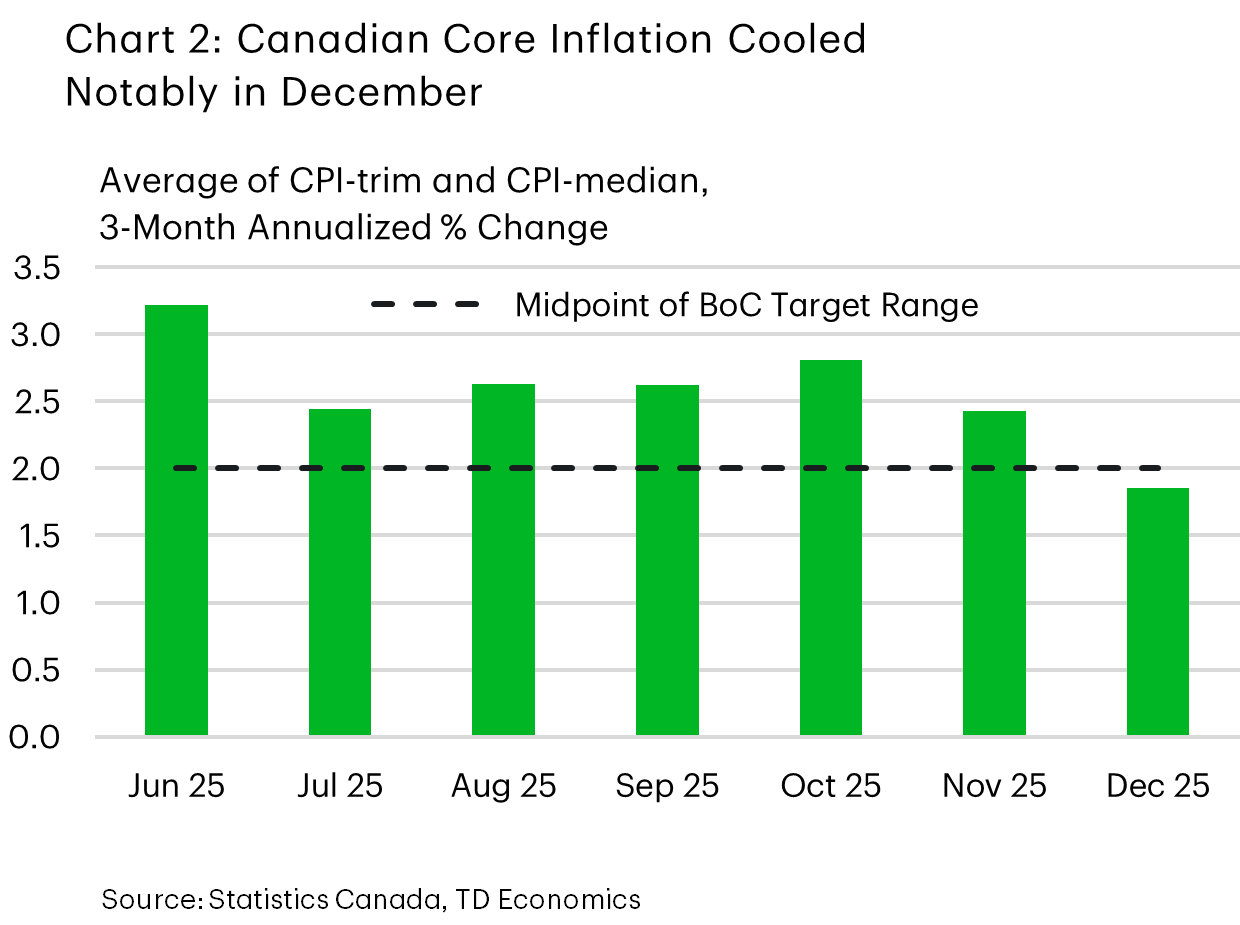

High prices were also a top concern for consumers in the Bank’s latest survey. However, there was some good news on this front this week. The Bank’s preferred core inflation metrics cooled in December (Chart 2), with the 3-month annualized percent change for the CPI-trim and CPI-median both ducking under 2%. What’s more, the share of items whose prices grew at 3% or more dropped (when measured on the same basis) - signaling a narrowing breadth of inflation across categories. However, the report wasn’t a complete slam dunk, as overall inflation increased by more than expected on the back of stronger food prices.

Tying these threads together, this week painted a picture of a soft underlying Canadian economy with moderating inflation pressures that still faces significant uncertainty. While this was enough for markets to slightly pare back their expectations of a rate hike later this year, we don’t think it was enough to meaningfully shift the policy dial. The Bank has repeatedly said that they are happy with the current policy stance, provided the economy evolves broadly in line with expectations. And, at 2.8%, core inflation landed almost bang-on the Bank’s expectation for 2025Q4. Indeed, it would take a significant undershooting of economic growth or meaningful softening in the labour market to force policymakers off the sidelines.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of January 16th, 2026

Financial News Highlights

- Headline retail sales rebounded in November from October’s decline. Sales in the control group rose for the second month in a row, pointing to resilience in consumer spending

- The housing market finished last year on a firmer footing. Existing home sales have now risen for four consecutive months, reaching the highest since early 2023 in December

- CPI inflation was steady in December at 2.7% y/y, down from a 3.0% peak in September.

Economic Resilience Amid Uncertainty

A full economic calendar this week built on last week’s payroll report in underscoring the economy’s resilience through a turbulent fourth quarter marked by the government shutdown. Geopolitical risks escalated amid violent protests in Iran and the prospect of U.S. involvement, sending the VIX index, gold, and oil prices higher mid-week—WTI briefly exceeded $60 per barrel—though prices retreated by week’s end as the threat of direct confrontation diminished. Surprisingly, Fed Chair Powell’s statement Sunday night where he spoke out on threats to the Fed’s ability to set interest rates free from political interference for the first time garnered little reaction from bond markets.

Resilience was evident in the retail sales report, as consumers appeared to have largely shrugged off the effects of the government shutdown. Headline sales rebounded by in November after a flat October, while sales in the control group—used in GDP calculations— were up 1% through the first two months of the quarter. This suggests Q4 2025 consumer spending growth was likely stronger than our earlier 1.1% (annualized) estimate. Next week’s personal income and spending data will provide more detail on households’ November income and spending, especially on services.

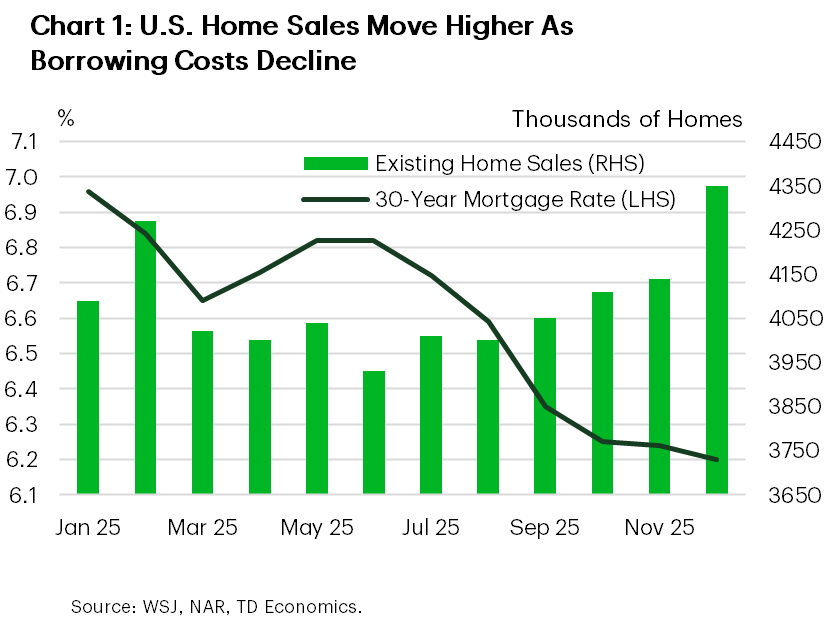

The housing market also finished last year on a firmer footing, with lower mortgage rates drawing more homebuyers off the sidelines (Chart 1). Existing home sales have now risen for four consecutive months, surging 5.1% in December to 4.35 million units—the highest since early 2023. We believe sales will continue to trend gradually higher this year; however, unless addressed, limited supply will continue to impede a stronger rebound.

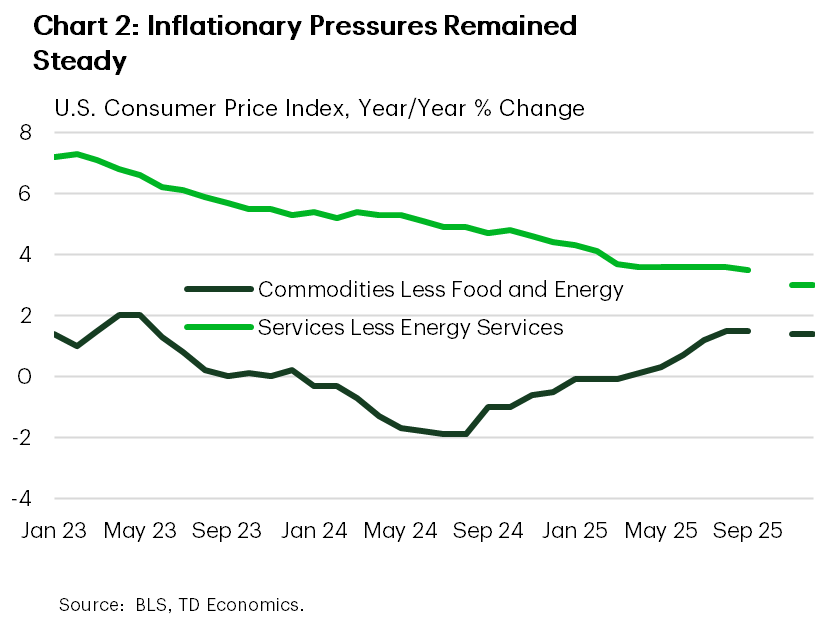

Inflationary pressures remained steady in December. The headline CPI was up 2.7% year-over-year, maintaining its deceleration from the recent high of 3.0% in September. Core goods prices were stable after five consecutive monthly increases (Chart 2). Food prices were somewhat elevated, rising 0.7% month-over-month (up 3.1% year-over-year), remaining a pressure point in households’ budgets.

Although inflation steadied in December, we still expect knock-on effects from tariffs to push it higher in the coming months. FOMC member Williams (voter) expects inflation to “peak at around 2-3/4 to 3 percent during the first half of this year,” but anticipates these will be “one-off” effects. Aside from tariffs, Williams noted that underlying inflation trends have been favourable, supply chain bottlenecks are absent, and the labour market is cooling gradually.

The latest Beige Book also reported both inflation and the labour market as broadly stable, with increased economic activity following the shutdown, and more Fed Districts seeing growth. Overall, recent data gives policymakers more reassurance that the economy stabilized at year-end while price pressures remained contained. This supports a “pause” on rate cuts for a few months, when tariff impacts are more clearly in the rear-view mirror.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of January 9th, 2026

Financial News Highlights

- The payrolls report for December came in weaker than expected, capping off the “low hire, low fire” 2025 jobs market.

- Global oil markets adjusted to the possible return of Venezuelan crude to global markets following U.S. actions in the country.

- Investors will have to stay tuned for the Supreme Court’s ruling on the IEEPA tariffs.

Data with A Grain of Salt

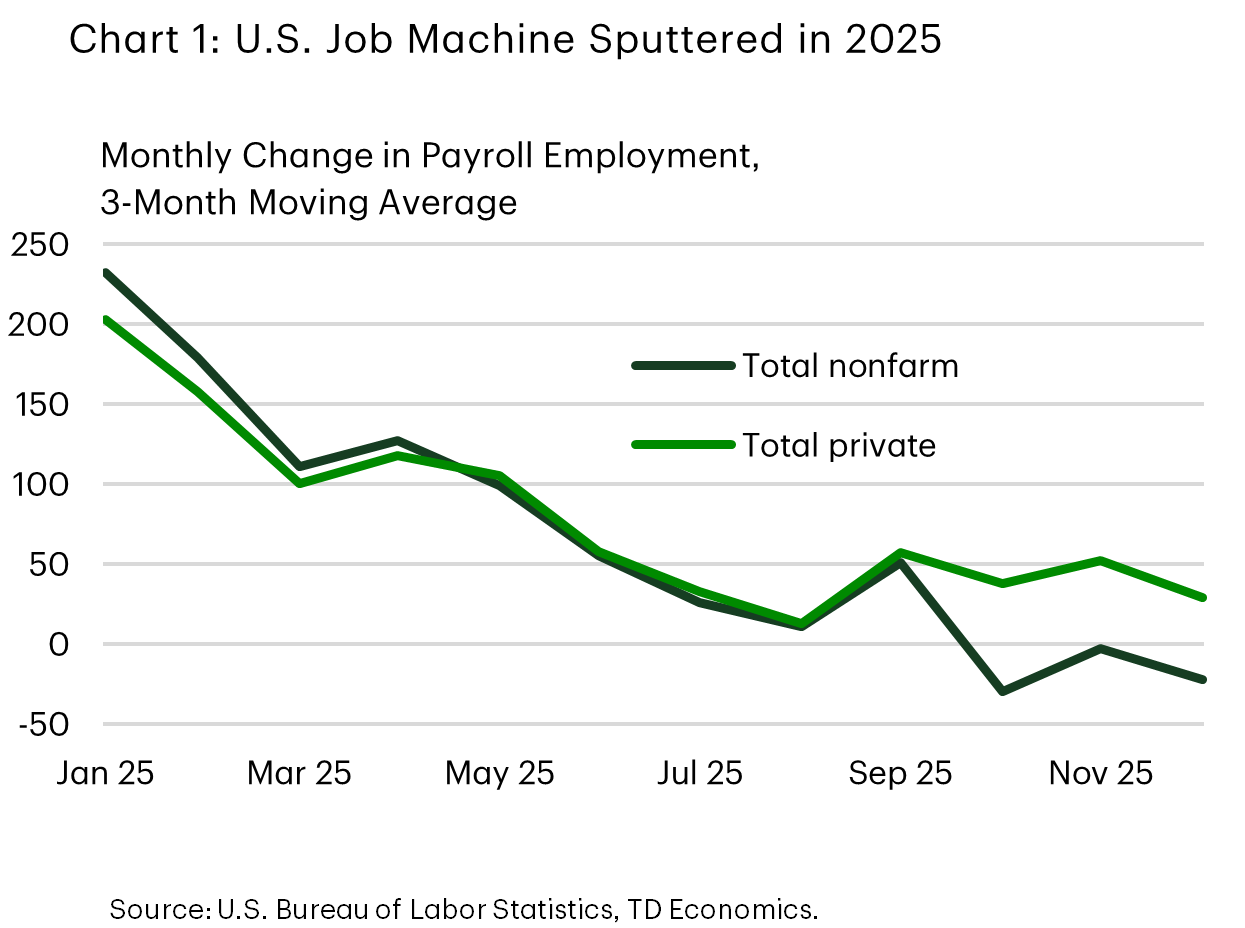

The world was on tenterhooks this morning as all waited to see if the Supreme Court would rule on the administration’s use of the International Emergency Economic Powers Act (IEEPA) to implement some of its tariffs in 2025. The much-anticipated IEEPA ruling did not come, so the big news of the day is the weaker than expected December jobs report. Private sector hiring slowed, prior months were revised lower, and the number of jobseekers declined, allowing the unemployment rate to fall even as jobs growth slowed. The data reinforce the view that 2025 was a “low hire, low fire” year, characterized by a pronounced deceleration in job growth and a modest rise in the unemployment rate (Chart 1).

Survey data this week were mixed. The ISM Manufacturing Index contracted for a tenth consecutive month, with respondents citing “tariff related pricing pressures” and notable reductions in 2026 capital expenditure plans. By contrast, the ISM Services surprised to the upside, highlighting continued resilience in consumer demand for travel, healthcare, and professional services. The divergence between manufacturing and services has persisted throughout the year, as manufacturing remains more exposed to tariff related uncertainty. Both surveys indicated easing price pressures and softening labour demand, consistent with today’s payrolls release.

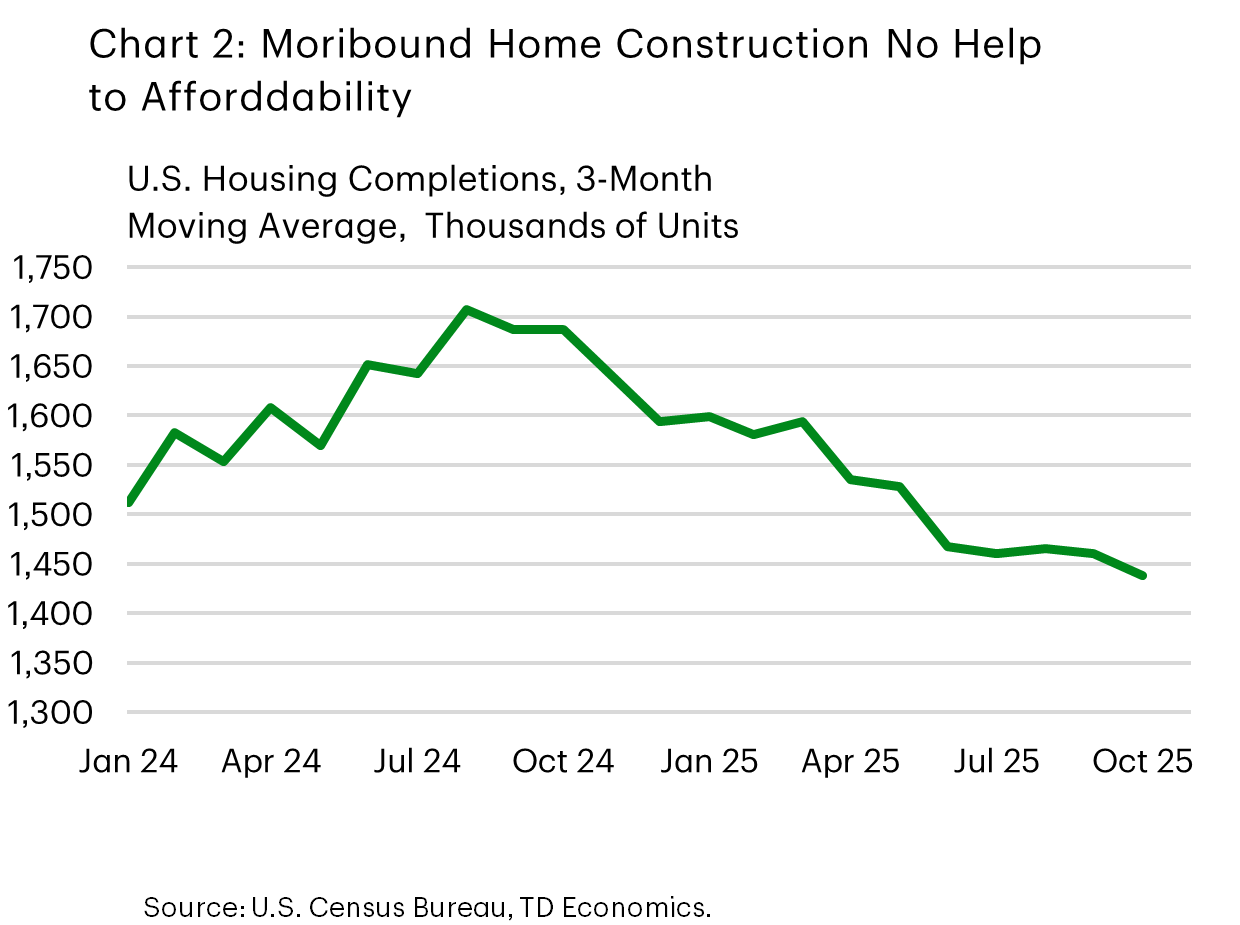

Developments in Venezuela added complexity to the oil market backdrop. Markets are assessing the administration’s commitment to the “Donroe Doctrine” and its implications for global oil supply. Despite Washington’s efforts to restore Venezuelan output, significant logistical and political hurdles remain. WTI moved down toward US$57 following the announcement that up to 50 million barrels of seized Venezuelan crude will be released to help address household affordability concerns. Adding to the affordability theme, housing data showed that homebuilding remains subdued, which doesn’t help the cost of housing (Chart 2). The administration has a clear desire to act on this front, promising a ban on institutional investor purchases and demanding government purchase mortgage-backed securities to help lower mortgage rates, though we await details on actual policy actions.

Prior to Friday’s jobs numbers, Federal Reserve officials suggested risks around employment and inflation were broadly balanced. Minneapolis President Kashkari indicated the labour market may be approaching equilibrium, while Richmond President Barkin characterized the economy as “finely tuned,” implying the FOMC would need to give equal weight to prices and employment. This reinforces our view and the view of the market that the FOMC is not in a hurry to cut rates further now, though we do expect to see interest rates come down later this year. We look ahead next week to the release of CPI inflation data, and after being let down by the Supreme Court this week, we are not going to be alone in being eager for news about when they may release decisions next.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of December 19th, 2025

Financial News Highlights

- Employment growth slowed in the first two months of the fourth quarter, owing to the impact of deferred resignations on federal government employment.

- Inflation fell sharply in November, but the degree of the descent and the condensed nature of the data collection period warrants caution in interpreting the data.

- Federal Reserve officials continued to voice a spectrum of opinions on the outlook for monetary policy that on aggregate spoke to a cautious approach moving forward.

Data with A Grain of Salt

This was arguably the biggest week for U.S. economic data in several months, as highly anticipated employment and inflation data delayed by the government shutdown was finally released. Financial markets largely took the data in stride, with U.S. Treasury yields falling slightly on the week, while equity markets were roughly unchanged as of the time of writing.

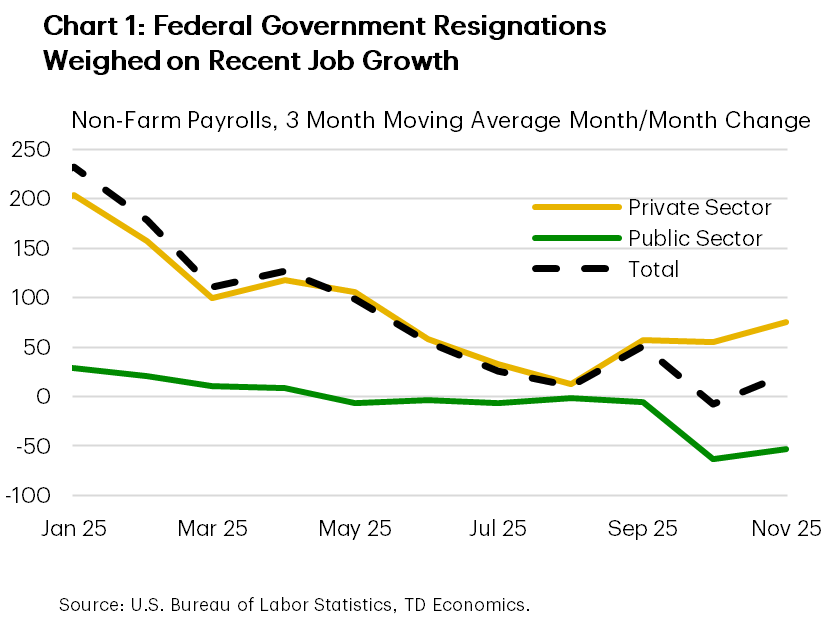

On the data front, the employment report showed that the economy continued to add jobs in the fourth quarter. However, headline job growth was weighed down by a large decrease in federal government jobs in October (Chart 1) - a byproduct of the deferred resignation offers sent out earlier in the year. Despite the near-term distortions, job growth has decelerated through the second half of the year, which has led to an uptick in the unemployment rate and motivated the 75 basis-point reduction in interest rates implemented by the Federal Reserve since September.

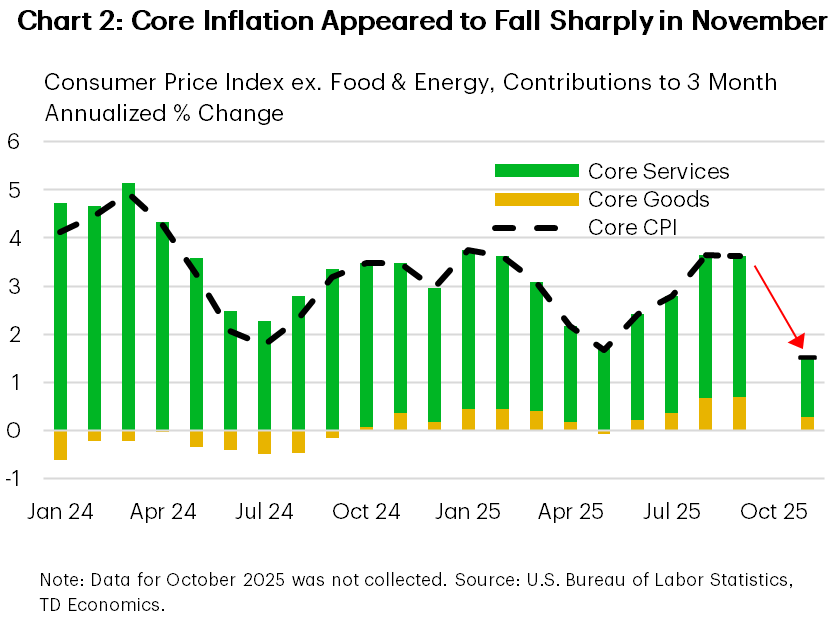

The pace of monetary policy easing has been deliberately gradual though, as inflation risks have been rising at the same time. However, November CPI data showed that there may have been a break in this trend in recent months, with the annual percentage change in core inflation falling to 2.6% - the lowest level since March 2021. Given the shorter collection period for this data owing to the government shutdown and the sharp drops recorded in several index categories (Chart 2), this data should be taken with a grain of salt. Market pricing for the Federal Reserve’s January meeting was largely unchanged, with only a 25% chance for a fourth consecutive cut.

The handful of Federal Reserve officials we heard from this week offered notably different assessments on the policy rate outlook. Miran made the case for aggressive rate cuts, positing that inflation metrics were anomalously high, while Waller also took a dovish tone but noted a gradual pace of rate cuts would be warranted going forward. On the other end of the spectrum was Bostic, who voiced greater concern for inflation risks and stated he did not currently see the need for rate cuts in 2026. Other speakers, including Vice Chair Williams, echoed Powell’s comments from his press conference last month that monetary policy was in a good place heading into 2026. Despite growing dissent among FOMC members, the balance of opinion is one of relative caution heading into the new year. Market pricing has followed suit, with another rate cut not expected until the Fed’s meeting in late April next year at the earliest.

Looking ahead to next week, there will be few items on the economic agenda during the holiday shortened week, but the preliminary estimate for third quarter GDP on Tuesday will be a highlight. A strong reading for annualized growth of roughly 3% is expected, which will likely be followed by a deceleration in the fourth quarter owing to the government shutdown. Nevertheless, we expect the economy to grow by 2.2% in 2026, aided by fiscal and monetary policy support.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.