Financial News for the Week of September 8, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investors had lots to digest this week, with the lineup including communication from central banks, natural disasters and growing geopolitical tensions. The dynamics weighed on equities, while sending gold and Treasuries higher. Economic data remained largely positive, but diverging views among Fed officials point to some uncertainty as to the near-term path of interest rates. The October departure of Vice Chair Fischer is likely to add to that uncertainty.

- Economic data is likely to sustain some volatility due to the effects of Hurricane Harvey and the impending Hurricane Irma. Today’s swift deal in Congress to extend the government’s funding and borrowing limit until Dec. 8th, along with a $15.25 bn. relief package, should nonetheless provide some solace for the economy.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

More Stormy Weather And Volatile Data On The Horizon

Despite this being a holiday-shortened week, investors had lots to digest, with the lineup including communication from central banks, natural disasters and growing geopolitical tensions. The latter was the dominating factor at the start of the week, with markets opening on a dour note as investors poured into safe haven assets. The dynamic sent gold and Treasuries higher, while also benefitting crude oil. Conversely, long-term yields and the trade-weighted U.S. dollar sustained their downward trends – the latter falling to early 2015 levels.

Nonetheless, the theme of synchronized economic growth leading to a removal of monetary stimulus was back on display this week. An improved performance of the Eurozone and Canadian economies, which have been growing at rates significantly above potential lately, inspired more hawkish stances among their central banks. In this vein, the BoC hiked its key interest rate for the

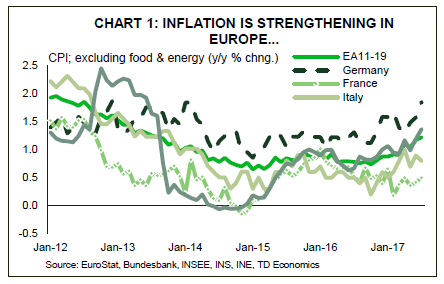

U.S. economic data was similarly positive. The trade deficit remained largely unchanged in July, and net exports are on track to contribute positively to economic activity for the third consecutive quarter. At the same time, the ISM non-manufacturing index followed its manufacturing counterpart and rebounded in August. The renewed vigor in both ISM metrics points to economic growth gaining momentum, with an upbeat tone in the Beige Book echoing a similar narrative. What is more, the prices paid components of both indices continued to point Admir Kolaj, Economist to rising price pressures (Chart 1). While we are yet to see these manifest in inflation metrics, the trend should still provide some comfort to the Fed as it meets to discuss monetary policy in two weeks’ time.

Ahead of that meeting, a number of speeches from Fed officials took place throughout the week. The most significant were those of voting members Brainard and Dudley. Brainard’s speech, which suggested treading carefully over low inflation, was decisively dovish. Meanwhile, Dudley retained a more hawkish tone, but did acknowledge his ‘surprise’ to the shortfall in inflation and suggested that ‘structural’ factors may be at play. The diverging views point to some uncertainty as to the nearterm path of interest rates. The October departure of Vice Chair Fischer, at a time when the Fed Board already has three vacancies, is likely to add to that uncertainty.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of September 1, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Substantial positive revisions to Q2 US GDP indicated stronger momentum going into the third quarter than previously thought, with Hurricane Harvey expected to shave 0.1-0.4 ppts. off growth in Q3.

- Inflation continued to be stubbornly elusive in July but we still expect a hike by the Fed in December, given that inflation will likely strengthen in the coming months.

- Global economies continue to strengthen alongside the US, with China’s Caixin manufacturing PMI expanding to its highest level in six months in August, led by strong foreign demand for goods.

Inflation Remains Elusive in Q3

It was a busy week for data this week in the US, with investors looking for clues on how the economy is performing and whether it warrants further tightening. Substantial positive revisions to Q2 US GDP indicated stronger momentum going into the third quarter than previously thought, with Q2 growth revised up to a robust 3.0% annualized. However, Hurricane Harvey, which made landfall in Southeast Texas last week, looks to be a transitory obstruction for the economy in Q3. The storm is expected to shave 0.1-0.4 ppts. off growth but a similar acceleration in Q4 should leave the second half of the year unchanged on balance. Harvey will also necessitate the passage of a disaster assistance package by the federal government. On that note, until further details surrounding policy and tax reform materialize, investors will remain fixated on economic data.

Evidence to support the Fed’s tightening path was mixed as the week progressed. July’s personal income & spending report highlighted the pivotal role of the consumer in the economic recovery, with strength in real spending apparent. But the missing piece of the puzzle continues to be inflation, which has been stubbornly elusive during this recovery. And this was compounded by Friday’s jobs report that indicated relatively subdued wage growth –a trend that does not bode well for the inflation outlook (Chart 1). We still expect a hike by the Fed in December, but expect that inflation will materialize in the coming months. Manufacturing activity displayed pronounced strength in hiring in August while the positive ISM reading for the month prefaces continued strength in the sector going forward (Chart 2). As such, investor confidence in the American economy remains intact, whichalongside weaker inflation has supported US equities.

Asian economies have also shown increased momentum lately. Case in point, China’s Caixin manufacturing PMI expanded to its highest level in six months in August, led by strong demand for exports. That’s a welcome development given concerns regarding the economy’s slowing growth this year and the role that government debt has had in stimulating growth. Other Asian economies echoed this constructive tone, leading the MSCI Asia Pacific Index to a level just shy of a decade high.

With a relatively quiet data release schedule for next week, investors will turn their attention to the array of speeches being made by FOMC members. Of central importance will be their views on the soft inflation and wage prints in recent data. Ultimately, we do not expect these developments to dissuade the Fed from beginning balance sheet normalization in the coming weeks, but some improvement on the inflation front is likely to be needed before another rate hike by the Fed.

Katherine Judge, Economic Analyst

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 25, 2017

HIGHLIGHTS OF THE WEEK

- A very quiet week for economic data had markets anticipating Chair Yellen’s remarks at Jackson Hole. Her speech largely went over old ground on financial stability and the role of regulation.

- Next week, President Trump is expected to join the chorus of Republicans promoting tax reform. We still don’t know the details, but September is likely to see the debate heat up as Congress gets down to brass tacks writing legislation.

- Add to that the potential for an 11th hour solution on the debt ceiling and funding government beyond September, and investors could be kept on the edge of their seats over the next couple of months.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

Washington Likely to Keep Markets on Edge

September is likely to keep markets on the edge of their seats awaiting details of tax reform plans, and the potential for fireworks surrounding the debt ceiling and funding government beyond September (see recent report). The GOP surely needs some kind of legislative achievement to show voters in the mid-term elections, raising the stakes to get some kind of tax reform done in short order. Last week’s market turmoil demonstrated just how sensitive markets are to signs that Trump might not be able to implement his lower-tax pro-business agenda.

President Trump is scheduled to start making speeches in support of tax reform next week. Joining in with the chorus of GOP Members of Congress stumping their tax reform plans throughout August. But, we still do not know the details of what that agenda will look like. The high level statement of principles released before the August recess by the “Group of Six”, was meant to give direction to the two tax-reform writing committees (House Ways & Means and Senate Budget) that will hash out the gory details of the package in September.

We know the controversial border adjustment tax is off the table. Reading between the lines of the statement, they are (not surprisingly) seeking to lower the corporate tax rate, lower taxes for “pass-through” businesses, and likely move towards full expensing of capital expenditures. Recent leaks from the process suggest a corporate rate between 22-25% is being considered. The Tax Foundation has estimated that reducing the CIT rate to 25% and allowing full expensing costs $1.2 trillion (tn) over ten years. On the flip side, eliminating the deductibility of interest payment would generate $1.2 tn, at current tax rates. Allowing companies to repatriate cash from overseas at a one-time low tax rate, is almost certain to be included and would generate between $140-150 billion.

On the personal side, there is talk of capping the mortgage interest deduction. That could generate over $300 bn if it is the level of eligible debt is capped at $500K, and would largely be paid by taxpayers in the top 20% of incomes. Repealing the state and local tax deduction, would also generate significant revenue (potentially $1.7 tn). These “pay-fors” could fund lower personal tax rates or double the standard deduction, which would improve simplicity, and benefit middle-income taxpayers the most (see our recent report).

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 18, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A relatively good week for economic data was overshadowed by geopolitical events. Volatility spiked late in the week, the Dow suffered its largest one day loss since May on Thursday, and the 10-Year Treasury rallied to 2.17%.

- Investor nervousness is understandable, but there is little reason to doubt the ongoing economic expansion. U.S. retail sales rose by a robust 0.6% in July and were upwardly revised in June.

- Minutes from the FOMC’s July 26 rate announcement showed a Fed looking for proof that inflation is moving toward target, and agreeing that balance sheet reduction should begin soon (likely in September).

Good Data Overwhelmed By Geopolitical Concerns

A relatively good week for economic data was overshadowed by geopolitical events and concerns about the economic leadership within the Trump administration. On Thursday, volatility spiked, equites saw their biggest declines since May (the Dow down 1.2%) and Treasuries rallied (U.S. 10-year fell to 2.19%) as investors sought the protection of safe assets.

The understandable nervousness among investors notwithstanding, there is little reason to doubt the ongoing economic expansion. Retail sales rose by a robust 0.6% in July and were upwardly revised in June. The details were encouraging with broad-based strength across categories. Given consistently strong job growth, accelerating wage growth and benign inflation, consumer spending should remain healthy over the second half of the year. We expect personal spending to rise by 3.0% in the third quarter. With additional support from business spending, real GDP should rise by about as much.

On the topic of inflation, the minutes from the Federal Open Market Committee’s July 25-26 meeting gave additional detail on how monetary policymakers are responding to its recent misses. The dilemma for policymakers is how to explain the continued downward drift in inflation in spite of ongoing tightening in the labor market. The minutes offered several possible explanations: a weakened relationship between resource slack and inflation, a lower natural rate of unemployment, greater lags in the relationship between economic tightening and inflation, and restraints on pricing power due to technology and globalization.

Overall, their faith is being tested, but it has not been lost. “Most participants thought that the [Phillips curve] framework remained valid” and still believe that inflation will return to target over the medium term. At a minimum however, they will need to see some proof that inflation is moving toward target in order to continue to push up policy rates.

All of this assumes that the political situation in Washington remains stable. September will be a busy month for Congress, who has to pass an increase in the statutory debt ceiling and find a way to continue funding the government and avoid a shutdown. At the same time the administration will continue to push for personal and corporate tax reform. If Congress fails to reach accord on either the debt ceiling or government funding, we would expect increased volatility and additional losses in equity markets that still appear priced for perfection. As it has in the past, the financial and political damage would likely move politicians to quickly fall into line.

James Marple, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 11, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets this week have been largely driven by corporate earnings and political events, with tensions on the Korean Peninsula escalating to the point where markets can no longer ignore them.

- Inflation strengthened in the Eurozone, with prices growing by 0.13% in July and the year-over-year measure accelerating to 1.2% with strength particularly apparent in Germany and Spain.

- U.S. inflation surprised to the downside once again, with prices growing by 0.1% in July – or half the expected pace. Despite the soft CPI print and PPI figures, we expect inflation will strengthen somewhat in the coming months.

Inflation Strengthens in Eurozone, But Stays Soft in U.S.

Markets have this week been driven largely by political events and corporate results. Second quarter earnings continued to impress, boosting sentiment and stock valuations. Oil prices also helped, with the WTI benchmark rising above $50 on Thursday morning, helped along by rising global tensions and a drawdown in US inventories.

Escalating tensions really begun to weigh on markets on Thursday afternoon with stock indices having the worst day in three months. Volatility sprung to life, with the VIX rising to 17. The tensions have so far boosted the flow of money into safe-haven assets, such as G7 government bonds. At the same time, risk assets exposed to the peninsula, such as the Kospi, Shenzen, and Nikkei equity indices fell on the week. While we don’t expect situation on the Korean Peninsula to result in armed conflict, it could lead to weaker economic performance as consumers and businesses in the region pare back spending.

As far as economic data, this week was all about inflation. The story was relatively good in Europe, with several economies seeing robust readings. Core CPI in Germany and Spain rose by 0.4% and 0.3% (m/m) in July – the fastest monthly pace of several years. Price gains in France and Italy were less apparent, and averaged 0.13% for the Eurozone as a whole. Still, inflation in year-on-year terms accelerated to a four-year high of 1.2%, with these readings likely to provide further comfort for ECB officials to begin considering paring back on bond buying.

Inflation was far less robust in the U.S. with the producer price index (PPI) report on Thursday as well as its consumer cousin a day later, underwhelming. Total PPI declined 0.1%, marking its first decrease in eleven months, while the core measure pulled back by just as much in July, with the year-on-year measures decelerating by 0.3 percentage points to 1.9% and 1.8%, respectively. The consumer price index (CPI) also missed expectations, increasing by half of the 0.2% m/m gain that was expected.

There are reasons to be hopeful. This week’s NFIB survey offered some reassurance, with the share of firms raising selling prices rising to 8% - the highest share since mid- 2014. There was also an increase in the share expecting to raise prices from 19% to 23%. At the same time, labor market progress continues at a resilient pace. With unemployment at 4.3%, wages growing at 2.5% y/y, and the trade-weighted dollar down 8% from its peak in December, inflation is likely to turn higher in the months ahead. This should allow the Fed to continue its plans to normalize its balance sheet and perhaps sneak in one rate hike before the year is out.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

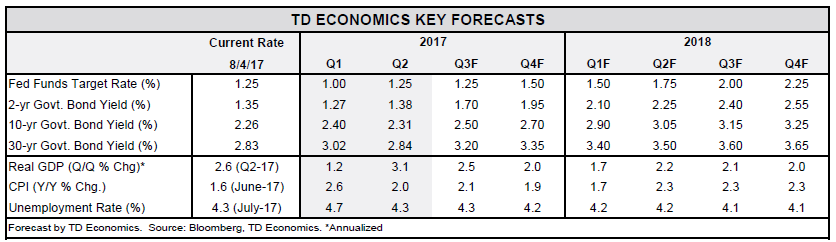

Financial News for the Week of August 4, 2017

HIGHLIGHTS OF THE WEEK

- U.S. stock indices remained supported by the continued flow of favorable earnings releases. Bond yields and the U.S. dollar moved lower through Thursday, but that dynamic reversed course with the robust payrolls report.

- The American economy continued to churn out jobs at a robust pace in July with payrolls rising by 209k. At the same time, the unemployment rate fell to a cycle low of 4.3%. Average wages rose a solid 0.3% m/m.

- Improvements in ISM manufacturing and non-manufacturing prices sub-indices, together with a slightly firmer core PCE price index suggest that a turnaround in inflation may be underway.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

Jobs Numbers Impress, But Still Waiting on Inflation

It was another good week across most markets. U.S. stock markets remained supported by continued flow of favorable earnings releases, with the DJIA breaching the 22,000 threshold by mid-week. A string of softer data releases through Thursday also led bond yields and the U.S. dollar lower. But that ended Friday morning, when a solid employment report boosted the dollar and inspired a bit of a sell-off in the bond market.

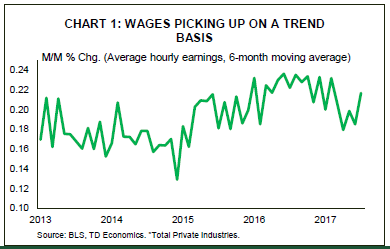

The report was indeed a beauty as the American economy continued to churn out jobs at a robust pace in July, with payrolls rising by 209k, beating market expectations for a 180k print. But there was more. The jobless rate dropped to a cycle low of 4.3%, while broader measures of labor underutilization remained near their pre-recession lows. More workers joined the labor force, with the participation rate recording a small uptick to 62.9%. While average wages failed to accelerate on a year-over-year basis (Chart 1), given the weakness at the beginning of the year, the monthly gain of 0.3% was very strong and marks the fastest pace in ten months. Going forward, we expect job gains to slow somewhat. However, the trend should also be accompanied by stronger wage gains. While the relationship between labor market slack and inflation has become more muted in recent years, and is taking longer to materialize, we believe the link still holds. As such, we believe that a pick-up in inflation should materialize before the end of the year, with the stronger data motivating the Fed to take interest rates higher (see report).

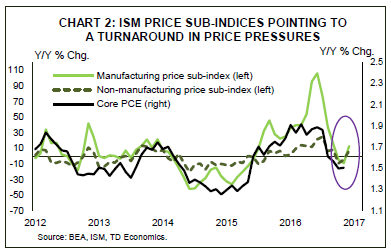

The ISM surveys provided mixed signals of the economy. The manufacturing index suggested that the sector continued to expand at a healthy, but slightly slower pace, supported by a rebounding global economy and the lower U.S. dollar. The non-manufacturing index also telegraphed a deceleration in activity, but remained in expansionary territory while most industries continued to report growth. Importantly, both ISM surveys indicated significant increases in their prices sub-indices. Together with a slightly firmer core PCE price index, which was revised up to 1.5% y/y in June this suggests that a turnaround in price pressures could be underway (Chart 2). Should this in fact be the case, we expect further tightening to take place later this year, with the Fed likely to slip in a December hike. Lack of such evidence, on the other hand, will likely stay the Fed’s hand as far as the hike, but is unlikely to prevent the Fed from starting the balance sheet unwinding process in the fall.

Admir Kolaj, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of July 28, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- It was a good start to the week for U.S. equities, with stock prices boosted by another round of strong earnings reports and a weakening in the US dollar to its lowest level in over a year. However, these gains were offset by dips in health care and tech stocks by Friday afternoon.

- As expected, the FOMC voted unanimously to leave its benchmark rate unchanged, while signalling that the balance sheet normalization process will likely begin in October.

- The American economy accelerated in Q2, returning to a slack-absorbing pace of 2.6% growth, led by strength in consumption and private fixed investment.

Growth Accelerates in Q2

It was a good start to the week for U.S. equities, with stock prices boosted by another round of strong earnings reports. Consumer discretionary and staples led the sectors in performance, a reflection of the increasingly important role that consumer spending is having in lifting growth. Energy stocks also posted large gains, helped by a rebound in the price of oil amid Saudi Arabia’s commitment to restrict oil exports in August and another bullish U.S. inventory report (Chart 1). By the end of the week, the weighty tech and health care sectors offset these gains. A weakening in the USD provided support for equities, notably early in the week, while European indices were weighed down by an appreciation in the sterling and the euro vis-à-vis the greenback –which fell to its lowest level in over a year.

The dollar did not get much support from the FOMC. As expected, the Committee voted unanimously to leave its benchmark rate unchanged, but the policy statement highlighted a dovish turn, with the Committee appearing more concerned about the tepid inflation data. This led markets to push out Fed hike expectations. Despite this, the Committee expressed their intention to begin the process of balance sheet normalization “relatively soon”. This is likely to be announced at the FOMC meeting in September, with run-off to begin in October. However, another rate hike is unlikely until at least the end of the year. We expect that a December hike may yet happen, but such an outcome depends on inflation firming in the coming months. Many of the disinflationary pressures appear to be transitory in nature, with cell phone discounts, lower commodity prices, and falling prices of imported goods related to past US dollar strength. But these pressures should ease in the second half of the year, while the USD upside potential remains limited for three reasons. For one, the Fed’s rate hike trajectory looks to be more gradual than previously communicated. Secondly, the balance sheet normalization will have a smaller currency impact than an equivalent rate increase, and lastly, strengthening global economies should allow central banks such as the ECB and BoE to pare back supportive monetary policy measures. Second quarter data supports this view, with both French and Spanish economies having expanded at a healthy pace in Q2.

Remaining top-tier domestic data releases this week telegraphed a mixed picture of the housing market. Existing home sales pulled back to a still healthy 5.52 million (annualized) as lack of inventory and eroding affordability prevented purchases. At the same time, new home sales ticked up 9.1% from a year ago, suggesting that demand remains intact. We look forward to next week’s bevy of reports that should clarify how the economy has done in the first month of the third quarter, with the employment, income & spending, and ISM survey reports being top of mind, as we seek confirmation that economic momentum remains robust during the third quarter.

Katherine Judge, Economic Analyst

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of July 21, 2017

HIGHLIGHTS OF THE WEEK

- It was a light domestic data week with investors focused on politics, central banks, and international data. U.S. equities set new records with the S&P 500 a mere 25 points from 2,500. while the dollar weakened broadly.

- China’s economy grew by 6.9% y/y in Q2 with broad-based gains. The robust headline, alongside consensus-beating details helped shore up confidence in the evolving and decelerating economy.

- Despite the unchanged policies and dovish tone from the BoJ and ECB both the yen and euro strengthened.

- U.S. data was robust but not market-moving, with investors looking forward to FOMC and Q2 GDP next week.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

More Growth.... Less Inflation

It was a light week for domestic economic data with investor focus primarily on political events, G7 central banks, and international data. China kicked off the week with the release of economic growth estimates for the second quarter. The world’s second largest economy grew by 6.9% in Q2 with gains broad-based. The robust headline, alongside consensus-beating details helped shore up confidence in an evolving and slowing economy with the strength of the largest consumer of materials providing some support to commodity prices.

Paradoxically, the yen and euro appreciated despite the dovish stance communicated on Thursday by both the Bank of Japan (BoJ) and the European Central Bank (ECB). The BoJ left the policy rate unchanged and will continue to buy assets for some time still. The BoJ upgraded the growth forecast for the Japanese economy, but also lowered the inflation forecast and pushed out its timeframe for achieving the inflation target. Gov. Kuroda now expects inflation to reach 2% a year later than previously projected, or by March 2020. This is the sixth time that the BoJ pushed out the timeline under his tenure.

A similar theme is apparent in the Eurozone. Growth projections were lifted over the medium-term while inflation forecasts have been downgraded, with inflation unlikely to hit ECB’s 2% target this decade. Importantly, in the latest press conference ECB President Draghi communicated that inflationary momentum in the Eurozone is not self-sustaining and the ECB is in no rush to taper its bond purchases at this point so as to maintain support.

U.S. economic data were relatively constructive. The pace of homebuilding bounced back above the 1.2 million annualized pace, Empire and Philly surveys telegraphed robust growth, and jobless claims fell to 233 thousand. Still, the robust data offered little to support the greenback, with political uncertainty related to the ACA, debt ceiling, and NAFTA remaining front-andcenter. The dollar also lacked Fed hawks’ support with the FOMC in a 10-day blackout period ahead of next week’s policy meeting. While we only expect only minor tweaks to the policy statement we look forward to the post-meeting speaking circuit in anticipation of updated Fed communication, which remains at odds with markets on upcoming rate hikes. We believe that the truth about rate hikes in the next eighteen months is somewhere between the market’s two and Fed’s four. Moreover, while we can’t rule out a hike later this year, the probability of such a move is diminished at this point, especially taken together with balance sheet normalization slated to begin in the fall.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of July 14, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Fedspeak took center stage this week. Fed Chair Yellen delivered prepared remarks to Congress, where among other things, she acknowledged the uncertainty as to when inflation would rise back toward its target.

- Taken together with Governor Brainard’s comments, markets interpreted the tone as dovish, with long-term Treasury yields and U.S. dollar falling, while U.S. equities soared toward all-time highs.

- Both the CPI and retail sales reports came in below consensus, adding further downside risk to the pace of Fed hikes over the next year and a half.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

Soft Inflation Risks Delaying Fed Hike

Fedspeak took center stage this week with six members of the FOMC making public appearances. In what may be her last Congressional testimony as Fed Chair, Janet Yellen delivered prepared remarks and answered questions in both the House and Senate this week. She reiterated the Fed’s narrative that the economy is healthy enough to withstand further rate increases and that the process of balance sheet reduction is expected to begin this year. That said, she did acknowledge the uncertainty as to when inflation would rise back toward its target, noting that a handful of past factors would pressure inflation down until they drop out of the annual calculation. Inflation numbers out this morning confirmed that price pressures remained subdued in June, with the softness casting some doubt as to the idiosyncratic nature of the recent loss in momentum (Chart 1).

The Chair elaborated on the neutral rate of interest, noting that it is currently low, necessitating patience as far as rate hikes. However, she suggested that the neutral rate would likely move higher towards the 3% mark as the temporary factors holding it down ease off, motivating additional rate hikes over the coming years. This marked a divergence from Governor Brainard, who suggested in her remarks this week that the neutral rate is “likely to remain close to zero in real terms over the medium term.” Taken together, markets interpreted the comments as dovish, with long-term Treasury yields and U.S. dollar falling, while U.S. equities soared toward all-time highs. The latter were also buoyed by rising oil prices, on account of a bullish U.S. inventory report.

Yields and the dollar were further weighed down by a soft retail spending report with sales retreating in June, falling short of expectations for a modest gain (Chart 2). While the softer print leaves our second quarter consumption estimate still near 3%, the story is less upbeat as far as momentum heading into the third quarter with consumption on track to decelerate closer to the mid-2% mark. Together with the relatively broad-based weakness in discretionary spending categories, the poor spending performance leaves us somewhat puzzled – particularly given the continued strength in the labor market. On the whole, the combination of the weak CPI and retail sales reports adds some downside risk to the pace of Fed hikes over the rest of the next year and a half.

Outside of the U.S., improving global growth appears to be emboldening other central banks to consider reducing stimulus. The Bank of Canada saw through soft inflation figures and raised its overnight lending rate this week for the first time in 7 years. Meanwhile, tightening talk has gained further traction at the Bank of England, and the European Central Bank looks to announce a taper schedule of its asset purchases later this year. Such convergence in monetary policy direction would help the Fed’s interest rate normalization plans, but for now all eyes remain firmly on inflation.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of July 7, 2017

HIGHLIGHTS OF THE WEEK

- Global bond yields moved higher this week following cautiously hawkish statements by central bankers last week.

- Above-trend economic growth in advanced economies is expected to persist. But, inflation is expected to lag owing to a number of structural factors working to suppress price growth.

- Altogether, model simulations of shocks to inflation and the unemployment rate supports the FOMC’s cautious pace of monetary policy normalization. The last thing the Fed or other global central banks would want to do is to have to reverse course several quarters from now, and risk impairing their credibility.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

Fed is Right to be Concerned with Low Inflation

Although a short week, the bond sell-off resumed on global financial markets, taking yields higher following cautiously hawkish statements by central bankers last week (Chart 1). Selling pressures intensified domestically and across the pond, with European markets reacting in advance of the tapering of ECB asset purchases expected to begin early next year.

Curiously, this repricing episode has little to do with a material change in underlying economic fundamentals. Indeed, economic growth in advanced economies has exceeded trend for a number of quarters and is expected to continue to do so through next year. Similarly, labor markets continue to tighten. This morning’s payrolls report shows that U.S. labor demand remains very healthy. The economy added 222k jobs in June – well above the estimated 80-100k jobs necessary to hold the unemployment rate constant. Furthermore, wage growth is encouraging, but still historically subdued given estimated tightness of the labor market.

Instead, markets had been caught overly discounting future inflation and rate guidance by central banks, and for good reason. Subdued inflation is a key concern of global policymakers, including the Fed, as the minutes of June’s FOMC minutes revealed this week. Participants are clearly concerned about the persistence of weak underlying inflation, even while they deemed risks to the near-term inflation outlook as broadly balanced.

Worryingly, these structural factors are not expected to recede anytime soon. As such, the question remains of how inflation-targeting central banks plan to respond to a world of rising demand but weak inflation. Historically, this combination has signaled a positive global supply shock, requiring a more accommodative stance of monetary policy, the exact opposite of what has been communicated by some central banks recently. This is because low interest rates are less stimulative to the real economy if price growth is more subdued.

Model simulations utilizing the Fed’s FRB/US model highlights the need for a more accommodative monetary policy stance (Chart 2). The persistence of a -0.5 ppt shock to underlying inflation in the U.S. implies that the fed funds rate should fall by up to 60 bps a year from now. In stark contrast, further labor market tightening, in which the unemployment rate persists 50 bps below the natural rate, would imply an immediate 50 bps increase in the fed funds rate. Altogether, this simulation justifies the FOMC’s cautious pace of monetary policy normalization. The last thing the Fed or other global central banks would want to do is to have to reverse course several quarters from now and risk impairing their credibility.

Fotios Raptis, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.