Financial News for the Week of July 16th 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Fed Chair Powell was in the hot seat as members of Congress peppered him with questions about what the Fed is doing about hot inflation. Core CPI inflation neared a 30-year high in June.

- Travel-related inflation has surged since March as the economy re-opens, driving up core inflation. The Fed is viewing this as transitory for now, but Powell was humble that forecasts are particularly uncertain.

- June retail sales also showed shifting consumer spending patterns, as sales related to going out have accelerated in recent months, while sales related to staying home have lost ground.

U.S. - Consumers are Heading Out and Paying Up

The U.S. data calendar heated up this week, and there is no hotter metric these days than inflation. With the annual pace of core inflation nearing a 30-year high (see commentary), Fed Chair Powell was on the hot seat in Congress, facing a barrage of questions about what the Fed is doing about it. Powell acknowledged that inflation is running well above the pace the Fed typically likes to see. He reiterated previous messaging that the Fed views it is a shock associated with the reopening of the economy – led by pandemic-related bottlenecks and one-time increases in the price of certain services.

However, he did acknowledge that there could be other areas where price pressures bubble up to replace the current sources of price pressures, and the Fed is watching it closely. He stated he doesn’t think we will have to wait long to find out if the Fed’s interpretation is accurate. He was humble that re-opening shuttered parts of an economy at this scale is unprecedented, and forecasts are particularly uncertain.

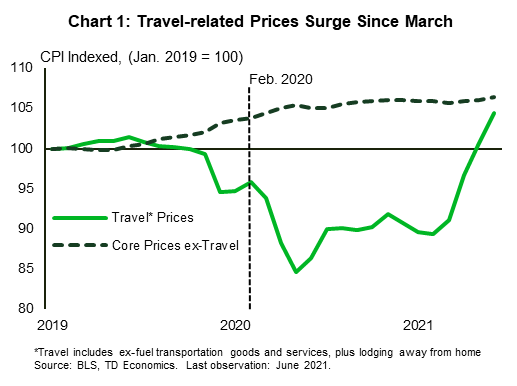

Looking at recent months, the biggest price increases have been in “things associated with travel.” After a year staying close to home, Americans are getting on the road again. Demand for travel-related goods and services is outstripping the industry’s ability to ramp up, and the price increases are steep. Semiconductor shortages have pushed up prices for both new and used vehicles, with knock-on effects on car rental prices. At the same time, prices for hotels, airfares and car rentals are recovering from price plunges early in the pandemic.

Looking at recent months, the biggest price increases have been in “things associated with travel.” After a year staying close to home, Americans are getting on the road again. Demand for travel-related goods and services is outstripping the industry’s ability to ramp up, and the price increases are steep. Semiconductor shortages have pushed up prices for both new and used vehicles, with knock-on effects on car rental prices. At the same time, prices for hotels, airfares and car rentals are recovering from price plunges early in the pandemic.

Since March, these travel related price increases have accounted for over half of the monthly increase in core inflation, despite accounting for less than 18% of the core inflation basket. Stripping them out would have left core inflation running around 0.2% m/m since March (Chart 1). We wouldn’t expect these monthly price hikes to go on forever, but as Powell pointed out, other areas could perk up. Medical care inflation has been decelerating sharply after big increases in 2019, and could accelerate once again. Shelter inflation, ex-hotels also decelerated earlier in the pandemic but is showing early signs of firming. There is plenty to keep an eye on when it comes to inflation.

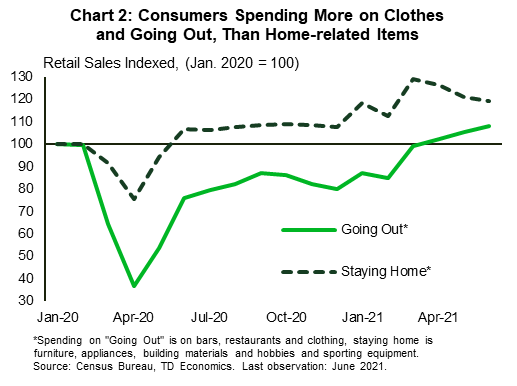

Evidence of shifting consumer patterns as the economy reopens was also seen in the June retail numbers. Overall sales rose 0.6% month/month, ahead of market expectations (see commentary). Sales at bars and restaurants and clothing and accessory stores were both up strongly – categories that could be labelled “going out.” Looking at the trend in this “going out” category, spending started to surge in March, and is now above pre-pandemic levels. On the flip side, spending on things related to staying home – furniture, building materials and sporting goods and hobbies has fallen since March (Chart 2). And, the retail sales numbers do not include spending on other affected services, like haircuts. We will need to wait until the June personal income and spending numbers are released at the end of the month to see how quickly services as a whole are rebounding.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 18th 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

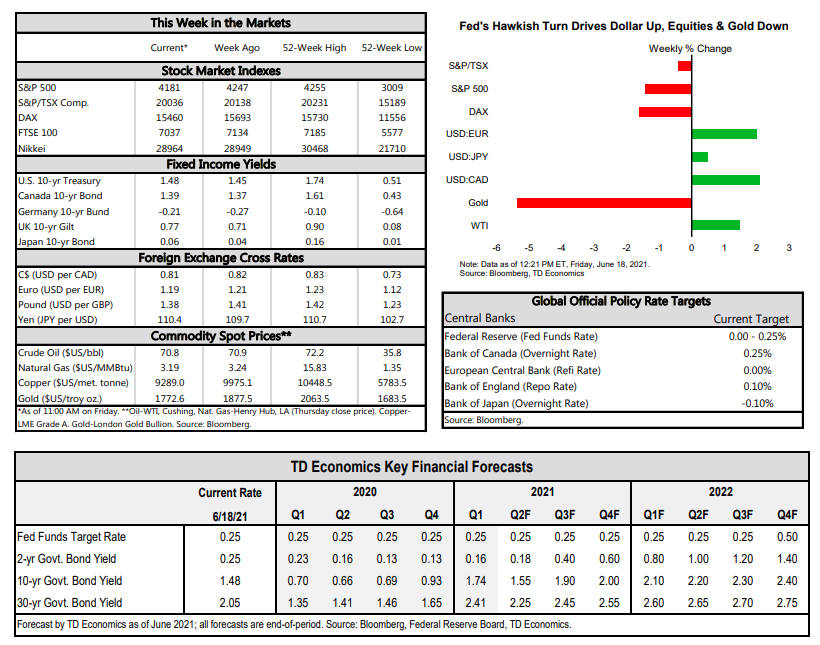

- The U.S. Federal Reserve continues to upgrade its outlook. And while Chairman Powell reiterated that the recent rise in

inflation was transitory, he acknowledged that there was a risk that inflation could be higher than expected. - Most U.S. Federal Reserve officials now expect to start raising interest rates in 2023, a year earlier than previously expected.

- The FOMC statement and Chairman Powell’s press conference this week likely marked the beginning of the end of

pandemic-era ultra-accommodative monetary policy.

U.S. - When Doves Turn Hawkish

All eyes were on the Fed this week. Four times a year the Federal Open Market Committee (FOMC) not only refreshes its policy statement but also gives updates on members’ projections for economic growth, inflation and the federal funds rate. June is one of those meetings. While the FOMC kept policy unchanged, most Fed officials now expect to start raising the federal funds rate in 2023, a year earlier than previously expected. Economic growth and inflation forecasts for this year were also revised upwards.

All eyes were on the Fed this week. Four times a year the Federal Open Market Committee (FOMC) not only refreshes its policy statement but also gives updates on members’ projections for economic growth, inflation and the federal funds rate. June is one of those meetings. While the FOMC kept policy unchanged, most Fed officials now expect to start raising the federal funds rate in 2023, a year earlier than previously expected. Economic growth and inflation forecasts for this year were also revised upwards.

With economic growth getting closer to potential and the labor market strengthening (despite the slight increase in weekly unemployment claims reported this week), the Fed has become more confident in the economic recovery (Chart 1). Success on the vaccine front has a lot to do with it. As the Fed’s policy statement noted, “progress on vaccinations has reduced the spread of COVID-19 in the United States. Amid this progress and strong policy support, indicators of economic activity and employment have strengthened.” While Chair Powell was cautious to add that the economy is not fully out the woods and the fast spreading delta variant could still lead to setbacks, most members were confident enough to raise their forecasts. The median projection for real GDP growth in 2021 was upgraded to 7.0% (from 6.5% in March).

With respect to the labor market, Fed chair Powell struck an optimistic tone. Powell said that “there’s every reason to think that we’ll be in a labor market with very attractive numbers, with low unemployment, high participation and rising wages across the spectrum.” In keeping with the chair’s message, the median unemployment rate forecast was nudged down to 3.8% in 2022 (from 3.9% previously).

With respect to the labor market, Fed chair Powell struck an optimistic tone. Powell said that “there’s every reason to think that we’ll be in a labor market with very attractive numbers, with low unemployment, high participation and rising wages across the spectrum.” In keeping with the chair’s message, the median unemployment rate forecast was nudged down to 3.8% in 2022 (from 3.9% previously).

On the inflation front, the Fed maintains that the recent rise in inflation is “largely reflecting transitory factors” and reiterated that it had the tools to tackle it if needed (Chart 2). While Powell acknowledged that there was a risk that inflation could be higher than expected, the median estimate for core inflation largely kept with the transitory theme. The forecast for 2021 was raised to 3.0% in 2021 but drops back down to 2.1% in 2022 (still up from 2.0% previously).

Meanwhile, the median projection for the fed funds rate remained at the lower bound through 2022 but increased to 0.6% in 2023. Last March, most Fed officials predicted that current rates would be maintained at the zero lower bound until 2024. The new projections now see two rate hikes in 2023.

What is more, while 13 FOMC members think the first hike could happen in 2023, seven members see it happening in 2022. This could well be the start of a trend. With the economic recovery set to continue at a healthy pace, more Fed members are likely to continue to signal an earlier start to the rate hiking cycle. As Chair Powell noted, this is “the beginning of the transition phase.” It could well mark the beginning of the end of pandemic-era ultra-accommodative monetary policy and the shift to a more hawkish Fed.

Sohaib Shahid, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 11th 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Consumer price inflation accelerated to 5.0% year-on-year (y/y) in May, once again coming in ahead of expectations.

Soaring prices for used cars and trucks (up 30% y/y) were a major factor in higher inflation in the month. - Job openings continue to soar, rising to 9.3 million in the latest April data. There are now as many job openings as unemployed people in America.

- The Federal Open Market Committee meets to deliberate monetary policy next week. No change in policy is expected

but look for migration higher in economic, inflation and interest rate forecasts.

U.S. - Fed Meets as Inflation and Job Openings Soar

The Federal Open Market Committee meets next week and will have a lot to mull over as it determines its next policy steps. Since August of last year, the Fed has been aiming to push inflation above 2% – not for its own sake, but to allow the labor market to fully recover from the shock of the pandemic. Inflation has now pushed well above 2% – headline CPI hit 5% year-on-year (y/y) in May of this year – but the labor market is still far from full recovery – in the same month, employment was 7.6 million (5.0%) below its pre-pandemic level in February of last year.

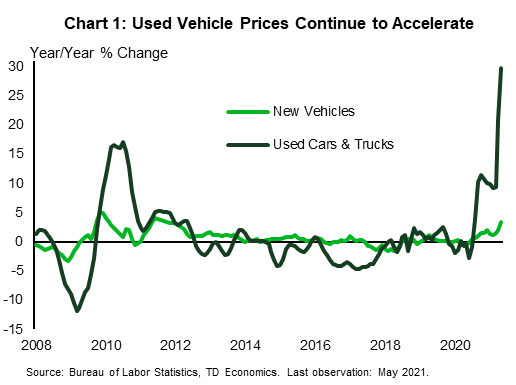

Fed officials have beaten a consistent drum that the acceleration in price growth is “transitory” and reflects the unique circumstances of an economy emerging from a one in one hundred year health shock. They point to the outsized gains in used vehicle prices (Chart 1). Vehicle demand has risen due to the lack of public transit alternatives and supply has fallen as production of new vehicles was stymied first by the pandemic and then by shortages of semiconductors (whose demand also skyrocketed).

Alongside fiscal stimulus, monetary policy has certainly helped to bring demand back to the economy. The challenge is that increasingly, what appears to be holding back the labor market is not a lack of demand, but of supply. The disappointing pace of job growth over the past two months cannot be chalked up to a lack of employer demand. Job openings in April rose to 9.3 million, the highest level on record and over 20% above its pre-crisis peak (Chart 2). There is now effectively a job opening for every unemployed person, the best ratio since January 2020, when the unemployment rate was just 3.5%. Rather, the challenge is that for a number of reasons people are either reluctant or unable to fill those jobs.

This is not to suggest that the Fed should raise interest rates next week or even a year from now. Low interest rates may not solve the supply challenges, but tightening financial conditions could worsen them. The hope is that as the pandemic ends, many of the supply-side constraints will solve themselves. For example, people will be more inclined to take jobs that require close interaction with others. Still, some of the delay in returning to full employment likely reflects deeper reallocation challenges. People who have moved from waiting tables to delivering online orders may not want to go back to their old positions. Or the jobs they used to do may simply not exist in the new digital economy.

In parsing future Fed decisions, look to the evolution of their forecasts. Fed members will clearly have to adjust their near-term inflation views, but longer-term views will be more informative. Similarly, on the economic front, the near-term is likely to see more improvement, but with an increasing chance of even more fiscal stimulus down the road – the Senate this week showed their ability to pass funding for infrastructure when the logic is keeping up with China – upgrades in future years could also come with higher expectations for the federal funds rate.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 4th 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Job growth picked up in May, with the economy adding 559k jobs and the unemployment rate falling to 5.8%.

- ISM indexes pointed to strong growth in manufacturing and services sectors in May, though supply constraints linger.

U.S. - Music to American’s Ears

An overture to May’s economic performance, this week’s data set a positive tone, which we hope will play accelerando from now onward. Friday’s much-anticipated employment report came in slightly lower than forecasters hoped for but had an upbeat spirit with hiring picking up in key sectors and the unemployment rate falling to 5.8% from 6.1% in April.

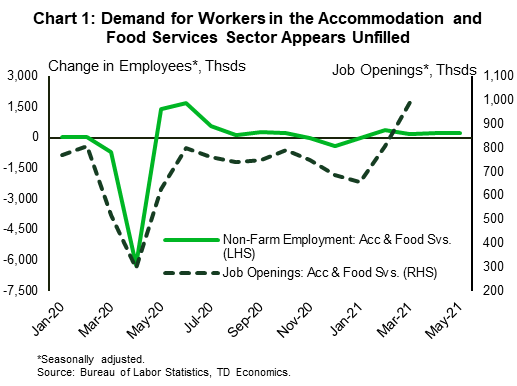

While challenges in finding workers, especially in the low-wage segment, continue to be highlighted in qualitative reports, (including the Fed’s June Beige Book), the pickup in job growth pushes back, at least a little, on the notion that labor shortages are a major constraining factor to the economic recovery. Accommodation and food service firms have been singled out as a sector with a sizeable number of unfilled positions, as echoed in job openings data (Chart 1). This is leading some businesses to offer sign-on bonuses and higher wages. Fortunately, they appear to be working. The sector continued to lead job growth in May, with 221k positions added, accounting for 40% of all the net jobs created in the month.

According to research by the Federal Reserve Bank of Atlanta, wage pressures are concentrated in low-wage service occupations that come with the highest customer contact. While expanded unemployment benefits may be contributing to a reluctance of some people to rejoin the workforce, wage pressures point to a well-functioning labor market where workers are offered higher pay to compensate them for the higher risk of exposure to COVID-19. Nonetheless, half of states have decided to halt federal unemployment subsidies by mid- to end of June in an effort to bring more workers to the labor market. This may hasten the job search for some but will leave those unable to come back to work due to health concerns or lack of childcare to suffer losses in income.

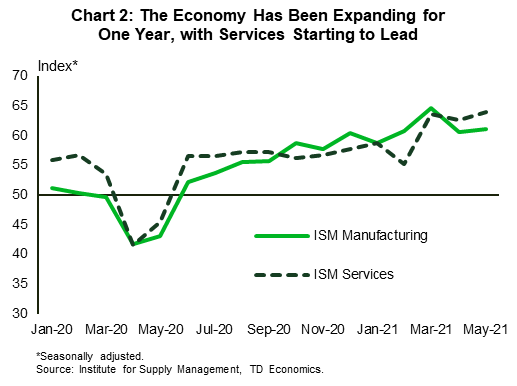

Other economic data also played in a major key this week. The Institute for Supply Management’s (ISM) reports on manufacturing and services sectors registered a full year of growth in a single month in May. The services sector broke its growth record set earlier this year in March, while maintaining an advantage over the manufacturing sector – a phenomenon more typical to “normal” times (Chart 2). Both sectors’ demand indicators gained momentum, while supply bottlenecks seem to have reached a high note with both backlog of orders sub-indexes hitting historical highs.

The Fed continues see these “supply-demand mismatches” as transitory. In a speech this week, Fed Governor Brainard noted that these mismatches are evident “on both the employment and inflation sides of [the Fed’s] mandate”, but also highlighted that the biggest contributors to core PCE last month were categories that are not the typical drivers of inflation. With that, it may be a good time to lower the volume on inflation worries, sit back and enjoy the tune of growing economic momentum.

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 28th 2021

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- First-quarter consumer spending growth was revised up to an even better 11.3% (annualized). Monthly data showed that nominal spending rose 0.5% in April, but inflation-adjusted (real) spending ticked down a touch (-0.1% m/m).

- The Fed’s preferred inflation gauge, core PCE, rose to 3.1% year-over-year in April, breaching the 2% target for the first time since 2018. Speeches from Fed officials earlier in the week helped calm inflation fears.

U.S. - Core PCE Inflation Shoots Above Symmetric Target

A second reading on U.S. economic growth this week left the first quarter print unchanged at a healthy 6.4% (annualized), even as the underlying components shifted. Downward revisions to exports and inventories were offset by upward revisions to business investment and consumer spending. Growth in the latter was upgraded to an even better 11.3% from 10.7% initially, thanks to a stronger showing in goods spending.

A second reading on U.S. economic growth this week left the first quarter print unchanged at a healthy 6.4% (annualized), even as the underlying components shifted. Downward revisions to exports and inventories were offset by upward revisions to business investment and consumer spending. Growth in the latter was upgraded to an even better 11.3% from 10.7% initially, thanks to a stronger showing in goods spending.

Today’s report on personal income and spending provided additional insight on the monthly trend through April. Nominal personal income fell by 13.1% last month, reversing part of the double-digit increase in March that was due to a large infusion of fiscal stimulus. Despite this, nominal personal consumption expenditures (PCE) rose by 0.5% as an improving employment backdrop, plenty of accumulated savings and easing fears regarding the pandemic lifted services spending by 0.6%. Stripping away price effects, real spending edged down 0.1% on the month, but following an upwardly revised gain of 4.1% in March, the second quarter is still in good shape.

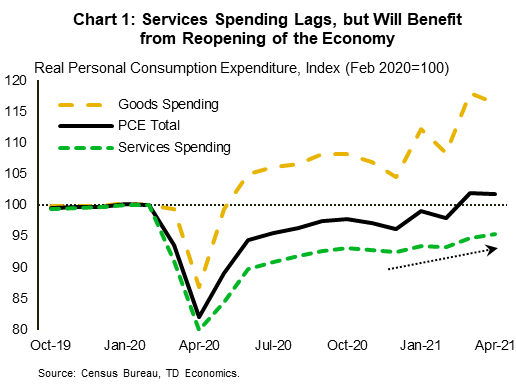

Indeed, consumer spending stands to benefit from the pandemic’s loosening grip on the economy. New COVID-19 cases have fallen from around 260k/day in early January to just 23k/day recently – a massive improvement. A continuation of this trend should lead to the removal of even more restrictions across states in the coming weeks. This bodes well for services spending, which is still below its pre-pandemic level (Chart 1). Improved demand for services will also lend a hand to the sector’s employment recovery.

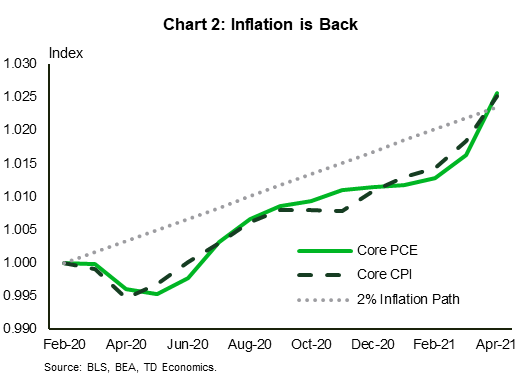

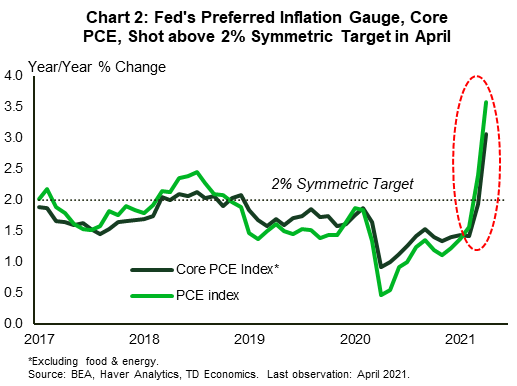

The other item highlighted in the personal income and spending report was inflation. Headline PCE inflation rose to 3.6% year-over-year in April, a notable acceleration from March. Meanwhile, core PCE inflation, the Fed’s preferred inflation gauge, rose to 3.1% y/y – breaching the 2% target for the first time since 2018 (Chart 2). Concerns over rising inflation have led to some market volatility in recent weeks, but the Fed maintains that large price increases will be ‘transitory’. Earlier in the week, a series of speeches from Fed officials drove that point home, with Fed Governor Lael Brainard expressing confidence in the Fed’s ability to “gently guide inflation back to target” should it need to. This helped soothe inflation fears ahead of today’s print. Positive equity market reaction this morning suggests that, for now, investors may be buying into the Fed’s narrative.

The other item highlighted in the personal income and spending report was inflation. Headline PCE inflation rose to 3.6% year-over-year in April, a notable acceleration from March. Meanwhile, core PCE inflation, the Fed’s preferred inflation gauge, rose to 3.1% y/y – breaching the 2% target for the first time since 2018 (Chart 2). Concerns over rising inflation have led to some market volatility in recent weeks, but the Fed maintains that large price increases will be ‘transitory’. Earlier in the week, a series of speeches from Fed officials drove that point home, with Fed Governor Lael Brainard expressing confidence in the Fed’s ability to “gently guide inflation back to target” should it need to. This helped soothe inflation fears ahead of today’s print. Positive equity market reaction this morning suggests that, for now, investors may be buying into the Fed’s narrative.

Transitory simply means “not permanent”, but it could still last for a considerable amount of time. With increased confidence in the economic outlook, there are limits to how long the Fed can stay in wait-and-see mode if it wants to maintain price stability. This suggests an earlier removal of stimulus than its current policy stance implies.

To that effect, there was a slight shift in tone among Fed officials this week, indicating that the time may be approaching to have a conversation about paring back asset purchases. Next week’s May payrolls report will help clarify the progression of the labor market recovery. We expect to see an acceleration from April’s unimpressive outturn, cementing confidence in the improving outlook.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 3, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investors this week were kept busy with the release of the GOP tax reform plan, which sent small cap stocks higher and the S&P 500 lower immediately after its announcement. President Trump nominated current Federal Reserve Board Governor Jerome Powell to succeed Janet Yellen as Chair of the Fed in February 2018.

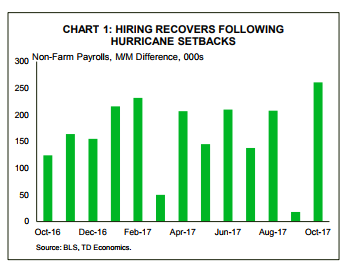

- Volatility as a result of Hurricanes Harvey and Irma skewed data released this week, but the outlook for the fourth quarter remains positive, with hiring in October recovering from hurricane setbacks. Inflation continues to disappoint, with core PCE holding steady in September at 1.3% y/y, and wage growth disappointing in October, rising only 2.4% y/y.

- We expect inflation to reach its 2.0% target late in 2018, with robust economic activity in the meantime giving the Fed enough ammunition to proceed with a rate hike this December.

Investors React to GOP Tax Reform Plan

Thursday’s release of the Republican tax overhaul plan finally gave investors more detail to chew on in determining the winners and losers of the most significant reworking of the tax code in over three decades. The plan slashes the top corporate tax rate from 35 to 20%, and the announcement boosted small cap stocks on account of their higher effective corporate tax rate, while the S&P 500 stumbled in the aftermath of the announcement. The proposal to cut the mortgage interest deductibility in half to $500,000 drove a sell-off in homebuilding stocks. This effective tax increase could dent housing demand particularly in high-priced markets, such as Washington, D.C. and Boston where the median home price already exceeds $500,000. Next, the bill will head to the House Ways and Means Committee before going to the House and Senate for approval. Should the plan progress smoothly, investors should look for small caps to appreciate further while large cap stocks will likely struggle as a result of the scaling back of interest payment deductibles. The USD depreciated as investors weighed the

Other events on Capitol Hill this week included President Trump’s nomination of current Federal Reserve Governor Jerome Powell to succeed Janet Yellen as Chair of the Federal Reserve on February 3rd, 2018. Given Powell’s views that align with the FOMC consensus, markets remained calm following the announcement. Moreover, in addition to tax reform prospects, investor sentiment was supported by indications that economic growth is likely to remain strong this quarter.

While real activity remains rosy, inflation continues to disappoint. Core PCE held steady in September at 1.3% y/y (Chart 2), while wage growth disappointed in October, rising only 2.4% y/y. Weak inflation continues to confound the FOMC, leading the committee to leave its policy rate unchanged this week. However, as the unemployment rate continues to push further below its natural rate, inflation is likely to gain traction in the year ahead and is expected to reach its 2.0% target late in 2018. We expect that these pressures should give the Fed enough ammunition to proceed with a rate hike this December.

Katherine Judge, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

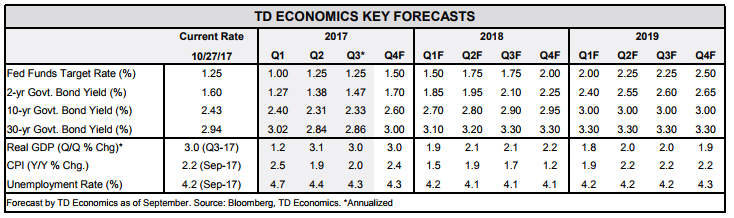

Financial News for the Week of October 27, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S. equities this week managed to recover from earlier losses following strong earnings and a series of upbeat economic

data. Durable goods orders and new home sales surprised to the upside, while the House approved a budget

plan, adding to the upbeat tone. - The advance estimate for third quarter GDP growth of 3% (annualized) came in better than expected despite hurricane

impacts weighing on domestic demand. - The ECB announced a reduction in its pace of asset purchases and extended its bond-buying program through September

2018 or beyond if necessary, acting to affirm a growing policy divergence between the ECB and the Fed.

U.S. Economy Steams Ahead at 3% Pace

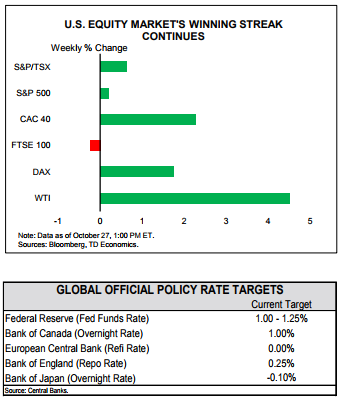

Financial Stocks gained this week on the back of strong earnings reports and on upbeat economic data. Durable goods orders rose 2.2% (m/m) in September – more than double the expected rate, while new home sales surged an impressive 18.9%. Although the latter can be partially attributed to a rebound in hurricane-hit areas, improvements were recorded in all regions, as activity was likely boosted by significant inventory shortages in the existing home market. The passing of a budget plan in the House, another step forward toward tax reform, added to the upbeat tone and proved particularly beneficial to Treasury yields and the U.S. dollar.

The most anticipated report of the week, BEA’s advance GDP estimate, reflected this positive momentum. Growth for the third quarter came in much better than anticipated, with the economy expanding at 3% (Q/Q annualized) despite hurricane impacts. The latter did appear to weigh on a few categories, such as services spending and both residential and non-residential construction, all of which dragged on domestic demand (Chart 1), although inventory restocking helped provide some offset. Net trade also contributed positively to growth, but likely reflected a hurricane-related fall in imports, suggesting some giveback ahead. Still, with rebuilding likely to lift fourth-quarter economic growth via a rebound in domestic demand, another print of around 3% appears to be in the cards. Given estimated trend growth of 2.0%, another quarter of above trend growth is consistent with a continuation of the current interest rate hiking cycle. As such, a December rate hike appears very likely, provided that we also see some cooperation from inflation metrics.

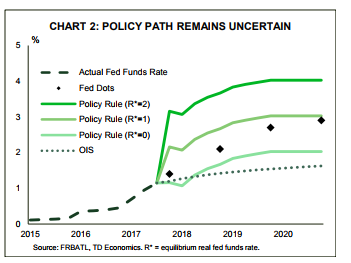

Beyond 2017 however, the interest rate path is more uncertain. This is not only due to evolving growth and inflation dynamics, but also a possible radical makeover of the Fed, which has a number of open Board of Governor positions and may soon get a new Chair. Among the frontrunners for the top position, former Fed Governor Kevin Warsh and Stanford professor John Taylor are regarded as somewhat of a challenge to the status quo, given their apparent preference for a more rules-based approach to setting interest rates. The current Fed under Chair Yellen views monetary policy rules more as guideposts and argues against a mechanical approach, the shortcomings of which include the failure to capture current cycle dynamics

and the difficulty in measuring the input variables. The latter can lead to significantly different paths (Chart 2, see report). Nevertheless, in the event that a strict rules based approach to monetary policy is implemented, it would point to a faster pace of interest rate normalization.

A number of humdrum central bank meetings took place thisweek,with Canada, Sweden and Norway keeping rates on hold. In contrast, the ECB meeting was more eventful as it announced an open-ended extension of its asset purchase program through September 2018 and a reduction in its pace of asset purchases to €30B/month starting in January 2018 from the present €60B pace. However, monetary policy is likely to remain loose in the Euro Area for some time as it lags the U.S. on both the inflation and employment front. This divergence in monetary policy is likely to remain a key driver of exchange rate moves for the foreseeable future.

Admir Kolaj, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of September 29, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investors paid close attention to developments from the White House this week, with President Trump’s tax overhaul proposal helping to send the S&P 500 to new highs.

- Inflation disappointed again in August, but some states are beginning to display meaningful wage acceleration, as we noted in our Quarterly State Forecast this week, which bodes well for the inflation outlook.

- Next week, investors should look for hurricane impacts to inject volatility into September’s U.S. data. As a result, auto sales should see a boost while net exports should experience a drag.

Equities Soar on Trump’s Tax Reform Proposal

Investors paid close attention to developments from the White House this week, with President Trump’s tax overhaul proposal sending the S&P 500 to another record high at the end of the week. Exchange and fixed-income markets were also impacted, with the greenback appreciating and the ten-year yield rising to its highest level in two months. The proposal contains a sharp reduction in the corporate tax rate to 20% (from 39.1% currently), in addition to the consolidation of personal income tax brackets from seven to three. But the Devil is in the details, of which the plan was largely barren. If delays or opposition to the proposal prevail, equities could pare their gains on diminished expectations for future earnings.

Meanwhile, on the economic data front, Friday’s PCE report marked another month of decelerating inflation in August (Chart 1). Consumer spending was also weak, but that is partly attributable to Hurricane Harvey’s disruption. The report disappointed markets, but not by enough to reverse the equity gains accrued as a result of President Trump’s tax plan announcement earlier in the week.

Across the Atlantic, the Euro Area is also grappling with missing inflation coinciding with solid economic growth. Underlying inflation in September remains subdued, reinforcing the ECB’s stance of cautiously tightening monetary policy. The first steps in winding down asset purchases are expected to begin next year, with further details anticipated following the ECB’s October meeting. Consumer and business confidence indicators have recently returned to pre-recession levels and investors have taken notice, with both the DAX and the FTSE ascending this week while German and UK government bond yields rose.

Next week, investors should look for hurricane impacts to inject volatility into September’s U.S. data. Specifically, auto sales should see a boost while net exports should experience a drag. This volatility should fade as rebuilding begins in the fourth quarter. While the Fed will look past hurricane disruptions in the data, inflation data will remain central in guiding monetary policy.

Katherine Judge, Economic Analyst

Financial News, Sept. 29, 2017

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

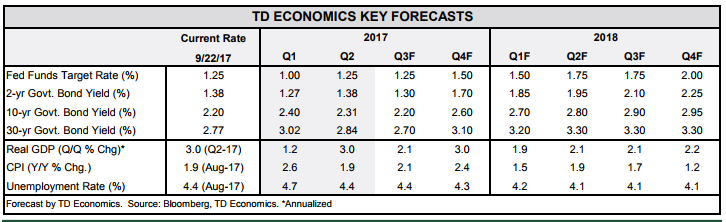

Financial News for the Week of September 22, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Finally, midway through 2017 global growth is looking better than it was a few months ago. Our latest Global Outlook discusses how the optimism that has been missing for several years has finally returned.

- With stronger global growth comes tighter monetary policy. This week the Fed formally took the next step of starting to reduce the size of its balance sheet.

- The Fed also reaffirmed that it expects to hike rates again this year. Our U.S. Outlook looks solid over the next two years, despite the hit from the devastating hurricanes. Reduced economic slack should lead to higher inflation, consistent with a gradual pace of rate hikes over the next two years.

We’ve Got To Admit Its Getting Better

In recent years, economic growth forecasts have suffered from serial disappointment. Economic outlooks have typically been downgraded part way through the year, but not so this time. Our latest Global Outlook discusses how a broadening and strengthening of expansions in advanced and emerging economies has helped restore a sense of optimism in the global economy that has been missing for several years.

The Federal Reserve is further along in reducing monetary stimulus, with four rate hikes under its belt. This week it formally announced that it will start reducing the size of its $4.4 trillion balance sheet in October. The pace will be very gradual, with the monthly runoff amounting to 0.2% of its balance sheet. The process was already laid out clearly in June, and as such there was little reaction in the longer end of the curve.

Markets paid greater attention to the Fed’s message on future rate hikes, and how that may have changed given the softness in inflation this year. Yellen acknowledgedthat not all of the weakness in inflation can be chalked up to transitory factors (as we discussed in our latest forecast). However, interest rate projections for the nearterm were left unchanged. The median expectation of Fed members is for one more hike this year and three hikes in 2018. Confirmation that the Fed hasn’t lost its faith in the Phillips curve did produce an upward move in shorter-term yields. And, the odds on a rate hike in December have shifted from a coin flip to being roughly two-thirds priced in.

The Committee also indicated that recent hurricanes are likely to impact inflation and economic activity in the near term, disrupting it first and then boosting it thereafter as rebuilding begins. However, the storms are “unlikely to materially alter the course of the national economy over the medium term.” As such, we expect the Fed to see through any of the volatility in the data over the coming months, with the storms unlikely to prevent the Fed from potentially raising rates at their December meeting – particularly if inflation data firms as we expect.

Overall, the U.S. economy is expected to continue its “Steady-Eddie” performance of slightly better than 2% growth over the next few years. Upside and downside risks to this outlook remain: either from a fiscal boost from Washington or from delayed capital spending due to policy uncertainty on taxes or NAFTA renegotiation.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

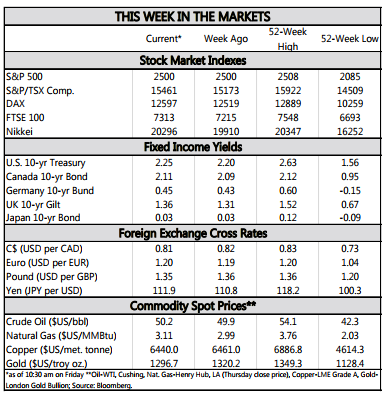

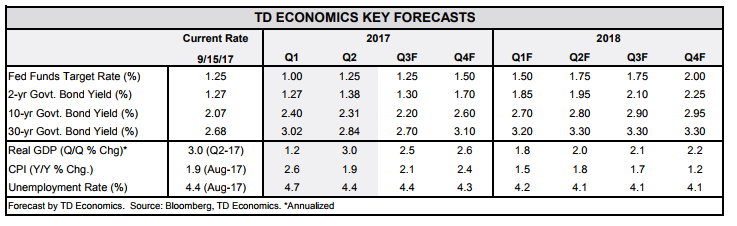

Financial News for the Week of September 15, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investors and analysts reading the economic tea leaves were given mixed messages this week. On the one hand, inflation ticked up, but on the other, consumer spending softened.

- Consumer prices rose 0.4% (m/m) in August, pushing inflation to 1.9% (y/y) from 1.7%. A sharp rise in gasoline prices on the back of refinery shutdowns contributed to the gain. Core prices accelerated to 0.2% (m/m).

- Retail sales, on the other hand, fell 0.2% in August. With downward revisions to June and July, momentum in consumer spending has slowed heading into the third quarter relative to its blistering pace in Q2.

The Data Giveth and the Data Taketh Away

Investors and analysts reading the economic tea leaves for signals on future Federal Reserve policy were given mixed messages this week. On the one hand, inflation ticked up, but on the other, consumer spending softened. Further muddying the water, both the CPI and retail sales reports were affected by Hurricane Harvey, a phenomenon that will continue in the months ahead.

One of the chief concerns of the Federal Reserve recently has been the persistent weakness in inflation. Despite ongoing improvement in the job market and an unemployment rate comfortably below target, price growth been slowing for much of this year. Inflation according to both the overall CPI and the core measure peaked in February. Energy prices contributed to inflation early in the year, but the impact was fleeting. Moreover, the weakness in inflation cannot be attributed entirely to idiosyncratic factors. Measures that strip them out, such as median and trimmed-mean inflation, have also decelerated noticeably.

One month does not a trend make, but August may be an early sign of a reversal in this downward trend. Headline consumer prices rose 0.4% on the month, pushing year-on-year inflation to 1.9% from 1.7%. A sharp rise in gasoline prices (6.3% month-over-month) on the back of refinery shutdowns due to Hurricane Harvey contributed to the gain in the headline.

More convincing was the gain in core prices and in the aforementioned median and trimmed mean measures. Core prices rose 0.2% on the month (0.249% to be precise), the strongest gain since January. While Harvey may have had some impact on core prices, the acceleration was broad-based with both median and trimmed-mean prices accelerating noticeably (both up 0.2%).

For the Federal Reserve, evidence that inflation may finally be heading higher should provide confidence that the economy is ready for higher interest rates. However, it will also want to see signs that the economic recovery remains on track. In that regard the pullback in retail sales (down 0.2% in August) provided a cautionary note As with the CPI data, Hurricane Harvey was likely an influence, especially for auto sales, which fell 1.6% in dollar terms (units fell 4%). Nonetheless, downward revisions to both June and July suggest less momentum in consumer spending even prior to Harvey. While spending is likely to rebound as the recovery efforts from Harvey and Irma take shape, a broader-based slowdown will not go unnoticed at the Fed.

All of this comes as the FOMC is due to meet to deliberate policy early next week. The Fed appears unlikely to hike its key lending rate at this meeting, but it is likely to announce plans to gradually begin unwinding its balance sheet. These have been well telegraphed to markets with most of the impact on bond yields already priced in. More important will be how much the statement recognizes the recent moves in inflation and how this comes through in the expectations of FOMC members for future policy rates, which will be released in the Survey of Economic Projections along with the policy statement. -4 Stay tuned until Wednesday afternoon for more details.

James Marple, Director & Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.