Financial News for the Week of September 30, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Concerns over German banks and a surprise production cut announcement by OPEC provided some volatility to financial markets this week.

- Economic data was mixed this week. Second quarter real GDP was revised up to 1.4% (from 1.1%), and August goods exports beat-expectations. This was offset by weaker-than-anticipated consumer spending data in the month, which declined 0.1%.

- While the composition has shifted slightly toward foreign demand and away from domestic demand, the economy continues to track real GDP growth close to 3.0% in the third quarter, enough for the Federal Reserve to remain on course for a December rate hike. A key data point to watch on this front is next week’s payroll report for September, where we expect a gain of 160k jobs – slower than earlier in the recovery, but still consistent with ongoing labor market improvement.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

VOLATILITY TO CONTINUE

Concerns over German banks and a surprise production cut announcement by OPEC provided some volatility to financial markets this week. Equity markets were up following the OPEC

The see-saw action is likely to continue as financial markets digest a number of key event risks over the next several months including the U.S. election, another OPEC meeting in November, an Italian constitutional referendum, and last but not least, a potential rate hike by the Federal Reserve.

OPEC’s extraordinary meeting was light on details, but telegraphed its intent to cut production to a target range between 32.5 and 33 million barrels a day. The WTI benchmark price rose an initial 5% from $44 to over $47 in reaction to the cut and has moved above $48 per barrel this morning. This is likely to be the extent of the impact, however, as continued oversupply should limit any further price gains. We expect prices to remain in the US$40-50 per barrel range in the near term, before gradually trending above US$50 per barrel in 2017 as the market moves into a more balanced position.

Still, slowly rising oil prices should provide some reprieve to shale producers and limit any further reductions in oil-related investment. This is welcome following six straight quarters in which declining oil exploration has cut an average of 0.3 percentage points (annualized) from quarterly real GDP growth. Unfortunately, overall business investment will continue to be a weak spot for the American economy in the third quarter, as telegraphed this week by a 0.4% decline in core durable goods shipments. The good news is that even as shipments fell, new orders rose, suggesting

that investment will pick up in the months ahead.

Other economic data was mixed this week. Second quarter real GDP was revised up to 1.4% (from 1.1%), largely on a smaller declines in business investment and stronger export growth. Export momentum continued into the third quarter with a 1.5% increase in August. Combined with a smaller gain in imports, net exports should contribute positively to third quarter growth.

These positive developments were offset by a downward revision to consumer spending (to 4.3% from 4.4%) in the second quarter and a disappointing outturn for monthly spending in August. Led by a pullback in durable goods, real personal consumption expenditures declined 0.1% on the month. As a result, the tracking for consumer spending growth has fallen to 2.7% (from 3.0% in our recent QEF). All told, while GDP is still tracking growth of slightly under 3.0%, the composition suggests a bit more foreign demand and a bit less domestic demand. As long as this progress is maintained, the Federal Reserve will remain on track to raise interest rates. With a rate hike a week before the November election unlikely, a December hike still appears the most likely scenario. A

key data point to watch on this front is next week’s payroll report for September, where we expect a gain of 160k jobs– slower than earlier in the recovery, but still consistent with ongoing labor market improvement.

James Marple, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of September 23, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The Bank of Japan announced two new policy measures this week, aiming to target the interest rate on the longer-end of the curve at zero, and pledging to let inflation overshoot the target – effectively committing to be slightly irresponsible. Still, a lack of an interest rate cut fanned the view that the BoJ may be running out of ammunition, which together with fears that these moves are too late, has thrown into question the efficacy of the new measures.

- The Fed also left its policy rate unchanged on Wednesday, albeit only “for the time being.” The case for a rate hike has strengthened, according to the Fed, with three members wanting to lift rates this week-exemplified by a rare triple dissent. The Fed has all but set itself up for a hike later this year, with most members remaining optimistic for the economic outlook. Having said that, future rate hikes are likely to be more gradual, with the Fed’s own projections toned down alongside potential growth estimates.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

FED STANDS PAT... FOR THE TIME BEING

This week has been rather an exhilarating one in financial markets. Alongside some weak data on domestic housing activity, investors were treated to two major central bank announcements

The Bank of Japan surprised many investors by adopting a couple of policy measures that were previously thought of as too radical by the bank. The first, referred to as yield curve control, aims to target the interest rate on the longerend of the curve at zero. The BoJ has essentially announced it will buy any 10-year JGBs should their price fall to that level. Secondly, Governor Kuroda pledged to let inflation overshoot the target – effectively committing to be slightly irresponsible. The BoJ also tweaked its QE allocation, aiming to buy more short-term debt to help steepen the yield curve and reweighing ETF purchases towards the domesticoriented Topix index away from the export-heavy Nikkei.

The BoJ did not lower interest rates, merely suggesting that such a move remains a “possible option for additional easing.” Lack of a cut fanned the view that the BoJ may be running out of ammo, which together with fears that these moves are too late, has thrown into question the efficacy of the new measures. The Bank has failed to fend off the deflationary mindset for years, with the pledge to overshoot only helpful if the target can be reached in the first place.

Across the Pacific, the Fed too, left its policy rate unchanged on Wednesday.

As such, the Fed has all but set itself up for a hike later this year. Fourteen of the seventeen officials now expect a rate hike later this year. Moreover, three of the ten voting members wanted a hike this week - a rare dissent that highlights divisions on the Committee. The Fed has made significant progress towards its dual objectives, particularly on the jobs front, with most believing the U.S. labor market is nearing full-employment. At the same time, while inflation remains below target suggesting patience, lags in monetary policy and fears that the fully utilized resources will soon begin to manifest on prices level appear to be swaying more members to want to get ahead of the curve.

All this suggests that the Fed will move sooner, but proceed more gradually. Such a scenario is corroborated by Fed members’ own projections, which have been revised lower and suggest a shallower path for future rates. Given the U.S. Presidential elections, we expect the Fed will opt to wait until December to raise rates. This should be a short-enough delay to keep the hawks at bay, while providing enough time to gather evidence of U.S. economic resilience. Having said that, such an outcome is not assured, with risks ranging from global imbalances to U.S. elections far from immaterial.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of September 16, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Market volatility picked up this week after a post-Brexit summer slumber, with moves dominated by speculation on whether we’ve seen the bottom for longer-term global interest rates. Hawkish statements by Fed presidents were trumped later by governor Lael Brainard’s speech, convincing the market that the fed will wait until December for its next rate hike.

- Mixed U.S. economic data this week was consistent with a cautious, patient Fed. Weaker than expected retail sales and industrial production data for August suggested modestly slower growth in 16H2, while stronger inflation data is consistent with absorption of economic slack.

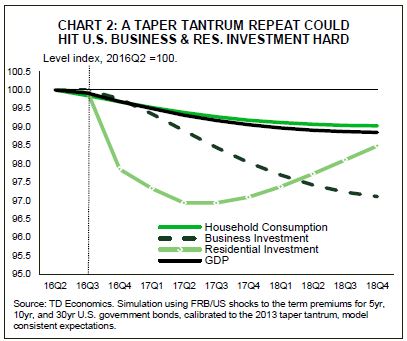

- Global economic data show growth picking up in the second half of the year, but financial fragilities remain at the forefront. Speculation about BoJ policy added to the pressure this week, spurring a sell-off in advanced economy bonds. A repeat of the 2013 taper tantrum episode would have serious negative repercussions on the U.S. outlook.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

VOLATILITY RETUNS IN SEPTEMBER

In the lead-up to next week’s FOMC meeting, market action this week was dominated not only by speculation of whether the Fed would raise rates, but also concerns that maybe, just maybe,

The global data flow this week was generally positive, confirming that demand is heating up in the second half of this year. UK retail sales for August failed to fully reverse the strength in July, giving further credence to the idea that the UK economy post-Brexit is generally evolving in line with the Bank of England’s August forecast. Furthermore, Chinese data for August confirm that growth will remain close to 7.0% (annualized q/q) in the third quarter, driven by strength in the services sector.

However, underneath this thin veneer of global stability

As we show in Chart 2, a shock to U.S. term premiums similar in magnitude to that observed in 2013 would be detrimental to the outlook for the U.S. economy. Business and residential investment would be hardest hit, falling close to 3% and 2.5% respectively below our baseline by the end of 2018. Overall, U.S. economic output would be about 1.2% weaker.

All told, with signs that excess slack continues to be absorbed in the U.S. economy and global demand is recovering, conditions are ripe for a fed rate hike. However, the risks remain titled to the downside, implying that a cautious Fed will likely defer a rate hike until December.

Fotios Raptis, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 26, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Economic data this week were supportive of the narrative of ongoing improvement in activity. Despite a slight downward revision to estimated real GDP growth in the second quarter (1.1% from 1.2%), the details showed an upward revision to consumer spending and business investment and a slightly larger drawdown in inventories.

- Janet Yellen’s speech in Jackson Hole noted the improvement, saying at “in light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal funds rate has strengthened in recent months.”

- With considerable uncertainty around the eventual neutral interest rate, the pace of future rate hikes will be glacial and contingent on ongoing calm in global financial markets.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

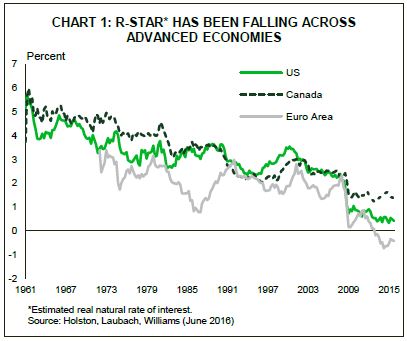

THE FAULT IS IN R-STAR

If you have been paying attention to Fed speak over the dog days of summer, you have likely heard talk of the “r-star.” It sounds arcane, but don’t let that fool you. While the concept is theoretical, its implications are real. As the Federal Reserve considers its next steps in normalizing monetary policy, estimates of “r-star” or neutral rate of interest will be a key determining factor.

Stated simply, the neutral rate is defined as the rate of interest at which there is neither upward or downward pressure on inflation. In theory, this rate is determined by the supply of savings relative to the demand for investment. In practical terms, the neutral rate is influenced by things like population growth, aging, and productivity growth.

The important point for investors is that current estimates of the neutral rate are thought to be much lower than in previous cycles. According to a paper co-authored by San Francisco Federal Reserve president John Williams, the current real (inflation-adjusted) neutral rate is somewhere in the neighborhood of 0%. With inflation of 2%, this implies a nominal neutral rate that is also 2%.

A few points bear making. One, there is no guarantee that the current neutral rate will remain the prevailing rate in the future. Shifts in preferences for saving or in opportunities for productive investment can shift the r-star. Unfortunately, estimating the neutral rate is an inherently backward looking process and gives us little indication of its future path. Second, a time varying neutral rate adds another layer of uncertainty to predicting the actual course of monetary policy. One can see this in Federal Open Market Committee (FOMC) participants’ own expectations for the fed funds rate. While the current consensus in terms of the long-run rate appears to be in the neighborhood of 3.0%, it has fallen 80 basis points since reporting began over the last year.

Even more, there appears to be little agreement about when this longer-run rate will prevail. At least one FOMC participant, James Bullard of the St. Louis Federal Reserve, has a base-case

This provides important context for debate currently occurring both within the fed and in financial markets about when the Fed will next raise interest rates. A chorus of Fed speakers have sounded the drum on the likelihood of an imminent rate hike. Janet Yellen, in her speech Friday in Jackson Hole, noted that “in light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal funds rate has strengthened in recent months.”

Given the stream of recent economic data, including this week’s revision to second quarter GDP growth, which showed an even higher rate of consumer spending and modestly upgraded inflation, the odds of the Fed raising rates before the end of this year are close to even. Nevertheless, there is little reason to expect the neutral rate to move much from its current low level. This means that the most that can be expected in terms of future rate hikes is one to two per year. And as we’ve seen over the course of this year, it will not take much in terms of global financial volatility to put off even this very modest pace of tightening.

James Marple, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 19, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The week offered plenty of data to gauge the strength of the global economic recovery, with the generally dovish rhetoric from major central banks, including the Fed, supporting global equities which also got a lift from the surge in oil prices.

- International data remained soft, solidifying expectations for further stimulative action from both the ECB and BoJ as soon as next month.

- U.S. data remained resilient, particularly so for domestically oriented sectors of the economy. Still, externally exposed manufacturing and mining activity appeared to rebound, suggesting that the worst may be behind these externally-exposed sectors.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

FED AT THE CROSSROADS OF MONETARY POLICY

The recent week offered ample economic data, both domestic and international, to gauge the strength of the global economic recovery. Helping frame the discussion on both sides of the Atlantic was a bounty of central bank communications. The generally dovish rhetoric from major central banks, including the Fed, has supported global equities which also got a lift from the surge in oil prices related to anticipated action from OPEC next month.

International economic data has not inspired much confidence in global economic resilience, somewhat disconcerting given rising global risks. Japanese economic growth stalled last quarter as the yen strength exerted a drag on trade, spurring expectations for further stimulus from the Bank of Japan when it meets next month. Ditto for the ECB, which is anticipated to ease further when it meets in September, motivated by slowing growth, potential Brexit fallout, and the associated downside risk to inflation. Headline prices in the Eurozone fell 0.6% in July and are up only 0.2% from last year, while core inflation – which typically leads the headline – remained stuck below 1% for ten months despite the substantial stimulus already implemented.

The global themes have become a growing source of concern for the Federal Reserve. According to the minutes from the late-July meeting, released midweek, many FOMC members have become increasingly concerned about the potential for external shocks to affect the U.S. outlook. Despite diminished near-term risks, the medium- to longer-term risks have become all the more entrenched in Fed discussions. Moreover, the significant disinflationary impulses from abroad and still low inflation expectations at home appearto have shaken confidence amongst many FOMC members about getting back towards the 2% target. Inflation figures for July underwhelmed expectations, with the headline and core rate slipping slightly to 0.8% and 2.2% y/y, respectively.

But, while the Fed is cognizant of risks, it has also acknowledged that the U.S. recovery is on a relatively solid footing. In fact, the recent upbeat information had alleviated some of the concerns about continued labor market improvement. Domestic-oriented data remained positive this week with the pace of homebuilding up to above 1.2 million (annualized) in July, while the near record-low initial jobless claims suggesting strength in the labor market through August. These data confirm that consumption and housing will remain a key support for the ongoing U.S. recovery. Furthermore, both manufacturing and mining, which are more externally exposed have been hard-hit, but have recently made progress despite weakness abroad.

The diminished risks and positive data flow have emboldened hawkish members of the Committee, highlighting the growing divergence of views. Two participants were ready to raise rates in July, with recent commentary by influential FOMC members attempting to boost expectations for a hike. While we don’t rule out a scenario in which data continues to surprise to the upside and enable the Fed to raise this year – something the markets feel is an even bet – we feel that patience levels have increased amongst the FOMC alongside fears of global disinflationary pressures and low-growth outcomes. As such, we expect the Fed to sit tight through the end of this year, proceeding only cautiously thereafter.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of August 12, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S. stock markets reached new highs this week, with the S&P 500, Dow, and Nasdaq all breaking records, but the economic data has been disappointing. Retail sales data for July suggests a slow start to third quarter consumer spending, which is now tracking 3% - much slower than the 4.2% pace last quarter.

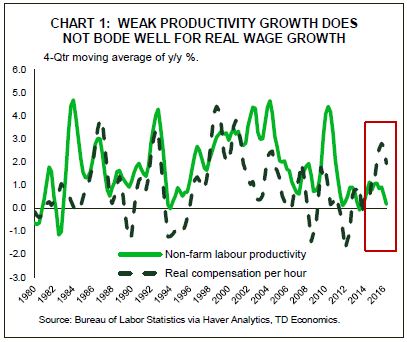

- Data on labor productivity growth released this week indicated a third consecutive quarterly decline. Falling productivity has highlighted the risks of the U.S. falling into a low-growth phase with persistent weakness in labor productivity boding poorly for real wage growth.

- In light of the elevated level of global economic uncertainty and the structural headwinds exerting downward pressure on the long-run growth rate of the U.S. economy, it would be prudent for the FOMC to delay tightening until there were clear signs that the U.S. economy is generating persistent inflationary pressures – something that’s unlikely to take place until next year.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

MORE EVIDENCE BUILDSFOR THE FOMC TO DELAY TIGHTENING

U.S. stock markets reached new highs this week, with the S&P 500, Dow, and Nasdaq all breaking records, but the economic data has been disappointing. Labor productivity declined for the third consecutive quarter in Q2, while this morning’s flat July retail sales report suggested consumer spending slowed at the start of the third quarter, with personal consumption expenditures on pace to grow by 3.0% during Q3. While this is not unhealthy growth, it is nonetheless a significant slowdown from the robust second quarter pace of 4.2%, and suggests less support for third

Economic growth is still poised to exceed the estimated sustainable trend rate of growth. Alongside a tightening labor market and a pick-up in inflation expectations, one could argue in favor for some removal of monetary accommodation in the near term. However, the case for remaining patient and delaying tightening appears to be strengthening. For one, the rise in global economic uncertainty since the UK referendum has accentuated the risk that a small crisis in an EU nation, possibly triggered by a bank failure, could spread more broadly through financial linkages. The risk that heightened financial market volatility, likely to result in a rapid appreciation in the U.S. dollar, is sure to keep the FOMC on the sidelines.

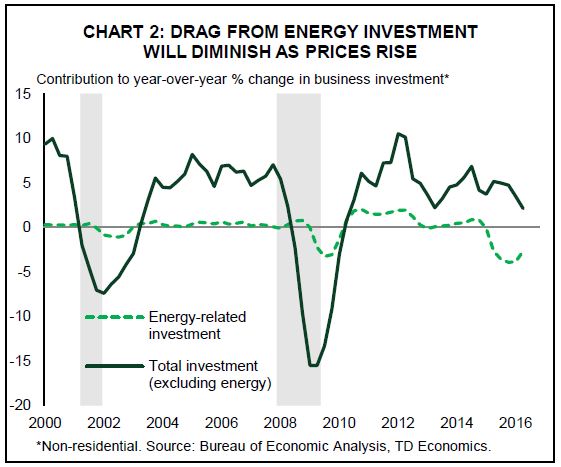

Secondly, there are also signs that not all is well domestically. The persistent weakness in labor productivity growth is a cause for concern (Chart 1). Lack of an increase in output per hour worked does not bode well for real wage growth despite a tightening labor market. Weak labor productivity growth is generally a reflection of a confluence of factors. One such factor is a lack of significant investment in capital necessary to produce a unit of output. The recent disappointment in non-energy business investment speaks to this (Chart 2). Furthermore, the rate of how quickly firms are

incorporating innovative ideas and processes that enhance their efficiency has slowed markedly in the aftermath of the financial crisis.

Lastly, there is a high level of uncertainty about the current amount of monetary stimulus supporting the U.S. economy. Recent estimates of the current real neutral rate for the U.S. economy

range from 0.2% to -1.0%. With the nominal fed funds rate near 0.35%, and core PCE inflation tracking around 1.6%, this implies a real fed funds rate of about -1.25%. This suggests a fair amount of monetary accommodation in the economy if the real neutral rate is close to zero, but the accommodative cushion nearly vanishes if the neutral rate is closer to the bottom of the estimated range. In fact, in such a scenario, a 25 bp move up in the FOMC’s target rate would remove all remaining monetary accommodation.

Overall, given the elevated level of global economic uncertainty, a U.S. economy facing structurally lower long-run growth prospects, and uncertainty about the current amount of monetary stimulus, it would be prudent for the FOMC to delay tightening until there were clear signs that the U.S. economy is generating persistent inflationary pressures – something that’s unlikely to take place until next year.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

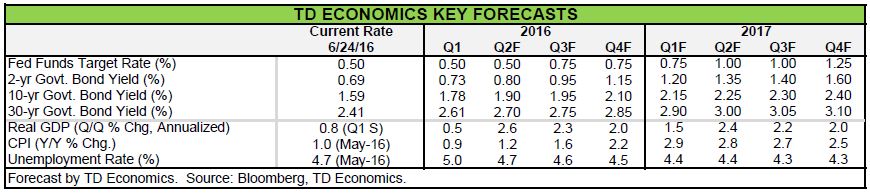

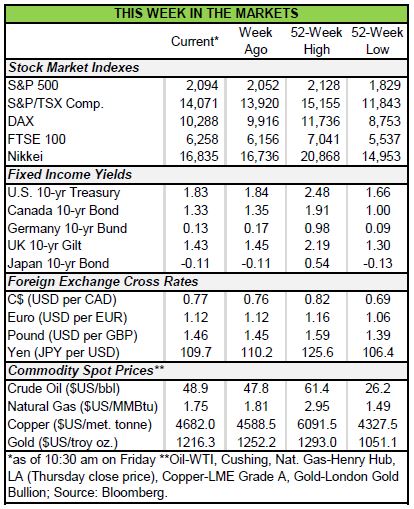

Financial News for the Week of June 24, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets were on tenterhooks all week in anticipation of the British referendum, with anxiety turning to panic overnight as Britain, in a historic vote, decided to leave the European Union (EU).

- Central banks announced readiness to deal with any fallout related to potential liquidity shortages, helping stem near-term pressures in global markets but longer-term implications of the vote are far from certain. Still, there is little doubt that the economic implications are a net-negative and could be far reaching.

- In her semiannual testimony to Congress mid-week, Chair Yellen noted the potential for “significant economic repercussions” of such an outcome that could “usher in a period of uncertainty,” and negatively affect U.S. economic activity, with the Fed likely to monitor global developments closely.

- Given the implications for slower U.S. growth and lower inflation, on account of the fallout, we expect the Fed will stay pat through the rest of the year.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

KEEP CALM AND TRADE ON... AS BRITAIN LEAVES THE EU

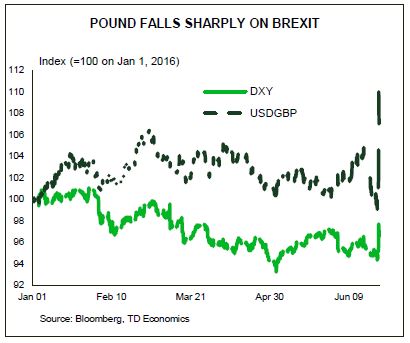

Markets were on tenterhooks all week in anticipation of the UK referendum. Anxiety turned to panic overnight as Britons, in a historic vote, decided to leave the EU. Despite the very close polls ahead of the vote investors increasingly positioned themselves for a status-quo result. In fact, sentiment was decidedly risk-on right through until voting booths closed at 10pm GMT. But, as results started to trickle in, doubts surfaced, with the BBC finally calling the vote for the “leave” camp at 4:45am London time. The final tally was 51.9% to 48.1% with 1,269,501 more votes cast in favor of divorcing the UK from the EU. Turnout was high, at 72.2%, but fell shy of that level in London, Scotland, and Northern Ireland – all bastions of the “remain” camp.

The pound fell as much as 12% versus the dollar as the outcome became clear. Gold and volatility surged while equities and the safest of bond yields slumped, before some retracement this morning. At this point, central banks have announced their readiness to deal with any near-term fallout related to potential liquidity shortages, with the Federal Reserve noting it is prepared to provide dollar liquidity through existing swap lines with major central banks. The concerted central bank move should help stem near-term pressures in global markets. But, longer-term implications of the vote are far from precise given the rapid and substantial repricing in global markets, the ensuing volatility, and uncertainty of the political response on both sides of the channel.

Despite the unknowns, there is little doubt that the economic implications are a net-negative and could be far reaching. The uncertainty and lack of access to the common market will almost surely decimate business investment in the UK and probably stifle trade with the EU (and potentially others) – something that’s not likely to be fully offset by the slumping sterling. The expected downturn will likely necessitate a monetary policy response from the Bank of England, which is most likely to cut rates at its meeting in August despite the expected uptick in inflation owing to the sharp currency depreciation. At the same time, while the EU may benefit from the exodus of capital from the UK into the region, it too will likely suffer from reduced trade ties and uncertainty, which could also drag on economic growth, delaying the region’s recovery even further.

While the economic impacts of Brexit will undoubtedly be most pronounced across the pond, the U.S. will not be immune to the fallout. In her semiannual testimony to Congress mid-week, Chair Yellen noted the potential for “significant economic repercussions” of such an outcome that could “usher in a period of uncertainty.” While the Chair didn’t believe such an outcome would trigger a recession in the U.S., she was forthright in saying that Fed officials “just don’t really know what will happen,” but will monitor developments closely, particularly as far as they relate to “domestic economic activity, labor markets, and inflation.”

On the domestic front, Chair Yellen’s testimony warned against focusing too much on a single data point and reinforced the view that despite the weak May employment report, the labor market continues to improve. This view was supported by this week’s initial jobless claims data, which fell down to 259 thousand. The Chair largely stuck to the script of accelerating U.S. growth, and indicated that wage growth is strengthening – corroborating a finding from our recent paper. Ultimately, rising wages and incomes should keep America’s economy supported through resilient consumption and the housing recovery – a view reinforced by this week’s data on existing home sales which rose to an eight-year high of 5.53 million.

The Chair declined to weigh in on when the Fed will next raise rates warning instead, perhaps ominously, that risks abound. In light of the negative implications from a surging greenback and financial volatility on U.S. trade and financial services industry, coupled with the downward pressure on inflation from the former, we expect the Fed will remain on the sidelines through the remainder of the year, and potentially well into 2017 given the downside risks that have surfaced.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 10, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Sparse economic data this week has left market participants dwelling on last Friday’s very weak jobs report.

- Chair Yellen’s speech on Monday did not reiterate the previously used phrase that the FOMC is considering a rate hike ‘in the coming months’, leaving markets confident that the Fed is in no rush to raise rates at this point.

- A slew of domestic data next week, along with the new Fed projections, will provide markets with more to chew on as investors try to get a better read on the broader economic outlook.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

PAYROLLS REPORT CONTINUES REVERBARATE THROUGH MARKETS

The speech was mostly dovish, expressing concern over Friday’s disappointing report and failing to reiterate a previously used phrase that the FOMC is considering a rate hike ‘in the coming months.’ Still, the Fed Chair noted that the economic positives outweigh the negatives and that one can’t put too much emphasis on a single number. She also pointed to a rebound in consumer spending and a falling number of people filing new unemployment insurance claims as positive signs.

These trends were further corroborated this week, assuaging some fears of weakening momentum. Initial claims fell to a mere 264k, beating consensus for a rise to 270k, and marking the fourth consecutive decline off its near-300k recent high in early May. Consumer confidence also held up in June, according to the University of Michigan survey, with the current condition sub-index particularly strong.

Global economic data, also painted a mixed picture. German factory orders declined by a sharp 2.0% in April and unwound most of the prior month’s 2.6% rise. Meanwhile, UK industrial production for April surprised sharply to the upside surging by 2% m/m against expectations for flat growth. The value of total exports also rose by 5.3% m/m, the strongest advance since early-2010, while goods exports climbed by an even stronger 9.1%. Nonetheless, this backward looking data out of the UK did little to sway concerns over the looming UK referendum that is less than two weeks away.

After last week’s strong rally, markets remained largely flat through the end of the week, with the S&P 500 little changed from the previous week’s close, at the time of writing. The downbeat sentiment from the payroll report carried into this week and alongside rising uncertainty surrounding the Brexit vote put a strong bid under very safe bonds, with the 10-year U.S. Treasury yield falling nearly 10 basis points by the end of the week to just 1.65%.

Looking forward to next week’s FOMC meeting, the market appears confident that rates will remain unchanged with the data-dependent Fed unlikely to ignore the recent labor market report, putting them in wait-and-see mode as they seek more evidence in support of a strengthening domestic economy. Whether the sharply reduced pace of hiring is due to a persistent slowdown in the broader economy, a temporary blip in the data, or marks a deceleration to a pace more consistent with fundamentals as cyclical factors wane remains top of mind. Next week’s slew of data, which includes retail sales, housing starts and inflation, should shed some light on this debate. Alongside a new set of projections from the Fed and a press conference with Chair Yellen, this data should allow market participants to further glean how the recovery is progressing, and get a better sense of the likelihood of a summertime rate hike – something we believe remains very likely.

Neil Shankar, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.