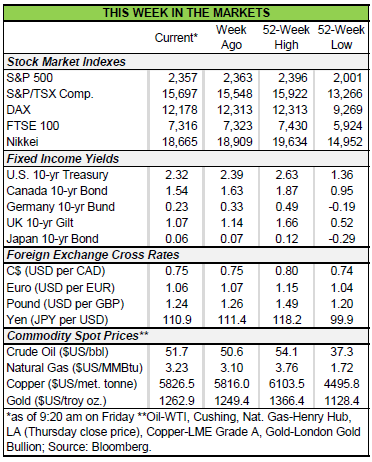

Financial News for the Week of April 7, 2017

HIGHLIGHTS OF THE WEEK

- U.S. economic data disappointed on a variety of fronts this week, but much can be chalked up to weather-related disruptions to the data.

- A paltry 89k payrolls gain was the biggest disappointment, but we are inclined to look past one month’s result and focus on a new cyclical low in unemployment and continued improvement in measures of underemployment. These should also help support a rebound in consumer spending through the remainder of 2017.

- In other news, the Fed is starting to discuss the process of unwinding its holdings of Treasuries and mortgage-backed securities (MBS). It pledged that moves will be well-telegraphed and are likely to start later this year.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

BLAME IT ON THE WEATHER

March payrolls data disappointed expectations, with only 98k new jobs in March, and downward revisions to hiring in January and February. A softer reading was expected after two heady months, but a 200+ reading in the closely watched ADP report earlier in the week had raised hopes. Hiring slowed across both the goods and services sectors, although it was more dramatic in services. Despite the unexpectedly weak payroll print, the household survey showed employment gain of 472k, pushing the unemployment rate down by 0.2 percentage points to 4.5%.

We are inclined to look past one month’s payrolls disappointment. Weather played a role in the March data on two fronts. Unusually warm weather in January and February

The job market should continue to provide a solid foundation for consumer spending this year, with the unemployment rate near pre-recession lows in March, and continued improvement in measures of underemployment.

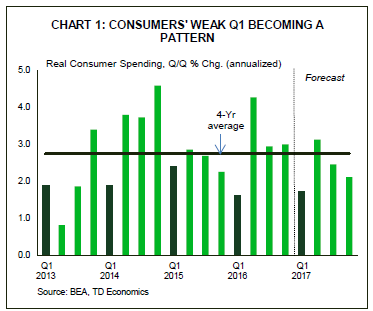

Other data this week confirmed that consumers took a breather once again in Q1, but we expect a rebound in spending in Q2, much like we saw last year. Q1 weakness has become a pattern. Consumer spending growth averaged 2% in Q1 over the past 4 years, while the other three quarters of the year have averaged above 3% (see chart). Eventually, this pattern will be fixed by adjustment to “seasonal adjustment,” but for now we are inclined to discount Q1 weakness.

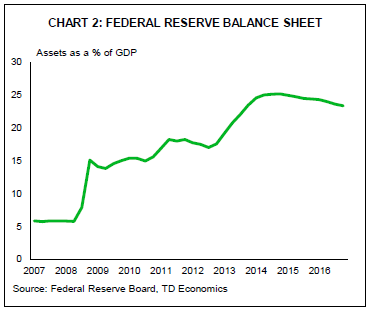

The Fed minutes also provided a peek into the FOMC’s discussion of how and when it will start the process of normalizing its balance sheet, now that normalizing rates is underway. Through the course of its asset purchase program, the Fed accumulated $4.5 trillion in Treasuries and MBS. Since purchases ended, the Fed has been reinvesting the principal payments, keeping its balance sheet steady.

Although things are still at the discussion phase, Fed members already agree on a few things. First, the process of ending reinvestments should be gradual and predictable, and rely primarily on passive phasing out of reinvestments. Second, most members agreed that the change in reinvestment policy should come this year. Third, the FOMC was unanimous that any policy change should be well telegraphed to the public. Our recent forecast calls for the Fed to

Markets are watching closely since removing the Fed from these markets could reduce demand for these securities, lowering prices, and taking yields higher, all else equal. Our latest forecast calls for a continued rise in Treasury yields, and balance sheet normalization is one of the forces expected to take yields higher. The Fed has control of this process. If the Fed doesn’t like the market reaction as it winds down reinvestments, it has the discretion to slow down or stop the pace of adjustment. This helps to mitigate the risks of an undesirable spike in yields.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of March 31, 2017

HIGHLIGHTS OF THE WEEK

- Following the failure to repeal and replace the ACA, market participants questioned the new administration’s ability to move forward with pro-growth policies. As such, major indicators opened lower on Monday, but risk sentiment recovered quickly as the week progressed.

- Positive developments included pending home sales data and an upward revision to fourth quarter GDP growth. Conversely, new data pointed to a deceleration for real consumer spending growth to below 1% (annualized) this quarter. That said, this appears to be only a temporary setback.

- Much of the recent sentiment uptick is related to the anticipated implementation of pro-growth policies. There are certainly risks on this front, suggesting that the Fed’s ‘wait and see’ approach is the right one as far as baking in any potential impact on the economy.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

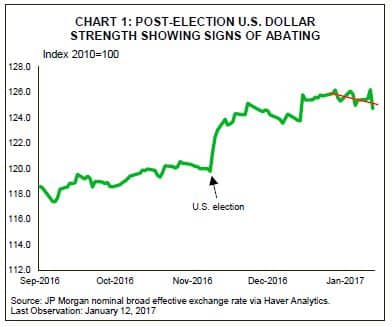

MARKETS OVERLOOKING POLITICAL SETBACKS

The failure of the bill to repeal and replace the ACA last Friday set the tone for investors at the start of this week. Market participants questioned the new administration’s ability to build consensus and move forward pro-growth policies, with major U.S. stock indices along with the greenback and long-term government rates opening lower on Monday. But, risk sentiment recovered as the week progressed, with most aforementioned indicators recovering beyond last Friday’s levels (Chart 1). This was despite the triggering of Article 50 – the official initiation of the long divorce proceedings between the U.K. and E.U. – which has been largely anticipated. The recovery was partly related to the quick pivot by the U.S. administration

The week was relatively light as far as first-tier economic data goes. But secondary indicators, such as pending home sales looked promising, surging in February and bringing the index level to a 10-month high. Unseasonably clement weather was part of the story, with some giveback likely in March. Nonetheless, this is a welcome development as it reinforces the notion that despite rising interest rates, housing continues to contribute to economic activity given solid labor market fundamentals.

Another positive development was the upward revision to fourth quarter GDP growth. The economy expanded by 2.1% (previously reported as 1.9%) due to more strength in consumer spending – upgraded by half-point to 3.5%. After that knock-out quarter, consumers tightened their purse strings at the start of this year. Data out this morning showed that real spending fell for a second consecutive month in February, with weather and delayed tax rebates likely playing a part. As such, real consumer spending looks set to advance by less than 1% in the first quarter of 2017. Still, this is likely to be only a temporary setback. Spending should bounce back in the second quarter, thanks to strong consumer confidence and accelerating income growth, restoring economic growth to a well-above trend rate.

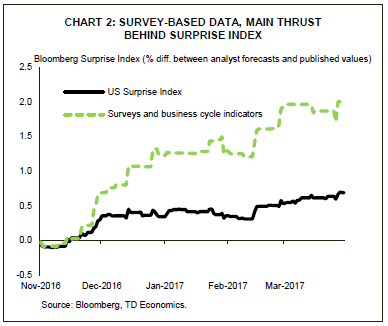

While the economy remains on solid footing there has been an increasing divergence between survey and sentiment metrics (soft data) and harder indicators of economic activity (i.e. sales and incomes). This narrative can be illustrated by Bloomberg’s surprise index where hard data has come in largely as expected while survey-based data has been the main thrust behind an improvement in the measure (Chart 2).

Ultimately, the strength of the economy will depend on which way the convergence will occur. Much of the sentiment uptick is related to the anticipated implementation of pro-growth policies. However, doubts as to the probability of success could quickly manifest into weaker readings. There are certainly risks on this front. For starters, tax reform is complex, and while lawmakers have some leeway, delays could put a dent in sentiment. Additionally, the failure to repeal and replace the ACA leaves the budget plan billions short, increasing the likelihood of scaled-down versions of other parts of the agenda. All told, it would appear the Fed’s ‘wait and see’ approach is the right one as far as baking in any potential impact on the economy, with the anticipated three hike per year pace seemingly appropriate for the time being.

Admir Kolaj, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

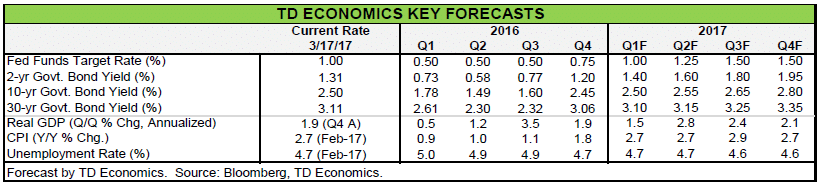

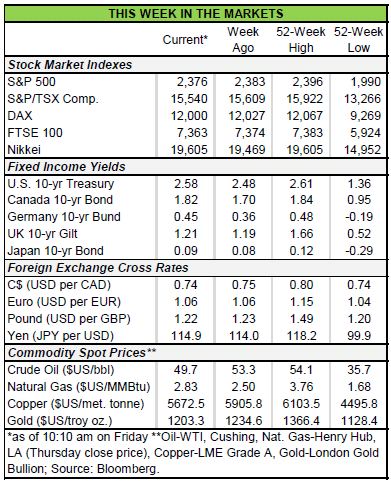

Financial News for the Week of March 17, 2017

HIGHLIGHTS OF THE WEEK

- The Fed carried out its well-telegraphed rate hike this week. Despite the Fed’s hawkish messaging in advance of the decision, its expectations for rate increases were unchanged, leading bond yields to dip.

- The Fed edged up its economic forecast for 2018, as did TD Economics in our latest forecast, released this week.

- Overseas, one populist threat to the Eurozone was vanquished this week as the populist right-wing party lost the Dutch election. However, the UK is days away from triggering the two-year Brexit negotiation process with the EU, so the risk of euro-driven market volatility remains.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

THE FED TAKES ANOTHER STEP ON THE RATE HIKE TIGHTROPE

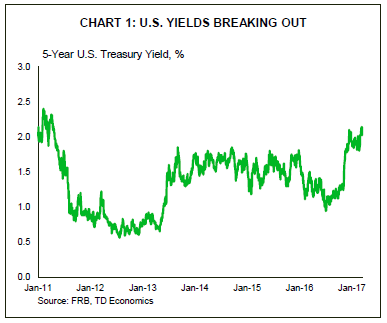

Markets were cautiously optimistic this week as the Fed carried out its well-telegraphed rate hike, and one populist threat to the euro zone was vanquished in the Dutch election. The Fed hiked the funds rate 25 basis points, to a range between 0.75% and 1.0%. Bonds rallied in the wake of the decision, since the hawkish rhetoric leading up to the decision was not born out in a more aggressive pace of rate hikes in the Fed’s “dot” plot. The Fed continues to expect to raise rates three times in total in 2017, unchanged from its December forecast. Even with a dip downwards in yields this week, the 5-Year Treasury yield remains close to a six-year high (see Chart).

During the press conference, Yellen characterized the economy as “progressing nicely”, and that the Fed views three hikes per year as a “gradual” pace in the current environment. While the median interest rate projection remained unchanged, the number of dots at the median rose (from six to nine). The Fed’s economic projections told a similar story, edging up by 0.1 percentage point its outlook for core inflation in 2017 and its outlook for economic growth in 2018. In other words, FOMC members are a bit more confident, but no more hawkish, than they were in December.

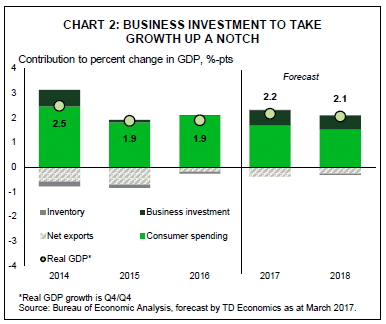

The Fed was not alone in nudging up its forecast. In our latest economic forecast released this week, we also bumped up our forecast for growth in 2018. The upgrade is largely owing to a more optimistic forecast for domestic demand, and business investment in particular. Measures of business sentiment have largely held on to their post-election jumps, and we expect that optimism will translate into increased spending over the next two years. Particularly now that the weakness in corporate profits appears to have turned around, and the worst is over in the oil patch.

As always, there are upside and downside risks to the outlook. The most notable upside risk stems from fiscal policy. We continue to believe it is too early to include any potential boost from the kinds of tax cuts or infrastructure spending that was promised during the campaign. As evidenced by the current debate on healthcare reform, it is going to take time for Republican members of Congress and the White House to reach an acceptable compromise on these key policy priorities. Therefore, we expect any fiscal boost to be a factor in the 2018 outlook and beyond, not this year.

Like the Fed, we also expect a gradual pace of rate hikes this year. Downside risks to the forecast have not entirely vanished. Concerns stemming from political uncertainty in Europe did clear one hurdle this week with the Dutch election result. But, France’s Presidential elections loom (on April 23rd and May 7), and the UK is on the cusp of triggering two years of Brexit negotiations with the EU. The potential for euro-driven market volatility to disturb markets’ current placid optimism is real. And on this side of the pond, the risk that the Trump administration moves from rhetoric to real protectionist measures on trade also looms.

Taking a step back to the here and now, the U.S. economy is doing well. The Fed must now walk a tightrope balancing the need to remove monetary stimulus against the risk of taking rates too high, which would dampen domestic growth too much or trigger risks abroad.

Leslie Preston, SeniorEconomist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

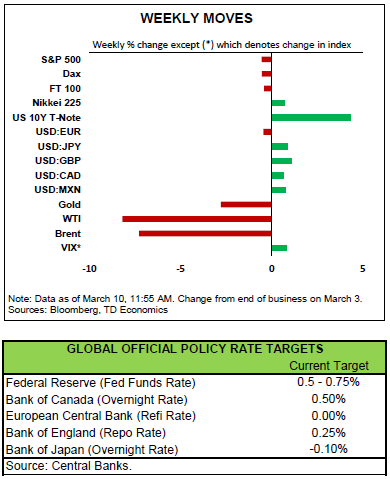

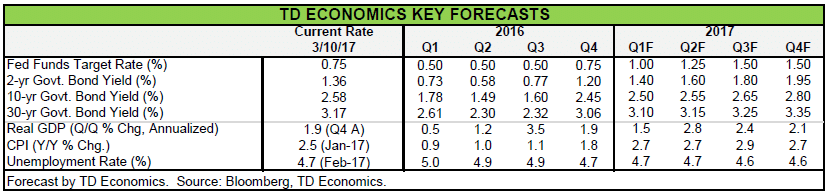

Financial News for the Week of March 10, 2017

HIGHLIGHTS OF THE WEEK

- Markets continued to price in lofty odds for a Fed hike next week, putting further upward pressure on the 2 year treasury yield – which remained near a nine-year high. The U.S. dollar also remained relatively well supported up 0.2% on the week. Meanwhile, equity markets took somewhat of a breather, but the S&P500 only ended the week 0.5% lower.

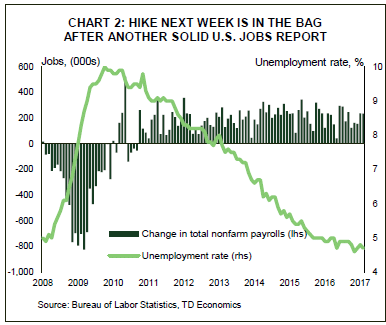

- There were few domestic data to sift through this week, until today’s highly-anticipated jobs report. The labor market added 235k jobs on the month, with some upward revisions to the prior month. Alongside a decline in the jobless rate, these developments have further cemented the case for a rate hike next week.

- With a March hike highly-expected at this point, markets are turning attention to what is in pipeline from the Fed. Three hikes this year, alongside global central banks that remain in highly-accommodative mode should continue to support the U.S. dollar and act as a weight on economic growth. Nonetheless, we expect economic growth to remain resilient supported by continued domestic strength.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

MARCH FED HIKE ALMOST CERTAIN ON STRONG JOBS REPORT

Following last week’s relatively hawkish comments from a number of FOMC members, market participants were waiting to see if domestic data out this week would corroborate the notion that the economy is strong enough to withstand a rate hike. Markets continued to price in a hike this week, with the 2 year treasury yield continuing to face upward pressure as a result, moving up another 7bps by the end of it, at the time of writing. The more aggressive take on Fed policy has provided some support to the dollar, but the strength was offset by less-dovish rhetoric from the ECB, with the DXY just 0.2% higher at the end of the week.

Globally, the ECB’s monetary policy decision on Thursday was in focus. While Draghi hinted at a scenario where the ECB could hike rates while QE is ongoing, it is likely that the central bank will still remain on hold for quite some time. In the context of a Fed that is moving toward a faster tightening cycle when compared to the one and done pace over the last two years, dollar strength will continue to remain an ongoing theme exacerbated by this apparent divergence in monetary policy.

Meanwhile, equity markets seemed to take somewhat of a breather. The S&P 500 closed down on three of the five trading sessions, but ended the week only 0.5% lower, at the time of writing. Higher interest rates and some strength in the USD, was partly to blame, as was the slide in oil prices. Moreover, some of the sell-off was likely related to profit taking as investors cashed in after a long winning streak.

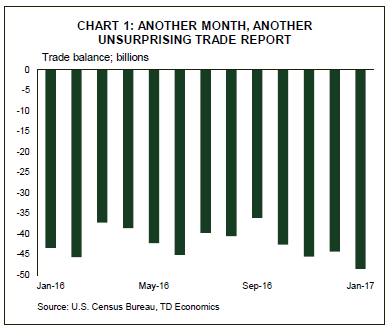

Apart from today’s employment report, there was a scarcity of first-tier domestic data this week. Tuesday’s January international trade report (Chart 1) was concerning, but the increase seen in the trade deficit to $48.5 billion was largely expected and came on the back of a strong rise in imports. It has been widely accepted that drag from net-trade will likely continue as a strengthening U.S. dollar makes imports relatively more affordable and exports more expensive. So, while disappointing given that it places a drag on overall economic growth, it only reinforced the notion that the U.S. consumer remains in good shape.

Still, while the magnitude of the positive surprise in ADP employment, which reported in the middle of the week, provided markets with a bit of a teaser, it was Friday’s payrolls report that stole the show (Chart 2). Non-farm payrolls rose by 235k in February, or well ahead of the 200k expected by the street. Upward revisions also added 9k positions and the unemployment rate ticked down by 0.1% to 4.7%. At this point these developments have cemented the case for a rate hike next week. Wage growth disappointed somewhat, but given the upside revision, accelerated nonetheless from 2.6% to 2.8% in February.

Despite the stronger dollar acting as a weight, we expect economic growth will remain resilient. Irrespective of fiscal stimulus, the economy appears to be at a point where it can handle a few hikes per year, with much of the strength hinging on the strength of the U.S. consumer. This is particularly the case if the data continues to come in robust, with wage and income gains boosting disposable incomes. Ultimately, we expect the Fed to raise rates next week, with two more hikes likely later this year should the economic outlook evolve as expected.

Neil Shankar, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

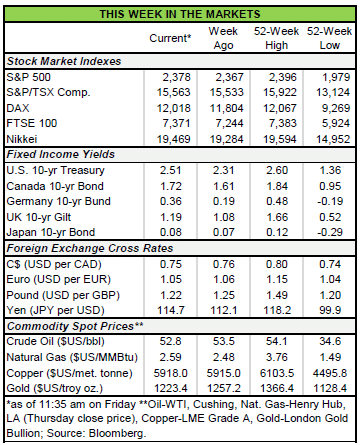

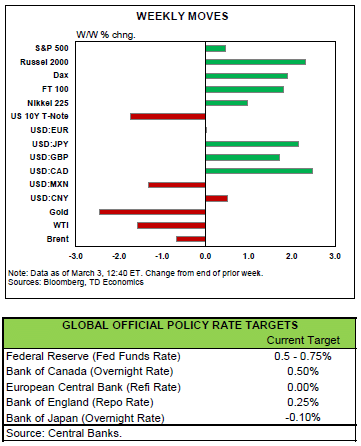

Financial News for the Week of March 3, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- It was an exciting week in markets this week, with plenty of domestic and international first-tier data, central bank communication, and the inaugural presidential address to Congress.

- International data has continued to paint a relatively bright picture of the world economy with inflation picking up in the Eurozone, Japan, and the U.K. The positive sentiment was further buoyed by strong PMI data across the globe, suggestive of a strong start to 2017.

- U.S. data was even more encouraging. Apart from some weakness in real spending and construction in January, which came on the back of a strong fourth-quarter, data on from purchasing managers pointed to building strength, with solid momentum in early-2017 also exhibited by regional business surveys, price metrics, and labor market indicators.

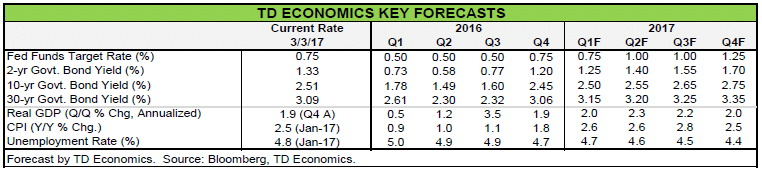

- In light of the strong data flow and increasingly hawkish rhetoric out of the Fed, we believe the FOMC will likely raise rates at its next meeting in mid-March, barring any downside surprises, with markets increasingly turning their focus from “when” to “how quickly” any potential hikes may come.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

Fed Primes Markets for March Hike, Aiming for Hat-Trick in 2017

It was an exciting week in markets this week. Alongside a much awaited tech IPO, there were plenty of first-tier data (both domestic and international), central bank speeches, and the inaugural presidential address to Congress. International data came in broadly constructive, while U.S. data came in even more robust. Alongside indications of rapid deregulation by the executive branch, and relatively hawkish remarks from FOMC members across the spectrum, this placed upward pressure on yields and pushed the odds of the March hike from just 1/3rd last week to near-certainty as of the time of writing. Markets now expect between 50 and 75 basis points of tightening this year. The more aggressive take on Fed policy has seen the U.S. dollar rally by nearly 1% across the common-traded basket. The higher dollar was not helpful to oil prices, which were already under pressure from building U.S. inventories. Still, sentiment was running high since mid-week, with U.S. equity indices setting new records and the Dow surging north of 21,000.

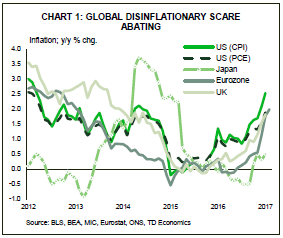

International data has continued to paint a relatively bright picture of the world economy. Inflation picked-up to a four-year high in Japan and has been accelerating in Europe and the U.K. (see Chart 1). While much of the headline print is related to rising oil prices, it nonetheless has pushed deflationary fears from investors’ minds. The price data was not alone in boosting sentiment, with the purchasing manager indices across the main global economies showing signs of health. Eurozone PMIs held near just north of the mid-50s mark, suggesting GDP growth of around 2% in the common-currency area, with the U.K. PMI holding near that mark also. Chinese PMIs, while lower, were healthier

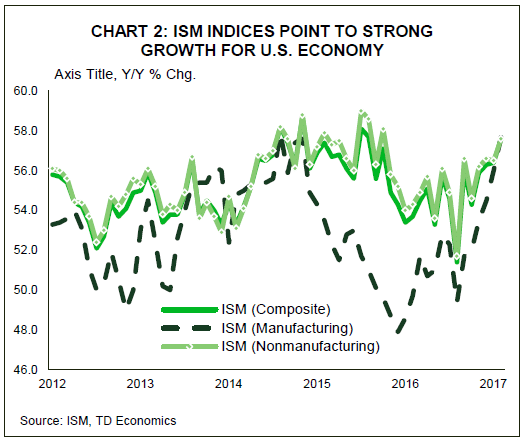

U.S. data was arguably even more constructive. While real consumption and construction disappointed in January, the monthly print at the start of the year, when seasonal factors are the highest, is notoriously volatile and has been misleading in previous years. Moreover, it comes atop of a strongly revised PCE print in the fourth quarter of 2016 – when consumers increased spending by a healthy 3% according to the second estimate of GDP. Other indicators, including ISM indices from both the manufacturing and nonmanufacturing sectors suggest the economy is progressing at a very healthy pace. Such sentiment is corroborated

by regional business surveys, durable goods orders data, and price metrics – with core PCE inflation rising by a decade-high 0.3% on the month.

While core PCE inflation – the Fed’s favored measure of price pressures – remains shy of the FOMC’s target at just 1.7% on a year-on-year basis, there is little question that the movement up has been swift. Given the wage pressures that have manifested in recent months, and are likely to continue to rise given the ever tightening labor market (initial claims fell to a 44-year low) and the lagged spillover from oil prices, it is likely that the measure will approach the 2% target as the year progresses. With this in mind, a more favorable international backdrop, and markets that are effectively giving the Fed a clear opportunity to hike in March, we believe the FOMC will take the opportunity – particularly given its proclivity to move earlier, but more gradually.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of February 24, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The outlook for economic growth got a bit rosier this week with the release of the preliminary February survey results of purchasing managers that showed economic momentum continuing to build at the start of 2017.

- The data flow this week was light for the U.S., but existing home sales for January confirmed that the U.S. housing market remains resilient despite the uptick in mortgage rates. Still, the outsized strength in January is unlikely to be maintained, as a number of temporary factors come off in upcoming months.

- Little news in the FOMC minutes other than a confirmation that the U.S. economy was evolving in line with expectations. Overall, the FOMC remains confident that the slow and steady absorption of economic slack, and the corresponding progress of inflation toward its 2% target, warrants a gradual pace of tightening of monetary policy.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

BUILD IT AND THEY WILL COME

This week we got further signs that global economic growth continued to firm at the start of 2017. Despite elevated policy uncertainty, financial market volatility remains low, but it’s unclear if this is a sign of market certainty or complacency about the economic outlook.

Indeed, the global outlook is looking a little rosier than a month ago. Preliminary surveys of manufacturers for February point to continued strong expansion in advanced economies despite elevated political uncertainty from upcoming European elections.

One thing markets have taken notice of is the gains Marine Le Pen has made in the polls. If she were to become President of France, the populist candidate plans to call a referendum on France remaining in the EU if she is unable to renegotiate its terms of membership. The threat of ‘Frexit’ caused spreads between French (and other euro area) bonds with German bunds to widen this week.

The data flow this week was light, but supported our view of U.S. economy growing above its trend pace at the start of 2017. Along with the supportive preliminary manufacturing survey data, January existing home sales rose to the highest level in a decade in January – despite a 70 basis point rise in mortgage rates since last September (Chart 1). Strong existing home sales are further confirmation of the progress the U.S. housing market has made since the crash over a decade ago. Nonetheless, this elevated level of activity is unlikely to be maintained in upcoming months for a number of reasons.

First, some of the activity likely reflects a pulling-forward in contract signings in order to lock-in low mortgage rates. Secondly, unusually warm weather also helped pull forward some activity from the spring market. Lastly, until more sellers put their homes on the market, the low inventory of homes will weigh on sales volumes and put upward pressure on prices (Chart 2). While several years of home price growth

The strong performance of the U.S. economy to start the year remains broadly consistent with the Fed’s economic projections, as was noted in the minutes released this week from the first FOMC meeting of the year. The Fed also discussed the uncertainty about the economic impact from the proposed changes in fiscal policy by the new administration, changes that will likely have material implications to the Fed’s economic projections and the pace of policy normalization. Overall, the FOMC remains confident that the slow and steady absorption of economic slack, and the corresponding progress of underlying inflation toward its 2% target, warrants a gradual pace of tightening of monetary policy. Our view is for the next move up the fed funds rate to take place in June, but we cannot rule out a March or May rate hike if the data flow surprises to the upside.

Fotios Raptis, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of February 17, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Despite heightened political uncertainty it was another good week in equity markets, with the three U.S. benchmarks reaching peaks mid-week before retracing somewhat ahead of the weekend.

- U.S. data came in well above expectations with survey indicators from the NFIB, as well as the New York and Philly Federal Reserve Banks rising to multi-year highs. The optimism was also prevalent across harder data, with retail sales as well as consumer and producer inflation metrics surprising to the upside.

- Together with the stronger data, Chair Yellen’s testimony where she indicated it “unwise” to wait too long to remove accommodation, boosted the odds of a March hike. Nevertheless, we continue to anticipate the Fed will wait until mid-year to raise rates next.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

ANIMAL SPIRITS CONTINUE TO TRUMP ANXIETY

Investors continued to be enamored by the potential for growth-inducing policies of President Trump this Valentine’s Day week despite relatively few details. While politics continued to drive headlines, financial markets were more focused on healthy earnings and robust economic data. The three main U.S. equity indices hit record highs on Wednesday, before paring back some gains through this morning. The sell-off in the bond market, which saw the U.S. 10-year Treasury rise near 2.5% by mid-week as Janet Yellen testified to Congress, also reversed course recently, with the

benchmark falling to 2.4% by this morning. Oil remained largely range bound, as the support from realized cuts by OPEC were offset by rapidly rising inventories in the U.S. where production has been recovering in recent months.

News across the Atlantic was largely lackluster this week. The economy of the Eurozone area grew by 1.6% in the final quarter of last year, missing expectations

Political uncertainty remained on the back-burner in the U.S. as investors focused on healthy earnings growth with U.S. corporate profits looking to grow by over 6% after three quarters of declines. Moreover, the animal spirits that have been driving stock markets since the election appear to also be showing up in the economic data.

Much of the positive sentime

The reduction in slack also appears to be manifesting in higher prices. Both the core CPI and PPI measures surpassed expectations, rising by 0.3% and 0.4% in January, respectively, with the headline consumer inflation measure accelerating to 2.5% (see Chart 2). The hotter-than-expected data is adding pressure on the Fed to not fall behind the curve. In her testimony to Congress this week Chair Yellen highlighted that waiting too long to remove accommodation would be “unwise,” suggesting that the Fed could raise rates in the near-future. While a March or May hike is not off the table should the data continue to come in above expectations, we remain of the view that the Fed will wait until June to raise rates.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of February 10, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- After last week’s start-of-month data dump and the prior week’s executive order deluge, this week has

been fairly quiet for U.S. investors. - International trade data was the only top-tier release, highlighting an improvement in the trade deficit and

suggesting some upward revision to fourth quarter GDP. Also constructive was the sustained decline in

initial jobless claims, which beat expectations and fell to 234k last week. - Rather than the data, the markets were more interested in what was being said by policymakers about

the U.S. economy, cheering the mere mention of what was touted by the president as a ‘phenomenal’ tax

plan. Plenty of Fed-speak also kept market participants looking for clues for the next Fed hike, but one is

unlikely until at least mid-year.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

QUIET DATA CALENDAR A WELCOME CHANGE

After last week’s start-of-month data dump and the prior week’s executive order deluge, this week has been fairly quiet for U.S. investors. Markets remained fairly upbeat, on continuing hopes of corporate tax reform and relatively positive earnings, with all three major indices setting records once again on Friday morning (Chart 1). The U.S. dollar also got a modest boost, with the DXY index 1.1% higher on the week, at the time of writing.

International trade data for December was the sole top tier U.S. release leaving participants with little to chew on by way of economic data. The trade deficit narrowed to $44.3 billion from $45.7 billion in the prior month (Chart 2), beating economists’ expectations for a more modest pullback (to $45.0 billion). Exports bounced back aft

The second-tier data was somewhat more inspiring. For one, initial jobless claims fell substantially, going against market expectations for a modest increase. The headline number fell to 234k for the week ending February 4th while the 4-week moving average declined to 244k, the lowest level since 1973. The job openings and labor turnover survey for December also painted a picture of an increasingly tight labor market, with job openings hovering around the 5.5 million mark, while the quits rate slipped only slightly to 2.0%, but remained near the cycle-high level of 2.2%.

Globally, economic data was more mixed. German industrial production hit the brakes in December, down 3% m/m. However, factory orders rebounded, up 5.2% on the month, providing some comfort that industrial production will bounce back in January. Less encouraging was the softer reading of the composite purchasing managers’ index in China which fell to 52.2 in January. While this still represents growth, it signals a slower pace at the beg

Still, data these days often tends to play second fiddle, with policy discussion about the U.S. economy taking center stage, particularly how any of these may impact the outlook for monetary and fiscal policy. President Trump suggested recently that he will within the next two weeks announce a ‘phenomenal’ tax plan with markets already cheering the mere mention of this initiative (see Chart 1 again).

In the follow-up to the Fed’s meeting last week, the Fed’s speaking circuit was out in full force. Philadelphia Fed President Harker kicked things off, alluding to a rate increase as early as March. However, his hawkish views were offset by the Minneapolis Fed President Kashkari, who cited the slow improvement in core inflation and limited cost pressures stemming from the labor market as reasons to remain patient. Evans (Chicago) and Bullard (St. Louis) also reiterated the dovish stance later on in the week, both citing concerns around the lack of inflationary pressures. Overall, none of this changes our take on the Fed’s next move, with our baseline view seeing the Fed raise rates twice this year, with the first coming around the mid-year mark.

Neil Shankar, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

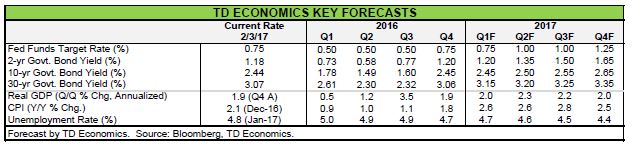

Financial News for the Week of February 03, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Political events and communiqués from the new administration, continued to dominate the headlines –

taking some of the attention away from what was a week of upbeat economic data. - The FOMC held rates steady this week, but remained upbeat about the economy – pointing to continued

improvement in the labor market. This narrative was corroborated by this morning’s employment report,

which blew expectations of 180K out of the water as payrolls rose by 227K. - In the near term, we expect the Fed to remain on the sidelines in order to observe how the economy behaves

under heightened policy uncertainty. If the economic expansion continues at the current moderate

but above trend pace of growth, we expect the Fed to hike around the mid-year mark. By that point some

of the missing pieces from the policy puzzle should have fallen into place.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

UPBEAT ECONOMIC DATA CORROBORATES FED NARRATIVE

Political events and communiqués from the new administration, whether formal or informal, continued to dominate the headlines this week – taking some of the attention away from the upbeat economic data. Equity markets eased off slightly from last week’s all-time high, while long-term treasury yields are expected to end the week roughly unchanged. The euphoric post-election momentum appears to have finally plateaued as both equity and fixed income markets remain range-bound near recent highs.

The lack of policy detail in key areas such as tax reform, infrastructure spending and trade is likely to have featured in the FOMC’s decision to hold the federal funds rate steady this week – a decision that surprised no one. The committee remained upbeat on the outlook, noting that the economy “continued to expand at a moderate pace”, while making reference to solid job gains and an unemployment rate that remains “near its recent low”.

This narrative was corroborated by January’s employment report, which blew expectations of 180K out of the water as payrolls rose by 227K (Chart 1). Gains were fairly widespread in the private services sector, while on the goods-producing side they were concentrated in construction (+36K) – a highly seasonal sector and thus one where we could see some reversal in the months ahead. The unemployment rate ticked up slightly to 4.8%, but for a good reason, as the continued improvement in labor market conditions is drawing in more workers from the sidelines - evidenced by the 0.2 ppts move up in the participation rate on the month to 62.9%. While this development is welcome and largely anticipated, taken together with the deceleration in wage growth to 2.5% y/y from 2.8% in the month prior, it is likely to hearten Fed doves to argue for continued patience.

Earlier in the week, personal income and spending data for December was also positive, providing a solid handoff for consumer spending growth heading into 2017. Incomes rose 0.3% m/m and spending rose 0.5% m/m. Consumer spending drove growth in the fourth quarter and we expect this momentum to carry into the first quarter of 2017. Manufacturing activity remained solid, as

Overall, the US economy continues to exhibit signs of improvement. In the near term, we expect the Fed to remain on the sidelines in order to observe how the economy behaves under heightened policy uncertainty. If the economic expansion continues at the current moderate but above trend pace of growth, we expect the Fed to hike around the midyear mark. By that point some of the missing pieces from the policy puzzle should have fallen into place, such as infrastructure spending plans. Yet, it looks like the highlyanticipated tax reform bill will not be written until summer. That, coupled with the slow nature of the political process in general, has the potential to lead to some pullback in consumer, business, and market sentiment. In the meantime, markets will continue to hang on every word from the new administration.

Admir Kolaj, Economic Analyst

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 13, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Financial markets this week were captivated by policy-related tweets and a mid-week press conference by President-elect Donald Trump that, while entertaining, proved to be short on policy detail.

- Retail trade data this week was broadly in line with market expectations, although the monthly advance was driven by increased purchases of autos and gasoline. Overall, the data remains consistent with our view that consumer spending will continue to support economic activity in 2017.

- Promises from policymakers are nothing new, and are an important driver of consumer and business expectations. However, the post-election euphoria may be premature. We remain hopeful that more policy certainty will materialize after the inauguration next week.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

RISING OPTIMISM BUT FEW DETAILS

Financial markets this week had a fair bit of information to digest, mainly in the form of verbal communication from policymakers. Despite what was deemed a disappointing press conference by President-elect Trump this week given the lack of policy detail, equity markets are expected to end up on the week, while Treasuries round-tripped and should end the week roughly unchanged. The main story in financial markets this week was the volatility in the U.S. dollar index, which could mark the third consecutive week of declines.

The key economic data print this week was the December retail sales figure that showed a rise in consumer spending driven largely by autos and gasoline. While broadly in line with expectations, sales ex-autos and gasoline were virtually unchanged from the previous month. Overall, the data is consistent with our narrative that tightening labor markets and past gains in real income growth should support consumer spending in 2017.

Other data failed to garner as much attention this week. November data from the job openings and labor turnover survey didn’t affect the narrative of a recovering labor market. Somewhat more interesting was price data from surveys of producers and international trade, which showed a pick-up in price growth over the last twelve months, driven in large part by higher energy prices.

Given the lack of significant surprise in domestic economic data, markets focused their attention on what was being said by policymakers about the U.S. economy, particular concerning the outlook for monetary and fiscal policy. While market participants have long appreciated the power of central bankers to move financial markets with a few choice words, the dramatic market moves in reaction to recent policy proposals by elected officials has been noteworthy. Recent examples include the market’s swift reaction to tweets by President-elect Trump, and the market

volatility observed during his press conference this week.

The general optimism in the nation’s equity markets to the election result have been echoed in surveys of business and consumer confidence. This week, the NFIB optimism index surged, ending 2016 with the largest quarterly increase since 1980. The University of Michigan’s monthly survey of consumer sentiment, while pulling back ever so slightly in January, remained similarly upbeat, well above its pre-election level and at a rate that historically would suggest

some upside to the outlook for consumer spending.

While stories have always mattered, and economists have long emphasized the importance of expectations about the future, there is a risk is that at least some of this elation is premature. With limited details on the scope of policy changes or their economic effectiveness, there is a chance that the fiscal policy of the new administration will fail to achieve the economic outcomes promised. In the short-term the rise in confidence (or animal spirits) is a positive for the outlook, but any disappointment could lead expectations to pull back.

Hopefully some of this policy uncertainty will begin to fade after president-elect Trump is confirmed as President at next Friday’s inauguration. Still, if the events of the past week are any guide, expect financial market volatility to persist.

Fotios Raptis, Senior Economic

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.