Financial News for the Week of December 23, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investor sentiment remained upbeat this week, with U.S. equities looking to end the week on a positive note for the seventh consecutive week despite some profit taking.

- Domestic data was relatively robust this week. Economic growth was revised up to a robust 3.5% during the third quarter, with the economy looking to expand by close to 2% during the last quarter of 2016. Sales of existing home rose to a nine-year high in November, while personal income remained flat last month.

- Our outlook for 2017 calls for growth of just over 2%. This should be enough for the economy to eat-up any remaining slack, with the ensuing wage pressures helping lift inflation closer to the Fed’s 2% target.s aftermath.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

ECONOMY TO ENTER 2017 ON A SOLID FOOTING

It has been quite an eventful year to say the least. The Dow finished last year at 17,500, after taking in stride the first Fed hike in nine years. It then proceeded to plunge below 16,000 by mid-January as anxiety over the Chinese economy mounted with worries over the global economy pushing oil down below $30 in February. And just as markets found their footing during springtime, the Brexit referendum stunned investors once again. By late summer, over $13 trillion in government debt was trading at negative rates. By early autumn, investors had tacitly accepted the mediocrity of global growth as a status quo and were increasingly writing off inflation as a phenomenon of years’ past, leaving bonds in high demand and equities somewhat directionless. But,

As we look towards the New Year we believe there are a few key themes that should increasingly play out during 2017. Overall, we expect 2017 to be a year which is characterized by: increased emphasis on fiscal policy, an inflection point for interest rates, continued U.S. dollar strength, firmer commodity prices, and plenty of volatility to go around – both internationally and domestically.

What is certain is that Donald Trump will inherit an economy that’s doing quite well. Data released this week indicated that the U.S. economy grew by 3.5% during the third quarter and is on pace to expand 2% in the fourth. However, this strong pace of expansion is unlikely to be maintained through

Overall, while we believe the higher dollar and interest rates will take some steam out of U.S. economic growth next year, we expect the economic expansion to remain resilient at just above 2%. This will enable the economy to continue eating up whatever slack remains, with the ensuing wage pressure helping lift inflation closer to the Fed’s 2% target. Given the monetary tightening that has already taken place, we expect the Fed to proceed cautiously going forward. While our projections for one hike are well shy of the market expectations and the Fed’s own ‘dots’ which suggest three hikes, we’d like to remind the readers that those same dots telegraphed precisely four hikes for 2016 – and we all know how well that projection turned out.

Michael Dolega, Senior Economic

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

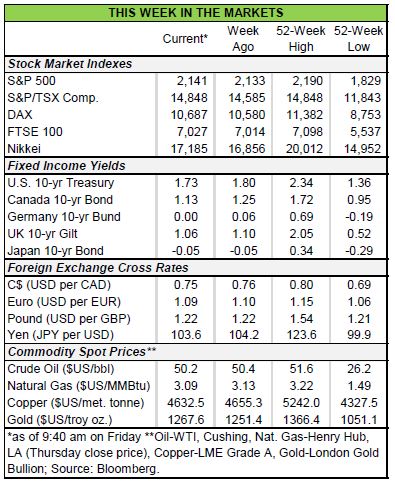

Financial News for the Week of December 16, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Despite delivering a widely anticipated quarter-point rate hike this week, the Fed’s more hawkish outlook for the pace of future rate hikes saw Treasury yields jolt higher.

- In our updated forecast we refrain from jumping on the fiscal stimulus bandwagon, given that significant policy shifts remain speculative at this point.

- In the meantime, higher bond yields will filter through to higher borrowing rates for consumers and businesses, and will ultimately diminish the need for Fed hikes. As such, our expectation for a very modest

pace of Fed hikes remained unchanged in our forecast.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

WHAT FISCAL POLICY GIVES, MONETARY POLICY MAKE TAKE AWAY

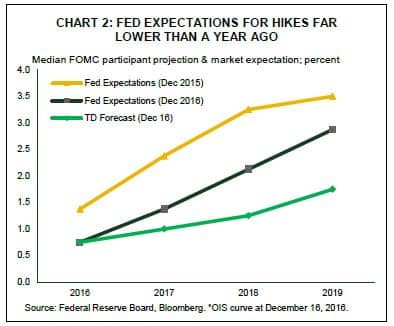

Despite delivering a universally expected quarter-point rate hike this week, the Fed still managed to jolt markets. Its slightly more hawkish rate outlook, with the median ‘dot’ now indicating one additional rate hike during 2017 for a total of three, took markets by surprise with the U.S. 10-Year bond yield surging 15 basis points since. Yellen characterized the shift as “modest”, and indicated it reflected some of the participants incorporating fiscal stimulus into their projections. She also made clear that with the economy very close to full employment, what fiscal policy gives in stimulus, monetary policy is likely to take away with faster rate hikes.

Clearly some FOMC members agree with markets’ assessment that fiscal policy is about to get more stimulative under a Trump administration. In our new Quarterly Economic Forecast, we refrained from jumping on the ‘optimism bandwagon’ that has been driving markets since the election. While we believe that many aspects of Trump’s platform could raise inflationary pressures – including restricted immigration and higher import tariffs – a significant fiscal stimulus package is far from a done deal.

We acknowledge that the Republican sweep in Washington is likely to yield significant policy changes, in particular on tax reform, deregulation and the Affordable Care Act. But, it is not at all certain how large a stimulus is in the offing. Many Congressional Republicans are determined to rein in the deficit, which already sits at approximately 3% of GDP, and will require new taxes or spending cuts to balance. On the campaign trail, Trump indicated that he would find savings to offset his tax cuts. He proposed to cut non-defense discretionary spending by 1% every year – the so-called “penny plan”. After ten years this would amount to a 25% spending cut in absolute terms versus current projected levels, and would produce a notable economic drag.

Reforms on the corporate side, including regulatory changes and tax cuts, could help to improve the climate for business investment, which hasn’t contributed much to growth over the 2015-16 period (Chart 1). But we would need to get more clarity on government policy initiatives before we adopt formal changes to our forecast.

In the meantime, higher Treasury yields will surely trickle through to borrowing rates for consumers and businesses. Combined with the sizeable appreciation of the U.S. dollar, this represents a tightening in financial conditions. This will likely weigh on the pace of investment in housing over the next couple of years , and a stronger currency is likely to lead to larger economic drag from trade.

Those impacts illustrate how, to a large extent, bond markets are doing the Fed’s tightening work for it. Higher rates farther out the curve lower the need for tighter policy going forward, rather than increase it. We suspect that this dynamic will contain the Fed to one hike in each of 2017 and 2018 – below others’ expectations (Chart 2). It is also worth noting that at this time last year the Fed thought it would be raising rates four times, not once, in 2016. All told, the high degree of uncertainty about fiscal policy and the reality that its impact on the economy is likely to be quite lagged suggests there is, once again, plenty of room for disappointment as far as future pace of Fed hikes is concerned.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 9, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Domestic data took a backseat to this week’s developments out of Europe with major political developments in Italy early in the week.

- On Thursday, the ECB revealed a reduction to its monthly asset purchases beginning in April of next year. The move was applauded by markets and seen as a dovish taper with ECB President Mario Draghi making it clear that this was a one-time adjustment and not a tapering down to zero.

- Data out of the U.S. did less to move markets, but continued to paint a picture of a solid domestic economy. With the much anticipated December FOMC meeting just around the corner, we are almost certain that the Fed will continue along its “gradual” hiking path come next Wednesday.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

INTERNATIONAL DEVELOPMENTS TAKE CENTER STAGE

The domestic data calendar took a backseat to this week’s developments out of Europe. To kick things off, markets were taking the ‘no’ outcome of Sunday’s Italian referendum quite constructively. This was despite the political risk attached to PM Renzi’s forthcoming resignation and the perception of a ‘no’ vote as supportive of Beppe Grillo’s Five Star Movement party. With a vast majority of Italians in support of remaining in the EU and retaining the euro, the fear that a ‘no’ vote would eventually lead to a UK-style exit from the EU was likely overstated.

Political news out of Austria provided markets with something else to cheer about. Presidential elections declared pro-EU candidate, Alexander Van der Bellen, as the winner, putting fears to rest that another forthcoming referendum on the EU, as campaigned upon by the far right Freedom Party, was on its way. To top these developments off, an unexpected resignation by New Zealand’s Prime Minister, John Key, added to the political uncertainty that had already materialized over the weekend in Italy.

The main event came later on in the week as the ECB’s policy decision came to light. At the conclusion of the meeting, the ECB’s Governing Council agreed to leave interest rates unchanged. However, the pace of asset purchases were adjusted such that they would fall by €20 billion to €60 billion per month in April 2017 and remain at that level through the end of December or beyond if deemed necessary. The decision to leave monetary conditions at a currently highly accommodative stance through 2017 bodes well for the gradual economic recovery in the Euro area and was

applauded by global market participants.

Things were less interesting at home. Second and third tier economic data did little in the way of moving markets. Of note was the rebound in the ISM’s gauge of the services sector in November, which rose to a 13-month high (Chart 1). Particularly encouraging were the gains seen in the business activity and employment sub-indices. Taken together, both components suggest that economic activity has accelerated after a slow start to the fourth quarter that may have been related to pre-election uncertainty and impacts of Hurricane

Countering some of this optimism was trade data for October, which revealed a broadly anticipated widening of theinternational trade deficit, a development that underscores the relatively weak external environment further exacerbated by a strong U.S. dollar and rising political uncertainty (Chart 2). Both U.S. dollar strength and political uncertainty will remain a dominant theme in 2017, likely acting as a drag on U.S. GDP over the next year.

Nonetheless, this week’s developments are unlikely to figure into next week’s much anticipated interest rate decision by the FOMC. Markets have been pricing in a 100% probability of a hike for over a month now, providing the FOMC with a strong signal that it is time to move along the Fed’s “gradual” hiking path. Domestic data has also been largely supportive, with the average pace of jobs growth coming in well above trend and firming wage growth continuing to nudge inflation towards the Fed’s 2% target. As such, we are almost certain that the fed funds range will be 25 basis points higher come Wednesday next week.

Neil Shankar, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 2, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

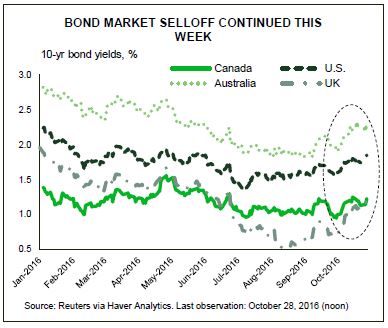

- Bonds sold off for the fourth consecutive week, while equity markets are set to decline for the first time since the U.S. elections.

- Investors have likely engaged in some profit taking in advance of next week’s events which could trigger increased market volatility. Sunday will see Italians voting on constitutional amendments and Austria’s Presidential election. But, the main event is set for Thursday, with the ECB widely expected to announce a tapering plan.

- Domestic data this week remained supportive of the narrative of continued U.S. economic recovery in the second half of this year. This morning’s payrolls data was less rosy than expected, but is unlikely to dissuade the Fed from raising its policy interest rate when it meets in a couple weeks.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

BOND MARKET SELLOFF CONTINUES FOR FOURTH CONSECUTIVE WEEK

The sell-off in global bonds continued through this week, marking the fourth consecutive week of sizeable losses for bond investors. The U.S. 10-yr Treasury yield hit 2.44% earlier this morning – a level not seen since mid-2015. European bond markets also sold off, with yields rising to early-2016 levels. The stock market failed to benefit from the exodus from bonds this week however, with

After some post-election euphoria, and with much uncertainty still remaining, investors look to have taken some profits and are repositioning themselves ahead of some important international events next week which risk triggering another bout of market volatility. Things will kick-off on Sunday, when Italians vote on constitutional amendments that would remove much of the legislative authority of the Senate, credited with creating legislative gridlock often blamed for delaying necessary economic reforms. Whatever the outcome of the referendum – which could result in the resignation of the pro-EU Prime Minister Matteo Renzi should it be rejected – isn’t likely to have material implications on financial markets outside of Italy. On the same day, Austria will hold Presidential elections for the second time this year after election irregularities were found in the May round. Although there are concerns about the potential election victory of the candidate from the far right FPO party, the election outcome is unlikely to have much impact on financial markets, with much of the authority in the office of the Austrian Chancellor rather than the President. The main market moving event is scheduled to occur next Thursday when the ECB is expected to reveal a plan to taper the pace of bond purchases alongside their interest rate decision.

Together with higher inflation expectations due to firmer oil prices, the anticipated tapering as early as the second quarter of 2017 accounts for much of the bond selloff this week.

The selloff was further supported by strong domestic data, which continue to support the narrative of an economic recovery in the second half of 2016. This week, the second estimate of GDP growth was revised up to 3.2% (q/q annualized), up from the initial estimate of 2.9%. Moreover, although consumer spending in October was somewhat disappointing – partly owing to warmer weather – but strong income growth over the past several months should contribute to a bright holiday season.

All told, given the inflow of positive data for the second half of 2016, even a large miss in this morning’s payroll report would have likely failed to dissuade the FOMC from voting to raise its interest rate target in a couple weeks. Although non-farm payrolls increased by 178k in November, well above trend, although the underlying details were not overly optimistic. Private sector payrolls disappointed, while the participation rate ticked down to a six month low, and wage growth slowed. While not a cause for alarm, today’s report highlights that the Fed will seek to tighten at a gradual pace, especially given the significant tightening already embedded in the recent run-up in rates and the dollar.

Fotios Raptis, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 25, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S. stock markets continued to rise, with all three major indices reaching record highs. Economic data on the domestic front was generally constructive, with a number of indicators surprising to the upside.

- The Fed minutes released this week confirmed what many already believed, mainly that the economy is making progress and that a rate hike is likely to come ‘relatively soon’. The market is now fully pricing in a rate hike in December.

- With limited details on the scope and timing of fiscal policy, the path of interest rates beyond December is perhaps even more uncertain in the election’s aftermath.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

MUCH TO BE THANKFUL FOR

With markets closed on Thursday in observance of Thanksgiving, this was a short, but exciting week. Investors continued to pull money out of emerging markets, while U.S. stock markets continued to rise, with all three major indices jumping to record highs for the first time since 1999 (Chart 1).

These market dynamics were largely responsible for boosting the value of the U.S. dollar against other major

currencies. The DXY index currently sits at a 13-year high. Economic data on the domestic front was also generally supportive, with a number of indicators surprising to the upside. Consumers felt upbeat in the aftermath of the election, with the University of Michigan consumer sentiment beating expectations and recording the largest single monthly gain since late 2013. This should bode well for consumer spending during the important holiday season. Durable goods orders also shattered expectations, rising 4.8% m/m in October, reinforcing an emerging recovery in business investment.

Data on housing was more mixed, with new home sales falling more than expected, but existing home sales surprising to the upside and reaching the highest level since February 2007. The recent climb in interest rates will likely pull forward home sales as consumers try to lock in rates, while having a dampening effect on activity in subsequent quarters. The recent back-up in mortgage rates may slow, but is unlikely to derail the U.S. housing recovery.

With respect to interest rates, the Fed minutes released this week confirmed what many already believed, mainly that the economy is making progress and that a rate hike is likely to come ‘relatively soon’. The market is now fully pricing in a rate hike in December with a probability of 100%. Rising inflation expectation in the aftermath of the election have strengthened the case for a hike, while next week’s payrolls report should provide further support with consensus expecting a gain of 180k – well above the level necessary to keep downward pressure on the unemployment.

As a result, the million dollar question has shifted from whether the Fed will hike to how fast it will hike going forward. Fed officials have been consistent in telegraphing a gradual hiking cycle. Still, with the unemployment rate quite low, there is a possibility that the economy may run a little hot, especially with the fiscal stimulus that has been pledged by the new administration. If that is to materialize, the hiking cycle would likely run a little faster as well.

As such, the path of interest rates beyond December is perhaps even more uncertain now than before the election. More clarity is likely to come in late January when the new administration begins to implement its agenda, while the Fed adjusts accordingly. For now, with the economy in decent shape and most financial and domestic data chiming in festive tunes, there is much to be thankful for.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 18, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The Trumpflation trade continued this week with emerging markets and bonds selling off, as money piled

into U.S. equities. - The U.S. dollar remained well supported this week, with domestic economic data telegraphing strength

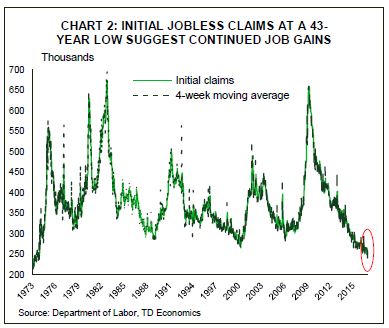

while comments by Fed officials suggested a rate hike looks imminent. - Highlights of the data-heavy week included housing starts rising to a nine-year high, initial jobless claims

falling to a 43-year low and retail sales notching up the strongest two months in just as many years. - Core inflation moderated to 2.1% in October from 2.2% in September, while headline ticked up to 1.6%

as past drag from energy prices continued to dissipate.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

DECEMBER RATE HIKE LOOKS TO BE IN THE BAG

The reflation (or Trumpflation) trade continued unabated this week. Investors continued to pull money out of emerging markets, which were expected to fare poorly in light of the President-elect’s anticipated trade policies. Treasuries too continued sell-off on rising inflation expectations as investors positioned themselves for pro-growth policies in the U.S. as well as anticipation of higher supply of debt related to unfunded fiscal stimulus. The 10-year Treasury bond yielded nearly 2.3% this morning, while the 30-year bond yield neared 3% – 40 basis points from pre-election levels.

Emerging market currencies have taken the brunt of the sell-off. The Mexican peso is down more than 20% from last year with half of the decline taking place since the election. Fears of rising inflation led the Bank of Mexico to raise rates by 50 basis points yesterday – its fourth move this year – to the highest level since 2009. Still, the Bank expects that inflation will notch above its 3% target next year while growth could slow given the “the new international environment.”

The Chinese currency also remained under pressure in recent days as capital outflows intensified. The People’s Bank of China allowed the yuan to depreciate by way of its daily fix by nearly 2% to the U.S. dollar from early-November –a record eleven consecutive days of declines. The weaker renminbi-dollar fix prevented the yuan from appreciating vis-à-vis its other trading partners, and potentially denting already slowing growth.

The U.S. dollar strength, which, last week was more related to anticipated changes in policy, was this week, supported by strong domestic economic data and Fed comments. On the data front, homebuilding activity surged to a nine-year high, and while partly related to Hurricane-related weakness in the prior month, it nonetheless painted a picture of strengthening residential

Despite core inflation moderating to 2.1% in October from 2.2% the previous month, the headline measure ticked up to 1.6% as drag from energy prices dissipates. While this remains below the Fed’s 2% target, the Fed appears increasingly comfortable that it will rise to target over the medium term. The Fed also is appears hesitant to further delay the rate hike, with Chair Yellen suggesting in her Congressional Testimony this week that such a move risks having to raise it faster thereafter and encouraging excessive risk taking. A December hike appears to be in the bag.

Michael Dolega, Director & Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of October 28, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The odds of a rate increase in December have continued to climb higher this week, rising to about 75%

from 67.5% a week ago and 54% last month. - Expectations were buoyed by hawkish Fedspeak and solid domestic data. Following declines in the prior

month, sales of new single-family homes and pending home sales both surprised to the upside in September.

Housing prices also continued to grow briskly in August, advancing by 5.3% y/y. - U.S. GDP was the key data release of the week. Based on the advance estimate, the U.S. economic

momentum accelerated markedly in Q3, with GDP rising by a healthy 2.9% (SAAR). - With near-term market expectations for monetary policy converging to those of the Fed and the economic

data remaining supportive, the FOMC will likely use next week’s statement to communicate its intentions

to raise rate in December.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

MARKETS AND FED NO LONGER AT ODDS

U.S. monetary policy was top of mind for investors this week in anticipation of next week’s FOMC meeting. Buoyed by hawkish Fedspeak and solid domestic data, the odds of a rate increase in December have climbed to 75% this morning – well above the near-even odds just a few weeks ago. Rising expectations that the Fed will move off the sidelines this year continued to support the U.S. dollar, which is trading near its highest level since January. Meanwhile, bonds continued to sell off, pushing yields higher, with yields on the 10-year Treasury note rising by 11 basis points this week.

Investors were treated to several Fed speeches early this week, ahead of the blackout period that began on Wednesday afternoon. Fed officials largely maintained the slightly hawkish bias, with Charles Evans (Chicago) noting that he expected the Fed to hike three times by the end of next year. St. Louis Fed President, James Bullard, also indicated that December was the “most likely” option for a rate increase.

In additional to this upbeat rhetoric, domestic data also remained encouraging this week. Following declines in the prior month, sales of new single-family homes and the index of pending home sales both surprised to the upside in September. While sales of new homes can be volatile on a month-to-month basis, they have been on an upward trend this year and 30% higher than last year. The newly-built market has been benefiting from the limited inventory of existing houses, prompting potential home buyers to visit homebuilder showrooms. A limited inventory of houses on the market has also kept the pressure on existing home prices. They continued to grow briskly in August, advancing by 5.3% y/y – a slight acceleration from 5.1% y/y pace seen a month prior. Home prices are now within a hair of a full recovery and are helping rebuild household wealth – having accounted for nearly half of the total increase in household assets over the past year.

While the gains in the above indicators were encouraging, the most eagerly awaited data release this week was the first look at third quarter U.S. GDP. The headline print did not disappoint. Following the sluggish near-1% growth that prevailed in the first half of the year, the U.S. economic momentum accelerated markedly in the third quarter with GDP rising by a healthy 2.9% (SAAR), beating the median consensus estimate of 2.6%. Consumer spending also remained resilient. While decelerating to 2.1%, the slowdown comes atop of an unsustainably strong 4.3% gain the prior quarter. The headline GDP print was also boosted by a positive contribution from non-residential investment, inventories, and international trade – all of which weighed on growth over prior quarters. We expect both non-residential and inventory investment to remain supportive in the coming quarters, underpinned by reduced drag from the oil sector and the rebuilding of inventories that were previously drawn down. Residential investment, which has disappointed in recent quarters, is also expected to turn from a headwind to a tailwind as rising prices and a limited inventory of houses on the market boosts construction. Meanwhile, the strength in net exports – which added an outsized 0.8pp to the headline number – is unlikely to persist. The gain in exports was driven by a large one-time boost from soybean exports. Moreover, U.S. economic outperformance and diverging monetary policy continue to pressure the dollar higher (for more detail see our recent Dollars & Sense).

All in all, with near-term market expectations for monetary policy converging to those of the Federal Reserve and the economic data remaining supportive, the door for a rate hike this year remains wide open. While a move next week remains a distant possibility, given the proximity to the presidential election, the Fed will likely use next week’s statement to communicate its intentions to seal the deal in December.

Ksenia Bushmeneva, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

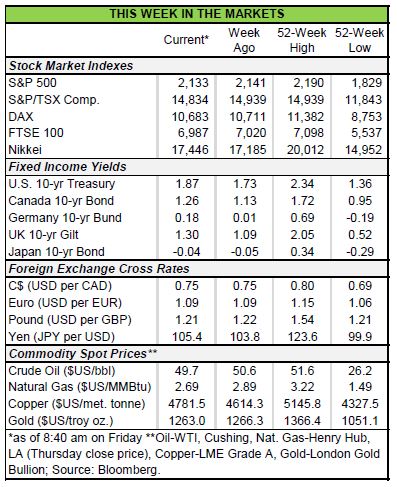

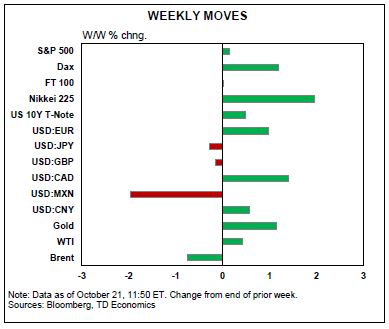

Financial News for the Week of October 21, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Stocks are poised to finish the week in positive territory for the first time in a month, helped by a good start to earnings season which suggests the U.S. profit recession is likely coming to an end.

- U.S. data remains supportive of a near-term rate hike with wage pressures broadening. Speeches by Fischer and Dudley this week suggest both are in favor of a rate hike this year given the current trajectory.

- The Chinese economy expanded 6.7% from a year ago in Q3, helping assuage fears that it is slowing more abruptly than anticipated. Consumption and fixed investment supported growth while industrial production disappointed. Despite the solid print, concerns about unsustainable credit growth remain.

- The ECB left policy rates and QE program framework unchanged this week, punting any policy refresh to December. ECB President Draghi adamantly talked down any notions of near-term tapering of asset purchases, emphasizing that policy will remain accommodative even after any eventual reduction in QE.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

WAITING FOR DECEMBER

Sentiment was good in global markets this week. Stocks look to finish the week in positive territory for the first time in a month. Earnings season was off to a good start in the U.S. with the U.S. profit recession likely to come to an end. U.S. longer term bond yields remained rangebound, while shorter dated securities continued to sell-off in anticipation of a near-term Fed hike. The dollar benefitted, rising to its highest level since February, on relatively constructive data and hawkish Fedspeak. Investor sentiment was also shored up by the ECB and positive Chinese data.

The world’s second largest economy expanded 6.7% from a year ago in Q3, helping assuage fears that it is slowing more abruptly than anticipated. On the whole, industrial production disappointed, but activity was shored up by fixed investment and consumption. While concerns that growth remains tied to unsustainable credit expansion remain, investors were nonetheless comforted by the figures with sentiment further supported by the reappearance of inflation. Nominal GDP advanced by 7.8% y/y in the quarter, with the GDP deflator advancing by the fastest pace in two years as drag from past commodity declines dissipates.

Inflation is also improving in the Eurozone, with headline prices up 0.4% in September and core CPI up an even stronger 0.5%. Still, the ECB’s Governing Council remains unconvinced that underlying inflationary pressures are building. The ECB left policy rates and QE program framework unchanged this week, as widely expected, with President Draghi punting any policy refresh to December – a meeting that will correspond with updated economic forecasts. Importantly, Draghi adamantly talked down any notions of near-term tapering of asset purchases, which caused a

sell-off in Eurozone bond markets, further emphasizing that policy will remain accommodative even after any eventual reduction in asset purchases.

Monetary policy will also remain highly accommodative in the U.S. despite the likely quarter-point increase in the fed funds rate target later this year. Chair Yellen’s speech last week, where she

Data released this week remained supportive of such narrative. While housing starts and initial claims disappointed somewhat, these may have been distorted by Hurricane Matthew. On the other hand, building permits and existing home sales both surprised to the upside, suggesting continued housing recovery. Inflation was also relatively firm, with headline CPI accelerating to 1.5% while the core measure remained just above 2% in September. Lastly, the recent Beige Book highlighted broadening labor shortages and wage pressures, corroborated by the 3.6% y/y gain in median wages. On the whole, both reports reinforce the notion that inflationary pressures in the U.S. are building and provide additional impetus for a rate hike in December.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

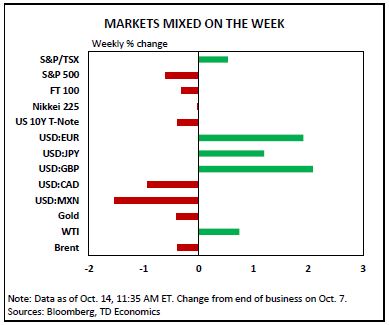

Financial News for the Week of October 14, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- After last week’s ‘Goldilocks’ jobs report, the positive data stream continued for the U.S. economy, with retail spending in September rising by the most in three months.

- Taken together, both reports provide confirmation that the American consumer will remain a key driver of economic growth as we slowly approach the very important holiday shopping season.

- The data appear to be falling in line with expectations of most Fed officials telegraphed in the minutes of the September FOMC meeting.

- Though a rate hike a week before the November election remains unlikely, the Fed looks increasingly likely to slip in an increase before year-end so long as data continues to cooperate and downside risks do not materialize.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

FOMC MINUTES FRONT AND CENTER ALONG WITH RETAIL SALES REPORT

The minutes from the September 20-21st FOMC meeting and speeches from a few Fed officials, along with the September retail sales report took center stage on the domestic calendar this week. The international calendar was relatively light, with few notable data out of China dominating headlines. Overall, the Chinese data disappointed, while domestic releases were far more

The key point of contention in the discussion had to do with the amount of remaining slack in the labor market. Some believed that slower payroll growth and a pickup in wages recently indicated “little or no remaining slack.” Others viewed wage growth as still-muted and argued that rebounding labor force participation suggested that slack remained. Markets reacted by upping the probability of a December hike above two-thirds, from closer to 60% the previous week. The USD also saw broad-based strength throughout the week, with the DXY rising by 1.3% through this morning.

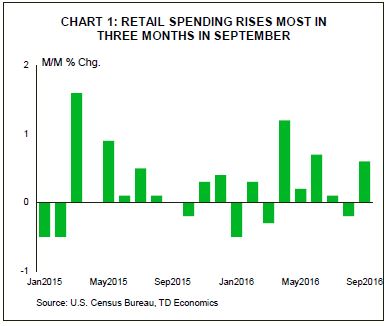

Following the minutes, markets turned to this morning’s retail sales report. After two months of relatively subdued performance, retail sales rose 0.6% in September (Chart 1). Figures for the two prior months were also revised up slightly. Overall, the bounce back in September fell in line with last week’s ‘Goldilocks’ employment report (Chart 2) and taken together, these provide confirmation that the American consumer should remain a key driver of economic growth.

On the other hand, international data was less constructive. Trade data out of China for September painted a rather grim picture. The trade surplus narrowed from $52.05bn to $USD42.0bn as exports fell sharply during the month, raising concerns of a sharper slowdown. Concerns around a ‘hard-Brexit’ also continued to surface, sending the British pound another 2.0% lower vis-à-vis the USD over the past week. Despite the Fed viewing near-term risks as “roughly balanced” at this point, both of these developments highlight the need for these developments to be closely monitored. – something the Fed intends to do.

While a softer global economy remains the current reality, domestically the data continues to come in relatively constructively. As long as this progress is maintained, a data-dependent Federal Reserve will likely remain on track to raise interest rates in the near future. Although a rate hike a week before the November election remains unlikely, the Fed appears increasingly likely to slip in an increase before year-end.

Neil Shankar, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of October 7, 2016

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

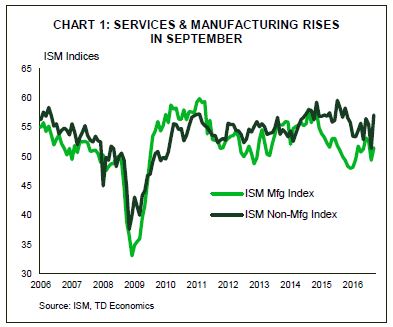

- While attention is focused on Hurricane Matthew, at least there was some good news from the U.S. economy. Both ISM sentiment indices pointed to greater confidence in September for manufacturing and services.

- A solid employment report added to the good news, with 156K workers added to payrolls in September. The details were also good, with the slight uptick in the unemployment rate from 4.9% to 5.0% due to a growing labor force, rather than job losses.

- Unfortunately, things weren’t so rosy across the pond. Recent statements from leaders in the UK and France reminded markets that “Brexit means Brexit”, which took the pound sharply lower on the week.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

AMERICANS GO BACK TO WORK IN SEPTEMBER

Many in the U.S. are more focused on potential damage being caused by Hurricane Matthew bearing down on the south this week, but the news for the economy was much sunnier. The overall

For the U.S. economy, the good news started with the ISM Manufacturing Index, which provided some reassurance industry is weathering the strong dollar and weak global growth. The index moved back up above 50 (see Chart 1), indicating expansion. It was followed with a jump up in the services ISM, also pointing to greater confidence on the services side of the economy. One of the more tangible measures of consumer confidence is auto sales, given the big ticket nature of the purchase, and sales in September improved. Solid September sales rounded out the strongest quarter since last year. This helps underpin our recent forecast that healthy consumer spending in Q3 was likely driven by durable goods purchases.

The September jobs report provided further evidence that robust consumer spending is well-supported by continued job gains. 156K new jobs were added to payrolls in September, roughly as we expected. Normally we wouldn’t cheer an uptick in the unemployment rate (from 4.9% to 5.0%), but in this case it was due to an increase in labor force participation, which is positive. The low level of labor force participation since the recession has been a

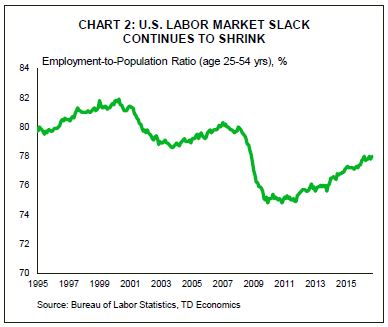

Zeroing in on the core working age employment rate (age 25 to 54), which removes the downward influence of population aging on the rate, the amount of “slack” in the labor market has made notable progress (see Chart 2). The stronger labor market is clearly drawing new, or previously discouraged, workers into the job market. This will please the Fed, as Chair Yellen has referred to slack remaining in the labor market.

The combination of higher oil prices and better economic growth signals also took market-based measures of inflation expectations (such as the 5-yr-5-yr breakeven rate) to their highest readings since May. This will also be welcomed by the Fed, which wants to see more evidence of inflation before raising rates again. Add it all up, and our case for a December rate hike has strengthened over the past week.

It wasn’t so long ago that the Bank of England was expected to be the next major central bank to raise interest rates. But the Brexit vote put a stop to that. Sentiment on the UK economy weakened even further this week as financial markets give up hope on a “soft” Brexit. Unsurprisingly, without preferential access to the UK’s largest export market the outlook for the UK dims. This has further dampened market sentiment on the pound, which now sits at its lowest level since 1985.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.