Financial News for the Week of June 30, 2017

HIGHLIGHTS OF THE WEEK

- Bond markets sold off sharply this week on remarks from monetary policymakers. Bond yields rose by 20 to 25 basis points in Germany and the UK, respectively. Yields on Treasuries also rose, but markedly less as U.S. data has underwhelmed.

- Momentum in personal spending dissipated slightly from the strong performance in the previous two months. Gains in real income surprised to the upside, and should underpin spending going forward.

- We look forward to next week’s employment report as a potential market mover. We expect a relatively robust print of 170 thousand jobs and unemployment to hold steady at 4.3%.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

Hawkish Central Bank Rhetoric Rattles Markets

Global markets were volatile in recent days. Bond markets sold off sharply since mid-week on remarks from monetary policymakers. Central bankers in the Eurozone and the UK have indicated that meaningful economic improvements should begin to warrant the removal of accommodative monetary policy measures. This hawkish sentiment saw bond yields rise by 20 to 25 basis points in Germany and the UK, respectively. Yields on Treasuries also rose, but markedly less as U.S. data has underwhelmed. The relatively softer U.S. data also led the dollar lower vis-à-vis the euro and the pound.

The lower U.S. dollar also helped to shore up oil prices that have been led higher recently by curtailed production related to maintenance of Alaskan sites and a storm in the Gulf of Mexico. Still, US stockpiles have remained high this summer, with oil prices likely to remain relatively anchored during the rest of the year.

Expectations of less-stimulative policy going forward have also led stock markets to retrench as investors across the Atlantic readied themselves for what may be end an era of cheap money. At the same time, comments by Fed Chair Janet Yellen on Tuesday indicated that the Fed is keeping a close eye on stock markets valuations, injecting further caution into U.S. equity markets.

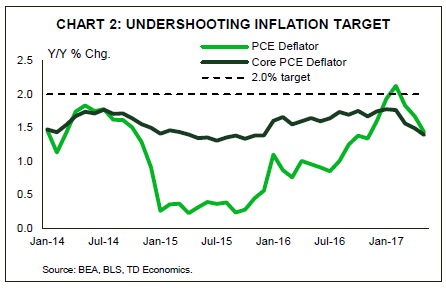

Still, the U.S. data came in relatively weak this week. While still supportive of growth in the second quarter, momentum in personal spending dissipated slightly from the strong performance in the previous two months. Gains in real income surprised to the upside, and should underpin spending going forward (Chart 1). But, this was partly related to the weakness in prices, which under-performed in May, corroborating anemic CPI growth on the month (Chart 2). There was also weakness in durable goods orders, which fell in May according to the advance estimate, suggesting weaker capital investment in the second quarter.

But, not all data were soft. Consumer confidence metrics rose according to both the Conference Board and University of Michigan surveys. Moreover, the goods trade balance narrowed slightly in May as automotive exports rebounded following two consecutive months of underperformance. With domestic US auto sales peaking last year, global demand will play an increasingly important role for growth in the sector. Exports should also get some support from a weaker greenback. We look forward to next week’s ISM manufacturing survey results to echo these positive developments, with readings poised to expand, mirroring upbeat regional surveys for June.

Katherine Judge, Economic Analyst

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 23, 2017

HIGHLIGHTS OF THE WEEK

- Equity markets started off the week on a positive note. But the advance proved transitory as oil prices slid into bear territory, sending energy stocks and the main indices lower.

- With little in the way of economic data, Fed speeches took center stage. While echoing support for last week’s decision, some Fed speakers appeared to take on a more dovish tone, with Harker and Evans putting an emphasis on waiting for further proof to hike again.

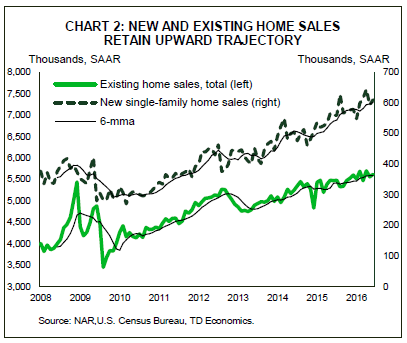

- The only significant economic data releases this week pertained to housing activity. Existing home sales surprised on the upside. Meanwhile,sales in the smaller and more volatile new home market, also rebounded in May.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

FED SPEECHES TAKE CENTER STAGE

Markets started off the week on a positive note. Tech stocks bounced back on Monday as industry leaders met with President Trump at the first gathering of the American Technology Council. Meanwhile, financials were buoyed by comments from FOMC voting member Dudley that didn’t seem too concerned with the slowdown in inflation. Sentiment was also supported by Macron’s majority-win of the French parliamentary elections.

Unfortunately, the advance proved transitory. Oil prices slid into bear territory on account of rising production among the U.S., Libya and Nigeria and doubts as to whether recent OPEC cuts would be sufficient to manage the supply glut. This sent energy stocks and the main indices lower and enabled a move toward safe heaven assets (Chart 1).

With little in the way of economic data, Fed speeches took center stage. Given that last week’s decision to hike was not unanimous and the fact that inflation has drifted lower, FOMC members appeared to be on the defensive. Vice-Chair Fischer pointed to “high and rising” home prices as one of the hazards of keeping rates low for long. While echoing support for last week’s decision, other Fed speakers appeared to take on a more dovish tone, with Harker and Evans putting an emphasis on waiting for further proof to hike again. Bullard (non-voter) suggested that the expectation for rates rise to 3% over the next two and a half years is “unnecessarily aggressive.”

Still, the Fed is sticking to its guns in expecting another rate hike by the end of this year, betting that the factors weighing on price growth will prove temporary and that a tight labor market will pull up wages and buoy inflation. They may also get some help from a lower U.S. dollar, which is well off its peak level set earlier this year and is on track to end lower again the week. A lower dollar should help put upward pressure on goods prices, which have been consistently negative over the past year.

Rising interest rates, combined with robust price growth on the bigger resale segment are expected weigh on affordability. Still, households are likely to withstand the incremental increases in borrowing costs thanks to a solid labor market that is poised to deliver continued job and income gains. An improvement in the homeownership rate is also expected to provide a gentle tailwind as outlined in our recent report, with resales expected to advance by 3.4% this year and 2.6% in 2018 to nearly 5.8 million by the end of the forecast horizon. Price growth should remain strong this year, holding near 6%. But a rebound in for-sale inventory, which is expected to be more of a factor next year, will help keep price growth in check at around 4% in 2018.

Admir Kolaj, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 2, 2017

HIGHLIGHTS OF THE WEEK

- The U.S. job machine slowed in May (+138k jobs) as the unemployment fell to a sixteen year low of 4.3%. A pullback in the participation rate contributed to the fall in the unemployment rate.

- The Federal Reserve’s preferred measure of price growth slowed in April to 1.7% (from 1.9%), while the core measure fell to 1.5% (from 1.6%).

- Weak inflation will probably not forestall a rate hike in June, but continued weakness could be enough to delay further rate hikes. Just as much as job growth, this is an important metric to watch for guidance on future Fed action.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

THE FED'S CONUNDRUM: LOW UNEMPLOYMENT, SLOW INFLATION

The Federal Reserve has a conundrum. Its dual mandate is for maximum employment and price stability. On the latter, inflation has remained stubbornly below its 2% target. In April, the Fed’s preferred core inflation measure slowed to 1.5% from a recent peak of 1.8% in February.

On the former however, it’s becoming harder and harder to argue that the American economy is not nearing full employment. In May, the unemployment rate ticked down to 4.3% – its lowest level in sixteen years. Broader measures of unemployment, such as the U6 (which adds marginally attached workers and involuntary part-timers to the tally) also fell to 8.4% - its lowest level in nearly a decade.

There are a few ways to square this circle. The first, as referenced by Brainard, is that well-anchored inflation expectations have reduced the impact of economic slack on inflation. In economics jargon, the slope of the Phillips curve may still be negative (inflation rises as unemployment falls), but it has flattened.

A second explanation is that even as unemployment has fallen, so has the theoretical unemployment rate associated with full employment. On this front, the median projection for the long-term unemployment rate among FOMC members has moved consistently downward. Given the recent moves in unemployment and inflation, there is a good chance that it will do so again in June. There is a good argument that an aging population puts downward pressure on the natural rate of unemployment. One can see this dynamic in Japan where the measured unemployment rate is at an all-time low, yet the economy continues to be plagued by deflation.

A third explanation is that the unemployment rate is no longer an accurate measure of labor market slack. While the more inclusive measures have also been falling, the still-limited rebound in core-age participation rates suggests more slack may exist. Alongside a potentially lower natural unemployment rate, this larger “shadow” gap could be diluting the inflationary impact of the tightening labor market.

Putting it all together, the improvement in the labor market may provide the impetus for the Federal Reserve to continue to raise interest rates, especially if productivity remains weak and it is satisfied that wage growth is moving higher. Still, it cannot ignore the inflation side of its mandate. Continued underperformance on the inflation front will strengthen the case for patience and likely lead the Federal Reserve to slow the pace of rate hikes.

James Marple, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 26, 2017

HIGHLIGHTS OF THE WEEK

- Despite the upward revision to first-quarter GDP growth, with the second estimate indicating a 1.2% annualized gain on stronger consumption and investment, market reaction was relatively subdued given that the overall story is largely unchanged.

- Although investors are almost fully pricing in a June rate hike, the yield curve flattened this week as longer term growth prospects became murkier and the Fed communicated that the balance sheet unwinding process would be protracted.

- Strength in consumption should leave the U.S. economy 3.3% larger this quarter, for an average growth of 2.2% during the first half of the year. While this is far from red-hot, it nonetheless is enough to reduce slack and should enable the Fed to continue along its gradual rate hike path.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

FED MINUTES SIGNAL JUNE RATE HIKE

Despite the upward revision to first-quarter GDP growth, with the second estimate indicating a 1.2% annualized gain on stronger consumption and investment, market reaction was relatively subdued given that the overall story is largely unchanged. After another slow start to the year in 2017, economic growth appears to be rebounding this quarter, and should help to further diminish labor market slack.

That narrative was expressed in the minutes of the FOMC meeting released this week, which confirmed that participants are willing to see through the first-quarter weakness, and more robust data should be enough to justify a June rate hike. The minutes suggested some discomfort about softer inflation readings for March and April, with the Fed anticipating the upcoming inflation reports to confirm the one-off nature of the declines. Next week’s payrolls should also help mitigate further concerns should the American economy continue to produce jobs at a healthy clip and wage growth pick-up.

Despite investors almost fully pricing in a June rate hike, the yield curve flattened this week as longer-term growth prospects became murkier and the Fed communicated that the balance sheet unwinding process would be protracted. Trump’s proposed budget released this week featured projections of a drastically reduced debt-to-GDP ratio. But the feasibility of the plan is already being contested given its generous underlying growth assumptions. At the same time, the administration’s efforts to push through health care and tax code reform are being met with significant opposition from Congress, leading bondholders to pare back their longer-term growth forecasts. So far, equity investors have remained upbeat, with stock prices recovering last week’s losses, supported by stellar first quarter corporate earnings.

Oil tumbled this week as OPEC’s extension of production cuts through to Q1 2018 fell short of market expectations. The decision comes amidst a surge in US shale production to its highest level since August 2015, keeping oil inventories elevated and having the potential to undermine OPEC’s agenda. Having said that, we expect that oil will find its footing and will end the year higher as U.S. production growth decelerates and the market rebalances.

Economic data out this week was relatively modest. Sales of new and existing homes pared back in April, after a strong start to the year. Moreover, April’s advanced international goods trade balance widened unexpectedly as the surge in imports outpaced the rise in export volumes. Ultimately, the strength of U.S. demand and a relatively elevated dollar will boost imports and hinder export growth, with offsetting impacts on U.S. manufacturers. Next week’s ISM manufacturing index will likely telegraph continued growth for the sector, albeit at a slightly slower pace.

Next week’s income and spending data will provide information on how consumers and inflation performed during the very important handoff month of April. We expect growth in consumption to accelerate from 0.6% in the first quarter to about 3.4% during Q2. Taken together with some inventory investment, the strength in consumption should leave the U.S. economy 3.3% larger this quarter, for an average growth of 2.2% during the first half of the year. While this is far from red-hot, it nonetheless is enough to reduce slack and should enable the Fed to continue along its gradual rate hike path.

Katherine Judge, Economic Analyst

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 19, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investors perceived this week’s political developments in the U.S. as likely to delay the implementation of pro-growth policies. As a result, they risk assets sold off midweek in favor of gold and treasuries. Risk appetite appeared to make a comeback toward the end of the week along with some reversal in earlier trends, particularly among American equities.

- Underneath the political noise, the economy continued to emit mostly positive signals which included a rise in industrial production and capacity utilization, and falling jobless claims. Homebuilding appeared to be a soft spot at first glance, but the details reveal a better story.

- The Fed will keep an eye out for financial market stress, but is likely to continue focusing on signals from the economy. So far, the outlook for the second quarter remains solid, with growth currently tracking north of 3% annualized. As such, odds are still in favor of a June hike.

CUTTING THROUGH THE POLITICAL NOISE

To say that political events dominated headlines this week may be somewhat of an understatement. The U.S. administration found itself in hot water once again over allegations of misconduct. Mounting political pressure reached a boiling point with the appointment of a special prosecutor to probe Trump-Russia ties. Financial markets perceived these developments as likely to delay the implementation of pro-growth policies such as tax reform and infrastructure spending, and quickly sold off risk assets. By midweek global stock markets followed the rapid decline in American indices (Chart 1). The trade-weighted U.S. dollar gave up all of its gains recorded since the U.S. election. In commodities, oil retained its upward trend and is poised to end the week above $50/bbl, buoyed by news that Russia and Saudi Arabia may extend their production cuts along with a report from EIA showing falling U.S. inventory levels.

Underneath the political noise, the economy continued to emit mostly positive signals. Industrial production rose 1.0% in April – the biggest monthly gain in more than three years. Capacity utilization also rose to 76.7% – the best level since late 2015, boding well for future business investment. Weekly jobless claims fell unexpectedly, with levels now resting near decade-lows seen as further signs of a tightening labor market. Lastly, homebuilding appeared to be a soft spot at first glance, but the details revealed a better story. The headline was pulled down by the volatile multifamily segment, while the single family segment retained its upward trend (Chart 2). The latter is a much larger and better indicator of economic conditions, and its advance is reflective of continued progress in the labor market. We expect this trend to continue as rising wages support household formation and demand for new homes.

Looking at the big picture there are two main points worth highlighting. First, investors will continue to pay close attention to political events because the implementation of pro-growth policies remains the cornerstone needed to validate today’s rich stock valuations. Intuitively, this suggests potential for further volatility in the weeks and months ahead. Second, the Fed too will keep an eye on such developments, not because it has placed much emphasis on the pro-growth policies to begin with, but rather because a market downturn could weigh on the real economy. Unless it sees concrete signs of this occurring, it is likely to continue focusing on underlying signals from the economy, particularly those related to inflation where recent readings have disappointed. So far, the outlook for the second quarter remains solid, with growth currently tracking north of 3% annualized. As a result, market participants will continue to price in a June Fed hike, with odds from CME Group currently pegged at 74%.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 12, 2017

HIGHLIGHTS OF THE WEEK

- Markets started the week off on a good note on French presidential election results and fairly constructive earnings and economic data. The S&P 500 flirted with record highs, and the VIX fell to its lowest level in more than two decades.

- Sentiment soured later in the week as soft inflation data overshadowed a relatively robust retail spending report, with sales up 0.4% atop of an upwardly revised March gain. Total CPI inflation decelerated from 2.3% to 2.2% in April with the core measure slowing from 2.0% to 1.9% on the month.

- Expectations for a Fed rate hike as of June pared back slightly, but remained above 75% through this morning. Unless data continues to disappoint, we expect the Fed will raise rates next month, with another hike likely later on in the year.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

SOFT INFLATION DATA PARES JUNE HIKE EXPECTATIONS

Markets started the week off on a forward foot with rising confidence in the global economy, helped by last Friday’s strong U.S. jobs report, further enhanced by the French presidential election results. The price investors demand to protect against volatility dropped, with the VIX falling early in the week, and touching its lowest level since 1993. U.S. equities were also supported by relatively strong earnings reports early in the week, with the S&P 500 flirting with the 2,400 point level. Meanwhile a mild rebound in oil prices, following the bullish inventory report, shored up energy stocks since mid-week. The mood soured somewhat by the end of the week as a relatively good retail sales report was overshadowed by weak CPI data.

The election of Emmanuel Macron as President of France, the centrist candidate who ran on a platform of reform, was expected and largely priced in by markets. Still, it was a welcome development for global investors following the protectionist tilt in popular sentiment across many advanced economies over the past year. The result comes alongside some improvement in economic fortunes. This week, the European Union revised higher its Eurozone and U.K. growth outlook, with industrial production and employment growth in France coming in better than expected recently. But, while the new president has some political capital, he faces significant hurdles to enacting the much needed pro-growth reforms, with much riding on the results of the legislative assembly elections to take place in a month.

The U.S. data calendar was relatively light until Friday. The NFIB Index of Small Business Optimism held up well, while labor market strength was further confirmed by a strong job openings in March and a decline in both initial and continuing claims in early-May. Investors also had a number of Fed speeches to digest. Most of the speeches stuck to the script telegraphed by last week’s FOMC policy statement, suggesting the Committee viewed the early-year weakness as transitory, and expected a firming in ‘hard’ economic data during the second quarter. Most Committee members continue to see a fair chance for two more hikes this year, and see the Fed beginning to wind down the balance sheet late this year or in early-2018.

The Fed’s expectations were only partly confirmed by this morning’s data. April’s retail sales were shy of expectations, but nonetheless indicated more consumption momentum into the second quarter given the upward revisions to March spending figures. On the other hand, consumer

While the soft CPI numbers may embolden a more dovish tilt within the FOMC, we believe that the strong April producer and import price data, which typically leads consumer prices, should help support the case for a rate hike. Moreover, while the soft CPI data has slightly pared back expectations for a move next month, markets continue to price in odds near 75%. Ultimately, unless the data continues to disappoint, we don’t expect the Fed will pass on the opportunity to raise rates next month.

Michael Dolega, Director & Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 5, 2017

HIGHLIGHTS OF THE WEEK

- The past week was action packed with economic data and events in Washington. Data largely supported the view that the U.S. economy will bounce back from its winter weakness.

- The job market sprang back into action in April, enabling investors to heave a sigh of relief that the fundamentals remain in place for a Q2 rebound. The Fed expressed its confidence in the economy in its statement accompanying its stand pat rate decision.

- Still, weak auto sales and a recent loss in inflation momentum suggest the U.S. economy is not entirely out of the woods. The Fed will be watching the data closely in the coming weeks before the case for a June hike is cemented.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

ECONOMY SHOWING SIGNS OF SPRING THAW

From Washington to Wall street, there was no shortage of news for investors to digest this week. Data largely supported the view that the U.S. economy is bouncing back from its winter weakness. Markets have one eye turned on policy shifts in Washington too, where the GOP took baby steps towards repealing and replacing Obamacare (ACA). The revised American Health Care Act (AHCA) passed the House by a very narrow margin, but faces a bigger challenge in the Senate.

Investors heaved a sigh of relief on Friday as the job market bounced back in April, bearing out the Fed’s confidence in the economy expressed in Wednesday’s rate announcement. Payrolls advanced 211k jobs in April and the unemployment rate fell to 4.4% – the lowest level since 2007. Broader measures of labor market slack also declined, with the

As expected, the Fed kept interest rates unchanged on Wednesday and issued a largely status quo statement. It pointed to continued improvement in the labor market, while seeing through disappointing economic growth in the first quarter. The weakness in inflation in March was noted, but one-month’s result is unlikely to sway the Fed. As Yellen has continually emphasized, the Fed’s path is data dependent. So, members will be watching the data closely over the next few weeks as indicators for the second quarter are released. If the numbers confirm that a second quarter rebound is underway, and that the slowdown in inflation has not become more entrenched, we would expect the Fed to take rates higher in June.

Passing healthcare reform into law is arguably a necessary pre-condition to making further changes to the tax code. This is because the savings achieved leave room to cut taxes without expanding the deficit. The Congressional Budget Office has not yet scored the new bill, but the previous bill reduced the deficit by over $330 billion over the next decade. This is only about one-tenth of what is necessary to pay for Trump’s proposed tax cuts, but it might allow for some reduction in the corporate tax rate. In any case, there is a long road ahead on forging consensus on both the AHCA and eventually tax reform, leaving the potential for further sentiment disappointments in the months ahead.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 28, 2017

HIGHLIGHTS OF THE WEEK

- First quarter GDP growth came in at just 0.7% (annualized) - slightly weaker than consensus. The main culprit behind the slowdown was consumer spending, which barely grew. Much of the drag on growth appears to be temporary and we expect activity to rebound above 3% in the second quarter.

- The U.S. administration brought tax reform back into the limelight by releasing a revised one-page blueprint. An emphasis on tax cuts, coupled with a sigh of relief stemming from the French presidential election results, revived appetite for risk assets and helped lift major U.S. stock indices.

- The possibility of a government shutdown remains a near-term risk. Should it take place, the impact would likely not be enough to derail the economy, provided the shutdown is not prolonged.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

FIRST QUARTER GROWTH SOFT, ACTIVITY EXPECTED TO REBOUND

The week was light on primary data releases, with the advance estimate of first-quarter GDP dominating headlines. Growth was anticipated to be soft, and came in at just 0.7% (annualized). This is on par with our estimate, but slightly weaker than consensus and marks another year of soft first-quarter growth. The main culprit behind the slowdown was consumer spending, which barely grew (in what is becoming something of a pattern) (Chart 1). Not all was bad news however, as non-residential

Second tier economic data came in somewhat mixed, with a surge in new home sales, acceleration in employee compensation, resilient pending home sales, and some pullback in consumer confidence. Still, investor attention was primarily focused on political events. The U.S. administration brought tax reform back into the limelight by releasing a revised one-page blueprint. An emphasis on tax cuts, coupled with a sigh of relief stemming from the French presidential election results, where pro-EU candidate Macron took the lead in the first round, revived appetite for risk assets. This helped lift major US stock indices, while lowering prices for safe-haven assets such as gold (Chart 2).

The updated tax blueprint is broadly similar to its prior version. Differences include tweaks to individual tax rates and support for a territorial tax system where foreign earnings are exempt from U.S. tax. The absence of a destination-based cash flow tax, supported by the House Republicans, was also notable. The lack of detail makes it challenging to place a price tag on the plan, but one estimate pegs costs at between $3 and $7 trillion over the next decade. The plan is said to ‘pay for itself’, but broad consensus suggests otherwise, and without offsetting cuts the proposed changes are likely to bloat the deficit.

Politics continued

All things considered, the aforementioned developments are unlikely to sway the Fed’s decision at next week’s FOMC meeting, with the Fed unlikely to resume its hiking cycle until June. The possibility of a government shutdown remains a near-term risk, even as steps taken today will extend funding by one week. Even if it does occur, the impact will not derail the economy provided it is not prolonged. Drawing on the 2013 experience, a two week impasse would likely shave off 0.3 pp from quarterly annualized growth. Still, these effects could become amplified should the ongoing uncertainty spill over into private sector spending and investment decisions.

Admir Kolaj, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 21, 2017

HIGHLIGHTS OF THE WEEK

- Investor sentiment remained relatively upbeat this week on constructive economic data, positive earnings reports, and hopes for near-term pro-growth policies.

- Still, safe-haven assets remained in demand, supported by rising geopolitical tensions and anxiety over the first round of the French presidential election this Sunday.

- Overall, economic data has been coming in relatively healthy, both in the U.S. and other advanced economies, but the dichotomy between soft and hard data is hard to miss. This is particularly the case for the U.S. where survey data surged while hard data suggest that economic growth largely fizzled out in the first quarter. Having said that, some convergence appears to be in the offing.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

HARD AND SOFT DATA BEGINNING TO CONVERGE

Market sentiment remained relatively sanguine this week. Equities in the U.S. were supported by a string of positive earnings reports and hopes for near-term pro-growth policies. Treasury Secretary Steven Mnuchin indicated that tax reform is “pretty close,” helping lift spirits of investors who in recent weeks began to question the Trump reflation trade. Sentiment was also supported by robust growth in China at the start of 2017, with the economy growing by 6.9% (y/y) during the first quarter. Oil prices tanked this week on a large build in gasoline inventories in the U.S. while the dollar remained range bound - neither helped nor hurt by this week’s FOMC speeches from across the hawk-to-dove spectrum, with George,

The bid for safe assets is at least partly related to rising geopolitical tensions on the Korean Peninsula and in the Middle East. There is also plenty of anxiety over the French election, which has been further heightened after yesterday’s terrorist attack on French police. Polls suggest that a populist candidate, whether Le Pen or Mélenchon, is in good position to make it through to the second round but unlikely to clinch the runoff election. And even if so, there is still a long-road ahead before any referendum on the EU is even considered (see our French election preview).

Populist candidates have been boosted by weak economic growth and high unemployment in Europe. But, the economic data has been coming in better as of late. Reports this week confirmed the constructive data flow. Inflation advanced by a decent 1.5% (y/y) in March, while both consumer confidence and Eurozone PMIs surprised to the upside. At 56.7, the preliminary April composite PMI suggests growth carried into the second quarter after a good start to the year. Having said that, any survey data should be taken with a grain of salt, given the increasingly diverging performance of hard and soft indicators recently.

How exactly the convergence will manifest will be of utmost importance both for Fed policymakers and investors alike. Many among the FOMC expect to raise rates twice more this year. But, should the soft data weaken and converge closer to what the hard indicators are suggesting, two more hikes may not be an achievable target. On the other hand, should hard data trend higher, the Fed may be more anxious to raise rates, and may even begin the process of reducing their large balance sheet.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 14, 2017

HIGHLIGHTS OF THE WEEK

- Economic data this week remained consistent with the theme of an economy nearing full employment.

- Headlines were dominated this week by rising tensions with North Korea and the increased odds that the French Presidential elections could result in the victory of an anti-EU candidate.

- Comments from President Trump’s interview with the Wall St. Journal imply that tax reform is now secondary in importance to health care reform. Less scope for fiscal stimulus may imply a more gradual process of monetary policy normalization than previously anticipated.

[su_row][su_column size="1/2"]

[/su_column]

[su_column size="1/2"]

[/su_column][/su_row]

REFLATION TRADE FIZZLES AS GEOPOLITICAL RISKS RISE

There was little in terms of data this holiday week to move financial markets. February data from the job opening and labor turnover survey (JOLTS) showed an uptick in job openings, a downtick in new hires, and a reversal of previous month’s strength in the separations rate. Similarly, initial claims data for last week held near historic lows, further corroborating the theme of a healthy labor market. The key message permeating the data is that the job market is nearing full employment, yet more reason to look past last week’s disappointing payrolls number.

In addition to the labor market data, updates on small business sentiment and producer prices were released. The NFIB’s optimism index cooled for the second consecutive month, but small business remains highly optimistic by historical standards. Growth in core producer prices meanwhile, remains consistent with gradually rising price pressures.

Overall, there was little change in economic fundamentals this week to motivate the shifts in financial markets, which were drowned out by geopolitical developments and apparent shifts in domestic policy.

News out of North Korea dominated headlines early this week, with fears of an imminent confrontation between the U.S. and the pariah state contributing to a selloff in risk assets and a strong bid on safe havens such as Treasuries and gold. There was initially hope that the meeting between the Presidents of China and the U.S. last week would reduce tensions, but the subsequent bolstering of America’s military presence in the Korean peninsula has resulted in the opposite.

Markets also became concerned with the French Presidential election, which has seen a surge in another populist, anti-EU candidate in polls for the first round of elections set to take place in ten days. Jean-Luc Mélenchon, a far-left socialist candidate, is nipping at the heels of third placed Francois Fillon, and his momentous rise in the polls has raised the odds of a presidential runoff election in early May between two anti-EU candidates.

On this sid

These statements altogether suggest that stimulus from tax cuts is less likely in the near term. Less scope for fiscal stimulus may imply a more gradual process of monetary policy normalization than previously anticipated. Add into the mix elevated geopolitical uncertainty and it looks more and more like the reflation trade’s days are numbered.

Fotios Raptis, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.